A Uranium & Nuclear Energy stock squeeze like the 1970s is coming, $200+ uranium why? history rhymes.

-Record oil gold prices but Uranium outperformed 600%

-Big oil started mining uranium in the 70s & they profited from it long term

-Dogecoin market cap is larger than the U.S. uranium producers combined

-Nvidia is getting into Nuclear power because of their bottleneck $5 T MC

-AI data centers driving massive power demand 50 GW or 50 new Houston cities

-Datac enters 50% of planned capacity are likely delayed because of energy

-Uranium designated a U.S. critical mineral

-85 million lb deficit from AI reactor demand for the future

-U.S. Defense Production Act being used for nuclear fuel supply chain

-China currently building 50 nuclear reactors, 7 coming online this year U.S. built 55 in the 1970s in < 10 years

-Global nuclear build out accelerating 70+ reactors under construction 400 operational 300+ permitting

-U.S. Nuclear / Uranium Renaissance

-Stagflation-type environment risk

-S&P crashed -48% over 2 years Uranium ran up 500% from 1973 lows.

-AI race becoming a national security priority

-Global energy insecurity & Energy crisis

-Russia Uranium ban effect 2027- supply risk via conversion, enrichment

-SMRs + HALEU demand & technology surge dozens of SMRS pending permits

-$4.3B U.S. push for domestic enrichment

-AI arms & Space race = national security priority

-Years of underinvestment in uranium mining long mine lead times 5 -10+ years

-Long mine lead times, supply can’t respond quickly

-Utilities re-entering long-term contracting cycle

- Largest producers cutting output/Supply Constraints

-U.S. pushing to fast-track nuclear & uranium permitting

-U.S. Government working directly with industry to secure domestic uranium, conversion, enrichment

-Push for streamlined NRC licensing for reactors & fuel facilities

-Existing permitted projects being pressured to move into production faster

-Recognition that permitting alone isn’t enough, pricing must rise to incentivize supply

- Largest Uranium producer Kazatomprom reducing or constraining output

-Limited conversion & enrichment capacity globally

-U.S. starting from a very low domestic production base

-Bottlenecks across the entire fuel cycle

-Forward curve pricing higher uranium prices

-Fuel cycle prices rising conversion, enrichment, SWU

-Physical uranium market remains illiquid & opaque

-No fast supply response to demand spikes

-Energy security are becoming a global priority from Geopolitical risk & supply fragmentation

I will be making some more deep dive videos as I have in the past, you can still watch the hundreds I made on the thesis since 2020 on Uranium & Nuclear.

Kevin Warsh, the new Fed Chair, just made it clear why rates are going lower:

“AI is going to make almost everything cost less.

We’re at the front end of a productivity boom.

Economic growth won’t be inflationary—we’re in the early innings of a structural decline in prices.”

Elon Musk, Sam Altman, even Stanley Druckenmiller all expect AI to be strongly deflationary.

The next few years are going to be insane.

Breaking: The U.S. government just raised how much it pays UnitedHealth per senior on Medicare. More than Wall Street expected

Who bought before the announcement:

• Feb 25: Sen. Markwayne Mullin (R): Bought up to $100,000

• Mar 13: Rep. Gilbert Cisneros (D): Bought up to $15,000

• Mar 19: Rep. Richard McCormick (R): Bought up to $15,000

$UNH is up +30% since February

What people need to understand

And this is important

$UNH pulled back in a standard ABC pull back from $600 to $250, to its 0.618 Fib support

Exactly what to expect

CEO bought on this level too

It then started its reversal

Bounced in Wave 1 and then pulled back for Wave 2 over the last few months

Nothing was abnormal, non standard or a concern

This was a generational buying opportunity that behaved exactly as it should in Wave 2 and we built it up to one of our largest positions

It could not have been easier

🏥 Another Public REIT Gets Taken Private

Healthcare REIT Sila Realty Trust, Inc. $SILA surged nearly 20% on Monday after announcing that it has agreed to be acquired by Blue Owl Capital in an all-cash $2.4B deal at $30.38 per share - a 19% premium to its last closing price.

