ADISOFT TECHNOLOGIES – DETAILED CONCALL HIGHLIGHTS 🧾📊📑

Adisoft Technologies is a Pune-based industrial automation and digital transformation company that has spent over a decade building capabilities across automation, Industry 4.0, Industrial IoT, machine vision, robotics, traceability, production control systems and smart manufacturing solutions.

Over the years, the company has evolved from being a conventional automation service provider into a complete smart factory solutions provider capable of connecting ERP systems, IT infrastructure and shop-floor manufacturing operations into a single integrated ecosystem.

Management repeatedly highlighted that this integration capability is one of the company's biggest differentiators and allows it to create end-to-end digital manufacturing environments for customers rather than merely supplying automation equipment.

▪ Industrial Automation

▪ Industry 4.0 Solutions

▪ Industrial IoT

▪ Production Control Systems

▪ Traceability Solutions

▪ Machine Vision Systems

▪ Robotics

▪ Smart Manufacturing Solutions

▪ Digital Factory Integration

The company believes the Indian manufacturing sector is gradually moving towards connected factories where machines, software systems and data analytics operate in an integrated manner, creating a significant long-term opportunity.

🔸 INDUSTRY OPPORTUNITY REMAINS STRONG

Management remains highly optimistic about the long-term prospects of industrial automation and digital manufacturing.

As industries increasingly focus on:

▪ Industry 4.0

▪ Digital Manufacturing

▪ Traceability

▪ Smart Factories

▪ Industrial IoT

▪ Machine Connectivity

▪ Real-Time Data Analytics

▪ Error-Proof Manufacturing

the need for integrated automation solutions continues to rise.

The company believes it is well positioned to benefit from this structural shift as Indian manufacturers increasingly invest in automation, productivity improvement and data-driven manufacturing systems.

🔸 AUTOMOTIVE REMAINS THE CORE BUSINESS

Automotive continues to be the company's largest business segment.

Current Revenue Mix:

▪ Automotive – ~80%

▪ Non-Automotive – ~20%

Management remains highly positive on the automotive industry and highlighted continued investments by OEMs and manufacturers in new production lines, automation systems and plant expansion projects.

The company continues to benefit from:

▪ New Manufacturing Lines

▪ Capacity Expansion Projects

▪ Automation Upgrades

▪ Quality Improvement Initiatives

▪ Traceability Requirements

Management expects automotive to remain a major growth driver while simultaneously reducing overall dependence through diversification into other industries.

Long-Term Target:

▪ Automotive Contribution – 60–65%

🔸 DIVERSIFICATION INTO NEW INDUSTRIES

A key strategic objective is expanding beyond automotive.

Management is actively building capabilities and teams across:

▪ Pharmaceuticals

▪ White Goods

▪ E-Commerce

▪ Warehousing

▪ Packaging

▪ Printing

The company plans to hire sector specialists and domain experts to accelerate penetration into these industries.

🔸 PHARMACEUTICAL OPPORTUNITY

Management specifically highlighted pharmaceuticals as a promising growth area.

Rather than competing purely on factory automation, Adisoft is positioning itself around:

▪ Data Collection

▪ Production Monitoring

▪ Reporting Systems

▪ Traceability Solutions

▪ Production Analytics

These are areas where pharmaceutical companies increasingly require digital solutions for compliance, quality control and operational efficiency.

🔸 WHITE GOODS & E-COMMERCE OPPORTUNITY

The company is also targeting:

▪ Air Conditioner Manufacturers

▪ Television Manufacturers

▪ Refrigerator Manufacturers

▪ E-Commerce Warehouses

▪ Logistics Facilities

Management believes many solutions successfully deployed in automotive manufacturing can be adapted for warehouse automation, inventory tracking, traceability and production monitoring in these sectors.

🔸 PRODUCT & TECHNOLOGY PORTFOLIO

The company's offering spans multiple automation and digital manufacturing categories.

Key Solution Areas:

▪ Production Control Systems

▪ Traceability Systems

▪ Tracking Systems

▪ Poka-Yoke Systems

▪ Digital Picking Systems

▪ Vision Inspection Systems

▪ Robotics Solutions

▪ Machine Connectivity Solutions

▪ Smart Manufacturing Platforms

Management indicated that machine vision and robotics are currently among the fastest-growing areas of demand.

