Photo me Passport photos - what a day. Down 27% to £1.07

#MEGP is now trading like the business is broken. It isn't. ME Group isn't the only French consumer business reporting weakness in April to May 2026.

✓ https://t.co/G6qfuwjC8I 49.4% EBITDA margin

✓ Group ROIC 25-29%

✓ 8% yield while you wait

✓ 1,300 new machines rolling out

✓ Same management compounding EPS 26% CAGR for 3 years

Bought in at 107p avg today.

Macro pain ≠ broken business!

Translation: Crude oil sold off hard this week, as people living in fantasy land once again allowed Axios propaganda to persuade them an Iran peace deal is just around the corner, despite that any rational examination of the facts in evidence yields an opposite conclusion. Got it.

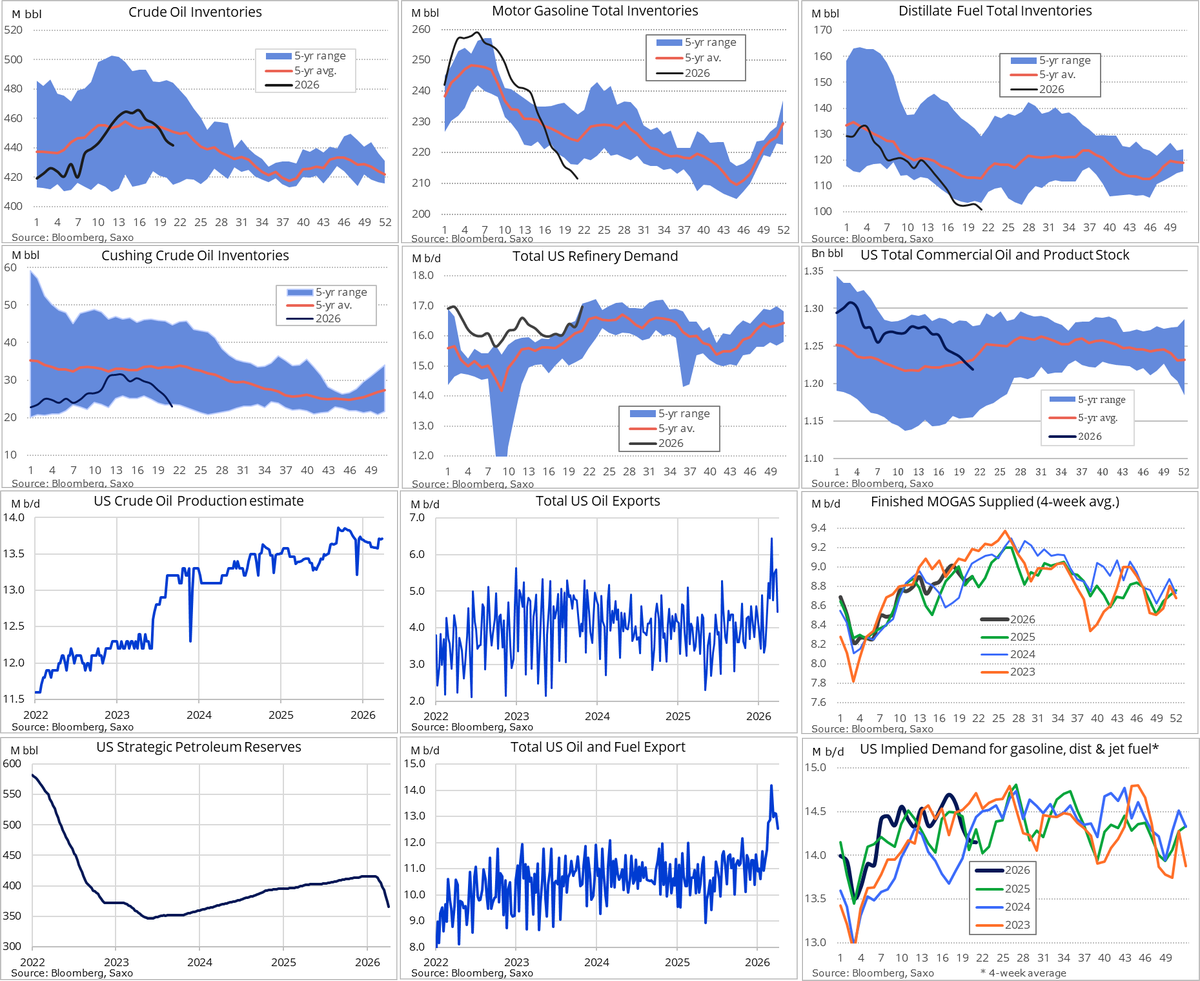

EIA's weekly data release for the week ending 22 May showed broad-based declines across U.S. crude and refined product inventories. Total crude oil stocks, including Strategic Petroleum Reserve (SPR) withdrawals, fell by 12.4 million barrels. Refinery demand surged to nearly 17 million barrels per day, potentially limiting export availability as crude exports slowed for a second consecutive week to 4.4 million barrels per day. Meanwhile, inventories at Cushing, Oklahoma - the delivery hub for WTI futures - declined by 2.8 million barrels.

