Prometheus Institutional🔥

Prometheus is built on deep research into how the economy & markets work. We translate that into systematic programs across global markets. We offer an ever-evolving, forward-looking, signal-based view of the global macroeconomic landscape.

Link ⬇️

"Our synthesis of these drivers suggests that most of the evidence continues to support equities in the near term. Macro regime probabilities, business cycle conditions, earnings momentum, and short-term regime dynamics all point to support for equities. On the downside, the level of earnings expectations growth is perhaps too stretched. This potentiates a material sell-off if we start to see a reversal of the broad set of supportive conditions. There is a moderately high bar set to achieve this reversal. As such, long equity exposure with tight risk control will likely remain well supported."

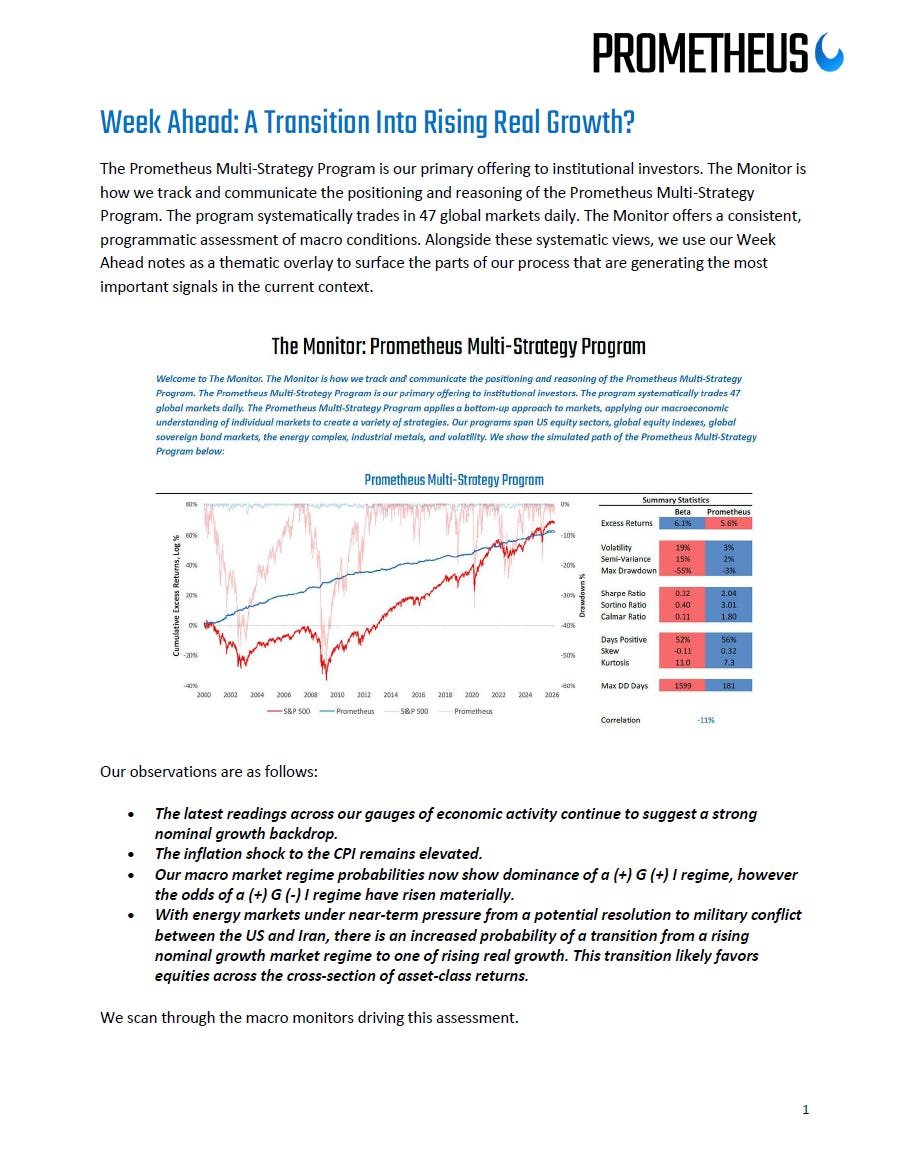

A Transition Into Rising Real Growth?

We use our Week Ahead notes to surface the parts of our process that are generating the most important signals in the current context.

