Gary Becker also wrote this great paper also perhaps relevant for social media...

… I recall when beta-delta and temptation "behavioral" models came around Gary told me he was open to these approaches but just emphasized how lots can be learned with standard rational case.

Let me explain why I believe modern economics is such a powerful tool for understanding the world. I’ll do this by discussing a great paper by Simone Cerreia-Vioglio, @UncertainLars, Fabio Maccheroni, and Massimo Marinacci, “Making Decisions Under Model Misspecification,” published in the Review of Economic Studies a few months ago.

Imagine I want to drive from UC San Diego to UCLA, but I’ve never driven that route before. I need to build a “model of the world” to guide me, which we usually call a map. Maps are simplified representations of reality. They can’t include every detail if they’re to be useful. Borges, in his short story On Exactitude in Science, makes this point beautifully. (In practice, I don’t draw the map myself—I use an app—but someone still had to make it.)

Because maps simplify, I can’t fully rely on them. Maybe last night’s storm knocked down a tree and closed a street, or there’s construction and the ramp off the highway in LA is shut down.

This uncertainty matters. Suppose I’m driving to UCLA for an important talk at 11 a.m. If the ramp is closed, I might need 15 extra minutes. When should I set my alarm to arrive on time, while still getting enough sleep to give a good talk?

The problem is that I can’t assign precise probabilities to all these contingencies. How likely is the fallen tree? Or new roadwork? Even the best traffic apps can’t capture every disruption, and some might happen after I’ve already left.

In economic terms, my “model of the world” (the map) is misspecified—and no matter how hard I try, I can’t fully fix that.

But sitting down and crying about misspecification doesn’t answer my basic question: when do I set the alarm? Too early, and I’m exhausted. Too late, and I’m late.

Simone and his co-authors offer a way to think about this. They start from the idea that we often hold several structured models of an economic phenomenon, grounded in theory. For example, a central bank might use a standard New Keynesian model and a search-and-matching model of money.

Yet, aware that each model is misspecified by design, the bank adds a protective belt of unstructured models—statistical constructs that help it gauge the consequences of misspecification.

The beauty of the paper is that it provides an axiomatic foundation for this protective belt (and even generalizes it to include a Bayesian approach). It shows that if a decision-maker’s preferences meet certain conditions —reflecting both rational and behavioral features— then those preferences can be represented by an augmented utility function that formally accounts for misspecification.

Crucially, we don’t assume that augmented utility function; we derive it. We start with general, plausible properties of preferences and prove that they imply such a representation.

That’s real progress. Instead of writing endless critiques of expected utility or rational expectations (as many have done for decades, with little to show), we now have a formal way to reason about misspecification—precise definitions, clear boundaries of validity, and awareness of what we still don’t know.

Take, for instance, a brilliant Penn graduate student on the market, Alfonso Maselli

https://t.co/rl2gu95V7t

His job-market paper pushes this frontier further. He studies cases where a decision-maker not only faces model misspecification but is also unsure which model best fits the data and can’t assign probabilities to them—what we call model ambiguity. In my example, the central bank is unsure whether the New Keynesian or the search-and-matching model fits better, and it worries that both might be incorrect.

If you read Simone et al. or Alfonso’s paper, you’ll see how misguided—and, frankly, cartoonish—many of the recent criticisms of economics on X have been.

First: the idea that economists don’t understand math or have “physics envy.” The math in these papers is subtle and advanced—utterly different from what physicists do (neither better nor worse, just distinct). An engineer transitioning into economics would find these tools unfamiliar.

Second: claims of ideological bias are unfounded. I have no idea about the political views of the authors, and I’d be surprised if anyone could infer them from the analysis—beyond vague guesses about typical academics.

Third: This has almost nothing to do with what one learns as an undergraduate, or even in first-year graduate school. If your knowledge of economics stops at an intro textbook, it’s best not to pontificate on the field’s frontiers.

Fourth: Is this science? Debating that word’s boundaries is pointless; every definition of “science” breaks down somewhere.

The Germans solved this long ago with the idea of Wissenschaft—the systematic pursuit of knowledge, whether of nature, society, or the humanities. By that measure, modern mainstream economics is clearly a Wissenschaft: a disciplined, cumulative, and highly useful effort to understand how the world works. Simone and his co-authors have demonstrated that beyond any reasonable doubt.

@PANCHOBH@IndianExpress@the_hindu@NKSingh_MP The Hindu article takes a static view of what everyone already knows, viz. that Bihar ranks last in per capita NSDP. The IE piece adds a dynamic lens, focusing on income 𝐠𝐫𝐨𝐰𝐭𝐡 and where Bihar could be headed, while still recognizing the state’s long-standing challenges.

In memory of Stanley Fischer, Economics in the Rear-view Mirror has posted a 1973 caricature of assistant professor Fischer in his U of Chicago days drawn by the graduate student Roger Vaughan. https://t.co/fMVZ6NYR8l

RIP Daniel W. Stroock (1940–2025): https://t.co/DKYAmIv8LR

He was a fundamental contributor to Malliavin calculus and the theory of diffusion processes.

[h/t Barry Simon]

