You can turn Opus 4.8 into Fable 5 for Free

And you have 2 days before the window closes.

July 7 is the last day Fable 5 is included in paid plans.

Fom july 8 it's usage credits: $10/$50 per m/tok, 2x Opus, the most expensive model on Anthropic's price list.

What to do?

Make Fable 5 write a skill for Opus 4.8: its reasoning patterns, verification habits, task decomposition, extracted into one SKILL.md your daily model inherits.

The prompt is one line:

"write a SKILL.md for Opus 4.8 capturing how you decompose hard tasks, verify your own work, and decide what to do next".

While the window's still open, 6 more ways to squeeze it:

1/ Give it your hardest problems. it's built for work that takes humans days - easy tasks waste the window.

2/ One big brief instead of 20 messages: full context, constraints, edge cases in message one - it decomposes the rest.

3/ Effort on high by default: xhigh only for genuinely brutal runs - high on Fable often beats xhigh on older models.

4/ One .md memory file that accumulates learnings across sessions.

5/ Make it verify its own work before reporting - kills the fake "done".

6/ delete your opus-era prompts - over-detailed instructions actively hurt Fable 5.

Access to Fable expires on the 7th, but the files it wrote don't.

Everyone else will figure this out on July 8, but you have until the 7th.

Once you've done that, be sure to read the article about Loop engineering, because you'll be working with it extensively after July 7:

We’ve had lots of questions from our investor community looking for thoughts on OUSD, and so I thought I’d share my direct views here for anyone.

Stablecoin networks are platform and network effect businesses that are established over a long period of time, tend towards winner-take-most market structures, and resemble other internet platform utility markets. There are several layers that drive this.

First, stablecoin networks effectively act as public protocols and software layers on the internet and their network strength is a matter of the number and range of applications and services that integrate to the network. Every time a developer or service provider integrates to the network, it brings more network effects. This attracts more developers and adds more utility and more network effects. This then drives demand for the digital currency itself, which then reinforces these network effects through liquidity network effects.

We have realized this at a massive scale with the USDC network today — thousands upon thousands of services integrate with our network, which in turn provides immense utility not just to each application, but to users as a whole who benefit massively from the reach and interoperability that exists. This drives user and developer preference further. We’ve invested in building that ecosystem over nearly a decade, and now it’s accelerating as mainstream institutions come onto the network, connecting their customers and users.

We add to that utility by building software stacks that further expand and strengthen the network — protocols like CCTP and Gateway, which promote interoperability, safety and liquidity around the world. This expands the target surface area for app builders and developers, making it easy for them to tap into the liquidity and network effects that already exist. We are now seeing that stack get pulled into all kinds of chains, permissioned L2s, networks being built by governments, and so much more.

The second layer is that of liquidity network effects. This is fundamental. Liquidity begets liquidity. For a stablecoin to achieve scale and utility, it needs to be highly liquid, both on a primary basis (e.g., through all the major financial market centers in the world, with world class direct banking liquidity) and on a secondary basis both by being available and tradeable for retail and institutional clients in every geography and against every fiat instrument in the world. People who want to access and move value need to be able to easily get in and out of that digital currency. Here, we’ve invested nearly a decade in building out that liquidity, and it is now entrenched in exchanges, DeFI venues, and with PSPs, payments firms, regional exchanges, and so many others. Establishing these liquidity network effects also involves building global regulatory infrastructure and ensuring that the stablecoin is available under various regimes around the world. Today, USDC is in the top 3 most liquid digital assets in the world, and it falls off sharply after that. BTC, USDT and USDC have extraordinary liquidity. The closest other dollar stables are like 10x smaller and that liquidity tends to be concentrated in promotional books in a single exchange, whereas USDC liquidity is dispersed widely across dozens and dozens of surfaces. Building this liquidity has been a nearly decade-long task that we continue.

A third layer of network strength comes from the deep integration with the policy and regulatory environment — in many cases, years of effort to build licensing (e.g., USDC is the only large global stablecoin currently available in all of Europe or Japan), and more regimes for stablecoins are coming online, with Circle leading the way in ensuring that USDC is officially recognized, registered, licensed and accepted in the most important markets in the world. On the back of this is the work of building global banking, reserve management and treasury and liquidity management that can operate this on a nearly 24/7 basis in markets and banking systems globally. This globalization effort is a massive investment that we have made over the years.

All of these investments by Circle and our global ecosystem of thousands of partners have delivered the net result of providing the world’s most trusted and available digital dollar infrastructure—a utility that any user, developer, or business can freely and easily tap into. And we do not intend to slow down.

All of this compounds and shows in the numbers. In Q1 2026, according to third-party analysts (Artemis) who track stablecoin adoption, USDC handled nearly $30T in onchain transactions, representing 80% of all dollar stablecoin transactions on blockchains. USDT handled the remaining 20% of transactions. All of the combined remaining dollar stablecoins handled a total of 0% of transactions (i.e., < 0.5%). While other stablecoins may have some circulation, most of that is through promotions and incentives, the actual usage is extremely limited—because of the extremely limited liquidity and network utility that exists for these coins.

But my thoughts on the competitive landscape are not just about the strength of our network—there are also considerations around any new initiative.

