Energy infrastructure and AI compute are converging.

PowerBank Corporation Nasdaq: $SUUN | Cboe CA: $SUNN announced plans to expand its strategic focus into AI compute infrastructure and modular data center development alongside solar and battery storage.

@powerbankcorp

Link: https://t.co/Tah4ot5Wnq

#RenewableEnergy #AIInfrastructure #DataCenters #SUUN

$SUUN tickers to $PBK tomorrow

solar → battery storage → AI data centers

1GW pipeline. modular compute LOI. IPP revenues +1,508%.

most overlooked AI infra name right now imo

🧵

---

2/ the evolution:

$SUUN → $PBK (June 3, 2026)

this isn't just a rebrand. the entire strategic thesis has shifted

they're positioning as vertically integrated energy + compute — owning the power source AND the infrastructure that runs on it

---

3/ why this actually matters for AI infra:

the biggest bottleneck for AI data centers right now isn't chips — it's power

grid capacity is years away in most markets

PowerBank's angle: co-locate modular data centers directly at their existing solar + BESS sites

no grid queue. no permitting from scratch. Speed-to-Power.

---

4/ the Nodiac LOI (April 2026):

Nodiac deploys modular, containerized data centers at sites that already have generation, land, and permits

PowerBank feeds them the sites. Nodiac brings the compute.

site-by-site definitive agreements still TBD — early stage, but the framework is real

---

5/ the fundamentals backing the pivot:

• 1GW+ North American development pipeline

• 100MW+ already built and operating

• IPP revenues +1,508% YoY to $9.3M

• Ontario BESS project now live

• NY solar + storage projects in execution

this isn't a blank-check pivot — there's real infrastructure underneath

---

6/ the risk:

Nodiac LOI is non-binding. no definitive agreements signed yet.

still loss-making. execution on the AI compute vertical is unproven.

if the data center angle doesn't materialize, you're left with a small renewable developer trading on a story

size accordingly

---

7/ the setup:

ticker change tomorrow = first time $PBK shows up on screens

algo flags, new search hits, fresh eyeballs

for a name this small, that's a real catalyst

Buying the dip and aiming for a multiplier

$SUUN $PBK #AIinfrastructure #smallcaps

Faster compounds:

$AAOI - 10x revenue ramp from optical transcivers h2 2027

$NBIS - 10x revenue ramp Q4 2026

$ARM - 5x revenue growth from their new AI CPU

$MRVL - 2-3x revenue growth from $MSFT Maia Ramp.

$AVGO - Long hyperscaler ASIC

$LITE - Long OCS / Google TPU

Win Semi - Foundry exposure to frontier industries

$TSEM - Long photonics, backlogged

SK Hynix - Memory exposure, extreme operating income ramp

With some barbell exposure away from Hyperscaler capex aside from Amazon:

$VNP - Long term rare earths for Western Supply chains

$NEO (TCX) - Robotics Supply chains

$AMZN - Robotics/AI cutting opex

$CRCL - Stablecoin long

$RDDT - Ridiculously high profit

$GLD - Safe Hedge

$IBIT - Halving 2028

$CVX Calls - Oil Hedge

And maybe long term (you know it's coming):

$INTC / $AMKR- Made in America supply chains

$SOI - Silicon Photonics / CPO substrates.

$RKLB - Long term call on Space industry

Then pick one or two small cap moonshots:

$SIVE - CW Laser Chokepoints or $IQE for Landmark rerating on restructuring were my two favorites.

There's others I've mentioned like $AEHR for testing or $VPG for Optimus.

How I actively manage my own stuff from $AXTI and others is a lot different risk profile than what others should do.

Going full port into high-beta in this macro environment is not the best idea.