We see signs of a regime shift.

@AahanPrometheus joined @practicalquant for a quick wrap on the current macro backdrop.

They discussed:

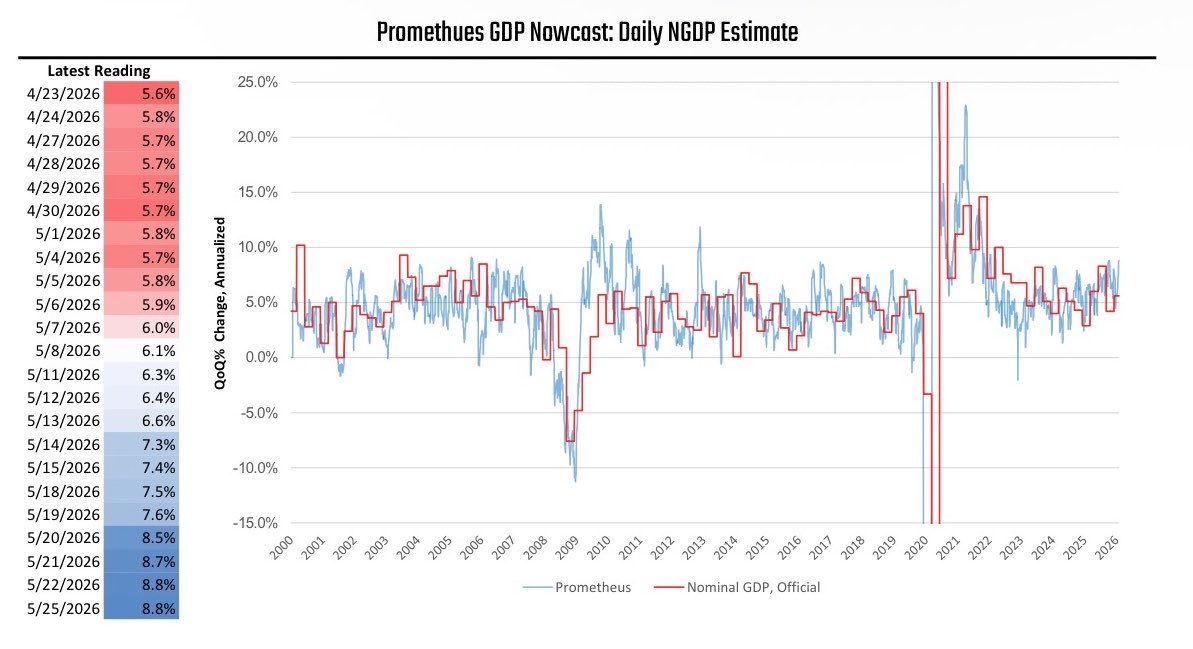

— Nominal GDP

— Inflaiton

— Macro Regirm Probabilities

— Oil Regimes

Give it a listen 🎧

The AI trade has carried this market through war, inflation risk, and valuation concerns.

But there could be some problems on the horizon for it.

On the latest Last Call, @CultishCreative may or may not drink a large glass of vodka while we break it all down.

https://t.co/Au0ffSt2FL

☑️ @EpsilonTheory on the political backlash building against AI

☑️ @AahanPrometheus on inflation, oil and the macro data

☑️ @spotgamma on extreme call buying and options market froth

☑️ Why rising earnings estimates have kept the market moving higher

☑️ What the SpaceX IPO means for all of this

Motor vehicle spending is directly reflected in GDP through consumer motor vehicle purchases and business investment in motor vehicles.

Motor vehicle sales remain soft versus the one-year prior:

Today was a disinflationary day in macro markets.

But it does not reset the pressure on the Fed to hike interest rates.

Nominal activity is still running too hot for comfort

Federal government spending continues to contribute to nominal GDP consistently. Fiscal spending continues to support the current macro backdrop, but remains far from its primary marginal driver.

Real income breadth has softened materially as the inflation shock has taken hold.

Not enough to bring trend rates of growth into contraction, but enough to cause a material dent.

Month In Macro: Into A Hiking Cycle?

The surge in global energy prices, coupled with resilient US nominal activity, is likely to put material pressure on the Fed to begin a monetary policy hiking cycle.

28 pages of granular macro. Free.

