Today we celebrate 10 yrs since founding @Lemonade_Inc 🎂 and 5 yrs since our IPO🥂. This double birthday begs a single question: did our AI strategy deliver—and will it lose or gain potency now that ‘everyone is doing AI’? Dive in →

https://t.co/5YN0Qhmbms

Lemonade’s Q1 results are 🔥. So much to share, where do I start?

First, get into the AI mood, click this, + volume ⏫

https://t.co/IDPCvrTHge (by @kidfrancescoli)

🚀10th consecutive quarter of accelerating IFP growth

🔥 Topline at $1.33 Billion (IFP +32%)

🔥 Revenue grew 71% to $258M

🔥 Gross Profit increased 159% to $100M

🔥 3.14M Customers

🔥 Adj. Free Cash Flow $17M

Lemonade Pet exploding!

✅ Surpassed $500M top line early in Q2

✅ #1 most searched pet insurance brand in the U.S.

✅ @lemonade_inc is now the 4th largest pet carrier in the U.S.

✅ AI-powered automation drives record claim handling efficiency (LAE: ~4%)

✅ Our data + tech edge lets us lower prices while boosting profitability

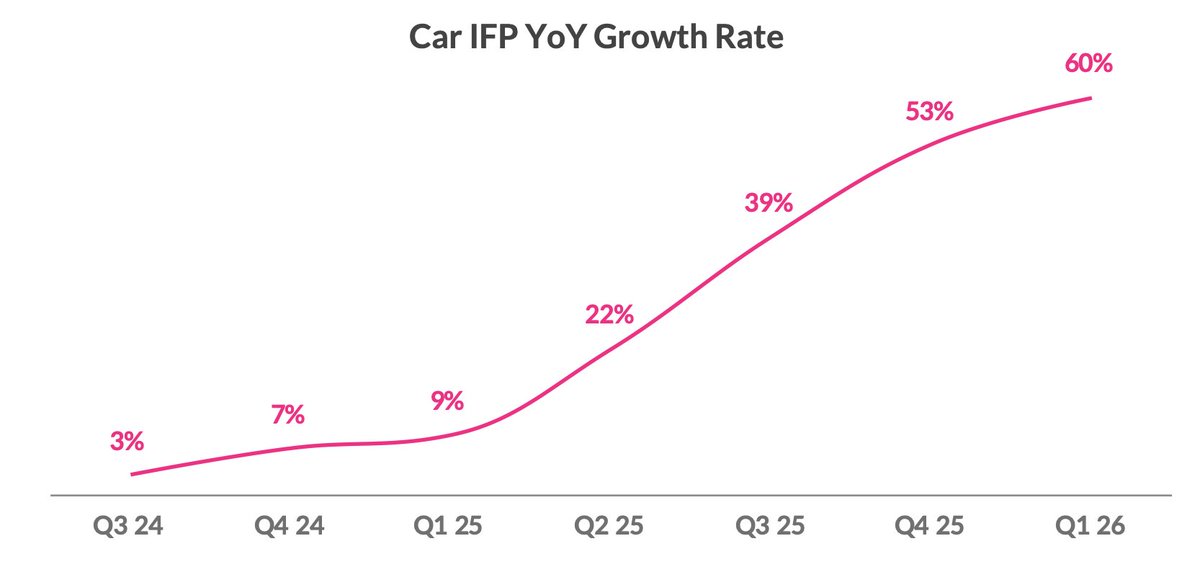

Car picking up speed

✅ Now at 60% YoY growth, $214M IFP

✅ Loss ratio improved to 74% (14 pts better YoY)

✅ Autonomous Car for @Tesla FSD conversion rate 70% higher than standard

And more...

↗️ Raising 2026 top & bottom line guidance

↗️ IFP per employee > $1M (3x improvement in 4 years)

↗️ Positive Adj. EBITDA in Q4

↗️ Investor Day in NYC November 17

$LMND One of the most misunderstood metrics in high growth insurance and fintech is LTV to CAC. For Lemonade, it is probably the clearest signal of whether the business model works long term, regardless of what GAAP net income shows this quarter. This took me a while to shift my mindset as I come from a rigid finance/accounting background.