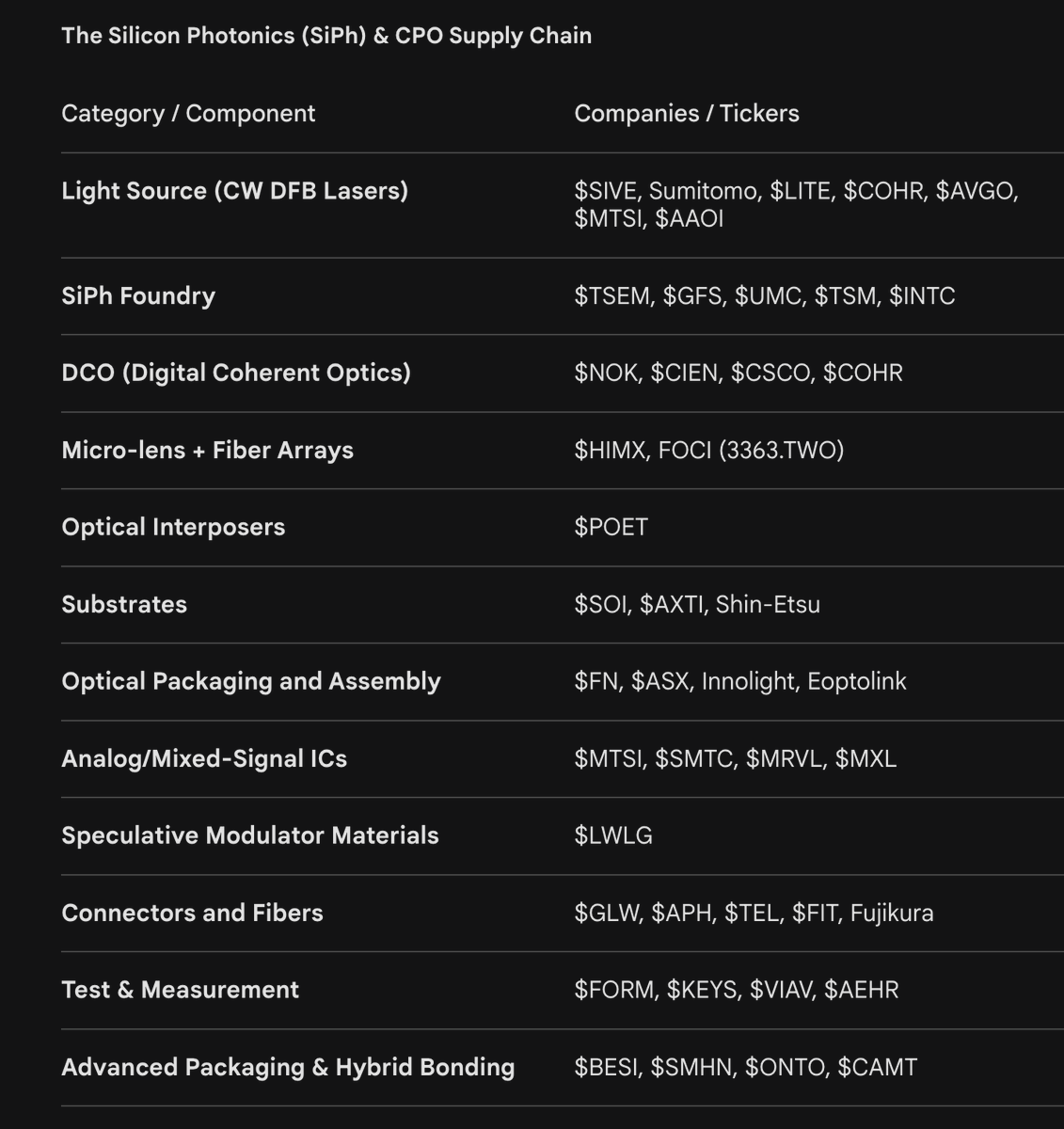

The upcoming CPO / Silicon Photonics Bottleneck Cheat Sheet:

$SIVE, Sumitomo, $LITE, $COHR, $AVGO, $MTSI, $AAOI - Light Source (CW DFB Lasers)

$TSEM, $GFS, $UMC, $TSM, $INTC - SiPh foundry

$NOK, $CIEN, $CSCO, $COHR - DCO

$HIMX, FOCI (3363.TWO) - Micro-lens + Fiber Arrays

$POET - Optical Interposers

$SOI, $AXTI, Shin-Etsu - Substrates

$FN, $ASX, Innolight, Eoptolink - Optical Packaging and Assembly

$MTSI, $SMTC, $MRVL, $MXL - Analog/Mixed-Signal ICs

$LWLG - Speculative Modulator Materials.

