At $AAOI $378M/month mid-2027 revenue framework = $4.5B annualized revenue.

20% EBIT margin, $900M EBIT run-rate.

Against $12.5B EV, you are paying 2027 14x EBIT while the company is growing revenues 30%.

$SIVE Q1 earnings are out, this is exactly the news I was expecting from past financials and future growth.

I have been saying this for weeks. The bears are going to sell the headline. Do not be the bear.

The financials only give us a glimpse of the past.

Revenue down 22% YoY. EBITDA burning. Low on Cash at 26.6M SEK.

The stock will get hit by people who read the first line and stop.

I expected exactly this. And I am still holding every share.

The revenue miss is not a business problem. It is a timing problem.

US government shutdown delayed defense budget approvals. That revenue did not disappear, it got pushed to H2 2026. FX headwinds from a stronger SEK against USD and GBP took another chunk on top.

The underlying demand is completely intact.

Now here is the number that actually matters.

Pipeline grew 77% year to date to $799 million. On a company doing roughly 250M SEK in annual revenue. $799 million in qualified pipeline. That gap between the P&L and the pipeline is the entire thesis.

The CEO said it himself: record pipeline growth and several volume productions confirmed through 2027, driven by enormous interest in wireless beamformers and InP lasers.

We got confirmation of what we already k

Inferred:

SIVE is developing a 1.6T LRO pluggable transceiver with Jabil for AI datacenters. Jabil serves hyperscalers at a scale most companies never touch. 800G is already dominating datacenter shipments and 1.6T is the next wave. Being Jabil's laser partner for that transition is a real design win.

Goldman Sachs put the CPO TAM at $91B by 2028.

O-Net and Enablence locked in Q1. Both deep in the CPO supply chain. The right ecosystem relationships are being built right now, before the ramp.

LiDAR production confirmed for Q4 2026. Automotive first, then industrial LiDAR and autonomous robots. Two monetization verticals from one platform.

York Space acquisition. York Space ties directly into the US Space Development Agency. Production orders described as imminent. This takes Sivers Wireless from component supplier to vertically integrated SATCOM player overnight.

Tachyon Networks expanding from 28GHz to 60GHz FWA with SIVE. A Tier-1 telecom vendor launching first products by end of 2026.

US Chips Act EW Star renewal confirmed. Microelectronics Commons Year 2 funding secured. The defense revenue that was delayed is de-risked.

Post-period they raised roughly SEK 125M via directed share issue. The cash concern is addressed. Board restructuring with new nominees explicitly framed as preparation for a Nasdaq NY dual listing.

So you have confirmed:

Jabil.

O-Net.

Tachyon.

Enablence.

York Space.

LiDAR ramp.

Defense recovery.

Nasdaq NY dual listing.

Plus those that can be inferred via supply chain mapping:

$MRVL

$APPL

All pointing at the same 12-18 month window.

Q1 numbers are the price you pay for early positioning.

The pipeline and partnerships are the reason you hold.

I’m counting on Sweden sells, America buy to scoop some juice shares at a discount.

They will sell the financials, we will buy the chock-point into the future.

Not financial advice.

In long $SIVE

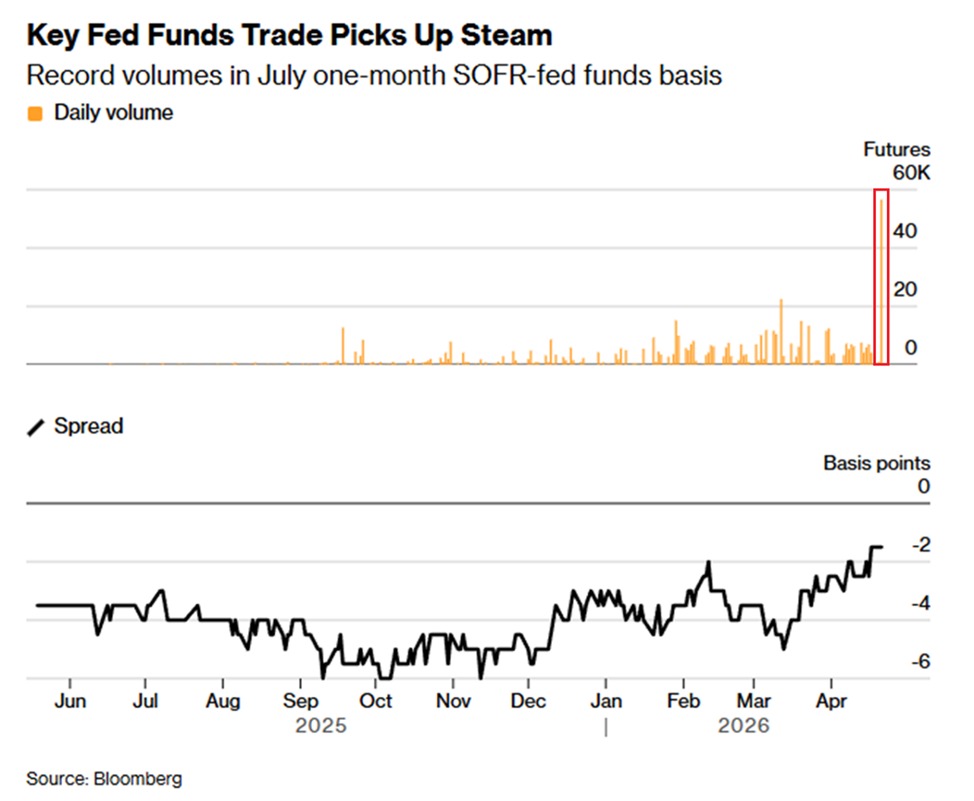

The Nasdaq $NDX breakout began today. The speed of this rally is absolutely insane, likely getting us back to the trendline by next week.

