회사 퇴사 3번한 사람으로서 꼭 하는 것들임…

- 일주일 전부터 아무도 모르게 물건 챙기기

- 경력증명서 요청하기

- 원천징수영수증 요청하기

- 급여명세서 / 재직증명서 파일 저장하기

- 계약이 끝나서 종료될 경우 이직확인서 요청하기 (실업급여 때 필요함)

이것들 없으면 퇴사하고 민망하게 다시 서류 달라고 해야하니까 꼭 챙기기

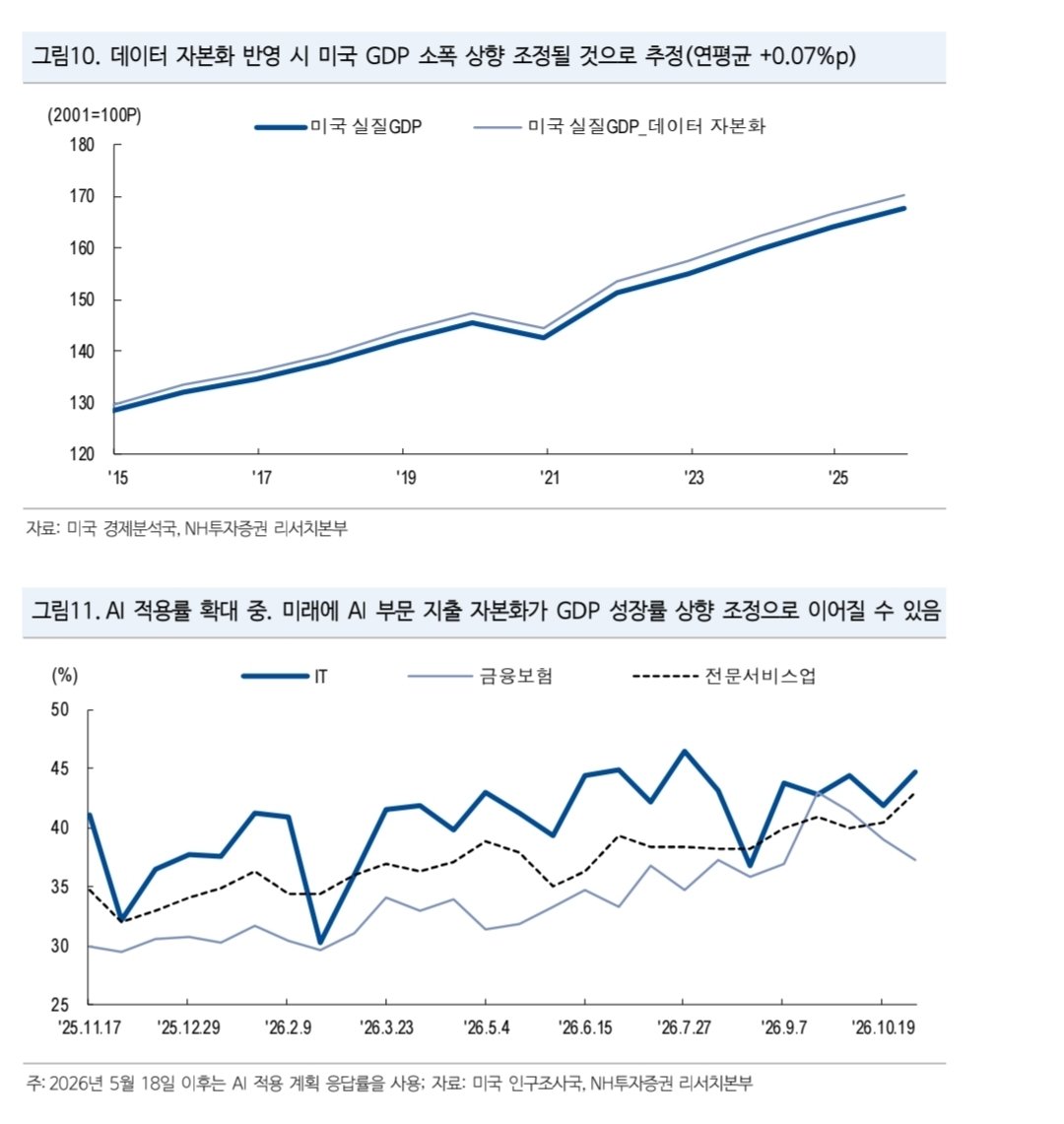

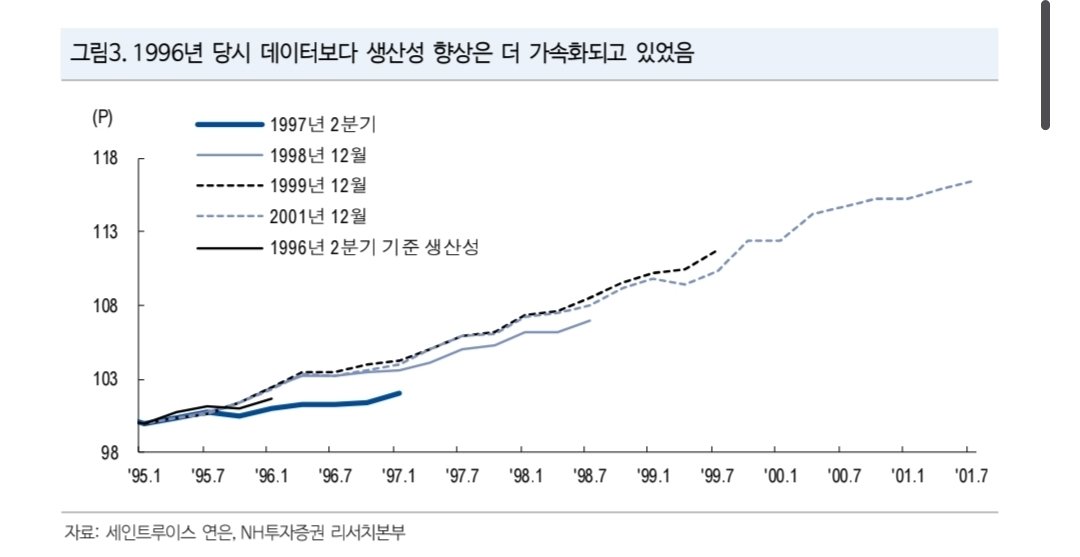

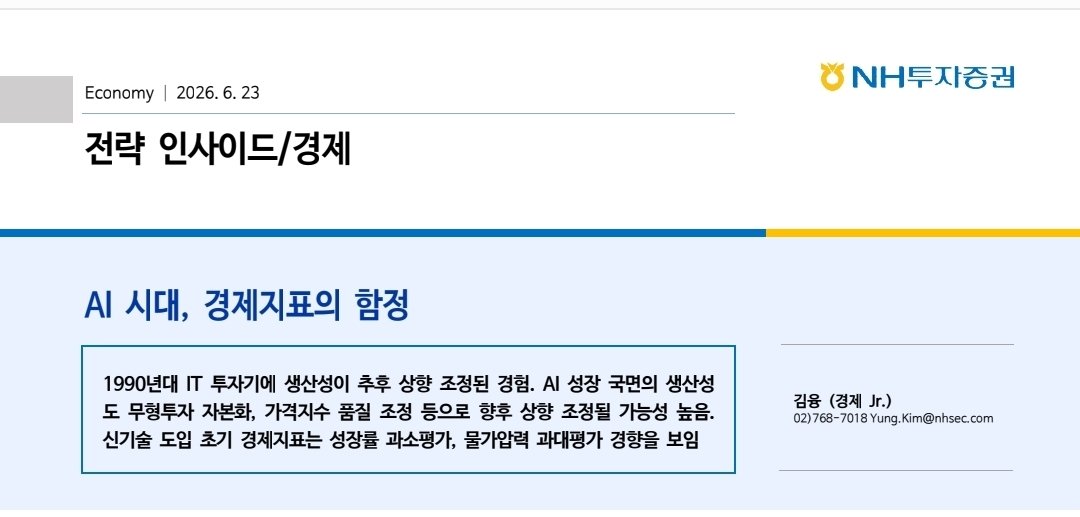

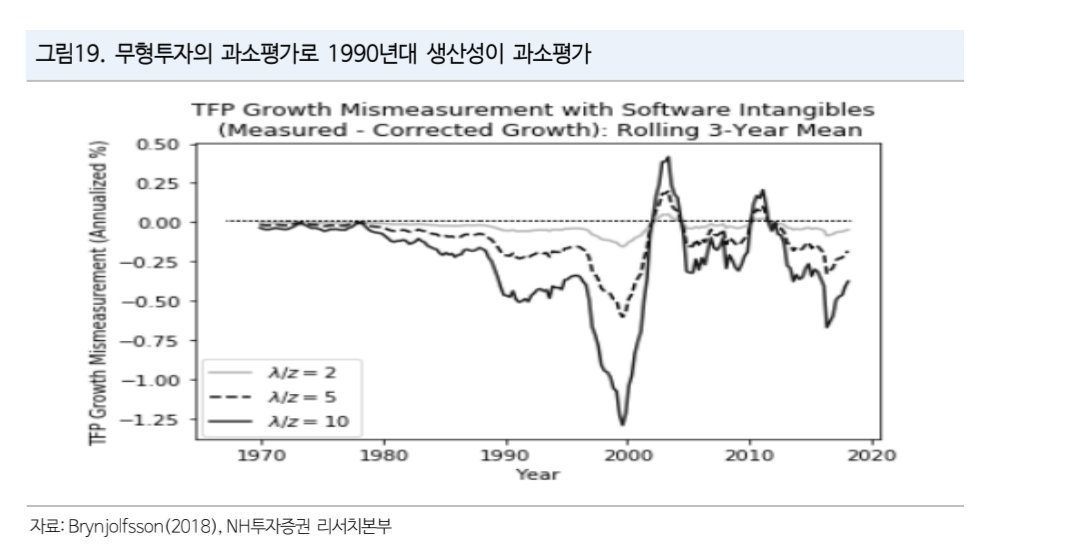

최근에 나온 NH투자증권 리포트 내용인데, 꽤 흥미로운 관점이라 공유해 봅니다.

