Apollo Micro Systems is steadily moving up the missile value chain.

The company already supplies power systems and RF/communication modules. With the acquisition of IDL Explosives, it is now entering the munitions segment as well.

Best example of vertical integration.

Kamath Associates (Zerodha Founders) 🔥

Spotted the 2-wheeler EV opportunity years before most investors.

In Apr 2024, Sachin Bansal wanted to divest his early angel stake in Ather Energy.

Nikhil Kamath stepped & bought

1.54% Stake through Kamath Associates

1.54% Stake through Nksquared

Invested around 282 Cr for 3.08% Stake

Combined ₹282 Crore investment is now worth over ₹1,185 Crore today.

Absolute value of their bet has grown by over 320%.

I'M Highly Bullish In 2 Wheelers EV Space.

🚀 You Have ₹5 Lakhs To Invest Today…

But the challenge is simple:

Pick only 5 stocks

Hold them for 10 years

No selling. No panic exit.

Which 5 names are entering your portfolio? 👇

Kirloskar Oil Engines - Building a Global Powerhouse 🔥

KOEL delivered one of its strongest years ever, balancing high growth, market share gains, margin expansion, and capacity creation, while staying firmly on track toward its $2 billion revenue ambition by FY30.

🔶️ Powergen: The Biggest Growth Driver

• Powergen revenue grew 32% YoY

• KOEL's DG market share increased significantly across segments

• Industry DG market grew 18% to ~1.79 lakh units, while KOEL grew 41%, selling 50,000+ units 💪

• High Horsepower (HHP) portfolio continues gaining traction, with sales reaching up to 3,000 kVA and growing adoption of Optiprime generators 💪

• Strong participation across data centers, industrial projects, and infrastructure demand

🔶️ Industrial Segment Scaling Up

• Industrial revenue grew 22% YoY to ₹1,444 Cr

• Growth led by construction, mining, and railways

• Construction business grew 44% YoY, benefiting from successful transition to new BS-V emission norms and customer wins

🔶️ International Business Crossing New Milestones

• International business crossed ₹1,000 Cr gross sales

• International revenues grew 37% YoY and 33% in Q4 💪

• Strong traction in both Powergen and Fluid Dynamics (pumps)

👉 Management emphasized building a true international footprint through local presence, distribution, and service capabilities rather than simply exporting products

🔶️ Aftermarket & Fluid Dynamics

• Aftermarket business grew 15% annually and 20% in Q4

• Focus on AMC-led service ecosystem and lifecycle management is paying off

• Fluid Dynamics business:

>> Domestic growth: 6% FY26

>> International growth: 36% FY26

• Exports continue to outperform with significant room for further expansion 💪

🔶️ Arka Fincap: Investing for the Next Growth Phase

• AUM grew 10% to ₹7,947 Cr

• Net Interest Income grew 11% to ₹266 Cr

• Expanded branch network from 34 to 137 branches

• PAT remained stable at ₹69 Cr despite heavy investments in secured retail lending

• Asset quality remained strong with:

>> GNPA: 1.2%

>> NNPA: 0.3%

🔶️ Massive Capacity Expansion Underway

• KOEL is investing aggressively to capture future demand 💪

• Phase 1

>> ₹700 Cr capex

>> Additional 50,000 engine capacity

>> Expected online by April 2027

• Phase 2

>> ₹1,400 Cr capex

>> Additional 20,000 HHP engine capacity

>> New manufacturing building at Kagal

>> Completion targeted over the next 2 years

👉 Management indicated the new ₹1,400 Cr facility alone can support ₹5,000–6,000 Cr revenue potential at maturity 💪

🔶️ Strategic Bets

• New subsidiary Kirloskar Advanced Systems formed to address opportunities in defence and advanced engineering systems integration 💪

• Continued focus on:

>> Data centers

>> High Horsepower generators

>> International markets

>> Alternate fuel engines (gas, ethanol, methanol, hydrogen blends)

>> Advanced energy solutions

👉 The company remains confident of achieving its FY30 target of becoming a $2 billion company, supported by market share gains, international expansion, and significant capacity additions

🔶️ Bottom Line

• KOEL is evolving from a traditional engine manufacturer into a diversified power solutions and engineering company

• With record earnings, rising market share, strong cash generation, global expansion, and ₹2,100 Cr of growth capex underway, FY26 marks another major step toward its FY30 aspirations.

