Don’t write off the dollar just yet.

After a >10% decline YTD (DXY from 110 to 98), COT data shows speculative USD short positions at record levels. Historically, such positioning (since 2008) has marked exhaustion points for downside — often preceding price stabilization or reversal.

A further dip can’t be ruled out (e.g., 2009), but most of the price adjustment appears priced in. A break above the March high at 104.7 — near the 200-day moving average — would confirm a trend shift. From a contrarian perspective, the probability of such a move is rising.

Source: @subutrade

By Daniel Belevich

U.S. dollar liquidity tightened in late April.

The Fed reduced its balance sheet by $17.7B, primarily through MBS runoffs. Foreign central banks also trimmed U.S. Treasury holdings by $16.4B.

The main pressure point was tax-related: the U.S. Treasury withdrew $101.5B from the system, raising its Fed account to $677.7B. An $87B outflow into the Fed’s reverse repo facility further drained liquidity.

As a result, bank reserves at the Fed fell by $208.6B to $3T, and SOFR rose to 4.41% by April 30 — signaling funding stress, though not disorder. $3T in reserves may be the threshold where market tension begins to build.

Looking ahead, near-term liquidity should ease as the Treasury draws down its cash balance (already down to $593B by May 1) with no room to issue debt until the ceiling is lifted.

The real test may come post-ceiling: rebuilding the Treasury’s cash target near $850B could pull bank reserves back toward $3T, maintaining pressure on short-term funding. If market depth remains weak, further issuance could force the Fed’s hand — but that’s a later story.

Source: FRED

By Daniel Belevich

UK FTSE 100 is overperforming S&P 500 Year-to-date.

Which structural differences make FTSE 100 more competitive in the current market state.

(A thread)

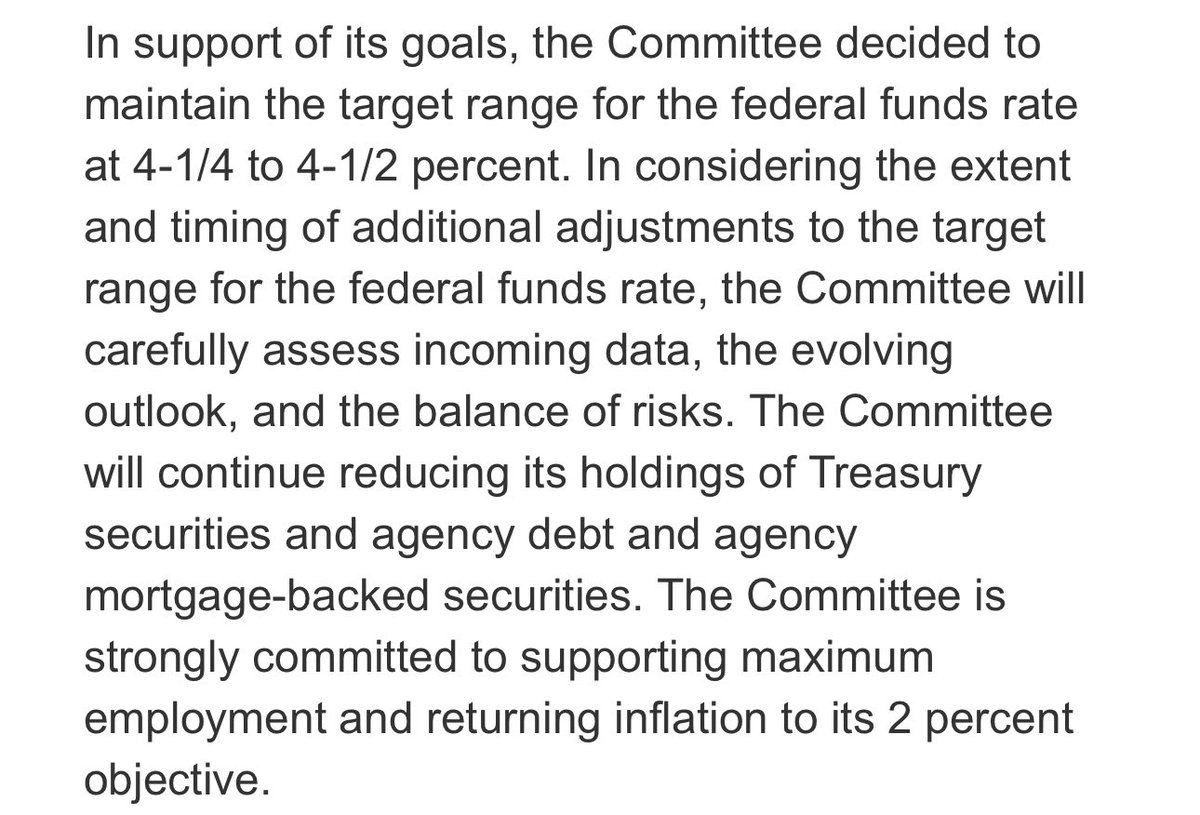

FOMC statement as scripted as usual, but what’s my view? No data = no triggers! Time to catch up with this blind rush and then… to flip flop wisely!