For a completely new manufacturing facility, project values can range between:

▪ ₹2.5 Crore to ₹10 Crore

depending on automation requirements and project complexity.

🔸 BUSINESS MODEL & MARGIN PHILOSOPHY

One of the most important insights from the concall was management's explanation of margin expansion.

According to management, the first deployment of a new solution requires significant investment in:

▪ Design

▪ Development

▪ Testing

▪ Customization

However, once the same solution is deployed repeatedly across multiple customers, profitability improves substantially.

This creates operating leverage and allows margins to improve over time without proportionate increases in development costs.

Management believes this reuse-driven model can continue supporting profitability as the business scales.

🔸 NEW BHOSARI FACILITY – MAJOR GROWTH DRIVER

One of the most important developments underway is the company's new facility in Bhosari, Pune.

Key Details:

▪ Plot Size – ~30,000 Sq. Ft.

▪ Built-Up Area – ~70,000 Sq. Ft.

Management described the facility as more comparable to a technology campus than a traditional industrial unit.

Current Status:

▪ Excavation Completed

▪ PCC Work Started

▪ Basement + Ground + First Floor expected by Sept–Oct FY27

▪ Production Expected to Start – October 2026

▪ Full Facility Expected by March 2027

The facility will integrate:

▪ Manufacturing Teams

▪ Software Teams

▪ Design Teams

▪ Project Execution Teams

under one roof.

Management believes this will significantly improve coordination, execution speed and operational efficiency.

🔸 CAPACITY EXPANSION & REVENUE POTENTIAL

Current infrastructure is approaching practical capacity limits.

Management highlighted constraints related to:

▪ Manufacturing Space

▪ Execution Capacity

▪ Employee Expansion

▪ Infrastructure Availability

The new facility is expected to remove these bottlenecks and support the next phase of growth.

Management indicated:

▪ Revenue Potential of New Facility – ₹650–700 Crore

▪ Time Required for Full Utilization – ~5 Years

An important point highlighted during the discussion was that larger infrastructure also improves customer confidence and increases the company's ability to secure larger and more complex projects.

Management believes the new facility will become a key catalyst for future growth.

🔸 ORDER BOOK & BUSINESS VISIBILITY

The company operates with relatively short project execution cycles.

Key Metrics:

▪ Average Project Cycle – 3–4 Months

▪ Opening FY27 Order Book – ~₹40 Crore

▪ Active Pipeline – ~₹85 Crore

▪ Orders Already Received – ₹46–47 Crore

▪ Around 40% of Annual Target Currently Under Bidding

Management expressed confidence in the quality of the order pipeline and future business visibility.

🔸 EXPORT OPPORTUNITY

The company has already executed export projects over the last two years.

Current strategy focuses on:

▪ Supporting Existing Customers Overseas

▪ Following Indian OEM Expansions

▪ Building International Capabilities

Management believes exports can gradually become an additional growth driver.

🔸 COMPETITIVE ADVANTAGE

According to management, Adisoft's biggest differentiator is its ability to integrate the entire manufacturing ecosystem.

The company can connect:

▪ ERP Systems

▪ IT Infrastructure

▪ Production Data

▪ Shop Floor Equipment

▪ Manufacturing Processes

into a unified smart factory environment.

Many competitors focus only on specific departments such as assembly lines, weld shops or press shops, whereas Adisoft can operate across the entire factory ecosystem.

Additional strengths include:

▪ In-House Design Capability

▪ In-House Software Development

▪ Strong Execution Capability

▪ Long-Term Customer Relationships

▪ Deep Manufacturing Domain Knowledge

🔸 TRADING BUSINESS

Apart from automation solutions, the company also operates a trading business.

FY26 Revenue Mix:

▪ Solutions Business – ~75–78%

▪ Trading Business – ~22–25%

Trading Margin:

▪ Approximately 10%

Although margins are lower, management views the segment as strategically important because it provides:

▪ Customer Access

▪ Market Intelligence

▪ Cross-Selling Opportunities

▪ New Business Leads

🔸 CUSTOMER CONCENTRATION

Management disclosed that the largest customer contributed approximately:

▪ ~65% of FY26 Revenue

The relationship has existed since the company's early years and continues to expand.

Management does not currently view this as a concern because of:

▪ Long-Term Relationship

▪ Recurring Opportunities

▪ Strong Customer Trust

Within its specialized automation niche, management estimates:

▪ Wallet Share – ~90–95% with this customer.