$GLW, $APH, $TEL, $FIT, Fujikura - Connectors and Fibers

$FORM, $KEYS, $VIAV, $AEHR- Test & Measurement

$BESI, $SMHN, $ONTO, $CAMT - Advanced Packaging & Hybrid Bonding

Many are private companies from Lightmatter, Ayar, Ranovus and others.

Now... Everyone is asking... How do you profit?

If you look at the forecast for CPO TAM, it's a straight line up, and next year is inflection point for CPO mass deployment.

The alpha is capturing the rotation:

From the current EML bottlenecks ( $LITE, $COHR type) to SiPh / CW DFB architectural winners for CPO.

Highest upside potential are the ones that aren't included in current cycles.

But that are in the next.

Companies like $SOI, $SIVE, or $AEHR are perfect examples.

Ride the current pluggable bottleneck like $AAOI.

But the alpha is frontrunning institutions with the next CPO bottleneck.

The capital rotation is inevitable.

3 HIDDEN BANGER 🔥

$AEHR

Silicon Carbide is eating the EV world alive - and Aehr Test Systems is the company making sure every single chip actually works before it hits your car. No Aehr = no quality control. They’re the invisible backbone of the EV revolution. Slept on. Not for long.

$AAOI

Applied Optoelectronics is riding the AI data center wave HARD. They make the laser components that move data at the speed of light inside hyperscale data centers. Every time you use ChatGPT, something AAOI-adjacent is working overtime.

$AXTI

AXT Inc. grows the exotic semiconductor substrates - Indium Phosphide, Germanium, Gallium Arsenide - that power 5G, fiber optics, and space tech.

Not financial advice.

Elon is completely right when he sounds the alarm that power/grid is vital for US dominance in AI.

My call for the once in a lifetime run for $XLU (grid/power utilities ETF) is playing out real time.

New calls are already up ~100%+ in the week alone.

Power generation and the grid is a measurement of industrial capacity and the US has every motivation to modernize and expand it.