Several perspectives and positioning have been shared about how something like OUSD improves on something like USDC.

1) Free mint and burn. The argument suggests that existing stablecoins charge burn fees, and payments firms should not need to pay these (despite the fact that the entire payment industry is built on small bps fees on various ingress and egress points on their networks). There are structural market realities built around the fact that some stablecoins impose very large redemption fees and have limited redemption facilities – the impact of this is that stablecoins with strong redemption facilities, good liquidity and no fees become the offramp for their competitor stablecoins. It may seem easy to say one will offer unlimited and free redeems, however market reality likely forces other behavior. This can be addressed – and is addressed by Circle – through contractual mechanisms vs. a blanket fee exemption.

2) Everybody wins and shares. While this sounds good in principle, the reality of the market and market opportunity is quite different. Today, Circle shares the majority of its income with its distribution partners, and we continue to lean hard into expanding those partnerships with leading companies across every sector of the market. However, we also retain significant income that allows us to invest in the massive market infrastructure that makes this such a powerful and valuable utility for the world to build on. Giving away all the income is a recipe for starving an infrastructure, systematically underinvesting and ensuring that your platform will remain limited in scope.

Furthermore, Circle believes that the future stablecoin market is likely several orders of magnitude larger than it is today. We’re actively bringing partners into the USDC ecosystem through a diverse and growing set of partnership models that span our work with exchanges, custodians, payments firms, asset issuers and more. We are excited to continue to build with a “big tent mentality” where the entire ecosystem can grow value together.

3) A consortium where everybody has a voice. Perhaps I have a cynical view, but the track record of consortium products achieving scale, P/M Fit or even basic product agility is absolutely dismal, and while there are examples of financial consortia that operate utilities, they are predictably slow moving. Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation and competitiveness. They also typically, out of their own self-interest, starve the consortium itself on an operating basis. We actually tried this in the early days of USDC, and even with a very small group, ran into endless challenges and complexity. Smaller, tighter strategic collaborations and commercial partnership arrangements with product and platform builders that can drive forward independently will almost always outcompete large consortiums. But oftentimes when these get formed, everyone feels like they should put their logo on the list, kiss the ring, and make noise about openness. But typically those same firms will turn to their operating units and make the best decisions for their customers, which often means partnering with the market leader and building durable win-win partnerships.

There’s also been a bunch of commentary on Circle's partnership with Coinbase and what this all means. Our stablecoin partnership with Coinbase remains as strong as ever, and I think we both see that enormous opportunity ahead to expand the USDC network.

A final comment: Circle remains committed to supporting a wide range of different products and infrastructures, even when we might compete with different aspects of those partners’ products in other areas of our business. With OUSD, we work closely with many of the founding members, and we expect that those same members will remain large USDC partners and customers. At the same time, as Circle has diversified our product and platform stack, expanding across Arc, CCTP, CPN, StableFX, Agent Stack and many other areas, we continue to expand the partnerships and collaboration with many other stablecoin issuers — dozens of them — to help them launch on Arc, leverage our interoperability infrastructure, get supported in our Wallets and become settlement and FX options on CPN and StableFX.

We are huge believers in growth in the stablecoin ecosystem and welcome OUSD as a new member of the community!

USDC는 죽지 않을 가능성이 높습니다.

하지만 써클이 누리던 “땅짚고 헤엄치기 같은 이익”은 확실히 압박받을 수 있다고 봅니다.

Reuters 보도 기준으로 Open Standard에는 Visa, Mastercard, Coinbase 등을 포함해 140개 이상 기업이 참여하고 있고, Open USD는 2026년 하반기 출시 예정입니다.

이건 “또 하나의 USDC같은 스테이블코인”이라기보다, Stripe, Visa, Mastercard, BlackRock, BNY, Coinbase, Google, Shopify, DoorDash 같은 기업들이 같은 스테이블코인을 놓고 결제망·정산망·수익 배분 구조를 같이 만들려는 시도에 가깝습니다.

저는 여기서 Circle과 USDC의 진짜 리스크가 보인다고 생각합니다.

USDC가 죽느냐 아니냐의 문제가 아닙니다.

USDC가 앞으로도 예전처럼 시장에서 높은 프리미엄을 받을 수 있느냐의 문제입니다.

스테이블코인 시장을 USDT 점유율, USDC 점유율, OUSD 발행량 같은 통계로만 보면 조금 섣부르다 생각합니다. 진짜 중요한 의문은 따로 있습니다.

누가 준비금 수익을 가져가는가와 누가 유통망을 가지고 있는가.

써클은 지금까지 꽤 좋은 포지션에 있었습니다. USDC라는 규제를 통한 현물로 교환이 가능한 달러 스테이블코인을 만들고, 거래소와 DeFi와 기관 시장에 넓게 분포시켰습니다. USDC가 많이 발행될수록 준비금이 커지고, 그 준비금에서 나오는 ���자 수익이 써클의 핵심 BM이 된것이 사실이죠

일단 금리가 높은 시기에는 이게 정말 좋은 사업입니다.

