Commercial payments is a $400B+ market. Barely touched. This week on @basispointpod, @SoFi CEO @anthonynoto mentioned Mesh as a commercial payments partner, noting "most people don't know about" it yet. They will. Proud to be part of this vision.

Sofi named #1 U.S. Bank

At @SoFi, we believe people deserve a bank that truly has your back, not just in branding and hype, but through a member-focused mission and products and services that are held to the highest standard possible.

That’s what SoFi stands for - and why we were named the No. 1 U.S. bank on @Forbes World's Best Banks list!

https://t.co/n4uAth9T2d

I spent over 1000 hours analysing $SoFi and wrote a 60-page deep dive for my college economics major finals.

These are the top 10 reasons SoFi will become the largest bank in America during our lifetimes (A thread)

Thank you to @SoFi and @AnthonyNoto for their early leadership in support of @TrumpAccounts.

Matching the federal $1,000 contribution is a strong commitment to helping families invest early and build long-term financial security for the next generation.

.👇Yes, sir. If this is enacted—and that’s a big if, though part of me hopes it is—we would likely see a significant contraction in industry credit card lending. Credit card issuers simply won’t be able to sustain profitability at a 10% rate cap.

Consumers, however, will still need access to credit. That creates a large void—one that @SoFi personal loans are well positioned to fill. I’ve long believed many consumers are disadvantaged by high-reward credit cards (they know who they are), only to end up carrying tens of thousands of dollars in balances at 20–30% APRs. In many cases, those balances are effectively interest-only and can persist indefinitely.

By contrast, a SoFi personal loan at 9–13% offers a lower rate with a fully amortizing structure that actually pays the balance down. If credit card lending contracts, SoFi can step in to offer borrowers a more transparent, lower-cost alternative to revolving debt. We could also expand to a larger target market & appropriate rates with still great returns.

This dynamic would also materially simplify marketing. Today, credit cards win the acquisition battle because consumers don’t realize they’re signing up for high-interest, long-duration debt—until they’re already deep in it. Only then do many borrowers find @SoFi as a solution to an existing problem. If credit card lending contracts, SoFi personal loans become the solution before the problem exists, not after. SoFi marketing shifts from debt consolidation to smart upfront financing.

Bottom line: less credit card lending could translate directly into more personal loan demand for SoFi. Giddy up!!

Also if this scenario plays out, underwriting discipline and borrower education become even more important—SoFi’s advantage isn’t just price, it’s helping customers exit debt, not revolve in it. GYMR!!

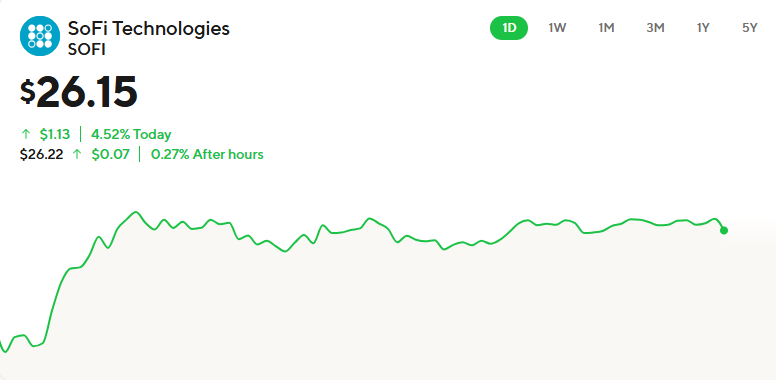

$SOFI JUST POSTED IT'S HIGHEST CLOSE EVER AT $26.15!!! 📈

Stock price milestones are dropping like flies.

Since I posted these targets on July 9, SoFi has taken out three out of the four of them:

SoFi ticker ATH was taken out on earnings day when it got to $25.11, beating the previous high of $24.65.

It's highest every close, which was previously $23.29 was taken out on August 12 when it closed at $23.65.

The only remaining milestone is the ATH from $IPOE days of $28.26. That's only 8% away.

LET'S GO!!!