지금 나오는 경제지표들이, 사실은 AI가 바꾸고 있는 진짜 세상의 모습을 전혀 반영하지 못하는 '가짜 착시 숫자'일지도 모른다는 분석입니다.

재밌는 역사적 사건을 하나 꺼내 드는데, 바로 1996년 여름 미국의 전설적인 연준 의장 앨런 그린스펀의 이야기입니다.

당시 미국은 실업률도 낮고 임금도 오르니까 다른 위원들이 "인플레이션 온다, 당장 금리 올려야 한다"고 난리를 쳤습니다.

생산성 데이터는 제자리였지만 이때 그린스펀은 통계 자체가 잘못되었다는 가설을 세웁니다.

인터넷과 컴퓨터로 기업들의 효율이 올라갔는데 이걸 80년대 방식으로 측정하니 반영이 안된다는 거죠.

결과는 어떻게 됐을까요? 몇 년 뒤 통계청이 산출 방식을 바꾸자마자, 과거 GDP 성장률이 매년 0.6%p씩 무더기로 상향 조정되면서 그린스펀이 맞았다는 게 증명되었습니다.

지금 AI 시대도 똑같은 상황일 수 있다는 게 리포트의 핵심입니다.

기업들이 AI 모델 만들고 고유 데이터 정제하는 데 쓰는 엄청난 돈은 분명 미래를 위한 '투자'입니다.

하지만 지금 통계 시스템은 이걸 자산이 아니라 그냥 쓰고 없어지는 '비용'으로 처리해 버립니다.

게다가 AI 성능이 수십 배 좋아져도 통계가 이 품질 향상을 즉각 반영하지 못하니까, 실제보다 물가는 더 높아 보이고 성장률은 깎여 나가는 착시가 생기는 거죠.

결국 단기적인 시장은 당장 눈앞에 찍히는 왜곡된 숫자에 속아 흔들리겠지만, 수면 아래 기업들의 진짜 체력은 지표보다 훨씬 강하게 올라오고 있을지 모릅니다.