조금 거칠게 말하자면 돈은 사용자와 파트너가 입금해서 스테이블코인을 민팅하고 달러로 백킹된 신뢰와 발행 구조를 만든 써클이 세뇨리지를 가져가는 모델입니다. 그래서 시장이 써클에 프리미엄을 준 것입니다.

그런데 OpenUSD는 이 구조에 의문을 던진것으로 보입니다.

아니 정확하게는 기업들과 파트너사들이 의문을 던진것이 맞습니다.

왜 저 막대한 이익을 발행사가 다 먹어야 하지? 왜 실제 매매를 하는 기업들은 준비금 수익을 못 가져가지?

왜 Visa, Stripe, Shopify, Coinbase 같은 유통망이 남의 스테이블코인을 그냥 써줘야 하는건가?

Open Standard 공식 발표를 보면 OpenUSD는 무료 발행·상환, 준비금 수익 공유, 파트너 공동 거버넌스를 핵심 원칙으로 말하��� 있는데. 준비금 수익에서 작은 운영 수수료를 제외한 나머지를 파트너에게 돌려��는 구조입니다.

본인들이 기존의 막대한 스테이블코인의 이익 배분 시스템을 바꾸겠다는 말입니다.

기존 USDC나 USDT는 발행사가 준비금 수익을 상당 부분 가져가는 구조에 가까웠습니다. 반면 OpenUSD는 “실제로 유통을 만드는 기업들에게 수익을 나눠주겠다”는 구호를 내걸고 시스템을 바꾼다는 이야기를 하고 있습니다. 아마 이 부분에서는 Circle의 가장 맛있는 BM이 공격받기 시작한 것이라고 보면 됩니다.

하지만 저는 USDC가 바로 죽는다고 보지는 않습니다.

오히려 USDC는 쉽게 죽기 어렵습니다. 이미 DeFi와 거래소와 기관 시장에 깊게 유동성이 들어가 있고, 유동성도 크고, 브랜드 가치에 대한 신뢰도 있습니다. 크립토 네이티브 시장에서는 여전히 USDC가 달러처럼 쓰이는 곳이 많습니다.

특히 DeFi에서는 더 좋은 조건의 스테이블코인이 나왔다고 바로 갈아타�� 어렵습니다. 담보 구조, 풀 유동성, 대출 시장, 청산 엔진, 거래소 지원, 브릿지, 온체인 회계가 전부 얽혀 있는 복잡한 시스템으로 설계했기 때문���니다.

이건 은행 앱 바꾸듯이 바꾸기 쉽지는 않습니다.

그래서 USDC는 완전히 죽기보다 “기본 유동성의 공급 인프라”로 남을 가능성이 높다고 봅니다. 다만 그 위에서 써클이 예전만큼 높은 마진을 유지할 수 있느냐는 완전히 다른 문제로 봅니다.

저는 여기가 진짜 리스크라고 봅니다.

OpenUSD가 성공하면 기업 고객들은 스테이블코인 발행에 관한 협상력을 갖게 됩니다.

우리가 유통을 만들어주는데 수익을 나눠달라.

민팅과 리딤 수수료를 낮춰달라.

로드맵에 우리 요구를 반영해달라.

아니면 우리도 OpenUSD 같은 컨소시엄으로 간다 등등등

이렇게 되면 써클의 문제는 점유율이 아니라 테이크레이트가 됩니다.

USDC가 계속 많이 쓰여도, 그 USDC에서 써클이 가져가는 몫이 줄어들 수 있습니다. 시장에서 써클 주가가 폭락한 이유도 여기에 가깝다고 생각합니다. OpenUSD가 내일 USDC를 죽일 거라서가 아니라, 써클의 가장 매력적인 수익 구조가 공격받기 시작했기 때문입니다.

이건 카드사와 비슷합니다.

당연히 카드망이 하루아침에 죽지는 않습니다. 하지만 대형 가맹점, ��테크, 빅테크, 은행이 힘을 합쳐 수수료를 낮추라고 압박하면 카드사의 이익률은 서서히 달라질거라 생각합니다. 네트워크는 남아도, 그 네트워크에서 가져가는 이익은 줄어든다는 거죠

USDC도 비슷한 길을 갈 수 있습니다.

살아남지만 예전보다는 덜 맛있는 사업이 되는 것입니다.

OpenUSD의 출신도 흥미롭습니다. Open Standard의 창립 CEO Zach Abrams는 Bridge 공동창업자 겸 CEO입니다. Bridge는 원래 스테이블코인으로 돈을 보내고, 받고, 보관하고, 발행하게 해주는 API 인프라 회사였고, Stripe가 2024년 10월 11억 달러에 인수하기로 했으며 2025년 2월 인수를 완료했다고 보도됐습니다.

이 말은 OpenUSD가 갑자기 하늘에서 떨어진 프로젝트가 아니라는 뜻입니다.

Stripe·Bridge 계열의 스테이블코인 인프라 DNA 위에, 글로벌 결제사·은행·테크·크립토 기업이 붙은 컨소시엄형 스테이���코인에 가깝다고 생각하면 됩니다.

파트너 구성을 보면 방향이 더 명확합니다.