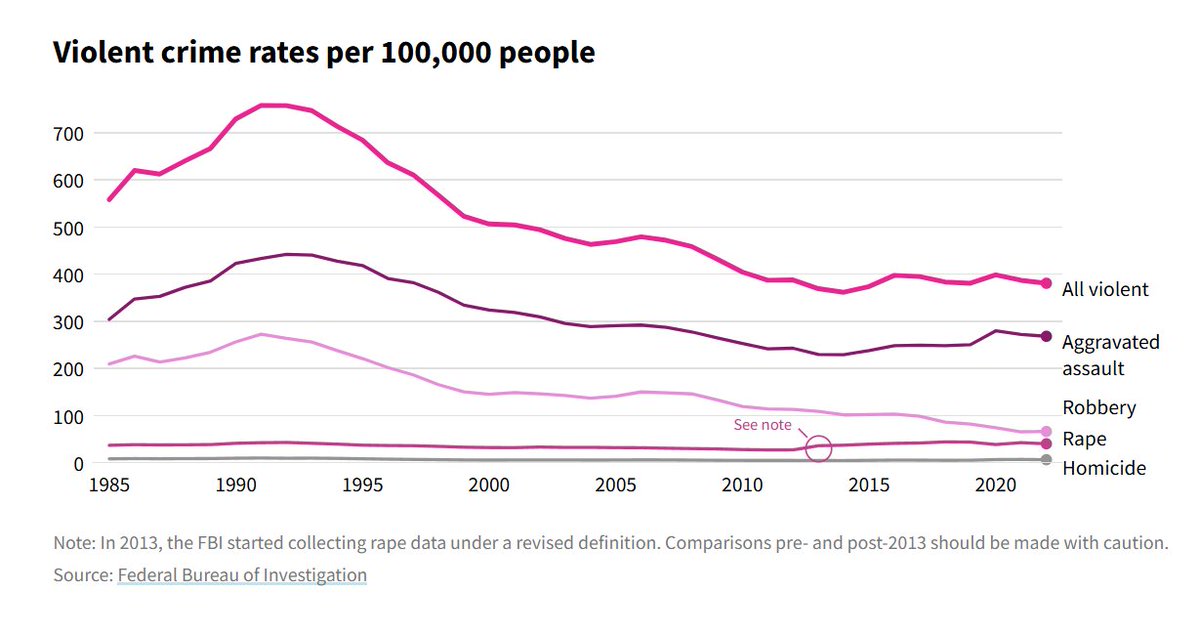

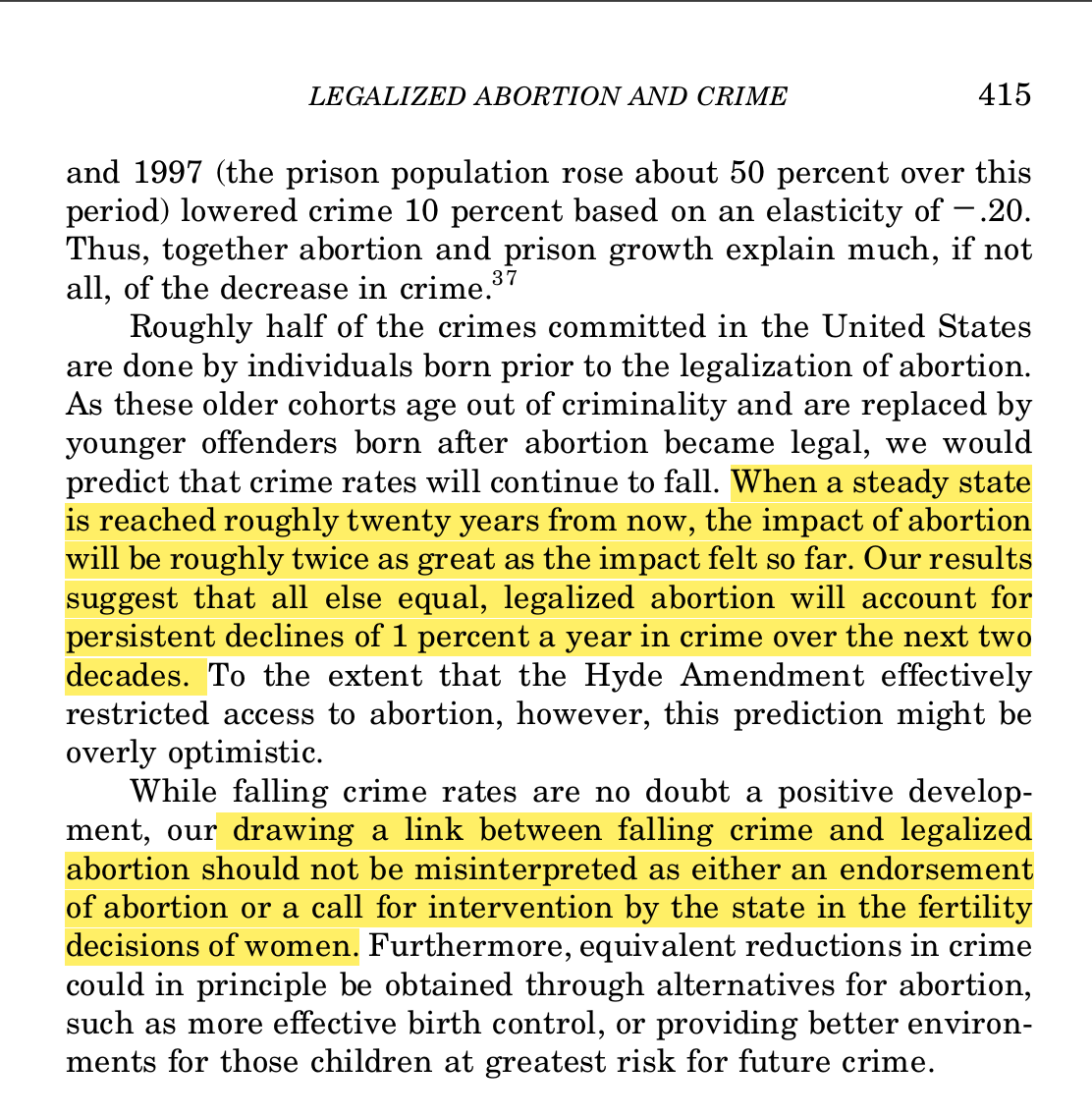

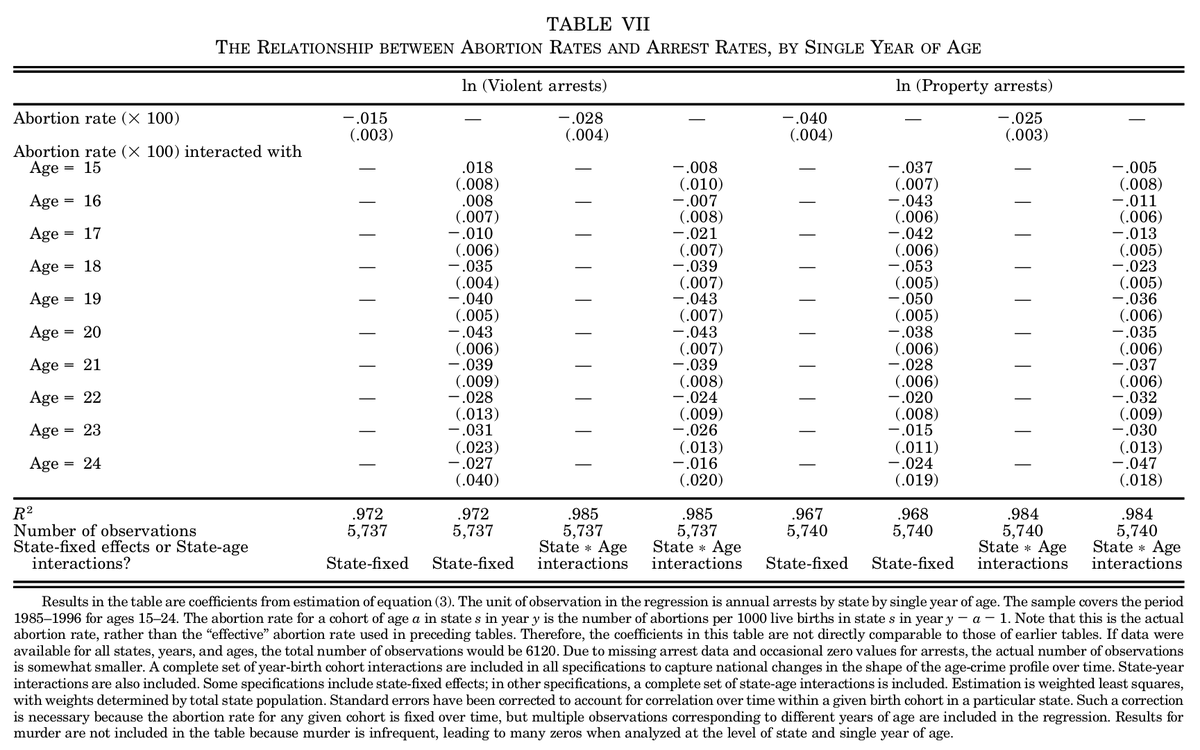

The authors clarify that their intention is not a political move toward any one direction in the Roe v Wade debate.