SILA owns 137 healthcare properties across 65 U.S. markets, along with three undeveloped land parcels, and has primarily focused on outpatient medical and healthcare services facilities.

Sila was among the newest public REITs, having completed a June 2024 direct listing on the NYSE after operating for years as a non-traded REIT.

Since going public, SILA has delivered performance roughly in line with the broader REIT sector index, while modestly outperforming its Medical Office Building REIT peer average.

The deal adds to a growing wave of M&A activity across the REIT sector, reflecting both renewed investor confidence in real estate fundamentals and the persistence of valuation gaps in public markets.

SILA becomes the sixth public REIT to agree to an acquisition in just the past quarter, joining deals involving Whitestone REIT, Two Harbors, National Storage, Veris Residential, Peakstone, and Apollo Commercial.

Notably, five of these six transactions involve private equity buyers, underscoring the continued appetite from institutional investors for stabilized real estate platforms trading below private-market values.

Private buyers have increasingly stepped in to acquire publicly traded REITs trading at discounts to private-market values, offering shareholders immediate premiums while capitalizing on what many view as attractive long-term pricing for institutional-quality real estate.

Since mid-2025, 15 public REITs have agreed to be acquired, including 12 by private investment firms and three by larger public REITs pursuing scale or portfolio repositioning.

In addition, over a half-dozen REITs have launched formal strategic reviews, signaling that boards remain open to potential transactions amid ongoing interest from private capital.

While these deals shrink the number of publicly traded REITs, they also serve as an important validation of underlying real estate values. In many cases, public REITs have continued to trade at meaningful discounts to net asset value, even as operating fundamentals across several property sectors—including healthcare—have remained resilient.

That dynamic has created opportunities for well-capitalized private investors to step in and acquire portfolios at attractive pricing while still offering shareholders a meaningful premium.

Healthcare real estate remains particularly appealing for long-term investors given its demographic tailwinds, essential-use characteristics, and fragmented ownership structure.

The latest transaction highlights a market where private capital continues to see compelling long-term value in real estate—even as public market valuations have yet to fully reflect improving fundamentals.

INSIGHTS:

🇺🇸 Three liquidity injections. Same week.

Fed injected $5,058,000,000 before market open. Treasury released $90,000,000,000 via TGA.

Now the largest Treasury debt buyback in history. $15,000,000,000.

Governments don't inject this much liquidity for no reason.

They inject it when something is breaking.

Or when they're preparing for something big.

The U.S. Digital Asset Reserve announcement is coming within weeks.

Connect the dots.

@RemingtonPeter8@aeberman12 So oil in the real world selling for 120$ to 280$, but 80$ on the paper market. WHEN ARE OIL INVESTORS GOING TO LEARN OIL IS A SHITTY SHITTY MANIPULATED MARKET! stop wining and buy uranium! Its so boring

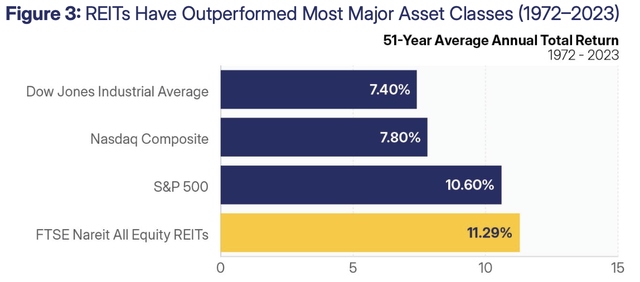

A lot of investors now view REITs as low-return income vehicles for retirees. That is backward. Over the longest time period available, REITs have actually outperformed the S&P 500 and even tech stocks. The last 5 years were rough, but that does not define the asset class.

$SPY $VNQ