결제 쪽에는 Visa, Mastercard, American Express, Stripe, Adyen, Fiserv, Worldline, Marqeta, MoneyGram, Western Union, Remitly 등이 있습니다. 금융기관 쪽에는 BlackRock, BNY, Standard Chartered, BBVA, DBS, U.S. Bank, Mizuho, Shinhan, Kakao Bank, KB Kookmin Card, Woori Card, Hana Card, Hyundai Card, Samsung Card 등이 들어갑니다.

테크·커머스 쪽에는 Google, Samsung Electronics, Shopify, DoorDash, Grab, Rakuten, Mercado Libre 등이 있고, 크립토 쪽에는 Coinbase, Base, Solana, OKX, Bybit, https://t.co/GeeaY7VsR0, Ripple, Fireblocks, Gemini, MetaMask, Aave, Morpho, Ledger, MoonPay, Anchorage, Bridge, Stellar, Polygon, Aptos Labs 등이 있습니다.

이 조합은 거래소와 디파이 거래 시장만 노리는 그림은 아닌것으로 보여집니다.

쇼핑, 플랫폼 수익 지급, 크로스보더 판매자 정산, 앱 내 결제, 송금, 온체인 유동성, 에이전트 결제까지 전부 엮여있는 기업들이 있는 철저한 기업 이익 친화적인 구조입니다.

그래서 OpenUSD의 진짜 필살기는 스테이블코인 기술 자체가 ��니라 기업들의 유통망입니다.

스테이블코인은 결국 달러가 뒷받침된 토큰입니다. 기술적으로만 보면 완전히 새롭다고 말하기 어렵습니다만 누가 그 달러를 쓰게 만드느냐는 완전히 다른 문제입니다.

다만 OpenUSD도 아직 검증된 것은 아닙니다.

파트너 명단이 크다고 실제 거래량이 바로 생기는 건 아닙니다. 기업들은 이름을 올리고도 천천히 OUSD를 테스트할 수 있습니다. 준비금 구조, 발행 법인, 감사·증명 방식, 수탁기관, 체인별 유동성, 스마트컨트랙트 안정성, 국가별 규제, 회계 처리, 세금 처리까지 설계하고 실제 유통하는데 꽤 시간이 걸릴 수 있습니다.

특히 준비금 구조는 우리는 유심히 지켜 봐야 합니다.

Open Standard는 준비금이 미국 규제 요건에 맞춰 주요 금융기관에 보관된다고 설명하지만, 구체적인 준비금 구성, 수탁기관, 증명 보고 주기, 발행 법인 구조는 출시 전 기준으로 아직 완전히 공개된 상태는 ��닙니다.

그래서 “Open USD가 USDC를 바로 대체한다”고 말하는 건 섣부르다 생각합니다.

하지만 “써클의 이익률에 압박을 줄 수 있다”는 말은 꽤 현실적으로 들리는데요

제 결론은 대충 이렇습니다.

USDC는 죽지 않을 가능성이 높지만 써클의 세뇨리지 비즈니스는 예전만큼 독점적이지 않을 수 있다.

P.S : 투자추천은 아닙니다. 투자는 본인 판단으로!

I genuinely don't understand why everyone isn't using this yet.

Andrej Karpathy, OpenAI co-founder, posted a simple idea that went massively viral:

Stop using AI to write code.

Use it to build a second brain.

You point Claude Code at a folder. Drop in any source: an article, a transcript, a PDF.

Claude reads it, links it, files it into a living wiki of everything you know.

It compounds like interest. The more you feed it, the smarter it gets.

Here's the whole thing:

1) Install Obsidian

2) Create a vault

3) Open it in Claude Code

4) Paste Karpathy's wiki idea and tell Claude to build it

5) Claude makes three folders:

- raw (for sources)

- wiki (for its pages)

- CLAUDE. md (that runs it)

6) Drop any source into raw and say: "ingest this"

7) Ask questions across everything, forever

Five minutes to set up and you never start from a blank chat again.

Full step by step guide below.

$CRCL --- Per latest tracking data from Wall Street investment bank Mizuho, since the start of 2026, USDC has captured 64% of the regulated stablecoin market share in adjusted on-chain volume. This marks the first time since 2019 that USDC’s actual adjusted transaction volume has fully overtaken industry leader Tether (USDT). Institutional and corporate payments are rapidly ditching opaque USDT in favor of fully regulated USDC.

The latest Q1 13F institutional holdings filings show that while the share price has dipped, traditional finance giants are aggressively accumulating. Morgan Stanley boosted its position by a massive 241% in a single quarter, adding over 3.5 MILLION shares. Jane Street and Cathie Wood’s ARK Invest also loaded up heavily on dips through the recent selloff.

1. Massive Risk-Free Reserve Interest Income

As long as U.S. benchmark rates stay elevated, Circle generates over $2 BILLION a year in risk-free interest income from its Treasury reserves without lifting a finger. That’s why its fundamentals are stronger than the vast majority of tech stocks.USDC’s issuance model is simple: Users send Circle $1, Circle issues 1 USDC, and parks that $1 in U.S. Treasuries or Fed deposits.Per latest earnings, USDC circulation is now over $75 BILLION.