But it is fascinating to see their predictions, made in 2001, hold up against the test of time.

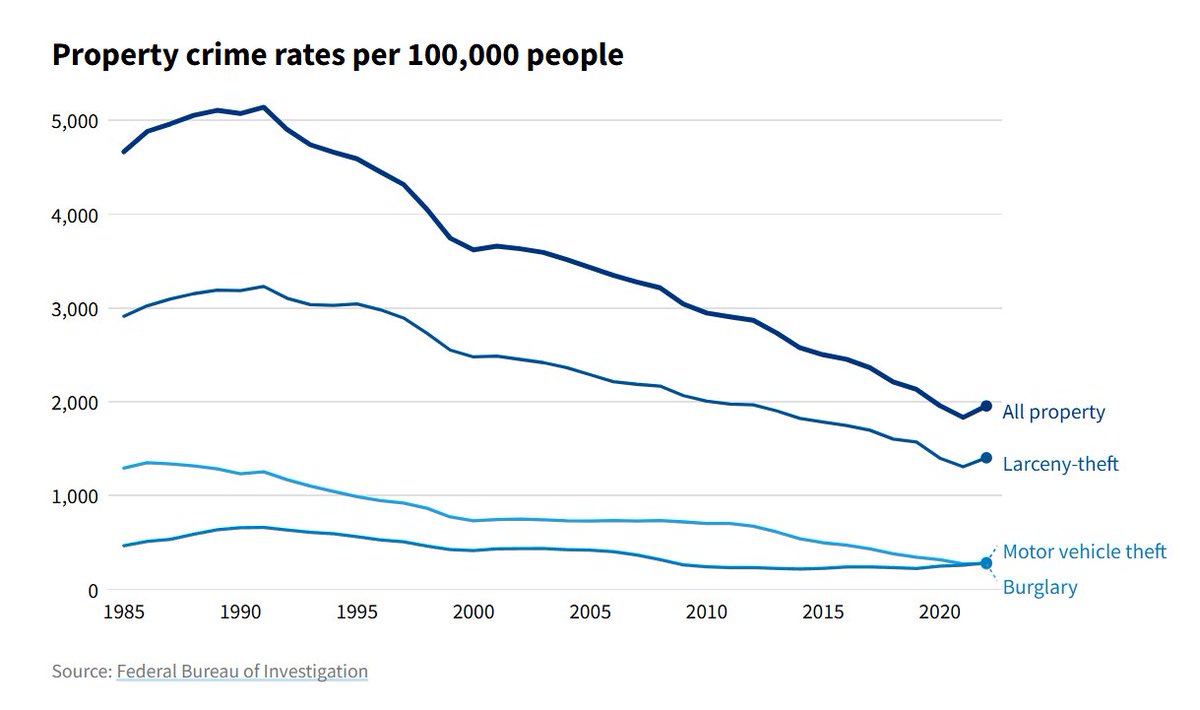

Look at the drastic drop below, what happened over the decades?