Source- @concall_in

👉 Follow @vishan_29 for more updates.

🔴 Disclaimer: No recommendation. For educational purposes only.

59 HIGH-QUALITY SMALL-CAP STOCKS TO STUDY, TRACK & RESEARCH 🔥🔥🔥

▪ KRN Heat Exchanger

▪ Quality Power

▪ Vintage Coffee

▪ Apollo Micro Systems

▪ Astra Microwave

▪ Krishna Defence

▪ Yatharth Hospital

▪ Syrma SGS Technology

▪ Sigma Advanced Systems

▪ Emmvee Photovoltaic

▪ Atlanta Electricals

▪ Senores Pharmaceuticals

▪ Powerica

▪ Park Medi World

▪ Aye Finance

▪ Precision Wires India

▪ Universal Cables

▪ Viviana Power Tech

▪ Sansera Engineering

▪ Pricol

▪ V2 Retail

▪ GMDC

▪ Raymond Realty

▪ Netweb Technologies

▪ ACME Solar Holdings

▪ Modern Insulators

▪ KSH International

▪ TD Power Systems

▪ Inox India

▪ Sedemac Mechatronics

▪ Aditya Vision

▪ Bhagyanagar India

▪ HBL Engineering

▪ Websol Energy System

▪ KPI Green Energy

▪ Interarch Building Products

▪ MBEL

▪ Aeroflex Industries

▪ Krishna Institute of Medical Sciences (KIMS)

▪ Kernex Microsystems

▪ Power Mech Projects

▪ Anand Rathi Wealth

▪ Shaily Engineering Plastics

▪ POCL

▪ Tenneco Clean Air

▪ Sudeep Pharma

▪ Nephrocare Health Services

▪ Om Power Transmission

▪ Ashapura Minechem

▪ GNG Electronics

▪ TruAlt Bioenergy

▪ Belrise Industries

▪ Kwality Pharmaceuticals

▪ Beta Drugs

▪ Shriram Pistons & Rings

▪ Marine Electricals

▪ PNGS Reva Diamond

▪ Fujiyama Power

▪ Jammu & Kashmir Bank

WHY IS IT IMPORTANT TO TRACK HIGH-QUALITY SMALL CAPS?

▪ Many of the biggest stock market wealth creators started as relatively unknown small-cap companies before evolving into mid-cap and large-cap leaders.