Ahead of the peak summer driving season, gasoline inventories fell to their lowest seasonal level since 2014, while distillate stocks dropped to around 100 million barrels, the lowest level for this time of year in 25 years.

It's not a particularly well known stock at this juncture. It's currently in the "African not profitable" bucket. That should change as the profits ramp.

I did a chart from 2026 profit & EPS rise dramatically & the PER goes the other way: -

A super Q1 2026 results statement from

#SRB Serabi #GOLD

The cash is starting to pile up despite its 6% dividend

Incredibly it still trades of a PER of just over 3

(less if you add back that cash)

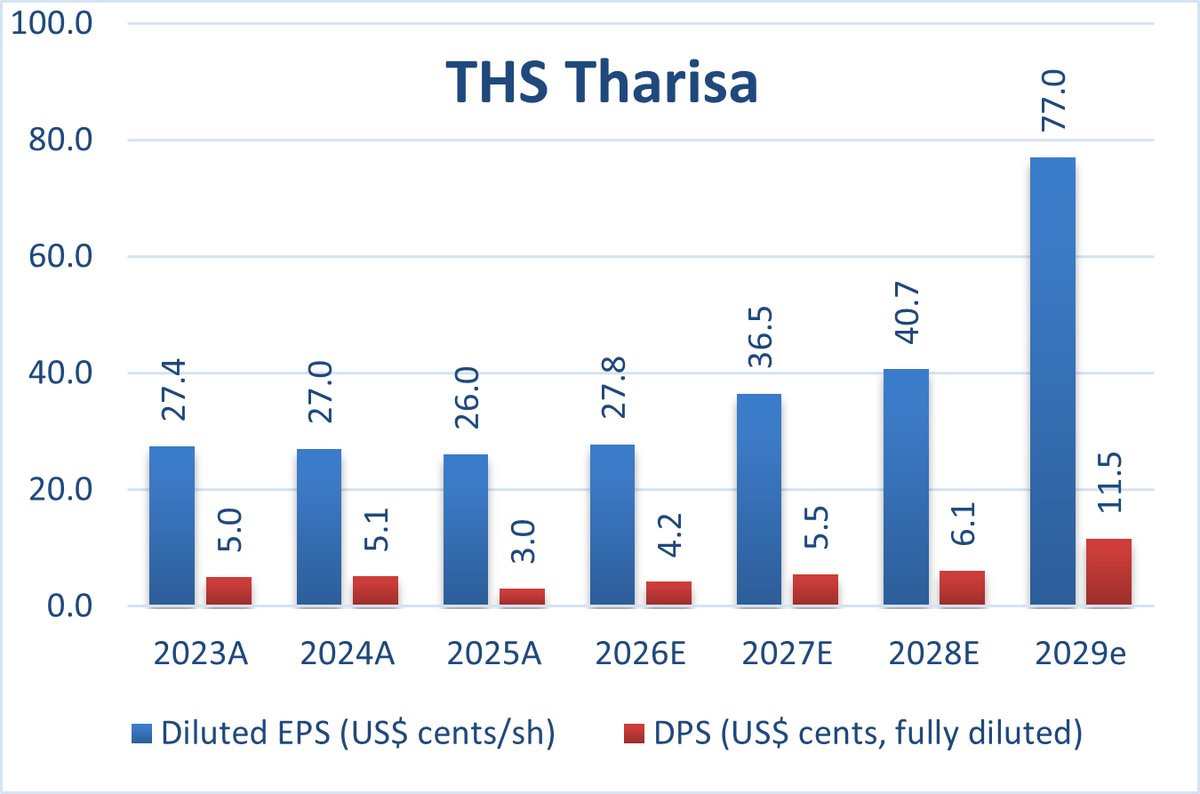

I've added to my positions in #SLP & #THS using divi earnings

Both stocks are far too cheap. I created the following chart for #SLP to illustrate the outlook (current year is in orange).