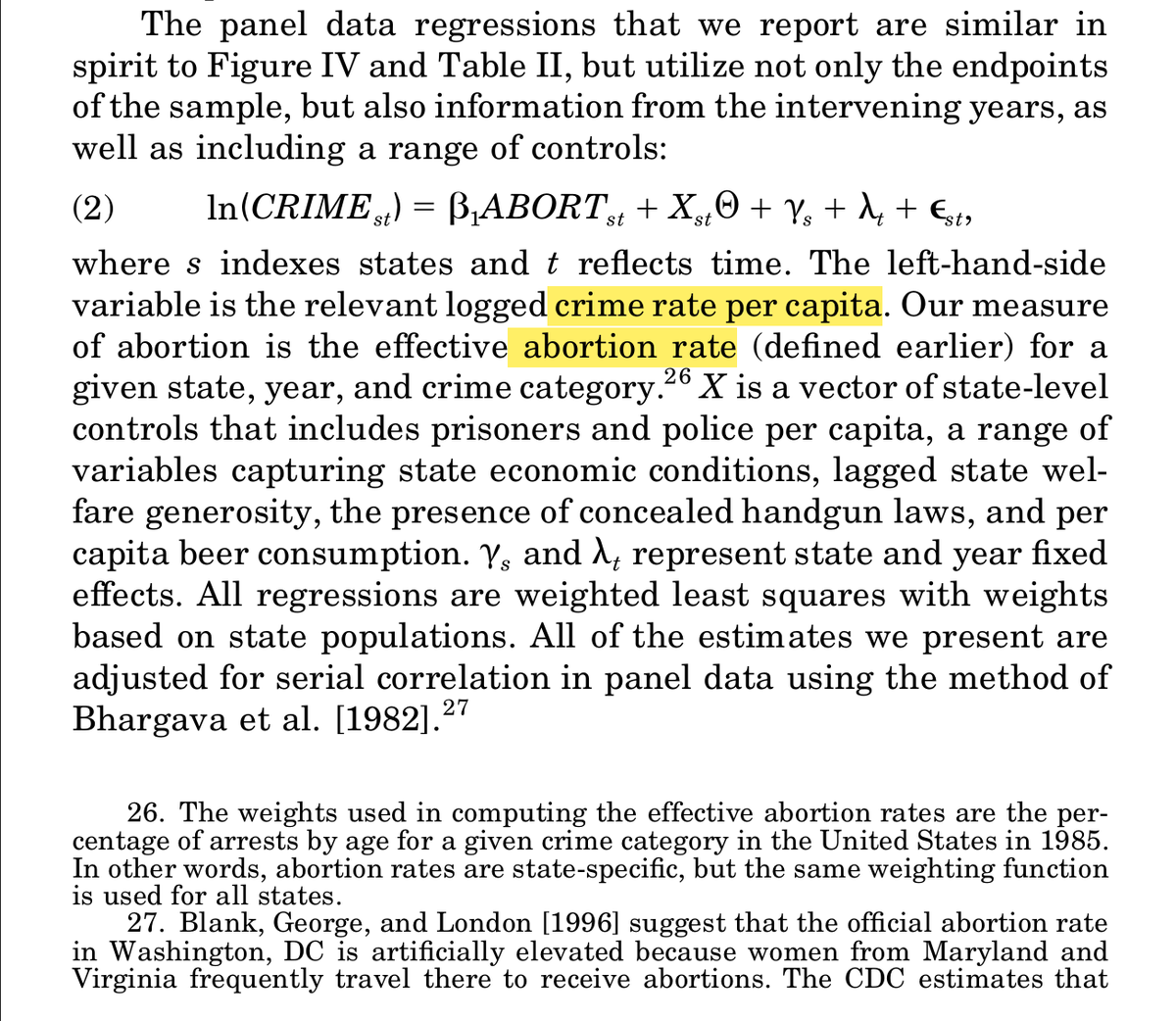

We will revisit the paper that inspired the chapter on Roe v. Wade in Steven D. Levitt's Freakonomics (2005).

This is a story of the criminal "population".

