Still debating the economics of a 10% APR credit card?

There’s already a 0% APR option available- with no late fees and no credit check.

It’s called Live Pay, by @earnin

.@jonmvdavis of @uoregon studied 1M+ @earnin

customers. We didn’t know what he’d find, but it’s clear—and matches what customers say: when people can access pay when they need it, wherever they work, incomes rise by $334/month.

https://t.co/31Ifa6QCiM

People work every day, and still wait to get the money they’ve already earned. That’s a system failure. More on this issue, and how @earnin is solving it, in a recent conversation with @bhorowitz and @eriktorenberg.

https://t.co/nNbIWiz8Uv

A @UConn & #UConnSPP study shows the negative impact of CT eliminating instant earned wage access (EWA) for workers. 2/3 of the research sample said instant EWA had positively impacted their finances. Read the study online https://t.co/j11BbZgFNB

@kerri_raissian@JNecciDineen

Ironic, isn’t it? People finally find a way to get back on their feet & the system pulls the rug out. Y does policy always seem 2 protect the status quo instead of people who need real solutions? 📷Read about the daily struggles of cash-strapped Americans

https://t.co/av5vZtmsgW

In November alone, @earnin's systems enabled access to over $1.5 billion in wages, as we continue to test and improve new products designed to give people more control over their financial lives.

Inflation isn’t just economic—it’s cultural.

We’re witnessing a ~$2 Trillion wealth transfer from those tied to the old system to those embracing new tech like Bitcoin. Savings lose value with all the money printing. Bitcoin, with its finite supply, gains.

All eyes have been on DC recently. @EarnIn is making a real difference for working Americans there. In 2024 alone, EarnIn has helped DC customers avoid on average $781 in overdraft fees.

How did I get started at @earnin ?

I never set out with the intent to start a company.

At my previous company, I heard that some of the employees were running into overdraft fees and payday loans.

When I asked one of them about it, it was not because she weren't being paid enough, but because she couldn’t wait until the following Friday to get paid.

We couldn't get the payroll system to pay her for days she had already worked. So I paid her out of my own pocket.

I soon realized that other employees had similar issues, so I started doing this for them as well. Then it hit me. It’s a systemic issue affecting millions of people.

That was how EarnIn came about.

So moving to read stories about how Earned Wage Access and @earnin help people manage financial challenges like the cost of healthcare.

https://t.co/sJQr9gSDHf

Another hypothesis to test.: Are people better off if money moves faster?

If money can be moved faster, should the GDP increase?

Money Supply * Velocity of money = GDP

The different temporary IDs would point to the same person. It's like having many phone numbers that all ring on the same phone.

Apple does something similar - when you add a card to the wallet, the merchant gets a different number each time, but they all authenticate against the same card.

What’s the cost of our outdated digital infrastructure?

Look at Social Security numbers - lifelong and unchanging ID numbers.

Instead imagine temporary, revocable IDs that work only for the specific company you gave them to. You could retire IDs you don’t want used again and get alerts for any use. This would greatly reduce ID theft.

The tech exists, but will the government solve the problem?

#IDTheft #DigitalSecurity

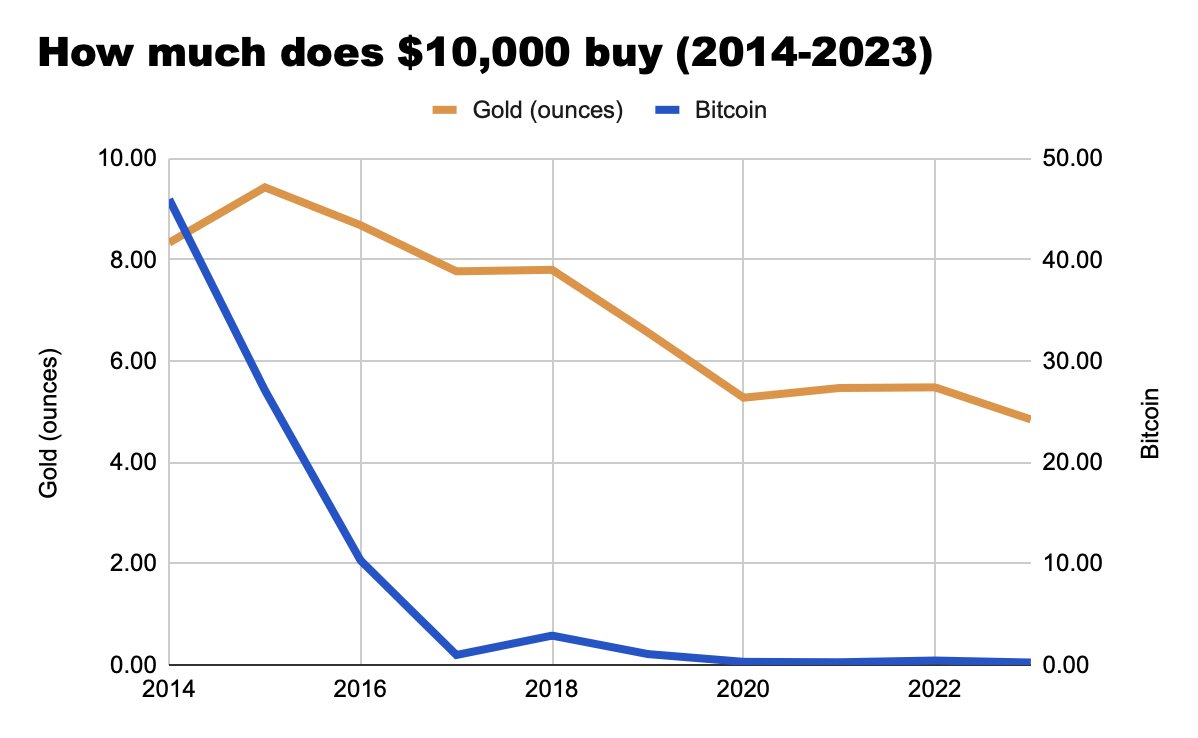

Fiat currencies (like the $) might be the ultimate secret monopolies.

If you had to choose a store of value, would you choose:

- Fiat currency where the supply (and price) is determined by a group of people making subjective decisions

- Gold, where the supply is constrained by physics and chemistry.

- Bitcoin, where the supply is algorithmically determined and programmatically enforced.

Oh wait, you cannot choose. The controllers of fiat currency regulate banks. And banks are not allowed to let you save in Gold or Bitcoin.