LTV to CAC is straightforward. CAC is what you pay to acquire one customer through ads, referrals, or any other channel. LTV is the gross profit you expect from that customer over their entire relationship with you. When people cite a 3x ratio, they mean that for every $1 Lemonade spends to bring a customer in, it expects about $3 in lifetime gross profit back. You can think of it similiar as a ROIC calculation.

That 3x benchmark matters for three reasons. It provides a margin of safety because it covers the acquisition cost, variable servicing expenses, and still leaves room for fixed costs and eventual profit. Below 2x you are likely destroying capital as you scale, and above 5x you are probably under investing in growth. It also shows the unit economics are actually scalable. If Lemonade can consistently acquire a renter for $100 and that renter produces $300 of lifetime gross profit, the core structure works. Whether the whole company is profitable then becomes a choice about how fast to reinvest, not whether the model is viable. And it separates growth from profitability. Lemonade is not GAAP profitable today because it takes the gross profit from existing customers and reinvests it into acquiring more customers at that 3x ratio. If LTV to CAC were 1x, the losses would be structural. At 3x, the losses are temporary and tied to the growth rate. This is a similar to $TEM where they are reinvesting 2/3rds of gross profit back into the business with a good ROI.

A simple example makes this concrete. Say Lemonade spends $100 to acquire a renter. That renter stays three years on average and pays $180 per year in premium. After reinsurance and expected claims, Lemonade’s gross margin on the policy is 55 percent. Multiply $180 by three years by 55 percent and you get $297 of gross profit. Divide $297 by the $100 acquisition cost and you get an LTV to CAC of about 3.0.

So the company spends $100 today and gets $297 back over time. On a cash basis it looks unprofitable in year one, but by year three that cohort has returned three times the initial spend. Scale that to 100,000 renters and you have deployed $10 million to generate $30 million in future gross profit. GAAP accounting books the $10 million expense immediately and recognizes the $30 million profit slowly, which creates the J curve where losses come before scale.

I see all of the critics often point to net losses, but the better question is whether Lemonade is effectively buying dollar bills for thirty three cents. A durable 3x LTV to CAC says it is. As retention improves, cross sell into pet, car, and home increases, and CAC trends down with brand awareness, that 3x can expand. Profitability will show up when management decides to ease off growth and let the cohorts mature.

Put simply, LTV to CAC proves the machine works. GAAP net income proves when you decide to stop feeding it.

I urge all investors too look more into unit economics. In many instances, they help predict the future cash flows of the company.

Oppenheimer Review of $LMND

"the market is behaving irrationally"

*Translated from a Hebrew research report*

The Israeli technology-driven insurance company Lemonade (LMND) reported financial results last week that significantly exceeded expectations and reaffirmed its intention to achieve positive EBITDA later this year. In our view, Lemonade represents one of the best examples of an organization built on artificial intelligence from day one, and it is now beginning to reap the rewards of that successful strategy. We believe Lemonade has the potential to become one of the largest and most important insurance companies in the world, setting the gold standard for premium pricing, operational efficiency, and profitability. LMND shares are covered by Oppenheimer U.S. with a Perform rating and no specified price target.

Financial Performance

The company delivered impressive revenue growth of 53% YOY, reaching $228 million and surpassing market expectations of $218 million. Gross margin improved significantly to 49%, well above the 40% consensus forecast. Adjusted EBITDA improved by 81%, narrowing to a loss of just $4.6 million compared to expectations of a $12.8 million loss. In addition, adjusted earnings per share came in ahead of forecasts at a loss of $0.29 per share, representing a 31% improvement versus the same period last year.