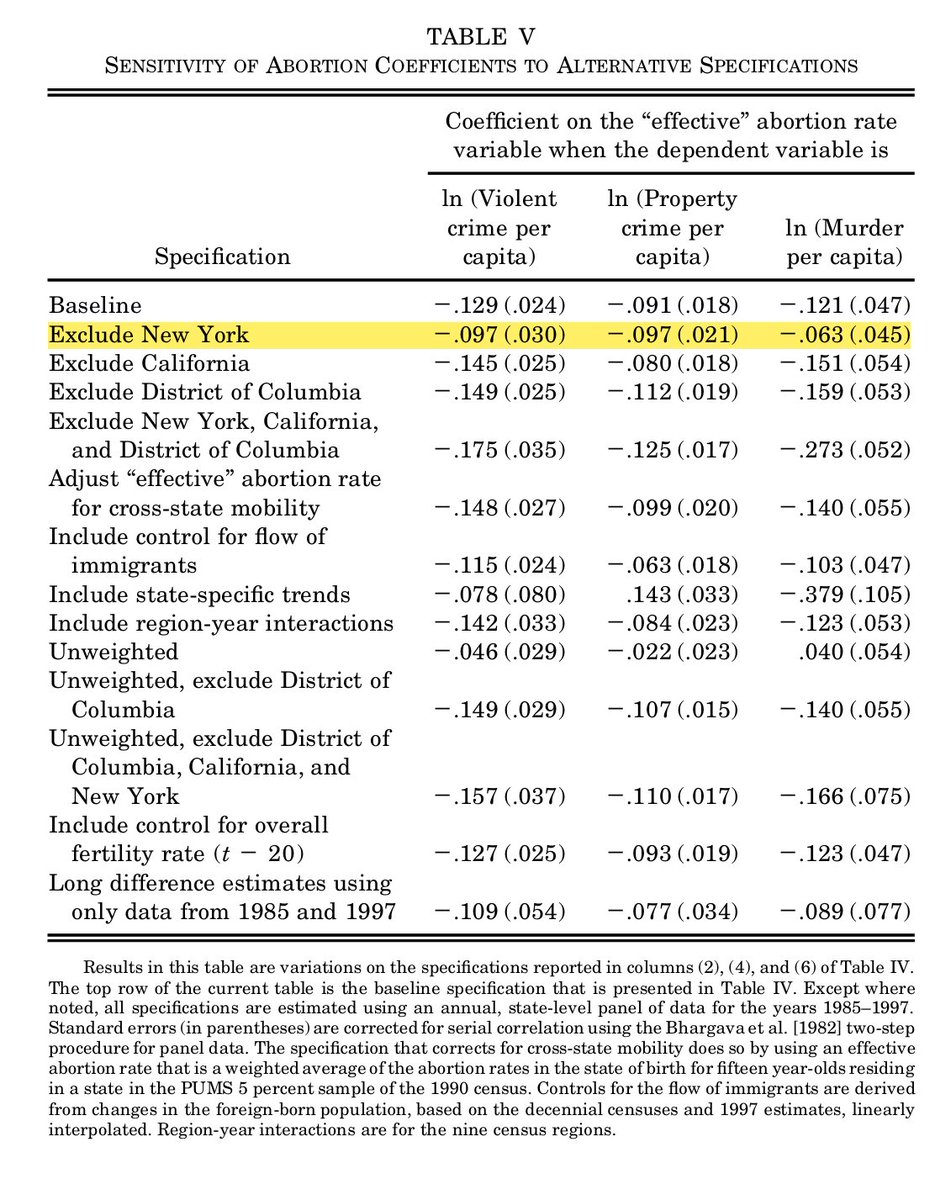

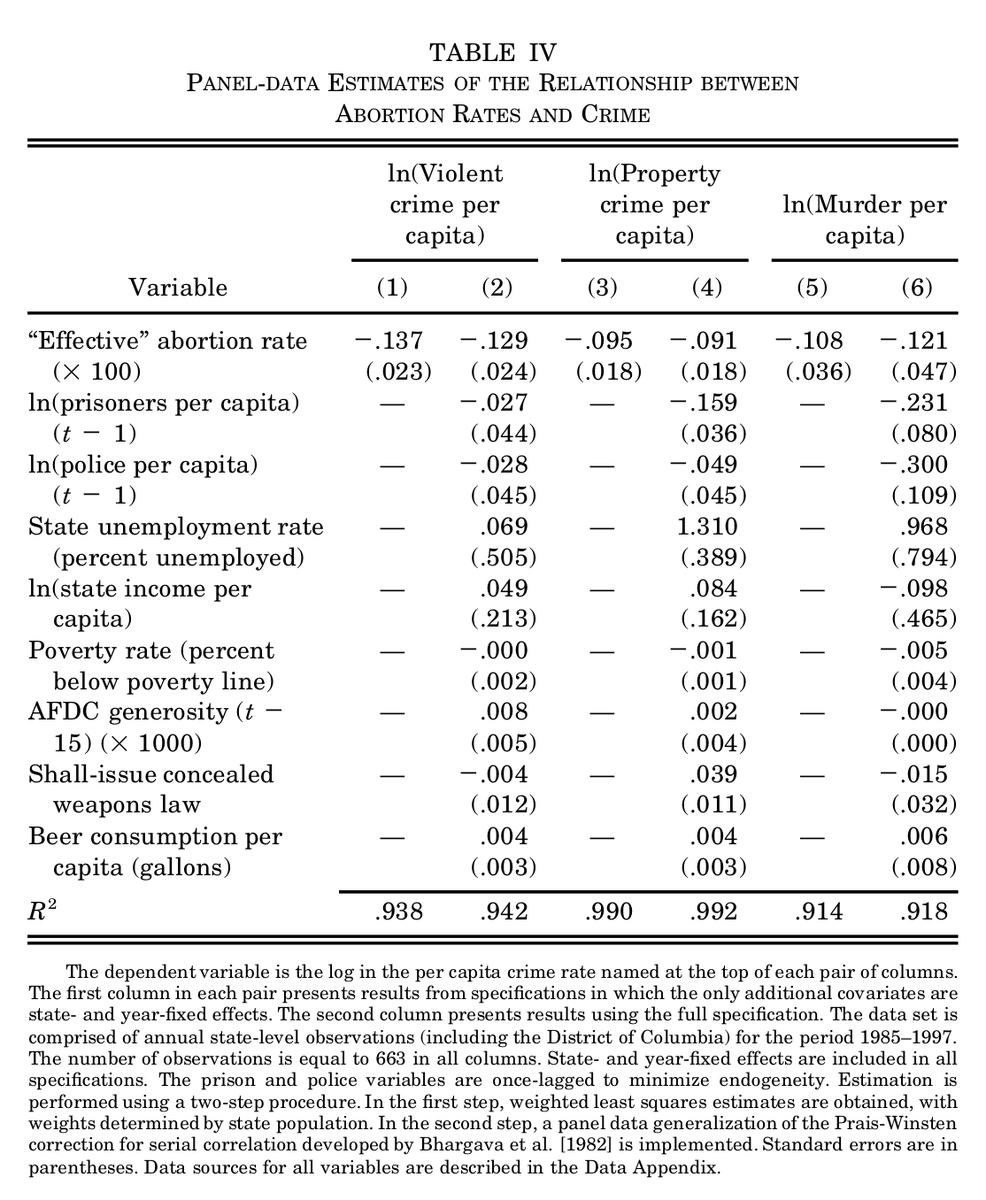

The patterns hold across the many controls and covariates they include in their regression specification, involving both the crime rate and arrest rate as the dependent variable.