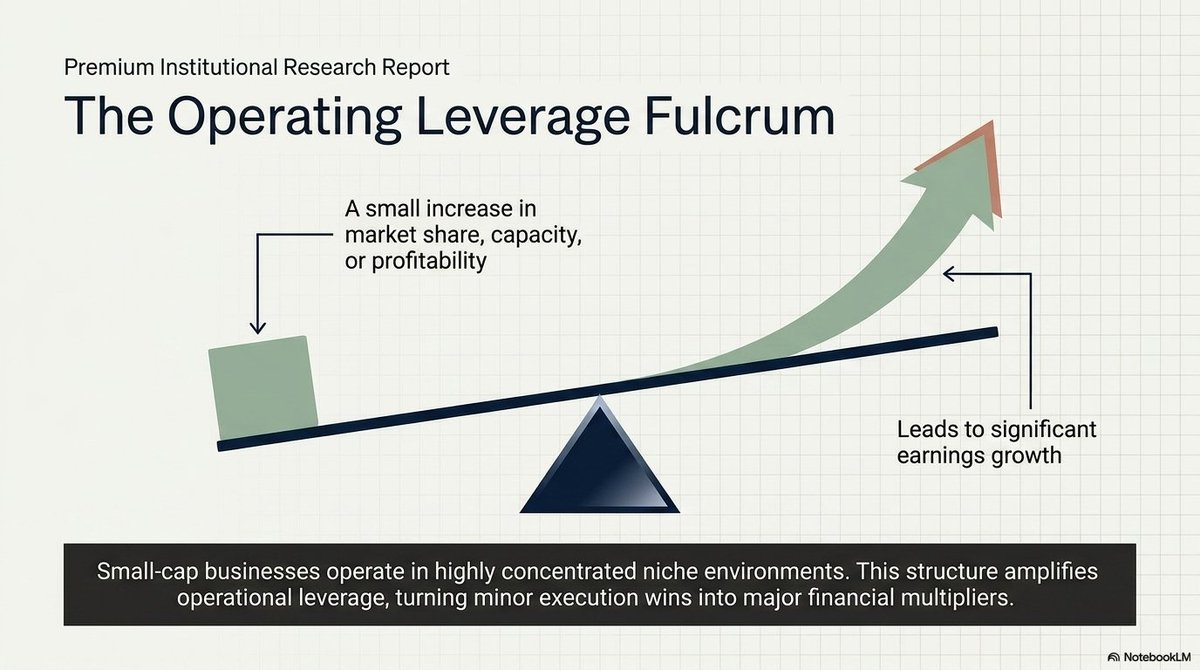

▪ Small-cap businesses often operate in niche industries where even a small increase in market share, capacity, or profitability can lead to significant earnings growth.

▪ Companies with strong management teams, healthy balance sheets, scalable business models, sector tailwinds, and consistent execution have the potential to create substantial shareholder value over long periods.

▪ Studying small-cap companies across sectors such as defence, power, manufacturing, healthcare, finance, renewables, infrastructure, electronics, and specialty chemicals helps investors understand emerging themes shaping India's growth story.

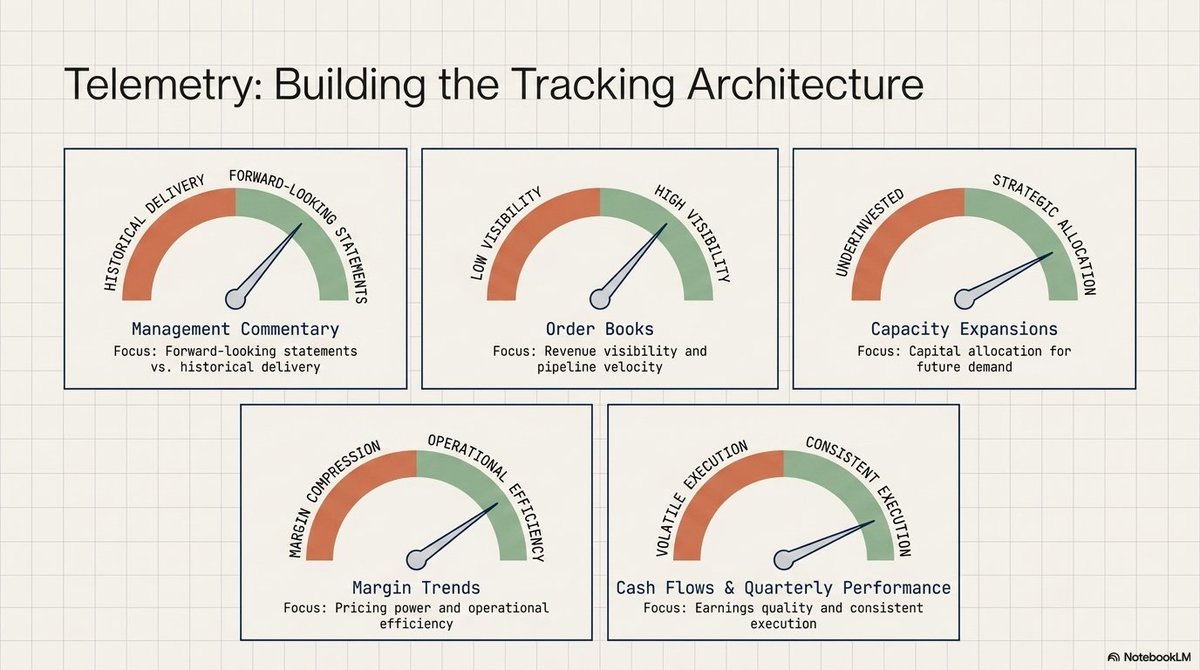

▪ Tracking management commentary, order books, capacity expansions, margin trends, cash flows, and quarterly performance can help identify businesses that are executing well before they become widely recognized by institutional investors.