🔸 WORKING CAPITAL & RECEIVABLES

Key Metrics:

▪ Working Capital Cycle – ~120 Days

▪ Payment Cycle – 45–60 Days

Receivables increased due to strong execution during the second half of FY26.

Management clarified that collections remain healthy.

Importantly, after year-end collections, only approximately:

▪ ₹28–29 Crore

remained outstanding at the time of the concall.

This provides confidence regarding the quality of receivables and collection efficiency.

🔸 PROFITABILITY OUTLOOK

Management remains confident regarding profitability.

Key drivers include:

▪ Repeat Business

▪ Solution Reuse

▪ Operating Leverage

▪ Better Project Execution

▪ Higher Value Addition

Management indicated that:

▪ PAT Margins of ~13–14% remain sustainable.

▪ Additional improvement opportunities exist over time.

🔸 DEBT POSITION

Management highlighted that the company currently maintains a relatively modest debt profile.

Long-Term Objective:

▪ Debt-Free Status Within Approximately 2 Years

supported by future growth and internal cash generation.

🔸 GROWTH OUTLOOK

Management remains confident about future growth.

FY27 Guidance:

▪ Revenue Growth Target – ~25%

Management further indicated that FY28 could witness stronger growth because FY27 will only see a partial contribution from the new facility.

With a full-year benefit from the expanded infrastructure, management believes growth could potentially exceed:

▪ 30%+ Growth in FY28

📌 KEY NUMBERS AT A GLANCE

▪ FY27 Revenue Growth Target – ~25%

▪ FY28 Growth Potential – 30%+

▪ Plot Size – ~30,000 Sq. Ft.

▪ New Facility Size – ~70,000 Sq. Ft.

▪ Production Start – October 2026

▪ Full Facility Operational – March 2027

▪ Revenue Potential of New Facility – ₹650–700 Crore

▪ Utilization Period – ~5 Years

▪ Opening FY27 Order Book – ~₹40 Crore

▪ Active Pipeline – ~₹85 Crore

▪ Orders Already Received – ₹46–47 Crore

▪ Project Cycle – 3–4 Months

▪ Automotive Revenue Contribution – ~80%

▪ Long-Term Automotive Mix Target – 60–65%

▪ Trading Business Contribution – ~22–25%

▪ Trading Margin – ~10%

▪ Largest Customer Contribution – ~65%

▪ Wallet Share – 90–95%

▪ Working Capital Cycle – ~120 Days

▪ Payment Cycle – 45–60 Days

▪ Receivables Outstanding After Collections – ~₹28–29 Crore

▪ Typical Project Size – ₹2.5–10 Crore

▪ Sustainable PAT Margin Range – ~13–14%

Disclaimer: This summary is based on management commentary and is intended solely for educational and research purposes. Please conduct your own research before making any investment decisions.

आप ब्रश करते हैं → Colgate

आप शेव करते हैं → Gillette

आप नहाते हैं → Pears

आप पहनते हैं → Levi’s

आप खाते हैं → Domino’s & KFC

आप पीते हैं → Coke & Nescafé

आपको फ़ोन चाहिए → Apple

…और फिर आप पूछते हैं कि रुपया डॉलर से कमज़ोर क्यों है? 🤔

@itsnitinverma Very true. Well simplified...good to learn & focus on major internal organs controlling the critical harmone balance rather than acting on typical superficial symptoms.

🚨 The Jio Financial Services (JIOFIN) growth engine is officially shifting from incubation to massive scale.

Here is the roadmap for 2026:

🛡️ Insurance: Allianz JV is live! Full life & general insurance entry targeted by late '26.

🏦 Credit: Pivoting to safer Secured Lending (Home Loans) + embedded checkout credit via Reliance Retail.

📈 AMC: JioBlackRock just crossed ₹15,200 Cr AUM in only 9 months.

💰 War Chest: A massive ₹15,700 Cr promoter capital infusion to fund this aggressive expansion.

A massive disruption in the Indian financial ecosystem is loading. 🇮🇳🚀

Do you think jio finance can become the next big thing in India ?

@RajStockWatch Total outstanding dues other than small & micro enterprises is 10x YoY, 16.73 Cr.

Seems executed big order from big enterprise &awaiting receivables. Management clarification and #WomanCart will be back in the game, otherwise it's already down 35% in 2 days.