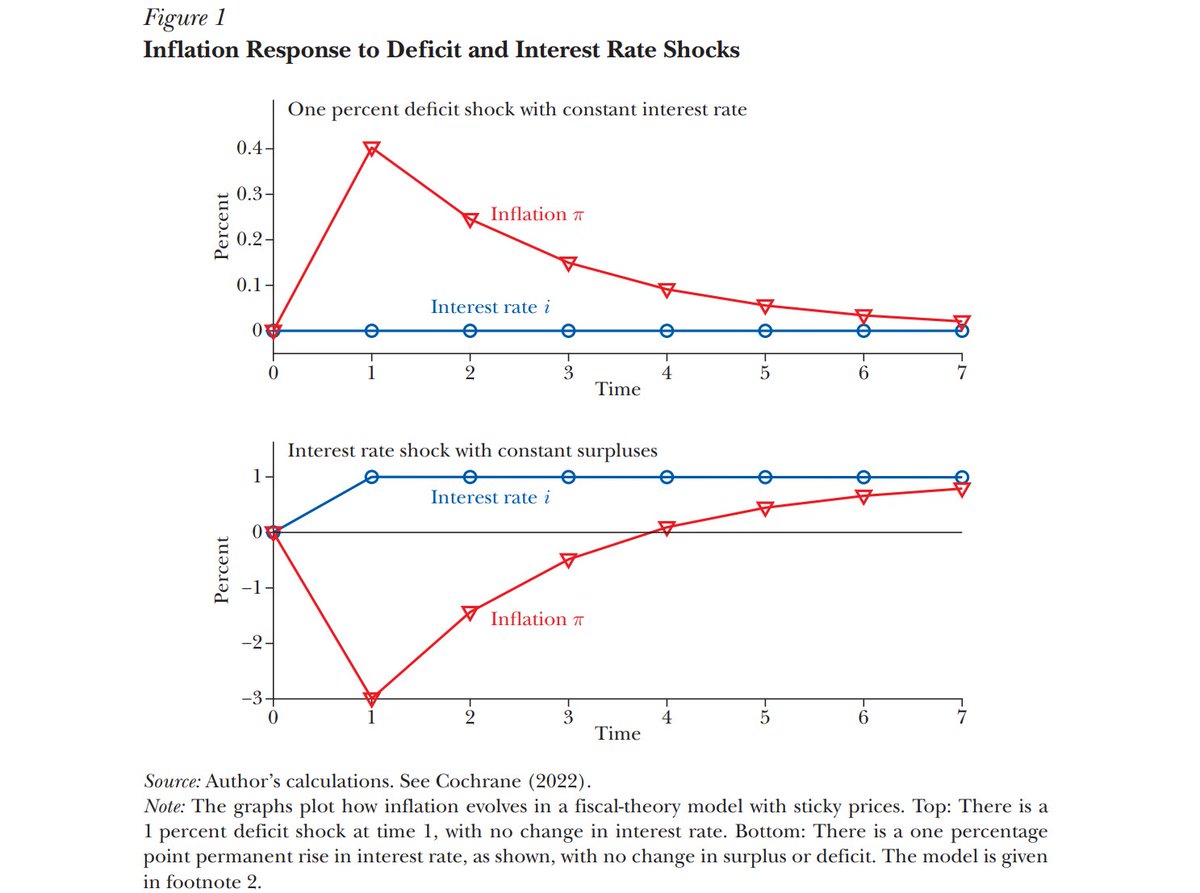

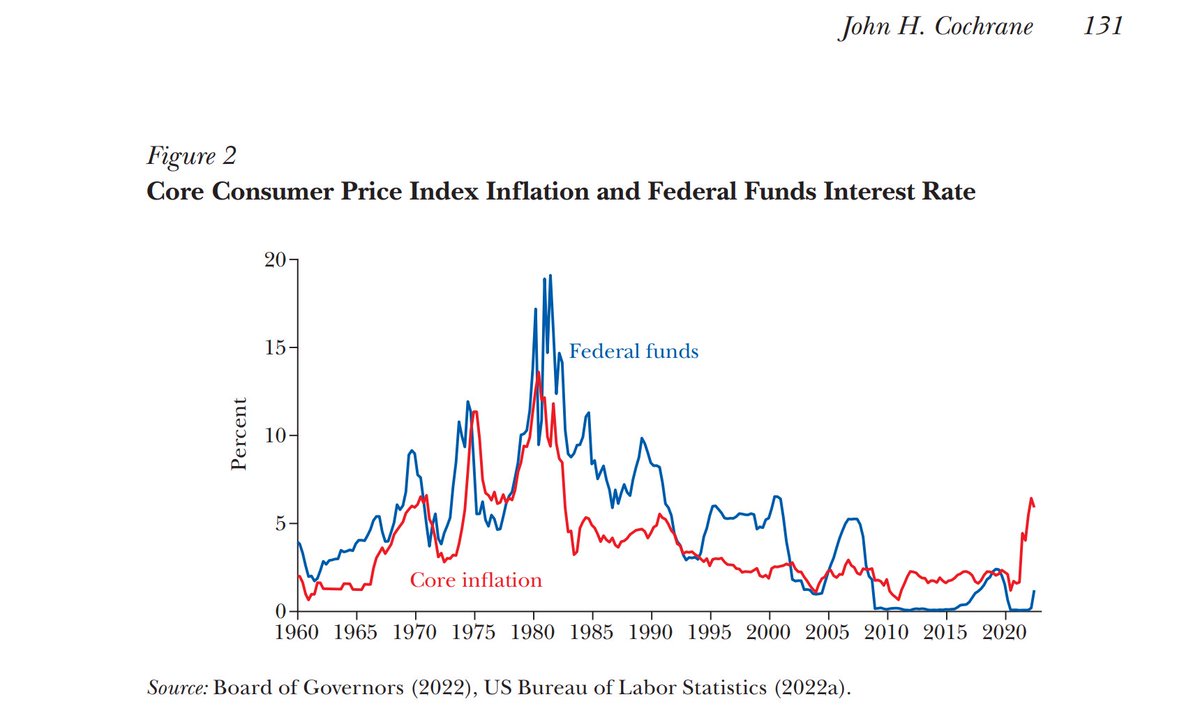

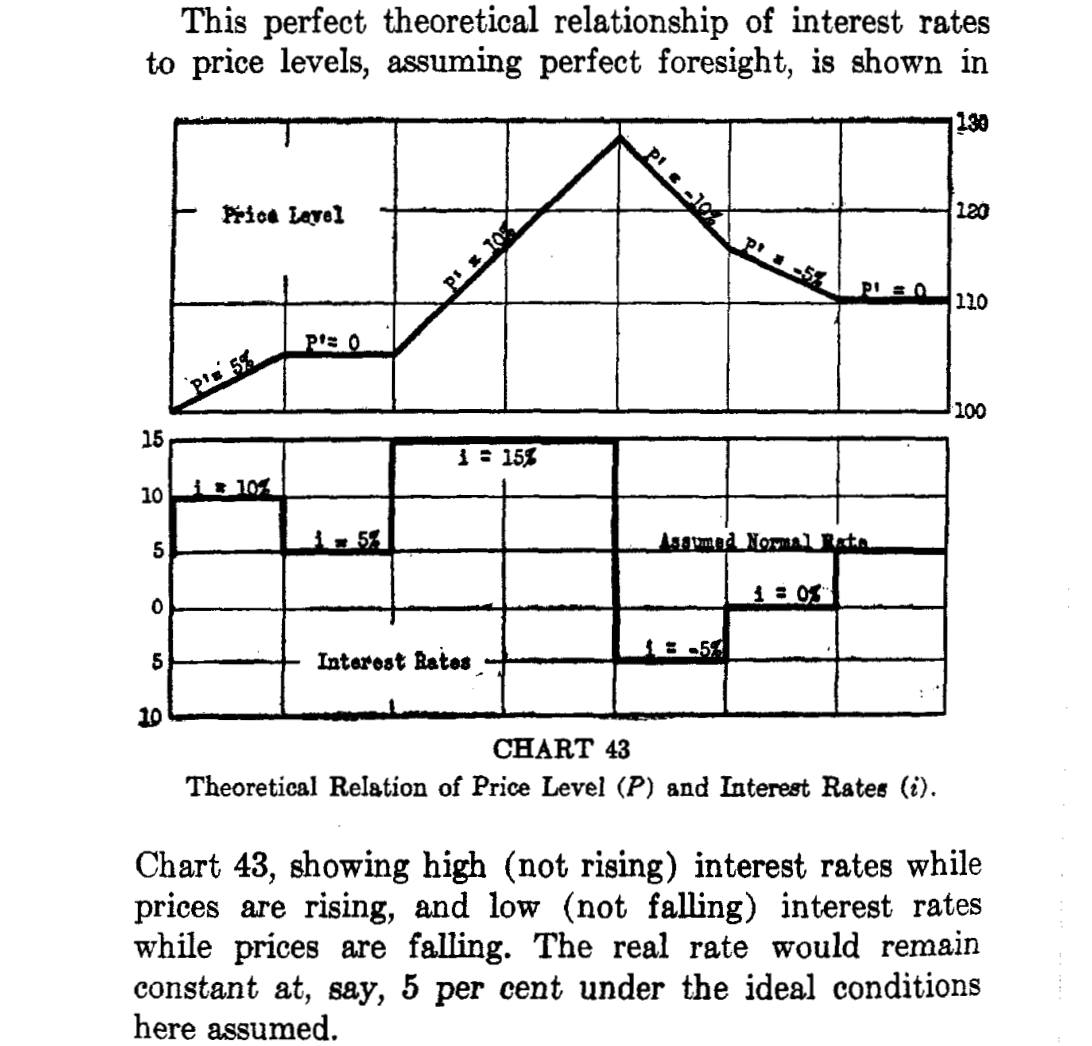

John Cochrane illustrating the Fisherian view -- that raising interest rates raises inflation.

Cochrane, John H. 2022. "Fiscal Histories." Journal of Economic Perspectives, 36 (4): 125–46.