▪ The objective is not to buy every company on the list. The objective is to build a high-quality watchlist, continuously track execution, monitor business developments, and identify companies that consistently deliver on their promises.

▪ Over time, a disciplined watchlist of fundamentally strong businesses can become one of the most valuable tools for long-term research and wealth creation.

DISCLAIMER

The above list has been prepared solely for educational, learning, research, and tracking purposes. Inclusion in this list does not imply any recommendation or guarantee of future performance. This is not a buy, sell, or hold recommendation.

🔔 Stock watch: Apollo Micro Systems

Could This Be the Next Big Defence Compounder?

India’s defence manufacturing story is still in its early innings, and one company that caught my attention which continues to execute exceptionally well is Apollo Micro Systems.

Why it stands out:

• Designs and manufactures mission-critical defence electronics, aerospace systems, avionics, underwater systems, weapon-control systems and military hardware.

• FY26 revenue surged 61% YoY to ₹904 crore while PAT jumped 91% YoY to ₹107 crore, delivering record annual performance.

• Q4 FY26 revenue grew 81% YoY while PAT surged 163% YoY, reflecting strong operating leverage and execution.

• Acquired IDL Explosives, expanding into defence-grade explosives, propellants and warhead systems.

• Received licence approvals for UAV manufacturing and secured export orders, opening new growth avenues.

• Beneficiary of India’s push for defence indigenisation, rising defence budgets and increasing exports.

What I like:

✓ Defence + Aerospace theme

✓ Explosive earnings growth

✓ Expanding capabilities through acquisitions

✓ Entry into UAVs and exports

✓ Massive long-term opportunity from Atmanirbhar Bharat

Key risks:

• Promoter pledge levels remain elevated and require monitoring.

• Working capital intensity is high, with long receivable cycles typical of defence businesses.

• After a sharp stock price run-up, valuation expectations have increased significantly.

Defence Electronics + Aerospace + UAVs + Import Substitution + Defence Exports

Apollo Micro Systems has already created enormous wealth for shareholders, but if management continues executing and India’s defence manufacturing ecosystem keeps expanding, the runway may still be much longer than many investors currently assume.

(Not a recommendation. Please do your own research & analysis after acquiring good knowledge)

#ApolloMicroSystems #DefenceStocks #DefenceManufacturing #MakeInIndia #AtmanirbharBharat #SmallCaps #IndianStockMarket #WealthCreation #Multibagger #FundamentalAnalysis #Investing

🖥️ Syrma SGS: Charging Up for the Global Electronics Supercycle 🔥

📊 Global & Indian EMS Boom

▪️ Trillion-Dollar Market: The global Electronic Manufacturing Services (EMS) market is projected to skyrocket from USD 1.04 trillion (CY24) to USD 1.36 trillion (CY29).

▪️ India's Massive Leap: India is set to be the fastest-growing geography globally with a 27% CAGR, expanding its global market share from 4% to 11%.

▪️ The $104 Billion Opportunity: India is poised to capture ~32% (USD 104 billion) of the incremental USD 319 billion global EMS growth.

🎯 Syrma SGS: Hyper-Growth Segments

▪️ Massive Addressable Market: Syrma’s specific focus segments are set to expand from USD 44 billion to USD 148 billion by CY29 - a staggering 41% CAGR.

▪️ Shift to High-Margins: Management is pivotally shifting away from commoditized segments toward high-barrier, sticky, and higher-margin sectors like Automotive/EV, Medical, Defense, and Aerospace.

▪️ Railways Leading the Pack: Railways and IT represent the fastest-growing target segment for Syrma, boasting a massive 50.4% CAGR driven by signaling modernization and localization.