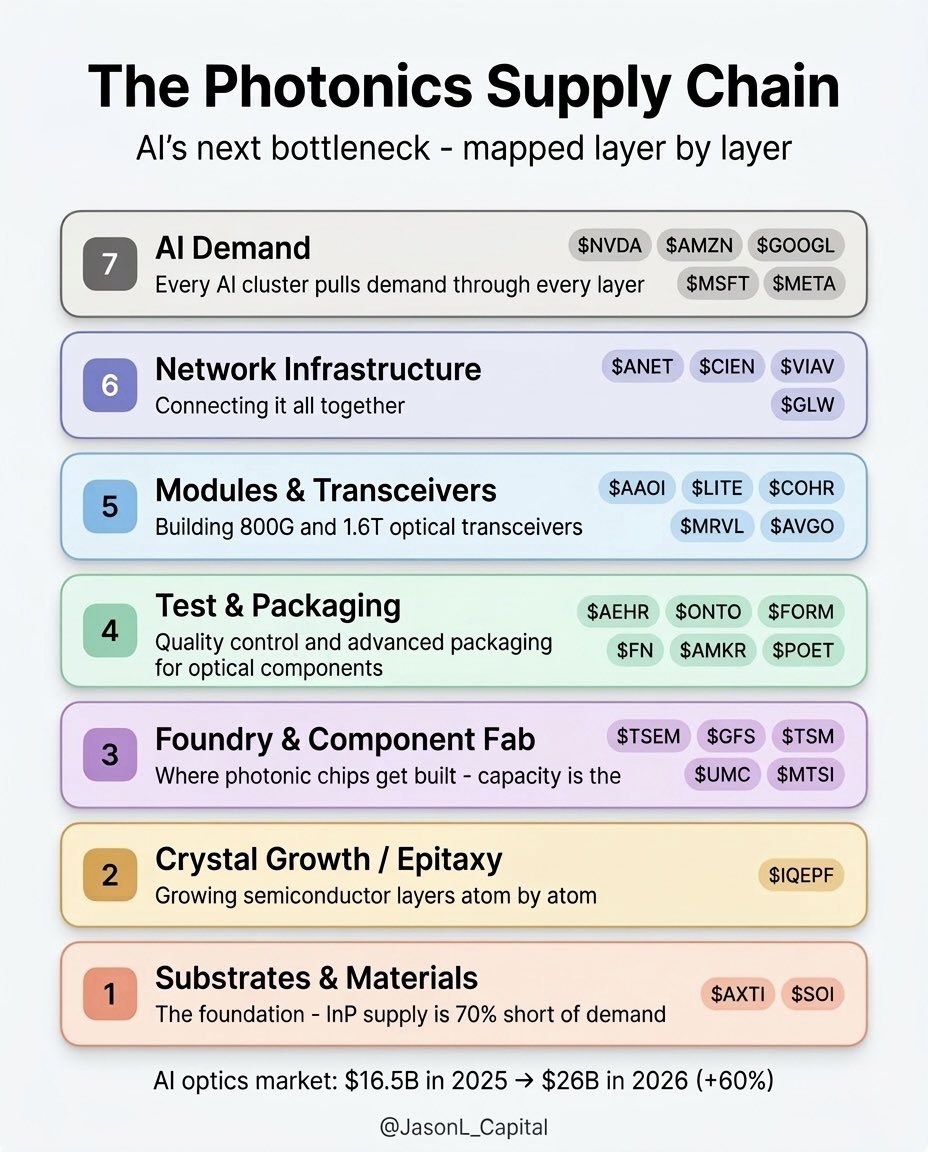

Since you asked for it here it is the full photonics map..

Photonics is the nervous system of AI infra.

GPUs like $NVDA and accelerators from $AMD do the compute. But once you scale to thousands of chips inside hyperscaler clusters ( $GOOGL, $MSFT, $AMZN, $META), the real bottleneck becomes how fast those chips talk to each other. That’s optical interconnect, moving data with light instead of copper.

Why this matters now:

AI models have exploded in size. When you train at scale, network bandwidth and latency become the constraint. Copper can’t handle the power and heat at 800G and 1.6T speeds. So hyperscalers are aggressively shifting to optics.

That shift cascades through layers:

Layer 1 – InP substrates

Light starts with indium phosphide. Players like $AXTI sit here.

Layer 2 – Epitaxy (growing laser wafers)

This is where laser structures are formed. $IQEPF and $COHR operate here.

Layer 3 – Laser chips (EML / CW lasers)

The actual light sources. $LITE, $COHR, $MTSI, $AVGO.

Layer 4 – Silicon photonics foundry

Where light is routed and modulated on chips. $TSEM, $GFS, $INTC

Layer 5 – Integration / optical engines

Combining lasers and silicon photonics. $POET, $ALMU.

Layer 6 – Test & burn-in

Ensuring reliability at extreme speeds. $AEHR (wafer-level burn-in), $FORM (probe), $KEYS (measurement).

Layer 7 – Transceiver modules (800G / 1.6T)

The pluggable units deployed in racks. $AAOI, $LITE, $COHR, $FN.

What’s happening structurally:

Demand is outrunning supply. Companies like $COHR are expanding InP capacity. $AAOI has said revenue is constrained by production, not demand. There’s a global laser shortage.

When that happens, margins migrate upstream. The tightest layer in the stack gets pricing power first.

Most investors focus on Layer 7 (modules). The real leverage often sits deeper — InP capacity ( $AXTI), epi supply ( $IQEPF), laser scaling ( $LITE, $COHR), and yield control ( $AEHR).

Photonics isn’t just “another AI trade”

It’s the physical constraint that determines whether AI clusters actually work at scale.

$AXTI has now reached the Moon if you listened anon?

Markets are scrambling to get exposure to photonics supply chains following $GOOGL record capex numbers.

If you ask an AI: “Is AXT or IQE part of Google TPU supply chains”:

- It will say no due to obscured multi-hop connections.

But if you map the flow from:

$AXTI ($2.1B) -> $IQE ($150M) -> $LITE -> Hyperscaler ASICs…

You might discover something early that markets haven’t priced in.

This is by far the best cleaner for Tesla white and black seats. It leaves a non-greasy matte finish and keeps them feeling new.

Highly recommend. If you use it religiously, your interior will stay looking new.

No, the latest paper with the GKP state has all components 30 dB away from achieving break-even, which is the milestone all other companies have achieved in the past two years.

