Biggest market puzzles

1. If global growth is so strong, why are oil prices flat?

2. Why no China reopening lift to commodity prices?

3. Why are yield curves inverted if there's no recession?

4. Why do so many people want to be long Euro?

5. Why has Fed pivot not lifted S&P 500?

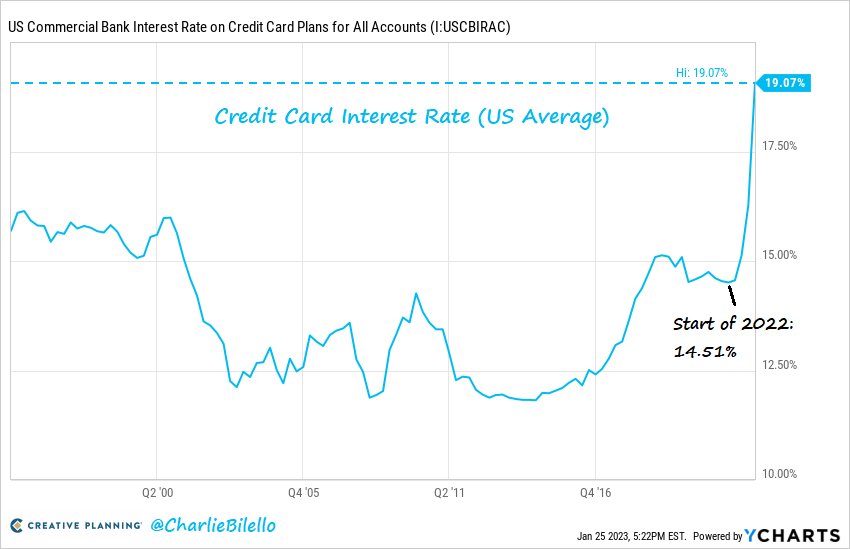

The average interest rate on US credit card balances has moved up to 19.07%. With data going back 1994, that's the highest rate we've ever seen, and 4.5% above the rate from a year ago.

''Liquidity''.

A crucial and widely misunderstood driver of financial markets.

Let's explain what liquidity really means, and where it's headed next.

A thread.

1/

The spread between 10-year and 1-year Treasury yields moved down to -1.26% last week, the most inverted curve since September 1981. The last 8 recessions in the US were all preceded by an inversion in this yield curve relationship.

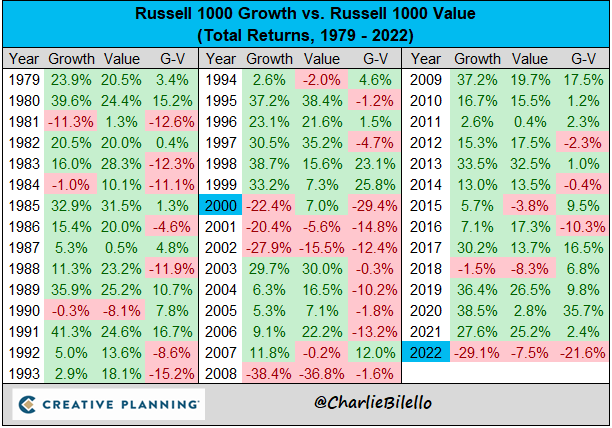

Growth stocks underperformed Value stocks last year by 21.6%, the 2nd widest spread on record with data going back to 1979. Only 2000 (dot-com bubble bursting) showed a greater differential (-29.6%), which was followed by 6 more years of Value beating Growth (2001-2006).