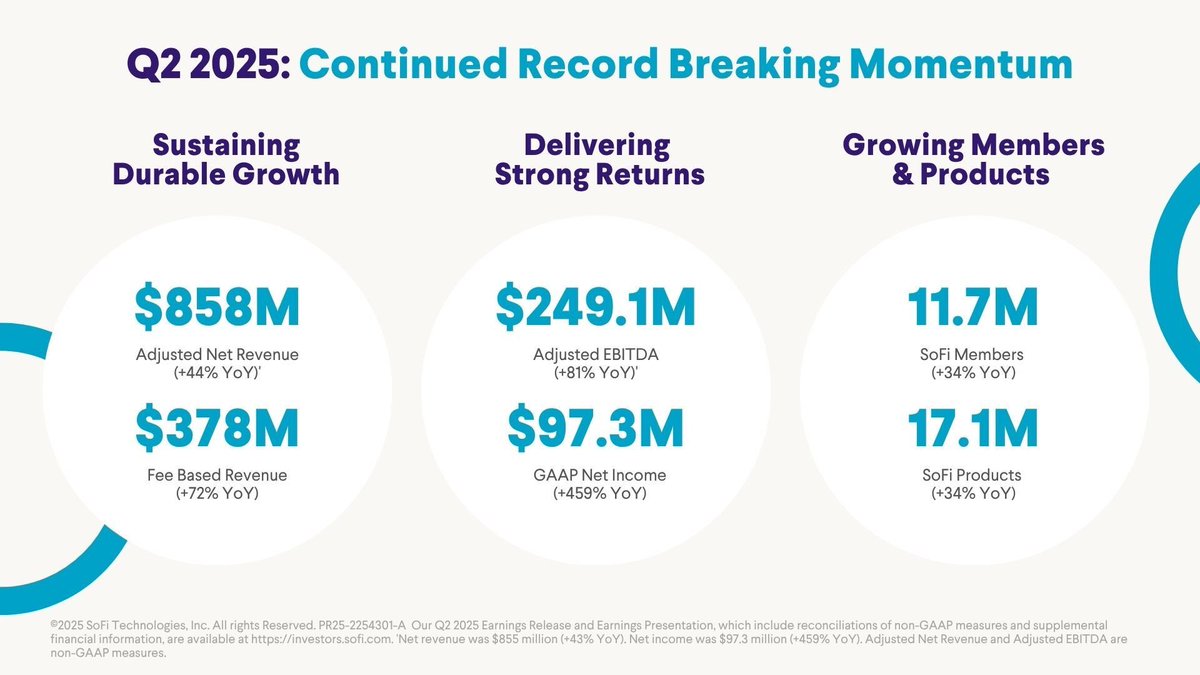

We @Sofi had an exceptional second quarter with record member and product growth and 44% adjusted net revenue growth – our highest in over 2 years. 29% EBITDA margin. The new rule of 70!! We’re building faster than ever to deliver unmatched value to our members and clients. Thank you to our @SoFi members for trusting us to help you achieve your goals.

More here: https://t.co/WUp2mIW9g5

$SOFI BLOWS OUT EARNINGS WITH A MASSIVE BEAT ON THE TOP LINE, BOTTOM LINE, AND GUIDANCE.

+44% YoY REVENUE GROWTH

Brand new ATH in new members

LPB volume was $2.45B

THIS QUARTER WAS RIDICULOUS!!!

On January 3, 2024, a boutique investment bank named Keefe, Bruyette, and Woods, or KBW, downgraded $SOFI to a sell rating with a one-year price target of $6.50.

That catalyzed the second worst day in the stock's history as it cratered 14%.

Sound familiar? It should, because they are trying to pull the same trick again this year. They just downgraded SoFi again just after the new year. Should you trust their analysis?

Fortunately, I have that report they published a year ago. So we can see how good their analysis was. Let's dive in, shall we?

We'll cover revenue, EPS, adjusted EBITDA, and then the analysis itself. By the end of this thread, you'll know just how much confidence you should have in their analysis...

Proud to share news that @SoFi will provide the financial backbone for @meshpayments, while @GalileoFintech continues to support payment processing.

Read more ⬇️

The Mesh Payments and $SOFI partnership is fairly recent. Their website showed Metropolitan Commercial Bank as their partner as recently as October 8 according to the Wayback Machine. It now shows SoFi