FOMC standing strong on 2% inflation thesis, which is fake, leads to disruption in new inflationary paradigm, much imminent under Trump47 era. Newly revised cost of capital and inflation frames are set to rise, but later.

The only point of control here - Summary of economic projections are not on the table this meeting. No data = no trigger for a significant move.

Every day till the next meeting (with Projections) is like being blind. Any adjustment to March projection can change dollar bias, now it will show its dependence only on capital flows and mostly US debt demand rebalancing.

In this case manipulative data on chinese deal can be the only driver besides those two factors until updated projections. Scenario for me? Dollar will become overbought in Q2 and next meeting’s projection will push it downward alongside yields.

Key metric here to observe is BE inflation (5/10y TiPS- 5/10y), any bounce is contrarian and blind with fake USD demand. UNTIL we have the data from FOMC on their 2% ride.

Nice risk opportunity to bet on USD with the whole market but main trick here - to flip flop right before the next FOMC due to inflationary projections (that can be manipulative although, but creating massive supply in mid-2025).

Source: Federal Reserve

by Nikita Chemodanov

U.S. trade deficit widened sharply in March, reaching a record $140.5B

Exports rose just 0.2% m/m to $278.5B, while imports jumped 4.4% to $419B — driven by pre-tariff stockpiling.

The 12-month deficit hit $1.11T, up 40% y/y. Over 80% of Q1 import growth came from just three categories:

Metals (incl. bullion): +$78B y/y (+852%)

Pharmaceuticals: +$53B y/y (+97%)

Computers & components: +$30B y/y (+66%)

Imports from the EU and Switzerland rose by $51B each — with Swiss inflows largely reflecting gold shipments into COMEX vaults.

In the Fed’s blackout period, Trump again called for rate cuts — now appealing directly to Board members rather than Powell, whom he criticized by name.

Source: Bloomberg

By Daniel Belevich

PBoC announces monetary stimulus to boost economic prospects, specifically inflation.

One may say that this is neutral, or slightly "bullish" for the economy since it clearly is the response for Trump's protectionism. Well, since Trump is clearly retreating from the trade war, and this variable is going to be somewhat cancelled. Let's see how its monetary stimulus may impact the markets, rest being equal.

Asian stock market seems to underappreciate the news. Heng Seng is up, and competes with US alternatives, however, when we look at autumn rally last year trigger with fiscal expansion, it was much more pronounced, and this is an understatement. CSI as well is not very optimistic.

So, one beneficiary may and should be, in being honest, Chinese stock market.

Well, stock market won't grow on its own, business activity, growing output and profits to reinvest. And it is not a secret that Commodities tend to correlate nicely with Chinese economy. Then, shall we see confirmation in PMI's and optimism in business reports, it should boost different commodities, from iron ore to silver. Interestingly, this happens at a time when ratio of Gold / (Any other metal) is on record highs (at least local). So maybe this change into Chinese monetary path may turn the tables for commodities.

And, let's go even more global. Michael Howell, author of Capital Wars notes how Chinese liquidity injections and GDP dynamics in general correlates with World economic momentum and global liquidity.

In turn, rising liquidity and growth, may benefit wide range of risk assets.

Stock market via increased growth expectations.

Gold & Crypto Majors via increased Global Liquidity.

This stimulus is surely underestinated at the moment, so it suggests that there is still room for short / mid - term volatility which can be utilised.

Source: Bloomberg

By Artem Gabak

“Bessent urges to act on debt limit by mid-July” is a headline, but what’s underneath? USD supply vs debt supply in terms of capital flows

Ray Dalio posted this month “Debt is a currency and currency is a debt”. Q2-Q3 ‘25 is more than suitable to observe this quote’s power.

Let’s take a look at Bessent’s rhetoric! We’ve come pretty short way from “Treasury has instruments to operate before the QE” to “government’s cash and extraordinary measures will be exhausted by August”. Anyway Republicans count on avoiding Dems demands for concessions in exchange for some votes. Debt maturity for the next 3 months: $70 bl in FRN, $55 bl in TIPS, 0 in bonds, $740 bl in notes. Interest payments not included, T-bills not included to watch it clearly enough.