@srir54@sudheep8531 Total outstanding dues other than small and micro enterprises is 10x, 16.73 Cr. Seems big order from big enterprise... awaiting receivables. One clarification and #WomanCart will be back in the game, otherwise it's already down LC.

@RajStockWatch I had replied to your post on #Supremepower..that it was a good buying opportunity at 132. Also mgmt is humble giving on ground reality guidance avoiding any over expectations by market (operators).

Sometimes when you read how Reliance built this entire Jio Finance network - insurance, AMC, the overall financial segment

They just integrated it with their own architecture which they built over time, did a few partnerships, and created lakh crore company out of nowhere.

This is just crazy. I think they even got a banking licence. So I really feel sometimes, wow, this is an incredible way to do business.

Hint - You will know when you go to a Reliance Digital store... and the pan-India distribution network that Reliance has built + trust over time.

Good post on shipbuilding opportunity scale with quantitative data

Shipbuilding is still largely unexplored

It's a 10-20-30 year opportunity

#Krishnadef and #Rappid valves are few microcaps stocks i can highlight from the space

many more can come with more research

@saur_agar7 Exclnt #Jiofinancil analysis. Hopefully will see demerger of reliance holding ltd to get true potential of financial business. Anyway it's a good proxy investment to Reliance Ltd with bonus of retail finance growth capturing engine at cheap valuations. Promoter buying is + too.

These Stocks Are Being Accumulated by FIIs - March 2026 Insights 🔥🔥🔥

Quality Power

Rajesh Power

Transrail

Hitachi Energy

GE Vernova T&D

Siemens Energy

Supreme Power

Sathlokhar Synergys

Prizor Viztech

Senores Pharma

KSH International

TD Power

Advait Energy

Danish Power

Jay Bee Laminations

OBSC Perfection

Sky Gold

GNG Electronics

TARIL

Kernex Microsystems

GRSE

Waaree Energies

Syrma SGS

Vidya Wires

Astra Microwave

Krishna Defence

Adani Power

Voltamp Transformers

Shringar House of Mangalsutra

When FIIs increase their holdings during a market correction, it becomes a high-conviction signal, not a random activity.

Firstly, FIIs typically deploy large capital with deep research, global comparisons, and long-term perspective. If they are buying when markets are weak, it suggests they are looking beyond short-term volatility and positioning for future growth.

Secondly, this behavior indicates sectoral conviction. From this list, a clear pattern emerges:

1. Power & electrification (transformers, cables, EPC, transmission)

2. Defence & aerospace

3. Renewables & energy transition

4. Electronics & manufacturing (PLI beneficiaries)

👉 This tells us that FIIs are not buying randomly, but are focusing on themes with strong multi-year tailwinds.

Thirdly, buying in corrections often means:

1. Valuations have become attractive

2. Risk-reward is favorable

3. Earnings visibility is strong

So instead of chasing momentum, FIIs are accumulating quality businesses at better prices.

Fourth, this also acts as a leading indicator:

➡️ If FIIs are increasing exposure in specific sectors, those sectors often outperform in the next phase of the bull run.

Lastly, many of these companies are:

1. Linked to India’s capex cycle

2. Beneficiaries of energy transition + infra push

3. Operating in high entry-barrier industries (EHV, defence, electronics)

👉 Which means FIIs are essentially positioning for India’s long-term structural growth story.

Key Insight

When smart money buys during fear, it is usually preparing for the next phase of growth.

Tracking such stocks helps identify early leadership for the upcoming bull run.

Disclaimer:

This is for educational purposes only and not investment advice. Please do your own research before investing

Mainboard Leaders & Their SME Counterparts - Hidden Opportunities You Can’t Ignore 🔥👇

Waaree Energy →Alpex Solar

Syrma SGS → Aimtron Electronics

Garden Reach Shipbuilders → Krishna Defence (recently migrated)

Transrail Lighting → Rajesh Power / Viviana Power

Yatharth Hospital → UniHealth Hospitals

Cupid → Anondita Medicare

Polycab → JD Cables / Prime Cables

Shilchar Technologies → Danish Power

Amara Raja Energy → Maxvolt Energy

Interarch Building → Sathlokhar Synergys

Acme Solar → Oriana Power

Gravita India → Baheti Recycling

Aditya Infotech → Prizor Viztech

Let’s continue building this list further - you can also add more mainboard players and their SME counterparts to make this list even more comprehensive and insightful.