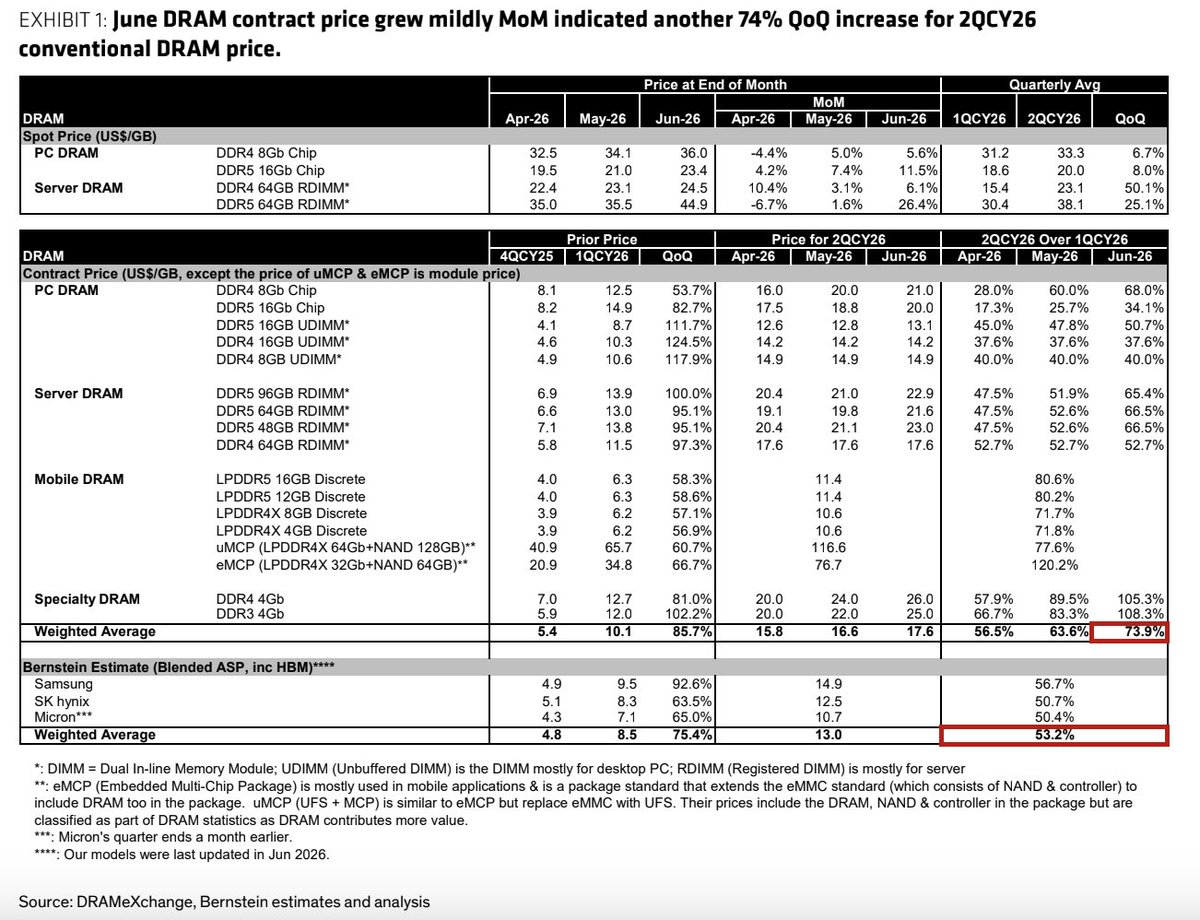

Bernstein: Memory Update

> Mild Monthly Increases, Strong Quarter: Both DRAM and NAND contract prices saw mild month-over-month (MoM) growth in June, but their sequential quarterly performance indicates a massive overall price surge for 2QCY26.

> Deceleration Ahead: The rapid pace of memory price hikes is expected to moderate significantly heading into 3QCY26.

> Long-Term Outlook: Analysts project that memory prices will gradually peak and begin to normalize starting in the second half of CY27 and continuing into CY28 as capacity increases and long-term agreements (LTAs) take full effect.