That’s increased USD liquidity. Not critical, but reasonable enough to be mentioned when we watch Bessent’s speech. Sure, USD typically experiences minimal disruption from routine maturities in terms of balanced debt management, but what about supply in this exact period? Can this supply from maturity contribute to USD weakness or be a subject for reinvestment? Yields remain high enough historically to bet on the 2nd, but global USD confidence is under pressure on ForEx.

My view: it can poorly affect non-commercial traders positioning due to market expectations, but without pushing USD downwards. Those amounts either should be reinvested or…my scenario: streamed into stocks! Yes, locally that demand factor confirms my bullish bias on US stocks with momentum till the next FOMC or at least next US labor market data. I remain greedy for stocks mid-term with expected capital flows from bonds to stocks, pushing yields higher simultaneously with breakeven inflation. “Sell bonds, buy stocks” should be the one for the upcoming weeks.

Data: US Treasury

by Nikita Chemodanov

The U.S.–UK trade agreement, framed by the White House as a strategic win, offers limited substance. It lacks binding provisions, enforceable timelines, or measurable commitments. The announced $6B in U.S. revenue reflects pre-existing import volumes and adds no structural change. The projected $5B export boost is speculative, unsupported by contracts or regulatory shifts.

Key items — ethanol and beef export figures — are aspirational only. Aircraft orders (~$10B) are likely part of pre-planned fleet updates. Tech tax relief claims are inaccurate; UK digital tax policy remains unchanged. Tariff adjustments favor UK automakers: 100K vehicles now enter at 10% instead of 27.5%, with U.S. revenue falling by ~$1.3B.

Metal tariff relief remains unresolved. Net impact: the U.S. may collect $1–1.5B less in duties than before the deal, while gaining no secured access to new markets. In practical terms, the agreement is politically expedient but economically negligible — and structurally more beneficial to the UK.

By Daniel Belevich

A recent chart from SentimenTrader highlights a rare VIX pattern: since inception, there have only been four instances where the VIX closed above 50 and subsequently fell below 30 on a closing basis.

These four events occurred:

– Early 1988, following Black Monday

– Late 2002, after the dot-com crash

– May 2009, post-global financial crisis

– May 2020, after the initial COVID shock

In each case, the return of VIX below 30 coincided with a meaningful tradeable low in equities. While markets occasionally dipped further afterward, downside was relatively limited compared to the prior decline. Risk/reward dynamics historically shifted in favor of buyers.

On April 8, VIX closed above 50. Yesterday, it nearly closed below 30, narrowly missing what would’ve been the fifth signal of this kind.

Two questions now arise: Will the VIX eventually close below 30 to confirm the pattern? And if it does, will historical tendencies hold — or will today’s elevated geopolitical and policy risks alter the outcome?

🏎️ New Week, New Opportunities! 🚀

A new week means new possibilities and new heights to conquer. We hope you’re ready to take on the market and race toward success with Furmula!

🏁 Racers, take your positions - it’s go time!

Let’s make this week unforgettable. Together, we’re unstoppable 💥

#Furmula #GameFi $FURM #NFT

Staking is Closer Than Ever!

The wait is almost over - FURMULA Staking is just around the corner. Are you ready to fuel your $FURM for the ultimate rewards? 💰

Stake, earn, and take the lead in the race to the top! Passive income, exclusive bonuses, and a whole new way to dominate the Furmula ecosystem await.

This is your moment to gear up and get ahead. Let’s make history together!

#Furmula #Staking #GameFi $FURM

🏎️ You Have No Idea What’s Coming! 🚀

Our community doesn’t even realize the amount of features and functionality the Furmula game will have. This isn’t just a game — it’s a full ecosystem where players can interact, compete, and truly immerse themselves in the world of racing.

✨ Stay tuned as we start revealing more details about the project very soon. The future of GameFi is here, and it’s called Furmula. 💥

#Furmula $FURM #GameFi

🏎️ Furmula Staking is Coming soon! 🚀

The countdown is on to turbocharge your earnings! 💰 With Furmula Staking, you’ll be able to:

🔥 Earn passive rewards by staking $FURM

🔥 Stake your NFTs and maximize their potential

🔥 Secure long-term benefits as part of the Furmula ecosystem

Why just hold when you can hold AND earn? Staking launches next week — don’t miss out!

👉 Get ready to take your GameFi experience to the next level.

#Furmula $FURM #Staking #GameFi

$FURMULA seems like a good runner!

It is at a dip, $40M mcap right now after their presale raised 10k SOL.

It has been 5 days since launched and they are still at x4 for presale buyers. Seems like they have a diamond hand community!

https://t.co/Yez3DHCeHN

#Partner