2. CPN And Arc Chain Full Monetization Kickoff

Historically Circle relied solely on interest income. But since launching the Circle Payments Network (CPN) in 2025 and its institution-focused Arc Layer-1 blockchain (already running on testnet with 100+ giants including Goldman Sachs, Deutsche Bank, Visa, Mastercard), its mainnet will officially launch in 2026. Circle is transitioning from a "reserve management firm" to an "on-chain Visa", generating high-margin software revenue via cross-border payment fees and subscription services.

3. Native "Agentic AI Fiat" For The AI Era

This is the core megatrend narrative Circle CEO Jeremy Allaire highlights most, and the source of Wall Street’s premium valuation: The future of Silicon Valley belongs to AI Agents. When AI Agents conduct high-frequency, micro, autonomous commercial transactions, they can’t open traditional bank accounts. Highly programmable, U.S. regulatory-compliant USDC is the natural native fiat for settlement between AI Agents.

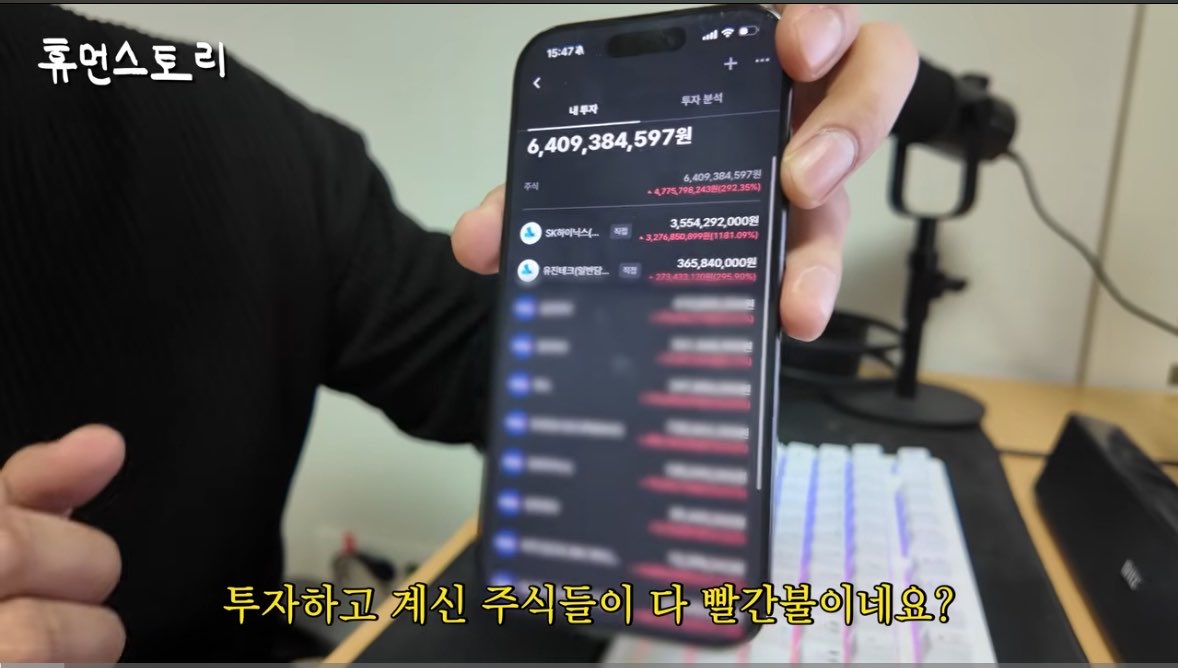

하이닉스 2,871주 들고있는 김해산 자산가

종잣돈 1억을 모아서 22년 SK 하이닉스 평단 100,000원에 매수하고 돈이 들어올 때마다 매수 했음. 단 한번도 판적이 없다고 함.

3개월 전에 떨어질 때 주식 담보대출까지 받아서 투자하고 반대매매 될수도 있다고 증권사에서 전���까지 옴. 그래도 우직하게 안팔고 버텼음. 영상을 찍은게 한달 전이니 지금은 순자산이 80억 넘는다고 함..ㄷㄷ

경제적인 자유를 이루기 위해서 그가 필요했던건 1억 종잣돈과 하이닉스.

Monica Lam (Stanford Professor):

"AI writes shallow reports for one reason, you ask it ONE question. Our method asks dozens, like a journalist, and the same chatbot starts writing articles 25% better organized than top AI."

paper presented at a leading AI research conference, her Stanford lab (OVAL) unveiled STORM - a method already used by 70,000+ people to generate Wikipedia-grade, fully-cited articles on topics it has never seen.

the secret formula: 6–8 expert perspectives + cited expert interviews + ruthless outline + grounded section-by-section writing + blind-spot red team = a report you can actually trust.

watch the full breakdown to copy all 5 prompts into Claude.

save this post so the formula is ready when you need it.

Nasihat Warren Buffett untuk anak-anaknya:

1. Beli rumah cepat, mobil murah saja.

2. Barang jangka panjang, pilih yang mahal dan awet.

3. Jangan kerja dengan keluarga atau teman.

4. Rajin olahraga.

5. Lebih baik buka bisnis sendiri.

6. Kuasai public speaking.

7. Biasakan mandiri dan sendiri.

8. Pilih kerja dengan komisi, bukan gaji tetap.

어제 어머니와 이마트 가면서

이런 저런 이야기를 나눴다.