30 dB is a factor 1000x in noise reduction. They can't even show coherence between two of those states, which is one of the most elementary requirement for actual qubits.

Their competitors need a factor 5x improvement not to achieve break-even (since they already did), but to start building CRQCs. Xanadu is several steps behind.

They pivoted to FTQC in 2022 only when it was obvious to everyone else that NISQ was over.

A real FTQC program is tens of billions of $. Private investors have sunk hundreds of millions into this and they need an exit who won't know better.

Xanadu just isn't realistically in the race.

Zero qubit in ten years is a massive red flag. The excuse "it doesn't apply to their tech" is BS, they just don't ship qubits and they never will.

Also Aurora was a gaussian boson sampler, strictly speaking it was still zero qubit back then too.

5 plays that can go 500%-1000% in 2026:

1. SOFI

Calls Jan 2027 $40 for $5 can go to $50+

2. QS

Calls Jan 2027 $25 for $5 can go to $50+

3. EOSE

Calls Jan 2027 $25 for $6 can go to $60+

4. CIFR

Calls Jan 2027 $35 for $7 can go to $70+

5. LAES

Calls Jan 2027 $5 for $2 can go to $20+

Here's 5 more plays I like here 🧵

$BE has gone from $18 -> $129 essentially on the realization that fuel cells can use nat gas to powers data centers. It’s now at $30B market cap.

$BW even after this move is at $450m ish. But it’s clear that nat gas can be used to power boilers and steam turbines to power data centers. They just signed a deal with $APLD that:

1) Probably is the first of more

2) Alone represents a truly transformative revenue opportunity

I am shocked it is not up more. I think people are price anchoring since $BW has run so hard already + shaky small caps lately. But the thing is, it might be a better r/r here than it was emerging shakily from bankruptcy at lows.

I am really excited by this name here, clearly there’s something to their tech. I don’t think $BE at 30B and $BW sub 1B makes any sense, personally.

Bitcoin miner turned AI bubble stock $IREN is up 22% pre-market on announcing a $9.7 billion GPU contract with $MSFT.

As always, the devil is in the details.

Before it can provide any service, IREN first needs to spend $5.8 billion buying the GPUs and ancillaries.

MSFT will provide $1.94 billion upfront, but IREN needs to come up with a further $3.86 billion to fund this capex.

Assuming this is debt financed at 10%, the 5-year contract achieves breakeven in year 4.

Here's the math:

Annual revenue: $1.94 billion

Initial capex: $5.8 billion

Total interest on loan: $0.77 billion

Gross profit: $3.13 billion

Annualized gross profit: $626 million

IREN currently spends $136 mn on SG&A to capture $500 mn in revenue. That amounts to 27 cents out of every dollar in revenue, down from 38 cents the previous year.

Assuming the same run rate and zero depreciation on the new data center facility, the company will spend $528 mn on SG&A to capture the incremental $1.94 bn in annual MSFT revenue.

Annualized operating profit = $98 million

Let's be charitable and assume the company manages to cut down SG&A to 20% of revenue.

Optimistic annualized operating profit = $238 million

While "$9.7 billion contract" makes for a great headline, the numbers throw cold water on this fairy tale.

Making $238 million on a $5.8 billion investment amounts to a mere 4.1% pre-tax return.

The hard truth is data centers are a low-margin business. Microsoft is smart, which is why they have signed this deal rather than build this capability in-house.

IREN investors have nothing to cheer for. This deal is inferior to simply buying 10-year US treasuries and calling it a day.