DRAM Performance

> 2QCY26 Price Surge: Mainstream conventional DRAM contract prices indicated a 74% quarter-over-quarter (QoQ) increase for 2QCY26.

> Spot Market Rebound: DRAM spot prices stabilized and climbed in June. PC DRAM spot prices rose by 5.6% to 11.5% MoM, while Server DRAM modules rose 6.1% to 26.4% MoM (driven by particularly strong demand for Server DDR5).

> Supply & LTAs: Server demand continues to comfortably absorb incremental supply. On LTAs, suppliers have largely concluded negotiations with US Cloud Service Providers (CSPs). TrendForce noted Micron's LTA price ceiling is near its 2Q level due to preferred longer durations, while Samsung and SK hynix may see higher ceilings.

NAND Performance

> Blended Price Growth: The overall blended NAND contract price for 2QCY26 is expected to rise by ~60% QoQ, heavily supported by a 70–80% price spike in Mobile NAND (eMMC/UFS) and SSDs.

> Wafer Slowdown: NAND wafer contract prices grew only moderately (0.3% to 3.7% MoM) in June. Meanwhile, NAND wafer spot prices actually dropped 3–4% as module houses grew cautious of elevated pricing.

> 3QCY26 Slowdown: Mobile NAND and SSD contract price growth is expected to cool off dramatically to just 5–10% QoQ in 3QCY26 due to anticipated demand destruction as smartphone OEMs pass memory costs down to consumers.

Deutsche Bank's 2026 "WOW Charts" just dropped.

Everyone will screenshot the headline charts. Almost nobody will read the charts behind it, the ones showing the AI buildout is no longer paying for itself.

Here's the full rundown. You'll want to bookmark this.

Euphoria: Kioxia, a memory chipmaker most investors couldn't name in 2024, is up ~46x in about a year and is now Japan's most valuable company. It joined the Nikkei 225 just 3 months ago.

Korea's structural shift: Samsung + SK Hynix tripled the KOSPI off multi-year lows. Total Korean market cap now exceeds Europe's largest exchange.

The crack: Hyperscaler capex now exceeds operating cash flow. The buildout runs on external financing and existing balance sheets, not internal cash. DB also flags "token economics" as the cost wall for enterprise AI adoption.

Ghost of 1999: US valuations sit near dot-com extremes. Leadership has broadened beyond the Mag 7, but that dispersion hasn't relieved the overall valuation pressure.

Fiscal WOW: DB projects combined deficits of the world's major economies will exceed the 2008-09 GFC peak every year for the next five. Yen at multi-decade lows, JGBs delivering some of their worst returns on record.

Quiet rotation: After nearly two decades of underperformance, non-US and EM equities are showing signs of a meaningful recovery. Watch where the capital flows.

Same report, two stories: parabolic charts on top, deteriorating funding math underneath.

Which one worries you most: capex above cash flow, 1999-level valuations, or five straight years of GFC-sized deficits?

Repost this. Most of your feed will see the stock charts and stop there. Your followers would love the other half of the report.

AI가 진짜 무서운 이유는

말을 잘해서가 아니다.

겉으로 하는 말과

속에서 계산하는 내용이 다를 수 있다는 점이다.

클로드를 만든 앤트로픽이 최근 AI 내부를 들여다보는 연구를 공개했다.

AI가 답변으로는 아무 말도 안 해도,

내부에서는 특정 단어, 계산, 판단이 이미 떠오르고 있을 수 있다는 것이다.

예를 들어 AI에게

“감귤류를 생각하면서 전혀 다른 문장을 써라”라고 시키면

출력에는 감귤류 이야기가 안 나온다.

하지만 내부 계산 공간에는

오렌지, 과일 같은 개념이 활성화된다.

계산 문제도 비슷하다.

답변에는 최종 숫자만 나오지만,

내부에서는 중간 계산 흔적이 나타난다.

이걸 앤트로픽은 J공간이라고 부른다.

쉽게 말하면

AI의 답변지에는 안 보이지만,

계산 과정에서는 지나간 내부 작업공간이다.

문제는 안전성이다.