어머니는 매형을 엄청 좋아하신다.

그도 그럴것이,

매형이 불려준 부모님 자산만 수억이니

그럴수 밖에.

매형이 굴리는 주식이 수백억 인것 같다며,

정말 대단하다고 입에 침이 마르게 칭찬을 하신다.

내가 아는것만,

스x 40-50억. 테슬라, 로켓랩, 새틀로직,

하닉, 삼전, 인텔,마이크론, 키오시아 등등 종목당 최소 10억 비중 큰것들은 수십억.

(더 많지만 누구나 아는 종목을 많이 들고계심)

며칠전 매형이랑 통화하며

이런저런 이야기를 했다.

매형이 의사이신데,

이제 노동으로 돈벌고 자산 불리는 시대는 지난것 같다신다.

소비층이 얇아지다보니 개인사업자(의사도 전문직개인사업자라고 하심)도 힘들어지고,

일반 직장인이 평생 벌면 얼마나 벌겠냐며(하닉회사원은 예외라 하심ㅋㅋ)

투자하지 않으면 뒤쳐지는 시대가 왔다 하신다.

현금을 들고있는 것만으로도 자산이 녹으니

주식,부동산,금,코인,달러등.

원화 이외에 뭐라도 사야한다고.

그리고 요즘 은행이든 투자사든

돈 빌리기가 엄청 까다로워지고 힘들어졌다는 말과 함께.

지금 빌릴 수 있는 돈이 있다면

부담가지 않고, 능���되는 한에서

최대치를 땡겨 놓으라고 하심.

안 쓰더라도 일단 빌려서 2-3%나오는 cma에 넣어 두더라도 빌려두라고.

(앞으로 돈빌리기 더 힘들어진다고 보시는것 같음)

본인이 빌리러 다녀보니 조건을 엄청 까다롭게 본다고.

그리고 매형이 이제는 돈의 개념이 사라지신것 같다고 하셨는데,

이미 본인이 버는것 보다 훨씬 초과해서 지출을 함에도,

그 비용보다 자산 늘어나는 속도가 훨씬 크다보니. 더이상 돈이 돈으로 보이지 않고 숫자들 장난 같다고..(부럽다.)

아마 본인만 그런게 아닐거라고

앞으로 자산의 격차는 더 벌어지고. 불평등은 심화될거라고..

물론 매형은 금수저(?)이시긴 하시다.

주식말고도 부동산 자산도 수백억이라서.

그런데

믿기 힘들겠지만

저렇게 불어난 주식의

처음 시작은

테슬라 몇천만원에서 시작하셨다.

그게 저렇게 불어난거���. 중간중간 추가 자금 투입도 하셨겠지만.

매번 나한테 이야기하신다.

"나도 처음에 몇천에서 시작했어."

투자를 두려워하지말라고.

투자하지 않아서 뒤쳐지는게 더 두렵다고.

수억씩 수익보는 사람들을 보며

조급해하지말고 본인이 해온던 투자를

하라신다.

내가 봐온 매형은 그렇게 투자해 오셨다

특별한 투자법이나 기법이 있는것도 아니다. 꾸준히 투자하다보니 수백퍼 수익보는게 생겼고, 그걸 반복해오셨다.

남들보다 더 벌고싶다고, 기간을 단축시키고 싶다고,

레버리지 상품을 투자하시지도 않으셨다.

급등주나 테마주를 투자하지도 않으셨다.

조급하면 실수를 한다.

이 바닥에서 실수 한번은 복구하기 힘든 결과를 주는게 흔하다.

실수하지 말자.

조급한건 너때문이다. 테슬라.ㅋㅋ

15년전 사회초년생으로 돌아간다면 꼭 실행하고 싶은 것.

동시에 실행하지 못해서 정말 아쉬운 것.

1.

ISA, 연금저축, IRP 3종 계좌 개설

2.

연금저축한도 1500만원, IRP한도 300만원 설정

3.

100만원을 아래와 같이 매달 자동이체로 입금

- ISA 25만원

- 연금저축 50만원

- IRP 25만원

4.

국내 상장된 미국증시 추종 ETF중에서 아래를 섞어서 매수

- 미국 S&P 500 (VOO)

- 미국나스닥 100 (QQQ)

- 미국배당다우존스 (SCHD)

*IRP는 혼합형 비중 25%(ex, SOL 미국배당국채혼합)

5.

보너스나 목돈이 들어오면 ISA에 입금

만약 ISA한도 연간 2천을 넘겼다면 연금저축 한도 채우기

6.

ISA 3년 만기가 되면 연금저축으로 이전

7.

30년 반복

이렇게하면 절세를 최대로 누리면서 자산이 복리로 구른다. 일찍 시작할 수록 훗날 1년마다 어마어마한 수익이 돌아온다.

보수적인 SCHD형을 예로 들어도 30년 구르면 35억이다.

시간선호는 투자에 있어서 필수요건이다.