▪️ High-Yield Medical Tech: Armed with FDA and MDSAP approvals, Syrma is executing an export-oriented strategy for medical devices (diagnostics, aesthetics), which command superior margins.

💼 Underappreciated Tailwinds & Exports

▪️ Hidden Defense Potential: Syrma's defense footprint is highly underappreciated; it already supplies PCBAs to defense programs and is set to ride the wave of indigenization, electronic warfare, and counter-UAS systems.

▪️ China + 1 Beneficiary: As a diversified electronics manufacturing platform, Syrma is perfectly positioned to disproportionately gain from global supply chain diversification and OEM outsourcing.

▪️ Structural Evolution: Syrma is successfully transitioning from a traditional EMS player into a premium, diversified technology platform backed by export tailwinds and PLI incentives.

🚫 No Recommendation

🚀 Potential Future Growth Leaders: Companies Targeting Aggressive Scale-Up Over The Next Few Years

▪ TD Power Systems Ltd ⭐

▪ DEE Development Engineers Ltd ⭐

▪ Azad Engineering Ltd

▪ Inox India Ltd

▪ Navin Fluorine International Ltd

▪ MTAR Technologies Ltd

▪ Sansera Engineering Ltd

▪ Sterlite Technologies Ltd

▪ Emcure Pharmaceuticals Ltd

▪ Sai Life Sciences Ltd

▪ Aeroflex Industries Ltd

▪ Quality Power Electrical Equipments Ltd

▪ Lumax Auto Technologies Ltd

▪ SJS Enterprises Ltd

▪ CCL Products (India) Ltd

▪ Knowledge Marine & Engineering Works Ltd

▪ Aimtron Electronics Ltd

▪ GNG Electronics Ltd

▪ Acutaas Chemicals Ltd

💡 Businesses with strong order books, capacity expansion plans, export opportunities, and management commentary indicating significant revenue growth ahead.

🔥 My Conviction Picks:

✅ DEE Development Engineers Ltd

✅ TD Power Systems Ltd

The next wealth creators are often identified before their numbers fully reflect their potential. Keep these companies on your radar. 📈

#DataPatterns

One of the most important developments at Data Patterns is the growing significance of its Electronic Warfare (EW) business. While many investors focus on traditional defence manufacturing, modern warfare is increasingly being defined by electronics, sensors, communication systems, and real time data processing.

Data Patterns has steadily built capabilities across electronic warfare systems, radar subsystems, mission computers, avionics, defence communication equipment and aerospace electronics. These are not low value components but some of the most sophisticated and technology intensive parts of modern defence platforms.

Electronic warfare is becoming particularly critical because future conflicts are not fought solely with missiles, tanks or aircraft. The ability to detect, disrupt, deceive, jam and protect communication and radar systems often determines battlefield superiority. This makes EW one of the fastest-growing segments within defence technology.

The company is also strengthening its presence in radar subsystems and mission computers. These systems act as the "brains" of military platforms, processing information from multiple sensors and enabling real time decision making. As defence platforms become more advanced, the electronics content per platform continues to increase.

Its avionics and aerospace electronics capabilities place the company in a highly specialized segment with significant entry barriers.

Developing and qualifying such systems requires years of expertise, extensive testing and close collaboration with defence agencies and OEMs.

India's push toward defence indigenisation further strengthens the opportunity. The government is increasingly encouraging local sourcing of advanced defence electronics instead of relying on imports. This creates a favorable environment for companies that possess proven indigenous technology and execution capabilities.

What makes Data Patterns particularly interesting is that it participates in the highest value layer of defence programs. While mechanical components can often face greater competition and pricing pressure, advanced electronics typically command superior margins and enjoy stronger technological moats.

As India expands investments in radars, electronic warfare systems, UAVs, missile programs, aircraft modernization and space based defence assets, the demand for sophisticated electronics is likely to grow much faster than the overall defence budget.

In many ways, Data Patterns is less a traditional defence manufacturer and more a defence technology company. If India's defence ecosystem continues moving toward greater self reliance and higher electronic content, the company could be positioned at the center of some of the most attractive growth opportunities in the sector.