Marketing Expert & MBA Grad. 🏴Welsh (north) in Manc UK. Tweets on MBA, marketing, brand, digital, lead gen, ABM, golf, football, Rammy, Manc & Wales

Mixed day to end week with Energy decisively lagging; sector now in worst spot YTD and MTD, falling behind traditional defensives (which were all higher today) … large-cap growth indexes fell most today while small caps held up relatively well; NASDAQ still leads YTD

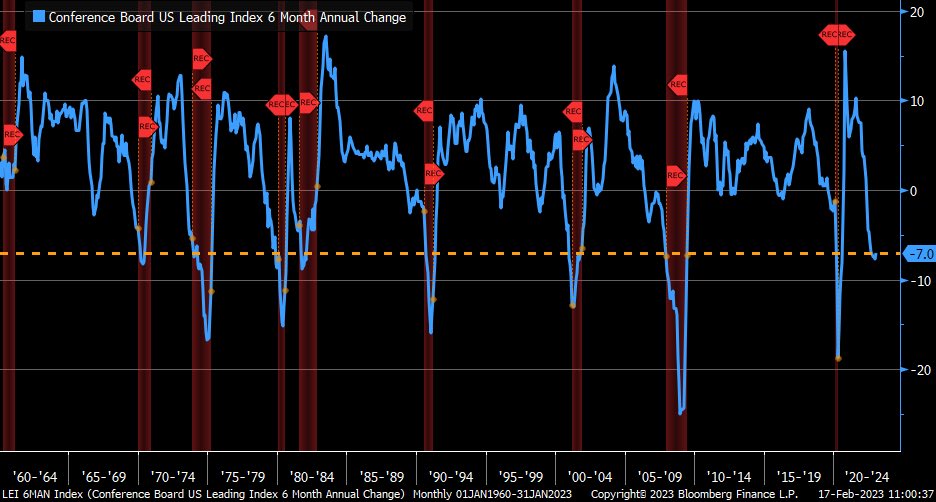

6-month annualized % change in Leading Economic Index from @Conferenceboard remains in negative territory (consistent with prior recessions) but hooked slightly higher in January to -7% (recent low was -7.7%)

Year/year % decline in Leading Economic Index from @ConferenceBoard remains negative (and consistent with prior recessions) but hooked up slightly to -5.9% in January

Leading Economic Index from @Conferenceboard fell in January by -0.3% m/m vs. -0.3% est. & -0.8% prior; relatively mild decline relative to recent months

Personal consumption goods component of January PPI saw small reversal in 3-month annualized % rate … fortunately, nowhere near surge during acute inflation phase

Deep sea (orange), air (white), and truck (blue) freight components of PPI are off their highs … rail (purple) continues to edge higher but rate of change has slowed over past year

Since market’s October low, Industrials (blue) sector has been leading, but now Tech (orange) has caught up … both are essentially tied with 20% gains

[Past performance is no guarantee of future results

NASDAQ 100’s selloffs from end of 2021 into middle of 2022 were consistent with increase in forward EPS (orange); yet now, forward EPS have fallen considerably as index has attempted to claw back losses

[Past performance is no guarantee of future results]

![LizAnnSonders's tweet photo. NASDAQ 100’s selloffs from end of 2021 into middle of 2022 were consistent with increase in forward EPS (orange); yet now, forward EPS have fallen considerably as index has attempted to claw back losses

[Past performance is no guarantee of future results] https://t.co/5sAUy11Aba](https://pbs.twimg.com/media/FpKxToOWAAA-e-7.jpg)