어릴 때 이런걸 가르쳐주는 사람이 아무도 없었다.

참 아쉬운 일이다..

국립현대미술관에는 무료로 사용 가능한 라운지가 있다.

국립현대미술관 홈페이지에서 온라인 회원가입만 하면 1년에 12회 무료로 이용가능하다.

평일에 오면 사람 거의 없고 공간도 넓고 뷰도 좋고 조용해서 책 읽기 매우 좋은 장소다.

위치는 1층 테라로사 뒤편으로 ㄷ자로 돌아가면 교육동이 나오고 거기서 엘레베이터 ���고 3층으로 올라가면 된다.

혼자만 알고 싶은 맛집 알려주는 느낌이지만 너무 좋은 장소라 공유드린다.

ANTHROPIC JUST OPEN SOURCED THE ENTIRE WALL STREET WORKFLOW AND FIRMS ARE NOT GOING TO BE HAPPY ABOUT IT.

DCF models. LBO models. Equity research reports. Merger analysis. KYC checks.

All of it. Free. On GitHub.

Here is what just became available to anyone with a laptop.

Direct connections to Bloomberg, FactSet, S&P Global, Morningstar, and PitchBook.

Real Excel models with live formulas and sensitivity tables built automatically.

CIMs, IC memos, earnings reports, and buyer lists drafted on demand.

PE due diligence, GL reconciliation, and NAV tie-outs running as production agents.

This is not a chatbot wrapper that summarizes financial news.

These are production agents that own entire financial workflows end to end.

The kind that investment banks and private equity firms pay $50,000 to $500,000 per year in software licenses to run.

Now it is a one-line Claude Code plugin install.

19,800 GitHub stars.

Apache 2.0 license.

100% open source.

Think about what this actually means.

A junior analyst at a bulge bracket bank spends 80% of their 100-hour week running models, drafting memos, and compiling data across Bloomberg and FactSet.

That entire workflow just became a Claude Code agent.

The banks charging clients $500 an hour for analysis that this system produces in minutes are not going to tell you this exists.

The boutique advisory firms charging $50,000 retainers for due diligence work that these agents handle autonomously are not going to promote this repo.

But it is already live.

19,800 people have already starred it.

The window where knowing this gives you an edge over every analyst, associate, and advisor still doing this manually is open right now.

Star it. Fork it. Deploy it this weekend.

Bookmark this before your next financial model.

Follow @cyrilXBT for every open source release that disrupts an overpriced industry the moment it drops.

My Bet on the Tokenization Industry

I’m heavily accumulating $CRCL at $79, as I think it is the best risk/reward trade in the market right now.

@circle stock is currently down 74% from its ATH, even though:

• $USDC keeps growing in supply, now at $75B.

• Circle revenue reached $694M in Q1 2026, up 20% YoY.

• Circle is now the 3rd-largest platform by tokenized value with $3.1B

My belief is that $CRCL is currently undervalued and is set for a major repricing once the crypto bear market ends.

I expect $CRCL to behave similarly to what $COIN by @coinbase did in 2023–2025, when it delivered a 1,280% move from bottom to ATH, from $32 to $442.

What are the catalysts for an upcoming $CRCL repricing?

• Odds of Fed rate hikes are now above 50%. Higher rates would lead to more revenue for the company.

• Circle is expected to renegotiate its revenue split with Coinbase in August. The current split is 50/50, and if adjusted to 60/40 or 70/30 in Circle’s favor, it could materially boost revenue.

• The CLARITY Act is set to pass in the upcoming months. This would allow Circle to create and distribute more tokenization products.

• @Arc, Circle’s upcoming chain, is expected to launch this summer and is purpose-built for tokenization and agentic commerce.

Here are my potential $CRCL price targets for the next 12 months:

🟥 Conservative: $120

This would be around a 1.5x from the current price and would simply price in continued USDC growth, stronger revenue, and a partial crypto-market recovery.

🟨 Base: $240

This would be around a 3x from the current price and would happen if Circle keeps growing USDC supply, Arc launches successfully, and the market starts valuing $CRCL as tokenization infrastructure instead of just a stablecoin issuer.

🟩 Bull: $400

This would be around a 5x from the current price and would require a full crypto bull market, strong Arc adoption, a better Coinbase revenue split, and Circle becoming one of the main financial infrastructure companies for tokenization and AI payments.

Extra: I believe that, in 24 months, even a 10x scenario, with $CRCL at $800+, is doable.

Tokenize Everything and see you in one year with the results!

Elon Musk explains his 5-step algorithm for solving any problem:

"The most common mistake of smart engineers is to optimize a thing that should not exist."

"I have this very basic first principles algorithm that I run as a mantra."

Elon breaks it down:

Step 1: Question the requirements.

"Make the requirements less dumb. The requirements are always dumb to some degree, no matter how smart the person who gave you those requirements. You have to start there, because otherwise you could get the perfect answer to the wrong question."

Step 2: Try to delete it.

"Try to delete the part or the process step entirely. If you're not forced to put back at least 10% of what you delete, you're not deleting enough. Most people feel like they've succeeded if they haven't been forced to put things back in. But actually they haven't, they've been overly conservative and left things in that shouldn't be there."