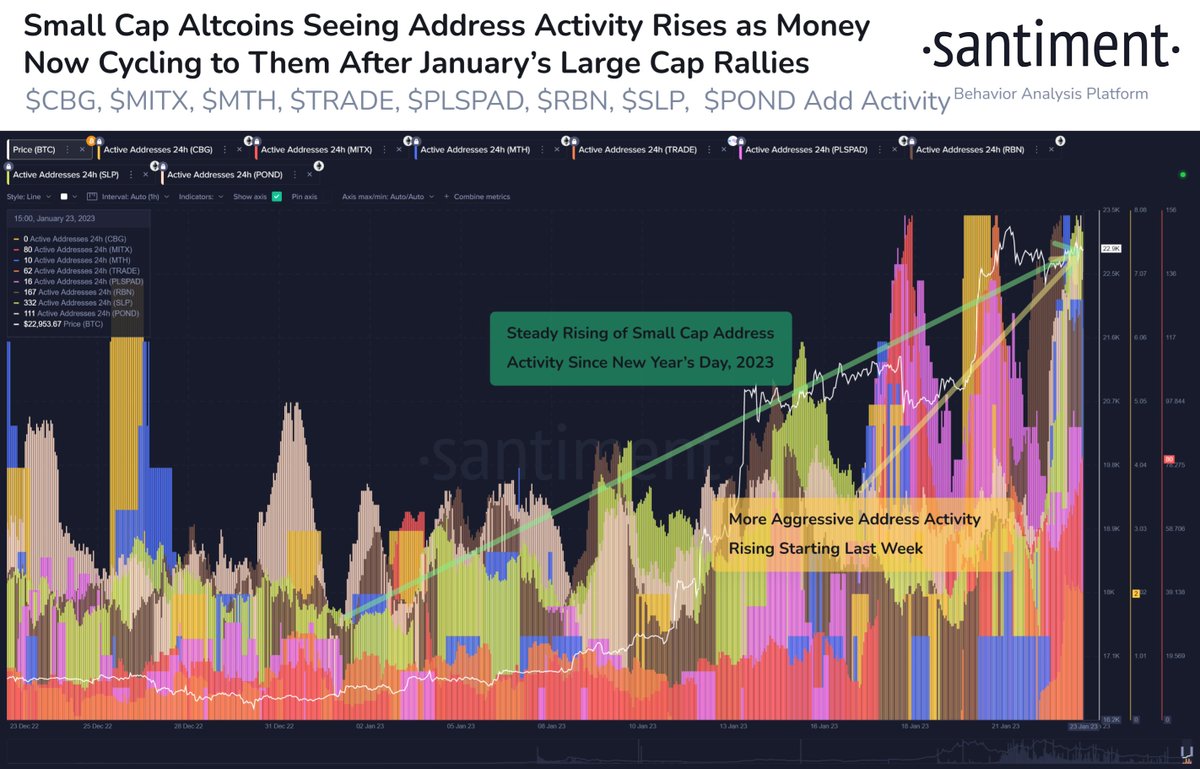

🤏 With large caps like #Solana, #Cardano, & #Polkadot drawing impressive return headlines the first 3 weeks of January, money now appears to be cycling to small caps. Active addresses are up big for $CBG, $MITX, $MTH, $TRADE, $PLSPAD, $RBN, $SLP, & $POND. https://t.co/VEJcMMgS6W

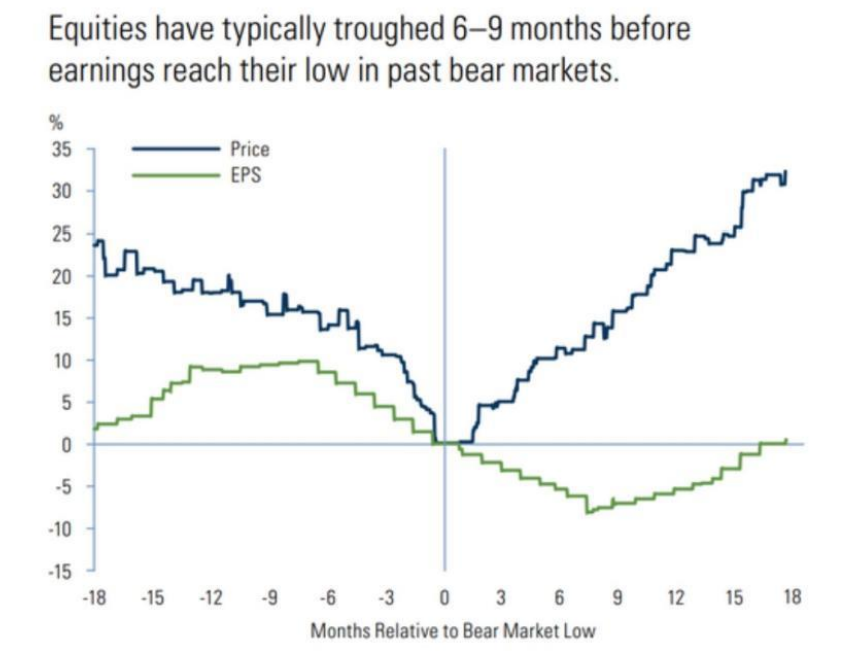

Excellent chart showing how earnings and valuations don't bottom together!

Historically, stock prices bottom 6-9 months before EPS reach their low as multiples start to rise reflecting Fed cuts and accommodative policy ahead.

I posted this 2nd January:

Relief rally Q1

FED Interest Rates pivot Q2

Bottom Q3-Q4

Of course we still need to wait and see where this pump takes us, but what do you guys think? 👍

Record weekly inflows into EM debt and equity markets.

Long EM was also the most consensus view I heard at a large investment bank conference in London last week.