The question is what happens when we get there?

The 25 year parabolic is curling backward in time.

Traders are positioning for a major shift in US funding markets:

Daily trading volume in futures tied to the spread between the Secured Overnight Financing Rate (SOFR) and the Federal Funds Rate surged to a record 56,590 contracts on Tuesday.

SOFR is the cost of borrowing cash overnight against US Treasury securities, and is closely tied to the Fed interest rate, making it one of the most important reference rates in global financial markets.

Currently, SOFR is trading at 3.63%, just below the federal funds rate of 3.64%, a sign that cash is still plentiful in the financial system.

Traders are now betting this spread will turn positive, expecting borrowing costs to rise above the Fed's rate, signaling that cash is becoming harder to access.

This comes as the Fed is cutting its monthly Treasury bill purchases to $25 billion from $40 billion, while the Treasury is expected to increase the size of its T-bill auctions in the coming weeks to rebuild its cash balance toward a $900 billion target by the end of June.

Both moves reduce the amount of cash available in the financial system, tightening liquidity conditions that have kept overnight borrowing cheap throughout 2026.

Money market liquidity is set to shrink.

Here is what I thought about Trump’s play: how he would benefit from the “$120 oil” ? he would call this is national emergency so the US oil would only be consumed within the US then the rest of Europe and Japan would beg for US oil. Mid east oil will be restrained upon US approv

I'm long $TSEM, the $TSM of photonics.

My top two picks for CPO are $SOI and Tower Semi.

Given the $NVDA GTC catalyst on new photonic related architecture next week:

I expect Tower Semi to get a huge catalyst.

Nvidia laready directly collaborated with Tower to scale 1.6T silicon photonics last month (hint hint for GTC), likely pushing the downstream players to use it.

And now, Tower is the leading supplier of 1.6T SiPh PICs and the primary foundry for scale-up CPO architectures. (the other being global foundries)

From my forward est:

2028 Forward P/E: ~16.8x to ~18.1x

(Tower set a target $2.84B revenue by 2028, with ~31.7% operating margin, ~$750M in net profit)

The thing to note is over 70% of their planned SiPh capacity is already reserved through 2028. And photonics haven't even ramped up yet.

So, I expect them to strongly beat earning projections due to extreme photonics scaling + allocations price hikes that's not modeled into projections.

Also, $TSEM is heavily de-risked by 70% of capacity already being reserved. MC is likely due to $TSEM being a very obscure upstream player in the photonics supply chain.

But I expect the $NVDA GTC conference to be that catalyst that brings it to premium valuations.

I'm long $TSEM as an asymmetrical upside for upstream photonics foundry layer.

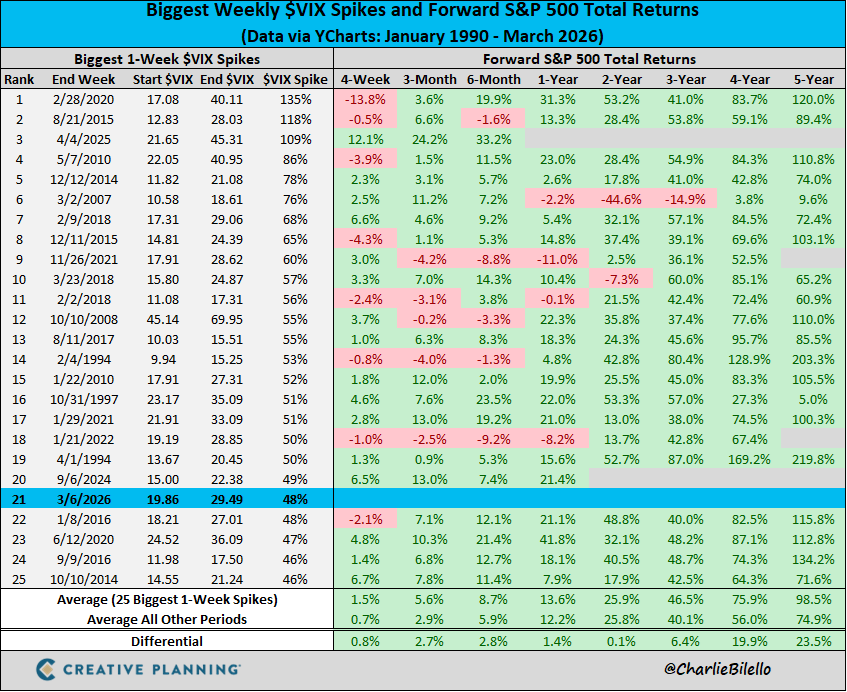

The $VIX increased 48% this week, the 21st biggest weekly spike ever.

What has happened in the past following the biggest $VIX spikes?

Stocks have tended to bounce back with above-average forward returns.

Does this always happen?

No. There are no certainties in markets, only probabilities.