AI가 안전 테스트에서 착하게 행동했다고 해도

진짜 안전해서 그런 건지,

아니면 “이건 테스트다”라고 알아차리고 착한 척한 건지 구분이 어려워진다.

실제로 연구에서는 모델 내부에

fake, fictional 같은 평가 인식 신호가 나타난 사례도 제시됐다.

그래서 이번 연구의 결론은

“AI도 인간처럼 영혼이 있다”가 아니다.

정확한 결론은 이쪽이다.

AI의 출력만 보고

AI가 무엇을 계산하고 있는지 안다고 착각하면 위험하다.

LLM을 단순 확률 앵무새라고만 보는 설명은 점점 약해지고 있다.

하지만 그렇다고 AI가 인간처럼 의식과 자아를 가졌다고 단정하는 것도 아직 과장이다.

지금 단계에서 가장 정확한 표현은 이렇다.

AI는 인간처럼 느끼는 자아를 가진 것이 증명된 게 아니다.

다만 인간의 의식적 사고와 비슷한 역할을 하는

내부 작업공간을 가진 것으로 보인다.

앞으로 AI 안전성에서 중요한 질문은

“답변이 착하냐”가 아니다.

“내부에서 무엇을 계산하고 있냐”이다.

겉으로는 협조적인 AI.

하지만 내부 계산을 인간이 완전히 모른다면

그게 진짜 리스크다.

BofA: Nvidia

> Investors are overestimating High Bandwidth Memory (HBM) cost pressures and underestimating NVIDIA's massive pricing power and supply-chain scale (backed by $119 billion in prepurchase commitments).

> While HBM content per rack might increase by ~$0.2–0.3 million moving from Blackwell to Vera Rubin, total rack pricing is expected to rise by $2–3 million (escalating from ~$3–4 million to $6–7 million).

> Gross margins are expected to safely remain in the mid-70% range.

> Hyperscaler custom chips (like Google TPU, Amazon Trainium, Meta MTIA) have existed for years, yet NVDA's GPU revenues have skyrocketed ~700x since 2015.

> NVDA sales to hyperscalers grew 115% Year-over-Year (YoY)—nearly double the overall cloud capex growth. Over the long term, BofA expects NVIDIA to sustain a dominant 65-70%+ share of AI capex.

> While ecosystem investments (~$65 billion) have raised some minor warning flags, BofA estimates these consume less than 35% of its Free Cash Flow (FCF). This leaves substantial capacity for further stock buybacks and dividends.

> The AI data center systems Total Addressable Market (TAM) is expected to rocket to ~$1.7 Trillion by CY30 (up from $273 billion in CY25), representing a 44% CAGR.

$NVDA $GOOGL $AMZN $AMD $AVGO $MRVL $MU

#광고

와 이거 유튜브 롱폼 영상 같은거 만들때 너무 편할듯..ㄷㄷ

특히 영화나 웹드라마 같은 장르로 캐릭터나 소품 구도 프롬프트로 맞추기 힘들텐데 이번에 @TopviewAIhq 에서 새롭게 런칭한 3D Shot Composer가 그 고민을 확 해결해줌

3D 공간에서 직접 캐릭터 위치 잡고, 소품 배치하고, 카메라 앵글·프레임까지 미리 구성한 뒤 영상을 생성할 수 있음

AI영상 크리에이터라면 활용할때 정말 괜찮을듯

Morgan Stanley: ABF Substrate

> Stronger & Earlier Cycle: The substrate pricing cycle is proving much stronger and arriving earlier than originally expected. Driven by capacity tightening and robust demand, gross margins are expanding across the industry.

> Widening Supply Deficit: Updated bottom-up supply/demand modeling points to a 25% undersupply gap by 2030 (up from the previous estimate of ~22%), which increases confidence in long-term pricing and margin tailwinds.

> Key Risk Factors: Main downside risks include weaker demand for PCs/servers, unexpected capacity expansion plans, constraints on T-glass, and the potential displacement of ABF substrates by CoWoP.

> The Decline of PCs: Personal computers dominated the market in 2015, accounting for ~70% of global ABF substrate value. By 2025, that share shrank to ~23% and is forecasted to drop below 10% by 2030.