Earnings Summary and Investor Call Highlights

The company reported dramatic improvement across all operating metrics. In-Force Premium (IFP) grew 31% to $1.237 billion, while average premium per customer increased 7% to $414, and total customers rose 23% to 2.984 million. The Gross Loss Ratio continued to improve at an unprecedented pace, reaching 52% in the current quarter compared to 62% in the previous quarter, bringing the trailing twelve-month figure to 64%.Particularly strong growth was recorded in the auto segment, where IFP surged 53% to $187 million alongside a sharp improvement in profitability. In Europe, IFP grew 150% to $60 million.Beyond accelerating top-line growth, the company reported stable Annual Dollar Retention of 85%, compared to 84% in the previous quarter and 87% in the prior-year quarter. This reflects management’s deliberate decision to prioritize underwriting quality and avoid renewing unprofitable policies. Management also demonstrated continued improvement in the LAE ratio (Loss Adjustment Expense, representing underwriting and claims handling costs), which declined to just 7%, compared to 9% in the comparable quarter and 11% in 2023. The company expects gross underwriting cost ratios to continue declining over the coming years, potentially outperforming leading insurers in the industry, which typically operate at LAE levels of 7%–9%.

Outlook

Looking ahead, Lemonade appears to be one of the primary beneficiaries of real-world AI deployment. Unlike traditional insurers, whose organizational structures were built decades ago on fragmented data systems that limit rapid innovation, Lemonade benefits from every improvement in computing power and large language models (LLMs). Its competitive advantage is expected to expand as it continues improving growth and operational efficiency across markets.

The company is also positioning itself as a pioneer in autonomous vehicle insurance, offering a product that integrates directly with Tesla vehicle data (via the FSD software), enabling pricing that can be up to 50% lower. This underscores Lemonade’s willingness and ability to adapt its technological models to the most advanced developments in the market.

Why Did the Stock Decline During Trading?

Following the earnings release—which substantially exceeded expectations for both the quarter and the full year—the stock initially opened approximately 15% higher but closed the session down around 6%. The following day, LMND shares fell an additional 7%, bringing the company’s market capitalization to approximately $4.3 billion, or an enterprise value of roughly $3.3 billion.We believe the sharp decline may have been driven by the CEO’s comments regarding plans to invest aggressively in R&D during the year (already incorporated into guidance), as well as broader negative sentiment toward software stocks—a category to which many investors continue to assign Lemonade, despite it not being a pure software company. In our view, the market is behaving irrationally and overlooking Lemonade’s structural advantage relative to competitors.

Conclusion

Lemonade continues to accelerate its performance and deliver impressive growth across all key metrics. We believe it is well positioned to become a leading player in autonomous vehicle insurance. The company plans to hold an Investor Day toward the end of 2026, where it will present its long-term strategic roadmap in greater detail—an event we are eagerly anticipating.

I know many are trying to explain the (so far) big drop today. It is pointless in my view. Algos, manipulation, tourists, or all of the above. Who knows? And it does not make any difference whatsoever.

The results were amazing. The potential energy keeps accumulating. The eventual rise will be great for investors.

And there is one big issue I don't see anybody talking about today: a big, BEAUTIFUL CHERRY on top of Lemonade's guidance for 2026.

Or at least that's what I see.