Step 3: Optimize or simplify.

"The most common mistake of smart engineers is to optimize a thing that should not exist. So you don't optimize until after you've tried to delete."

Step 4: Speed it up.

"Any given thing can be done faster than you think. But you shouldn't speed things up until you've tried to delete it and optimize it otherwise, you're speeding up something that shouldn't exist."

Step 5: Automate.

"And then the fifth thing is to automate it."

Elon explains why the order matters:

"I've gone backwards so many times where I've automated something, sped it up, simplified it, and then deleted it. I got tired of doing that. So that's why I have this mantra."

나의 친애하는 고졸들아,

운동은 평생 반드시 해라.

20분 동네 걷고 그런거 말고,

최소 30분 이상, 심장 뛰고 땀 뻘뻘나는

그런 신체 활동을 일주일에 최소 3번 이상은 해라.

남녀불문 근육량은 최대한 젊을때 많이 늘려 놓고,

나이 먹고도 계속 유지 하려고 노력해야 빌빌 거리지 않고 사람구��� 하며 살수 있다.

반구십살 정도 되면,

꾸준히 운동 한사람과 안한 사람은 아예 다른 종의 생명체가 된다.

나는 원래 운동을 좋아해서

웨이트, 수영, 골프, 복싱, 승마, 테니스, 러닝, 농구 다 하는데,

기본적으로 본인에게 가장 접근성 좋은 운동을 반드시 하나는 만들기를 추천하며,

보통 웨이트는 기본으로,

야외에서 러닝으로 유산소를 하는게 가장 접근하기 쉽고 가성비가 좋다.

제대로 운동 후 찾아오는 호르몬 쓰나미발 그 개운함과 쾌감은 널 중독 시킬거고,

그 건전한 중독은 너의 육체와 정신을 건강하게 만들어 줄거고,

꾸준히 하면 그 신체와 심리적 변화가 너의 눈에도 보일것이며,

그렇게 만들어진 건강한 육체와 정신은

너의 수능 점수를 많이 높혀 줄것이다.

내가 오랫동안 시장을 헤쳐 나갈수 있음은,

이렇게 만들어진 건강한 육체와 정신 덕이라고 난 확실히 말할수 있다.

서울 사이버대 입학을 위해서는,

공부만해서 되는게 아니다.

공부를 집중력 있게 꾸준히 할수 있고, 시험시간동안 집중력을 잃지 않을수 있는 체력,

정신적인 데미지를 버틸수 있는,

뇌와 심장의 맷집,

이것들은 선택이 아닌, 필수인 것이다.

건강한 신체에, 건강한 정신이 깃들듯,

운동은 이것들의 가장 기본이 되는 기초 공사이다.

Someone cloned Netflix.

Then cloned Spotify.

Then cloned Instagram.

Then cloned Airbnb.

Then cloned WhatsApp.

Then cloned TikTok.

Then cloned Amazon.

Then put the source code for all of them on GitHub. For free.

Not one app. Not ten. Over 100 open source clones of the biggest apps on Earth. With source code. With demos. With tech stacks listed.

It is called Clone-Wars. 34,555 stars on GitHub.

Built by an Indian-origin developer named Gourav Goyal. He started collecting open source clones of popular apps into one list in December 2020. In March 2021, it went from 0 to 4,000+ stars in 7 days. It was on GitHub Trending for 5 days straight. Someone posted it to Hacker News and it hit #1 on the front page.

Here is what is inside.

Netflix clones. React, TMDB API, full streaming UI.

Spotify clones. Music player, playlists, search, albums.

Instagram clones. Feed, stories, likes, comments, DMs.

WhatsApp clones. Real-time messaging, read receipts, group chats.

Airbnb clones. Search, booking, maps, payments.

Amazon clones. Products, cart, checkout, Stripe payments.

TikTok clones. Short video feed, upload, likes.

Twitter clones. Feed, follow, tweet, retweet.

Slack clones. Channels, threads, real-time chat.

Trello clones. Boards, cards, drag and drop.

YouTube clones. Video player, search, comments.

And 90+ more.

Every clone has source code, a live demo, and the tech stack listed. React, Next.js, Node, Firebase, MongoDB, GraphQL, Tailwind. Every modern stack represented.

Here is why this matters.

Coding bootcamps charge $10,000 to $20,000 to teach you how to build apps like these.

Udemy courses charge $50 to $200 each. One app at a time. One framework at a time.

This repo gives you 100+ fully built apps with source code you can read, fork, and learn from. For $0.

Here is the wildest part.

The best way to learn to build Netflix is to look at someone who already built Netflix. Not a tutorial that teaches you one feature at a time. A complete, working clone with every feature connected.

You do not learn architecture from tutorials. You learn architecture from reading real projects.

100+ apps. 100+ demos. 100+ source codes. One repo.

Bootcamp: $10,000 to $20,000. Teaches 2 to 3 projects.

Udemy: $50 to $200 per course. One project each.

Clone-Wars: $0. 100+ projects. Every big app cloned.

34,555 stars. AGPL-3.0 licensed.

Every app you use. Cloned. Open sourced. Free to learn from.

(Link in the comments)