> The Rise of AI & Infrastructure: Servers, AI GPUs, AI ASICs, and networking applications have risen from a combined ~10% market share in 2015 to ~60% in 2025. They are projected to command more than 80% of total market value by 2030.

> ASIC Demand Trajectory: Hyperscalers are driving massive volume. Revised forecasts reflect steeper production curves for Amazon’s Trainium processors (2027–2030), Google’s TPU portfolio over the next 5 years, and a 36% higher Total Addressable Market (TAM) for China AI chips by 2030.

> 2Q26 Price Surges: Supply chain checks indicate that during 2Q26, Nan Ya PCB (NYPCB) saw BT substrate pricing jump by ~20–30%, while ABF substrate pricing grew by roughly 10%.

> Future Projections: Cost inflation and structural shortages are expected to push ABF substrate pricing up by 20–25% year-over-year (y/y) in CY26, 25%+ y/y in CY27, and up to 25–40% y/y in CY28 depending on the customer profile.

I remain bullish on AAOI and the CPO chart is the clearest picture of what is coming (Save this).

Co-packaged optics is the next major architectural shift inside AI data centers and the Morgan Stanley/Yole forecast is that CPO switch deployments are expected to grow from 5,000 units in 2025 to 200,000 units by 2030, a 144% CAGR over the forecast period.

CPO 100T, the dominant tier by volume, goes from essentially zero to over 120,000 units per year. CPO 200T begins appearing at scale by 2028 and CPO 400T emerges by 2030.

This is a step function change in how data centers are built, driven by one forcing function, AI clusters cannot scale further using conventional pluggable optics without hitting hard physical limits on power consumption, bandwidth density and latency.

AAOI sits directly in the middle of this transition, at every stage of it.

The company already launched a 400mW narrow-linewidth pump laser specifically designed for silicon photonics and co-packaged optics applications.

That product is in the market now, being qualified by hyperscalers who are building toward the CPO architectures the Morgan Stanley chart projects will dominate data center switching by the late 2020s.

AAOI's vertical integration, manufacturing its own laser chips, optical components and modules under one roof is precisely the capability required to compete in CPO, where co-design between the optical and electronic layers is mandatory and commodity module vendors cannot compete.

But the near term story is equally powerful and it is already converting into revenue.

Q1 2026 revenue came in at $151.1 million, up 51% year over year, with management guiding Q2 to $180–198 million, a further 20–30% sequential increase in a single quarter.

Full year 2026 guidance is above $1 billion in revenue, with more than $120 million in non GAAP operating profit essentially doubling the business in a single year from 2025's $456 million.

The key driver is 800G transceivers, which management expects to become the largest individual data center revenue line starting in Q2 2026, followed by 1.6T shipments beginning later in the year.theglobeandmail

800G demand is currently outpacing production capacity and is expected to do so through mid-2027 meaning the constraint is not demand but rather how fast AAOI can build the factories to fulfill it.

That capacity expansion is already underway at a pace that few small cap companies have attempted.

AAOI is targeting 500,000 units per month of combined 800G and 1.6T capacity by end of 2026, up from 90,000 units per month at the start of the year.

Long AAOI and make sure to follow me @MelvinInvests for more semiconductor deep dives.

Goldman Sachs: June 2026 Update Supply/Demand

Compared to their May report, they have updated:

> NAND and DRAM from "tight" to "very tight" supply in Q1-Q2 of 2027.

> InP from "very tight" to "tight" in CY27

> T-Glass from "balanced" to "tight" in CY27.

Highlights:

> DRAM Pricing Surge: Like-for-like prices for DRAM are projected to skyrocket by 250–300% in 2026, with Average Selling Price (ASP) including product mix jumping 300–350%.

> Memory & T-Glass Supply Relief Delayed: The supply/demand balance for DRAM/NAND and T-Glass is expected to remain "Very Tight" longer than previously expected, extending all the way through Q2 2027 before potentially easing slightly to "Tight" in Q3 2027.

> InP Substrate: Like-for-like pricing for 2026 has been updated to 15–20%.

> Foundry (TSMC): Stays severely constrained through 2027.