Disclaimer:

This is for educational purposes only and not investment advice. Please do your own research before investing.

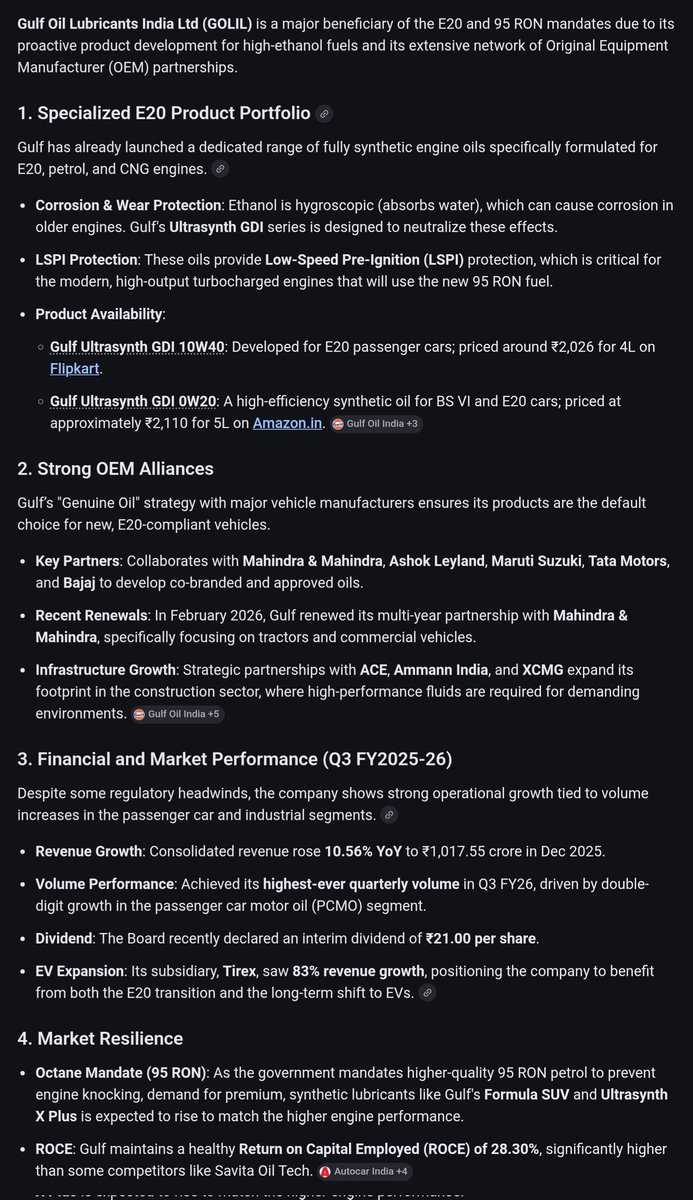

Ministry of Petroleum and Natural Gas, dictates that all oil marketing companies must supply petrol that meets two key specifications:

* Ethanol Blend: Up to 20% ethanol content.

* Minimum Octane: A Research Octane Number (RON) of 95.

#GulfOilLubricants India

Here are my 10 power rules

1. Choose great sector (10 year growth)

2. Early entry (big leverage)

3. Smaller players (lose small, win big)

4. Huge allocation in limited names

5. Great promoter (15+ yr exp, ethical, humble)

6. Track all updates about the company (twitter, linkedin, you tube, nse, bse, the whole internet)

7. Mentally ready for 70% win, 30% loss (happens mostly)

8. Increase winner allocation, reduce loser allocation

9. Sit for long time (boring investing)

10. Don't overfocus on every financial metric (a good promoter with a smart CA will take care of numbers)

Most points out of 10 are good to an extent

I am not very strict on financials as i mostly invest in micro caps

Out of these i look at promoter holding it should be significant and increasing/stable

Apart from that i trust the promoter to handle the financials

Too much tightness and rules and you won't be able to buy/hold most micro caps

Some SME/ Microcap stocks ( =<2000 cr ) in my watchlist 👀

In case of panic correction in the market

In no particular order

Emm force

Taurian

Influx health

Kabra Drugs

Parth

OSEL

Robu

OBSC

NPST

Airfloa

Fly SBS

Beezaasan

Yash High voltage

No recommendation to buy/sell/ hold.

Just sharing names for your study

Any other names?