https://t.co/dbR92sRZhY

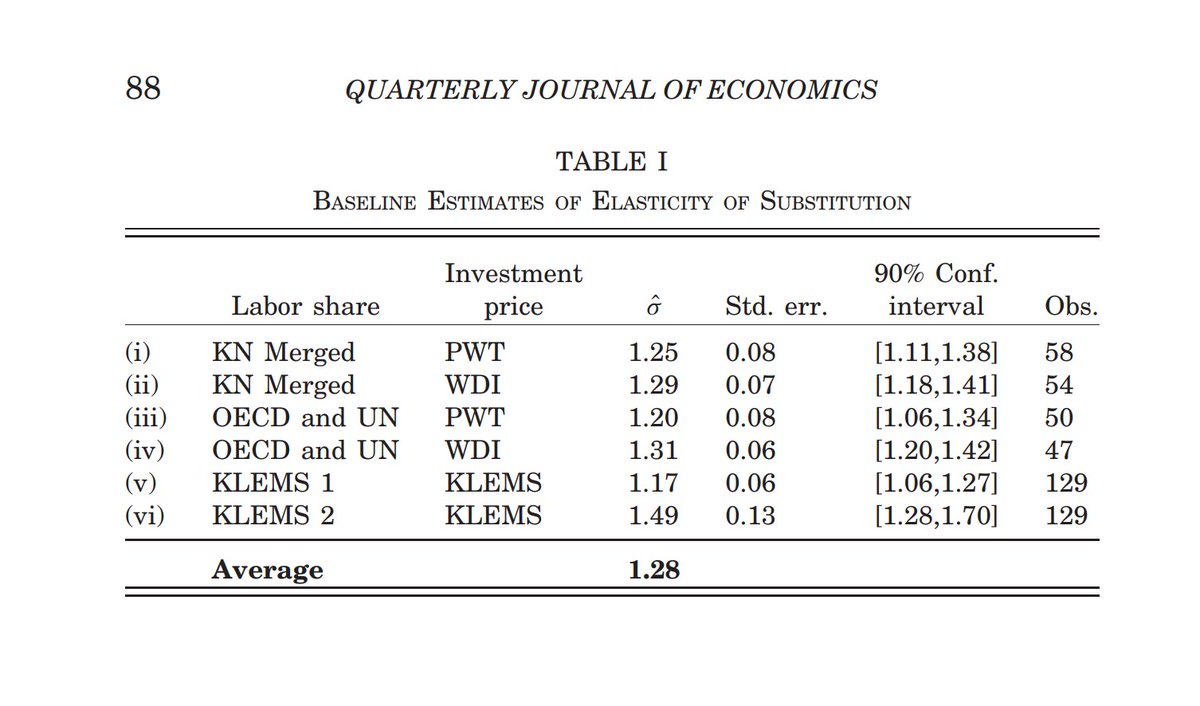

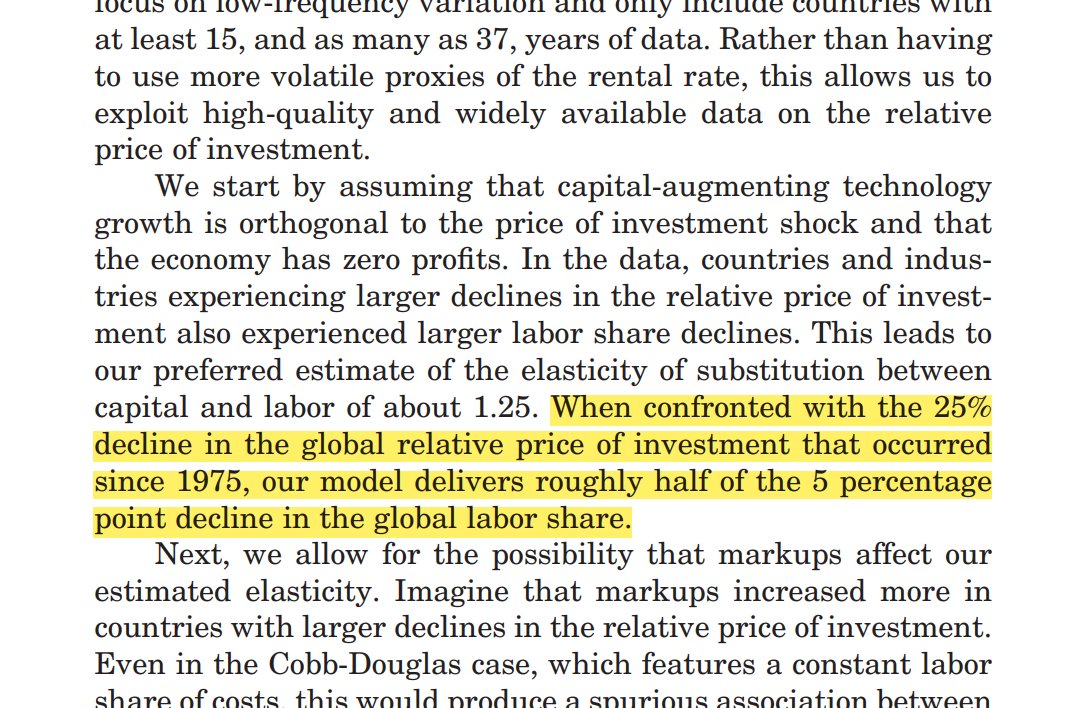

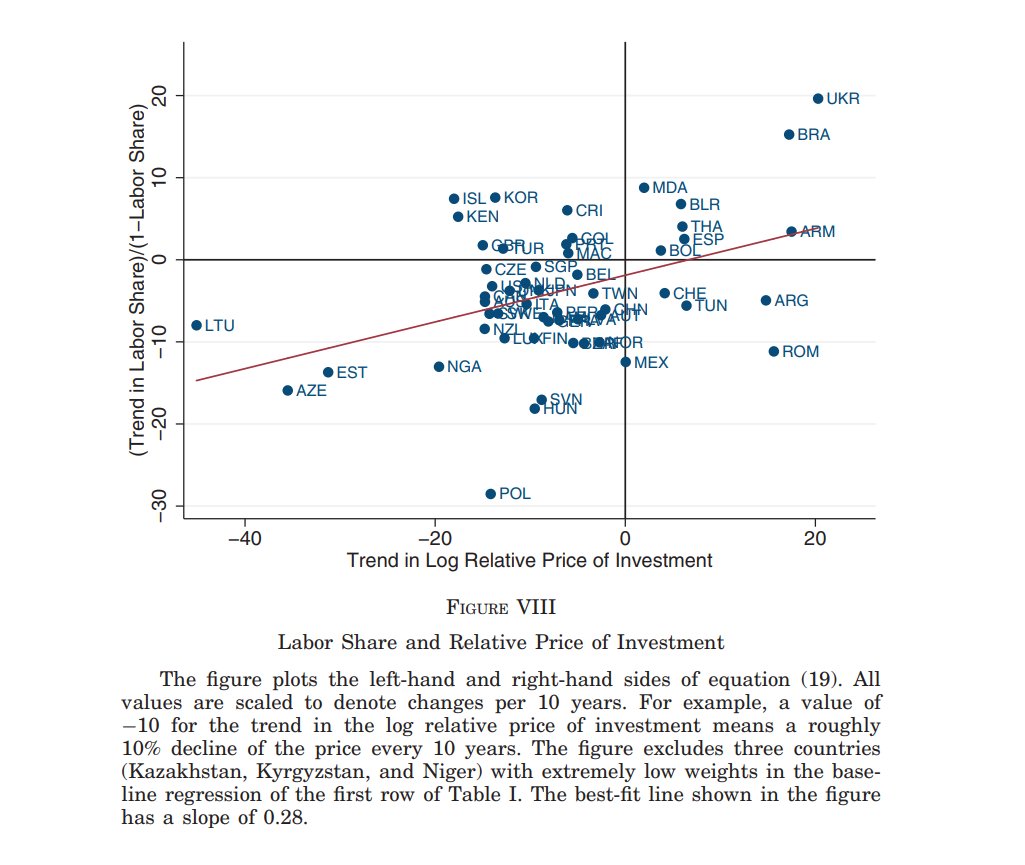

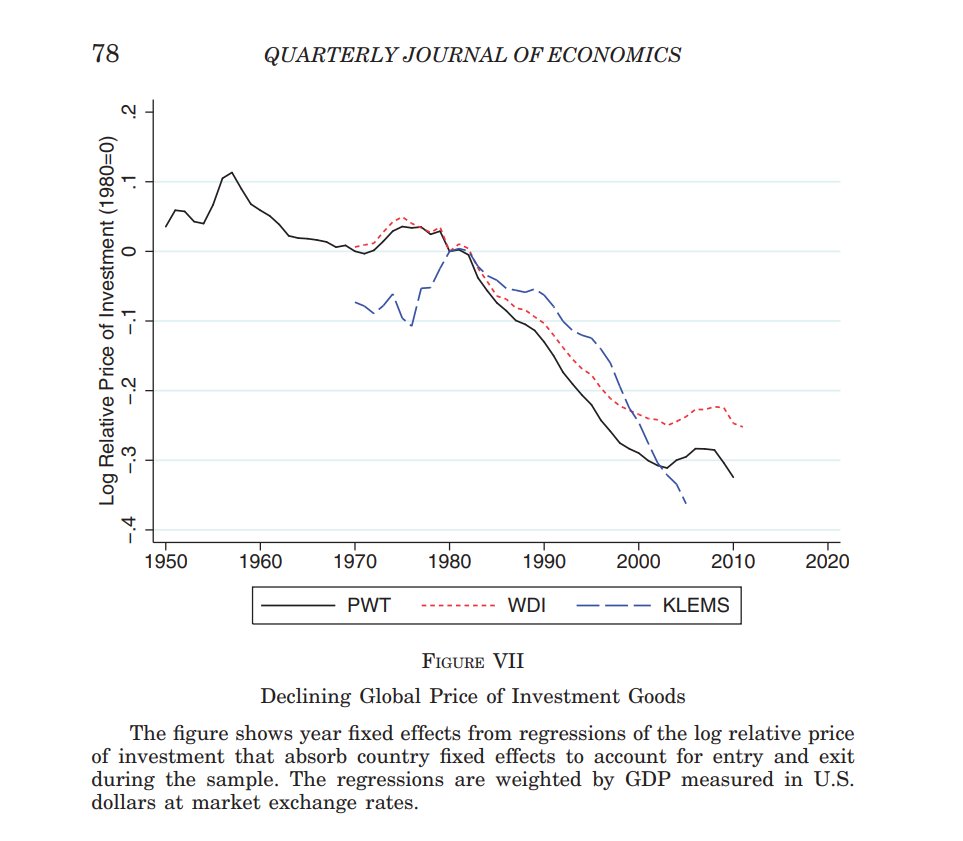

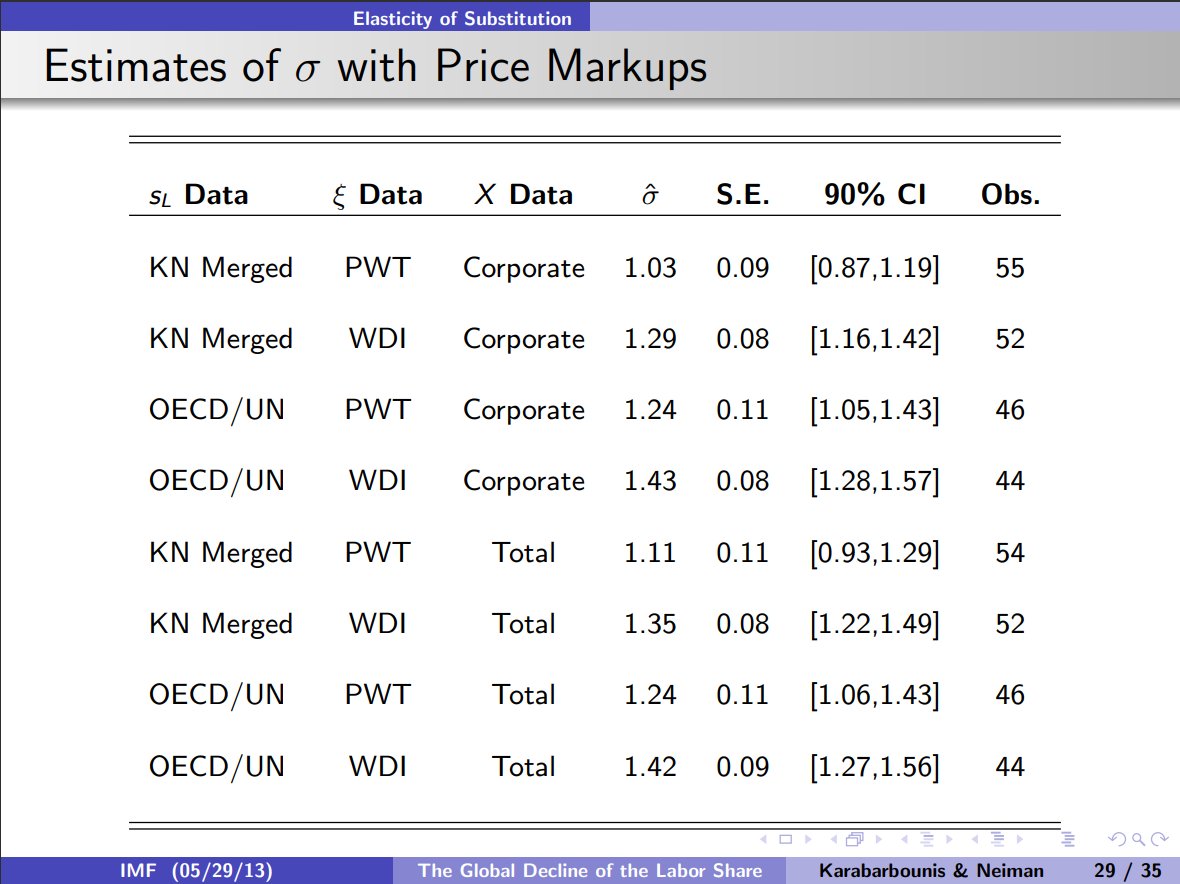

Karabarbounis, L., & Neiman, B. (2013). The Global Decline of the Labor Share. The Quarterly Journal of Economics, 129(1), 61–103.

https://t.co/jHvqobHWKl

Through a model, the authors postulate the impact of declining relative price of investment (decrease of cost of capital) on the declining labor shares across countries.