Similar to #THS earnings are in growth phase due to jump significantly in the next year.

In May 24 I noted that #PAF was about to enter a growth phase in production

#THS Tharisa should see a similar ramp up over the next 3 to 4 years, to illustrate the effect on earnings, I produced a chart using house broker's numbers.

THS currently pays a 4% divi, fPER is 3.9

I think that's a fair summary. It's a bit cliche to say that all politicians are liars, but I think it's fair to say that in the short time they've been in power, quite a few "promises" have been broken.

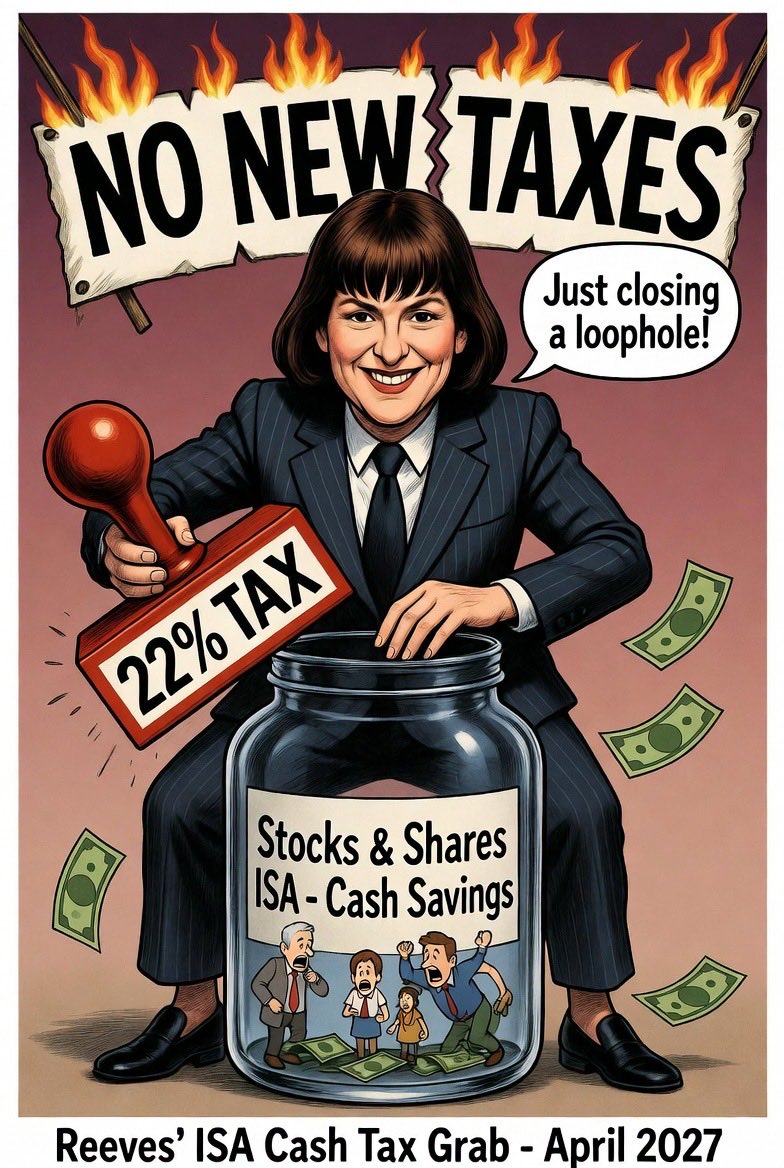

🚨 Rachel Reeves’ “no new taxes” pledge was total, bare-faced bullshit.

From April 2027 she’s hammering

ordinary Brits with a 22% tax on cash interest sitting inside Stocks & Shares ISAs — the one place millions of cautious savers and pensioners thought their money would stay safe.

First she slashed the cash ISA limit. Then she “closed the loophole” by coming straight for whatever cash people left in the stocks version.

This isn’t fixing anything. It’s a deliberate, sneaky raid on people who don’t want to gamble their life savings on the stock market just to keep what they’ve earned.

So much for “no new taxes,” Chancellor. You lied. Again.

This is why nobody trusts Labour with their money — because you always find a way to snatch it anyway.

#ReevesTaxGrab #NoNewTaxesMyArse #LabourStealthTax

According to the latest Insolvency Service data, business administrations in the UK are up 78% compared to the same period last year. This spike is largely driven by macroeconomic pressures.