Link ⬇️

Information and intellectual property investment continues to rise dramatically, with no corresponding rise in the associated employment of the sector.

This is stimulative to GDP growth AND corporate profits:

Systematically verified ✅

— During a business cycle expansion, buy the dip in equities (mean reversion)

— During a business cycle contraction, short into weakness (trend)

Using our ex-ante business cycle classification.

Month In Macro 🔥🔥🔥

28 pages of comprehensive and rigorous macro research.

100% free.

Everything you need to know about the economy and what it means for Treasury markets.

Link ⬇️

Into A Hiking Cycle?

The surge in global energy prices, coupled with resilient US nominal activity, is likely to put material pressure on the Fed to begin a monetary policy hiking cycle.

Our latest Month In Macro, over the course of 28 pages of research, explains why.

Into A Hiking Cycle?

The surge in global energy prices, coupled with resilient US nominal activity, is likely to put material pressure on the Fed to begin a monetary policy hiking cycle.

Our latest Month In Macro, over the course of 28 pages of research, explains why.

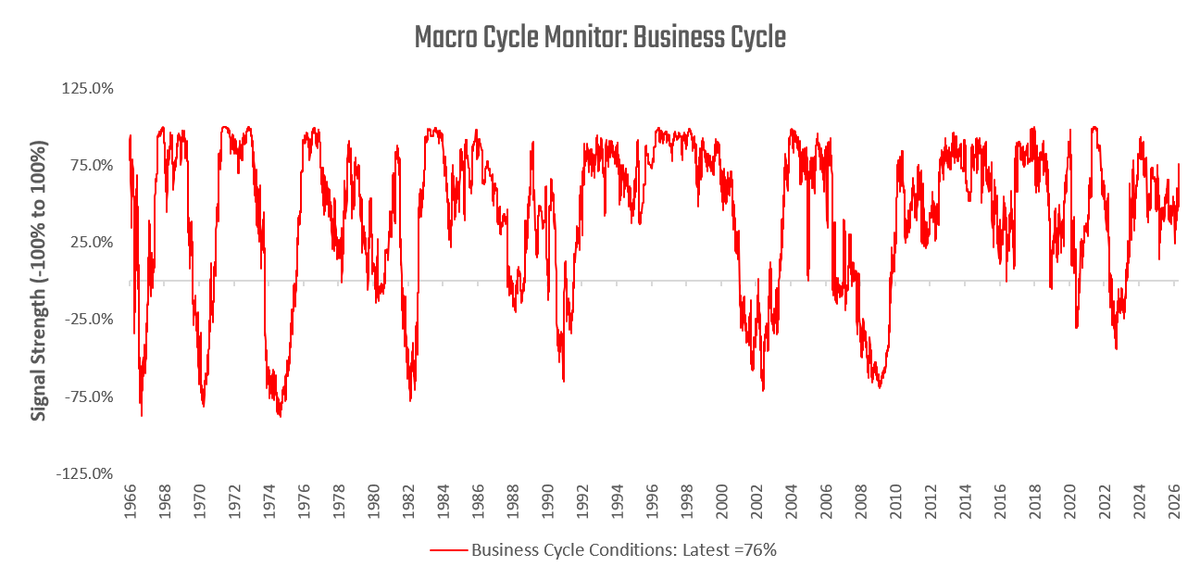

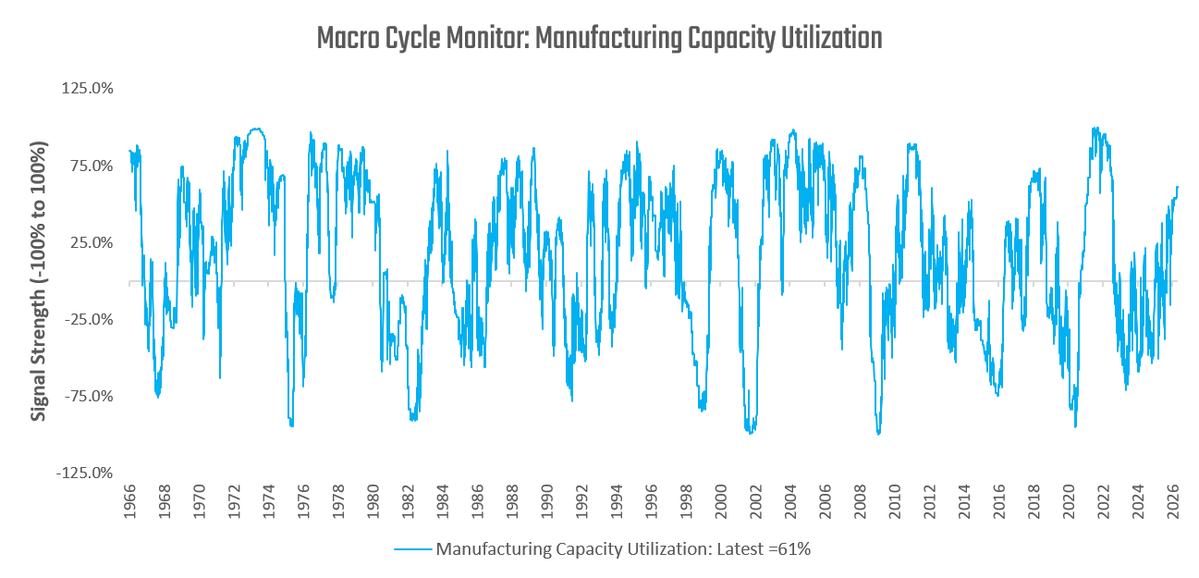

The business cycle continues to show an economy expanding, pressing up against capacity constraints, creating hiking-cycle pressures on the Fed.

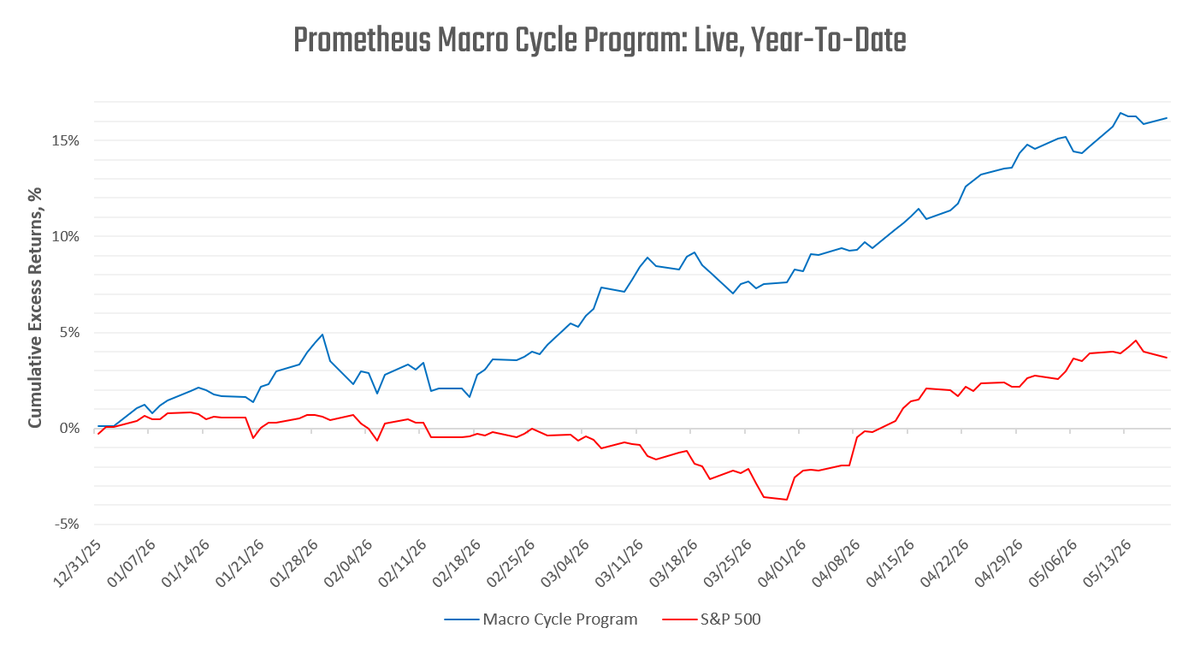

Our Macro Cycle Program continues to allocate in line with these views and is once again within range of new All-Time Highs.

Oil isn’t the only reason that interest rates are up. US labor data positive surprises are at a 2-year high. Feels like Groundhog Day with higher rates weighing on equities again, bringing out the loudest of bond bears.