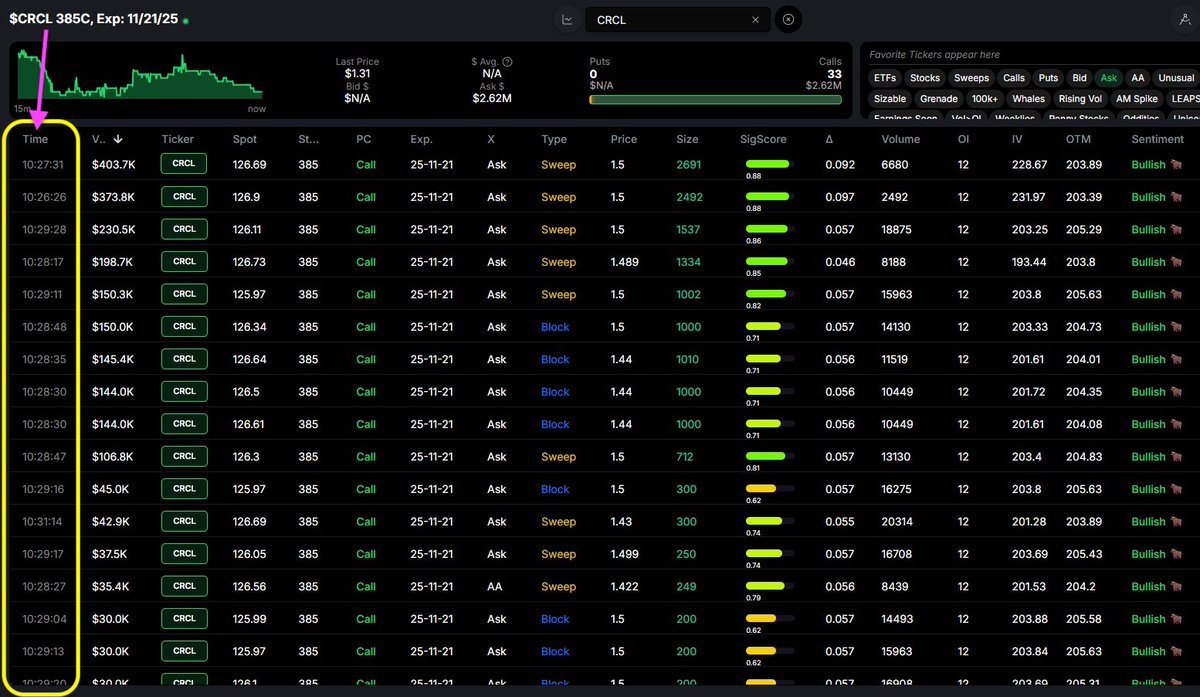

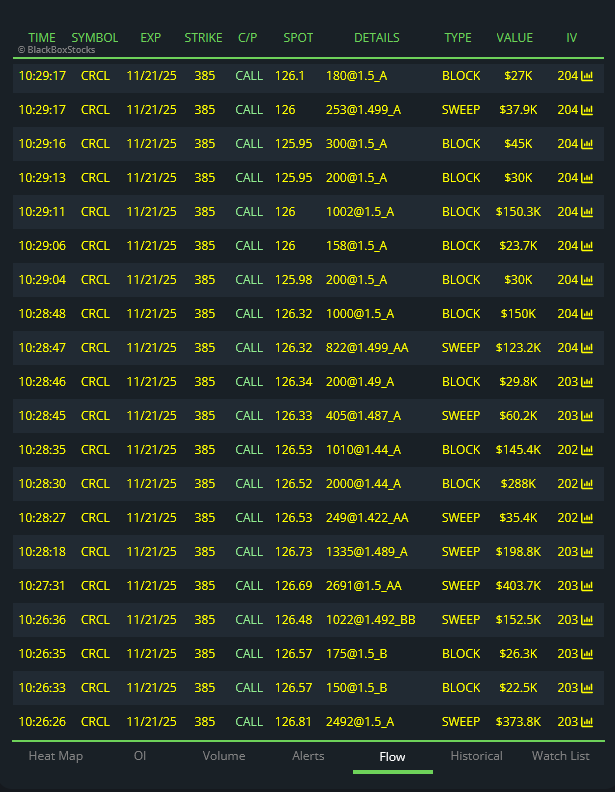

Underline this in your notes...actually, just $CRCL it.

I just found something *very* interesting about $CRCL.

There's $7.5M+ of premium on the 11/21 $385 calls...

With only 22 trading days until November 21st.

These are $385 calls...meaning to go "in the money", the stock has to increase 200%.

200% in 22 trading days.

Possible? Maybe.

Here's what is odd.

The "Payments Innovation Conference" was held on October 21st (two days ago)...

One of the speakers was our buddy, $CRCL president Heath Tarbert.

Heath was slated to speak at 10:50am-11:50am.

...and 20 minutes before Tarbert goes on stage, a $3.7M call buyer steps in at 10:30am.