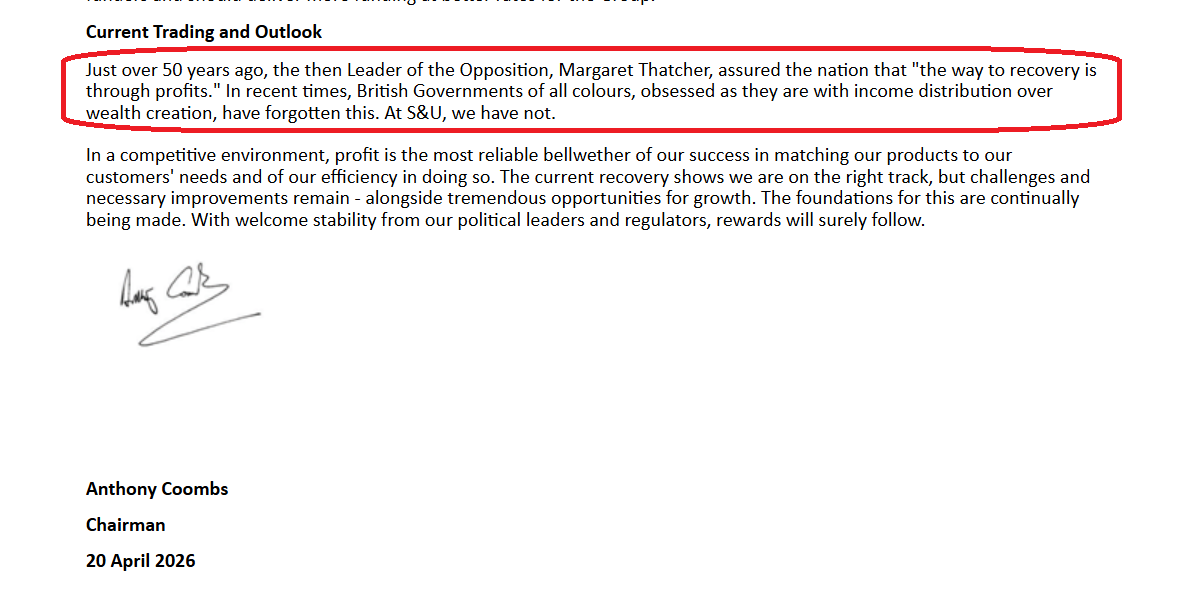

#SUS continues its habit of entertaining trading statements.

(I particularly enjoyed the misadventures bit).

https://t.co/FOMM6WwEVX

..oh and also performing really well in tricky market conditions 👏

#SUS Chair Anthony Coombs wins :

#lse#ftse "Outlook Statement of the day award 🏆👏🍾

...using the tried and tested method of referencing a past champion of business whilst calling-out the incumbent less-friendly government policy.

#CURY top portfolio performer today +15.3%

I took a long hard look at this one recently, considered the wisdom of holding a consumer cyclicals against the current macro. In the end I decided it was just too strong to cut. Brokers continue to upgrade PER of 9 looks modest.

In May 24 I noted that #PAF was about to enter a growth phase in production

#THS Tharisa should see a similar ramp up over the next 3 to 4 years, to illustrate the effect on earnings, I produced a chart using house broker's numbers.

THS currently pays a 4% divi, fPER is 3.9

#PAF Pan African Resources - South African #GOLD producer.

Guidance narrowed to top end today. 2025 will see a ramp up.

It's all in the timing with Miners. Best to buy just prior to the steep incline in production IMO (err...so about....NOW)

#FRP bargain #LSE#FTSE stock.

In line headline, but actually consensus f/c were LOWER than the "at least" figure in todays TS

All sectors have +ve outlook

opposite to the UK economy generally (which is good for FRP's business)

Quality business:

ROCE 28%

BV 5yr CAGR 36%

@greeisgoo I think it needs to show better growth metrics prior to any spin-off. They have added more expertise on selling the product so it could well start showing growth as a result. That in turn would make the sell price much higher.

#TCAP reports trading up strongly in all aspects. I had it a while now to the point it became my largest holding end of April. Despite record trading the share price is yet to regain pre-covid high:

#COST Costain continues to benefit from strong pipeline

Cash pile now at £175

net margin really strong for sector

Valuation still cheap - allowing for cash EV PER is <8

Divi policy rising

Chart I will update in due course - but a long way up to reach prior highs.

#COST Top portfolio performer today

Lots of good news in a detailed update - now a 1 bagger for me!

I won't be topslicing - has a lot of upside IMO. Long term chart shows only just breached 1st fib level tells a story.

Don't focus on the cost, focus on the value!