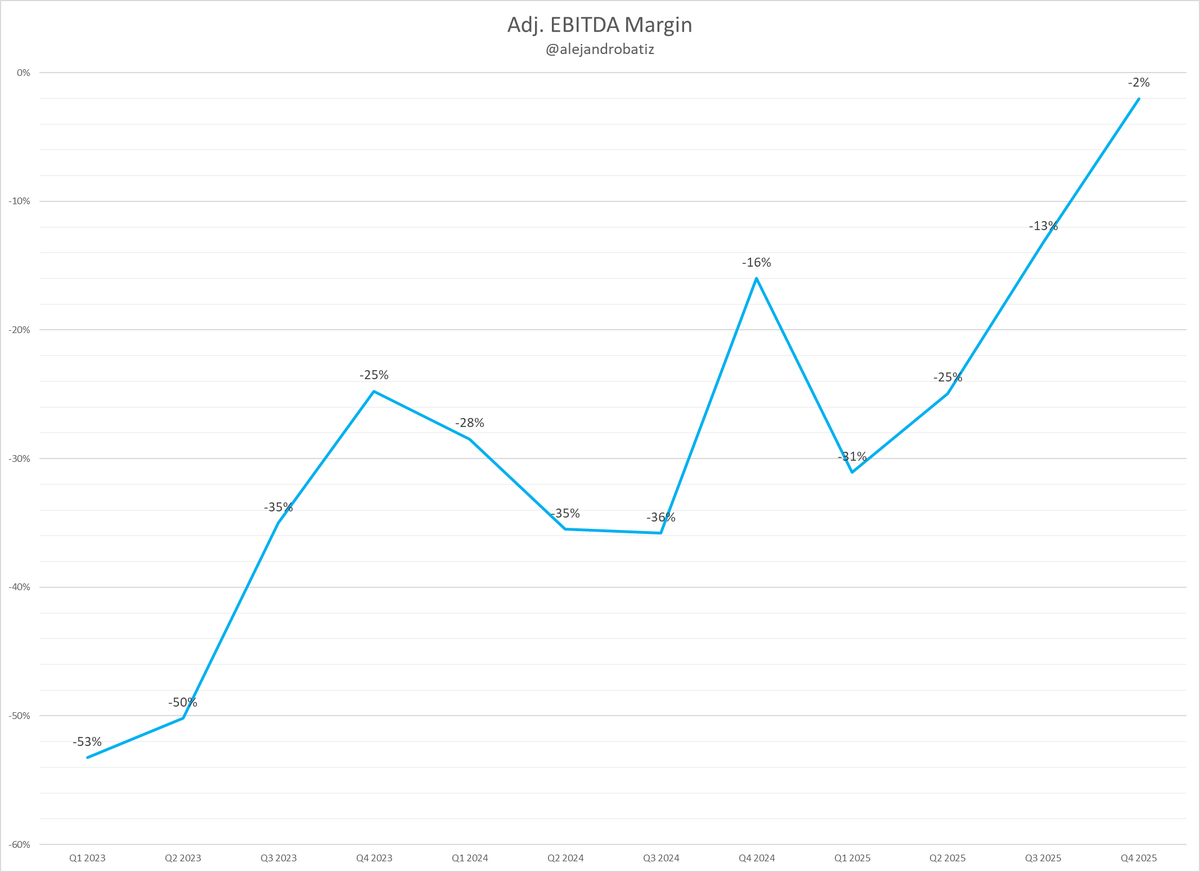

I have tried to adjust my model to reach -48 million in Adj. EBITDA for 2026 (as guided). Can't do it. Unless we get horrific CAT events in Q2/Q3 (LA-fires-kind of events). I think that is very unlikely. With a cleaner book and better AI-LTV models, very unlikely.

The best (or should I say worst) I can do is -20 for the year. But I can also see a realistic path for -1. We are so close to zero and revenue is growing so much that small changes have a big impact in the bottom line.

Take into account that we are just at -2% Adj. EBITDA margin!

With -20 Adj. EBITDA in Q1 (guidance is -22) and positive Q4 (I have it at +11, in a worst case), that leaves Q2 and Q3 for the difference.

Simple math -20+11=-9

That would mean -39 million for Q2 and Q3. In other words: Q1 (which is usually the worst month) equal to Q2 and Q3.

Even if we have worse GLRs in Q2 and Q3 than in Q1 (forecast), just with the operating leverage of the much higher revenue in each quarter and flattish Opex, we would get a much better Adj. EBITDA than in Q1. (Yes, I am taking into account the increase in growth spend.)

So I am calling it. Unless we get a monster, LA-fires-like CAT event this year, Adj. EBITDA for the year will fall between -1 and -20 million. A huge beat over guidance.

Also, with enough luck, if we get a stellar Q4 in 2026 like we just did for 2025, we might even be on the brink to the first EPS breakeven in Lemonade's history. It's a stretch, but not impossible.

Let's have a great 2026, regardless of Mr. Market's tantrums.

Presenting @Lemonade_Inc’s Q4 2025: our strongest quarter ever!