Confirmed across multiple options data platforms.

Good timing? Inside scoop? Friendly banter?

It's important to note that Heath Tarbert is former Chairman of the CFTC and Asst. Secretary of U.S Treasury.

...from a top-tier federal financial regulator to a leading a crypto firm?

Very notable.

Any catalysts, Luc?

Earnings...November 12th.

That's not all. LOOK AT THIS.

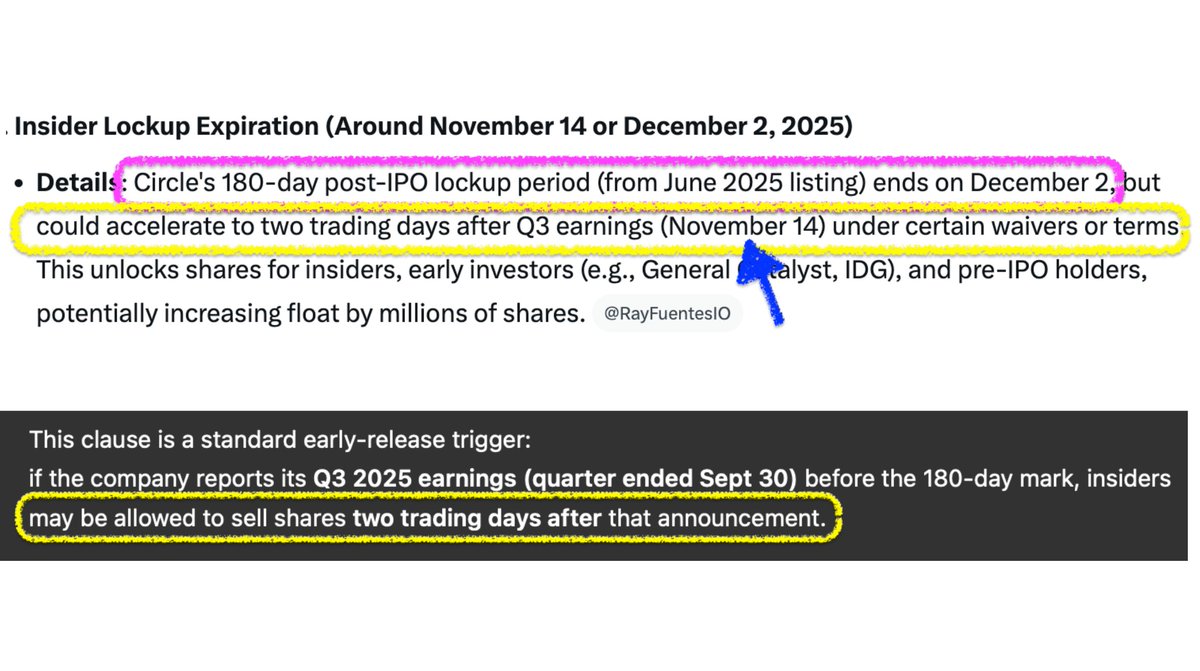

Circle's 180-day post-IPO lockup period (from June 2025 listing) ends on December 2...

...BUT could accelerate to two trading days after Q3 earnings (November 14)!

Something is going on with $CRCL.

The bizarre options activity, the "Payments Innovation Conference", earnings, lock up period ending?

I want in, $CRCL now $129.

guys if i knew why some mentally ill individual was throwing at this money on 385c i would have my entire net worth in this trade

if they were really committed they would buy the furthest strike there is at 390c

but really, the delta is .05 - there is a 5% chance this ends in the money (this seems high tbh)

earnings are November 12th, if a rapid move doesn't happen prior these are cooked even if it gaps 50pts on earnings from this level - with one week left, these are cooked

if you think they are from the future and know these work, buy shares or a closer to the money option so you have a slightly better chance of not losing your shirt

this is multiple days now of outlandish shit for $CRCL

BYND just ran 1000% so maybe a 30B market cap like CRCL can go 200% on the conservative side

$ABAT

Form: 8-K > American Battery Technology Company filed an 8-K on October 15, 2025, reporting the termination of a DOE grant, amendments to bylaws, and amendments to the board of directors code of conduct.

https://t.co/PVU0SfwxrZ