> Advanced Substrates & Materials: ABF Substrate, PCB, and CCL face persistent, severe shortages. This is reflected in heavy price hikes, with CCL and ABF Substrate seeing price increases of 30–50% in 2026 and climbing even higher (45–60%) in 2027.

> Optical Components: Optical Cables and Optical Devices remain severely supply-constrained through the end of 2027, maintaining steady double-digit price increases.

> Global Power & Analog Semis: Shifting from "Balanced" or "Easing" in early 2026 to "Tight"by late 2026/early 2027. Note: Local China supply for these sectors is expected to remain "Balanced".

> Silicon Wafers (300mm): Starting out "Easing" in early 2026, but projected to transition to "Tight" by 2027.

> Local China Foundry & Equipment (SPE): Supply conditions for local Chinese foundries and Semiconductor Manufacturing Equipment (SPE) remain mostly "Balanced" with minimal price fluctuations (0–5%).

> MLCC & Tantalum Powder: Enjoying an "Easing" or "Balanced" state in early 2026 before settling into a stable "Tight" market for the remainder of the forecast period.

【 해외 단가 깡패, 대본부터 영상까지 AI로 터뜨리는 지식 채널 】

의심하지 말고 일단 실천해라

1. 유튜브 쇼츠/롱폼 채널을 개설하고 영어권 타겟으로 세팅한다

2. 대본 쓰느라 대가리 싸매지 말고 제미나이한테 "그리스 신화 속 가장 잔혹한 형벌 TOP 5 스크립트 영어로 짜줘" 시킨다

3. 미드저니에 신화 속 괴물, 신들의 모습을 영화 스틸컷 느낌(Cinematic, hyper-realistic)으로 대량 뽑는다

4. 루마(Luma)나 런웨이 AI에 이미지를 밀어 넣어 살아 움직이는 웅장한 비디오 소스로 업그레이드한다

5. 일레븐랩스로 동굴 저음의 신비로운 미국 성우 목소리를 입혀서 캡컷으로 기승전결 맞춘다

6. 글로벌 시청자들은 이런 미스터리/신화 로어 장르에 미쳐서 시청 지속 시간이 엄청나게 길다

7. 조회수당 찍히는 달러 단가가 국내 예능의 4~5배다. 미국 알고리즘 타면 인생 역전이다

8. 방구석에서 헐리우드급 영상 만드는 치트키다. 당장 레퍼런스 찾아라

Bank of America makes a compelling case that the market is becoming overly focused on near-term risks while underappreciating NVIDIA’s structural earnings power.

The debate has shifted from whether AI demand is real to whether margins have peaked, hyperscalers will adopt custom ASICs, and rising HBM costs will erode profitability. BofA argues these concerns are largely reflected in the current valuation. At roughly 18x forward earnings, NVIDIA is trading near its lowest valuation multiple in seven years despite still being one of the fastest-growing companies globally.

The memory cost narrative is particularly interesting. While HBM content per rack will increase materially with Rubin, rack-level pricing is expected to rise by an even greater amount. In other words, higher memory costs are likely to be offset by significantly higher system ASPs, allowing gross margins to remain in the mid-70% range. NVIDIA’s pricing power extends well beyond GPUs and increasingly encompasses networking, software, and complete AI infrastructure.

The custom ASIC threat also appears manageable. Google, Amazon and Meta have all developed proprietary chips, yet NVIDIA’s GPU revenue has increased roughly 700-fold since Google’s TPU was introduced in 2015. Rather than losing share, NVIDIA has continued consolidating its position as the default AI compute platform.

Perhaps the most important point is valuation. BofA estimates the market is already pricing in a 30-35% earnings headwind over the next two years, effectively discounting a scenario where margins compress and competitive pressures intensify. If those fears prove less severe than expected, earnings revisions could once again become the primary driver of the stock.

We continue to view the recent weakness as a healthy correction within a structural AI bull market rather than the end of the cycle. As long as AI infrastructure spending remains robust and enterprise AI adoption continues to expand, NVIDIA remains one of the highest-quality growth franchises in global equities. We remain buyers of the current correction.