Recommended: Play this while reading- https://t.co/jHFp0vsNcn

Highlights (Y/Y)

🚀 9th consecutive quarter of accelerating growth

💵 $1.24 billion top line (+31%)

🔥 Revenue: up 53%

🔥 Gross profit: up 73%

🔥 Cash flow: generated $37m (adj. FCF)

🔥 ~3m customers

🔥 Adj. EBITDA loss improved 81%, now just -$5m

Car and Autonomous

✅ Lemonade Car grew 53%, now at $187m

✅ Loss ratio: 70% (TTM, down 23 points)

✅ Launched Autonomous Car Insurance for @tesla FSD (Supervised)

Europe

✅ Grew 150%

✅ 10th consecutive quarter of triple digit growth

✅ Loss ratio: 64%

AI Spotlight

✅ In the last 13 quarters- headcount shrunk 6%, while adding 1.2m customers

✅ 68% reduction in Pet cost-per-claim: from $44 in 2021, to $14 now

✅ Claims LAE at a record 6% (vs. 9% industry avg.)

More...

✅ Record breaking LMND gross loss ratio: now at 52%

✅ Growing cash (and investments) in the bank: $1.12B

Up next

⬆️ Guiding to 32% IFP growth in 2026

⬆️ 60%+ revenue growth

⬆️ Q4 2026 first positive adj. EBITDA quarter, 2027 - full positive year

⬆️ Announcing our upcoming investor day @ NYC, Nov ‘26.

Full details + financials: https://t.co/gDgJGSVuac

È uscito il numero di febbraio di #Tracce 🛎️

🔹L’editoriale: 👉 https://t.co/xgAoQmGwhh

🔸Abbonati: 👉 https://t.co/0ZR6sABmQ5

🔹Se sei abbonato leggi il numero online 👉 https://t.co/nHArb0bHex

The Most Important Discussion No One's Having

Here's a clip from my podcast with Daniel (Lemonade's CEO) about the impact AI has had on his business, and the impact it's having on society.

Full pod by Saturday.

$LMND

@wholemars I encourage you to do some digging. $LMND has a very similar retail analyst presence as $TSLA did back in the early days. I get a lot of the same vibes - super sharp and super bright retail analysts that have a much more fundamental grasp of the company's tech.

Meet the @Lemonade_Inc Timeline - One of our secret weapons, kept under covers… until now.

We started working on its foundations 10 years ago, before we wrote a single line of insurance code, and it has since become a core component of our Bionics Platform and Blender.

🧵>>

To paraphrase Voltaire, those who believe in absurdities can commit atrocities without ever thinking they’re doing anything wrong.

What would happen if there were an omnipotent AI that was trained to believe absurdities?

Grok is the only AI that is laser-focused on truth.

“Many insurance CEO want to sprinkle AI pixie dust on themselves” - @daschreiber CEO of $LMND on CEO of @AIGinsurance

Investors still do not fully understand the power of an AI native company like @Lemonade_Inc and how it compounds advantage.

https://t.co/LOPcEf4U1f

@CNBC

As I explained in the interview with @Gfilche:

- as risk per mile decreases from FSD,

- then premiums per mile will also decrease,

- then $LMND will be the best positioned to serve these customers because they can serve the “less loved” and lower premium Car customers in a highly efficient and autonomous way.

See my entire take on Car insurance in an autonomous world at 34:10 mark in video below:

https://t.co/fG8sgt3pBb

Scientists investigated the genome of one of the longest-living persons, Maria Branyas Morera, who died at age 117 in 2024

🟩They discovered that she had:

- Rare protective genetic variants in immune, metabolic, and neuroprotective pathways

- Exceptionally efficient lipid metabolism with low LDL and triglycerides, and high HDL

- Low systemic inflammation

- Strong immune system

- Diverse, youthful gut microbiome rich in Bifidobacterium (she ate 3 yogurts a day)

- Epigenetic age was much lower than chronological age

🟥However, she still had a few unfavorable features for aging:

- Severe telomere shortening (might have protected her against cancer)

- clonal hematopoiesis mutations linked to cancer risk

- Expansion of age-associated B cells (ABCs) expressing oncogene MYC

Full paper: https://t.co/wmHacve9BK

Still one of the most important slides from Investor Day.

▪️Currently at $850k of IFP/employee.

▪️Their goal is $4M/employee.

Four million per employee!