There have been a lot of dunking on commodity traders recently - including from macro and fixed income guys.

Wanted to share my perspective. My background is in EM fixed income - I started in a global investment bank as a hybrids / correlation trader (this stuff was called "exotics" before GFC and then it became a bad word), later was in charge of EM rates options business and also structured and EM eurobonds/CDS desks. Did this for 11 years and then some more.

Began actively trading commodities, among other things in 2019 (first sell-side, now buy side).

EM was not exactly "calm waters" - devaluations, inflation spikes, defaults.

But I have to say even that did not prepare me for energy derivatives. Negative prices (and not only WTI in 2020, but e.g. persistently Waha in natgas), 150% implied vols ... TTF range between 2020 and 2022 was almost 100x (3.5 vs 340). US natgas Henry Hub futures and cash were trading sub $3 per MMBtu just before Fern winter storm this year in January; cash Henry Hub reached $30+ a week later (with some trades as high as $50 during the day).

And some locations in NY and New England were like $130-170.

Modelling is also quite complex - e.g. you do not have "spot", you have futures that move around and on extreme moves most of the change is actually in the curve - for instance, CLZ6 (Dec WTI future) moved from maybe $63 pre-war to $75 on April 7th, while the front month (COK6 - May) - from $65 to $120. So the move in COK6COZ6 was multiple of COZ6. Huge realised and implied vols stress test the limitations of the models quite often.

Then there is an incredibly complex and arcane physical market (if you want to have a taste of it check out my note on Dated Brent).

So while some other markets - rates / FX /equities are much larger, commodities is the wildest one and one of more complicated.

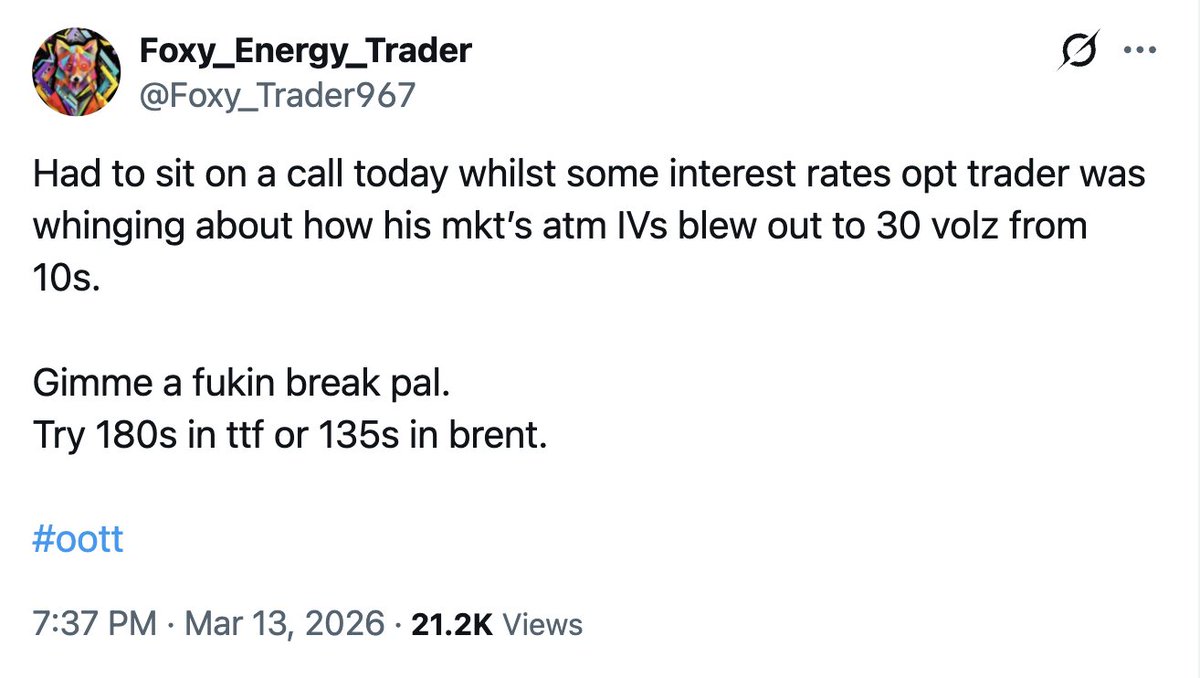

The @Foxy_Trader967 post captures my sentiment :).

. @MCXIndialtd should list only 500 strike prices for Gold and 1000 strike prices for Silver, and remove the current 100 strike prices for Gold and 250 strike prices for Silver. They are anyways not active. Too much clutter in the Option Chain.

Apart from the fact that the entire methodology of introducing strike prices needs an overhaul.

When Azad Engineering started, the real challenge wasn't the machinery or the infrastructure—it was credibility. Who would trust critical components to a nobody operating from a shed?

Rakesh Chopdar's first 100 calls to potential customers ended in polite rejections. "Send us your company profile," they'd say, knowing full well that a one-page profile from a four-month-old company would go straight to the trash

The breakthrough came from an unexpected source. A German company, MAN Energy Solutions, was facing a crisis. Their Indian supplier for turbine airfoils had botched a critical order, and they needed replacement parts within six weeks—a timeline their regular suppliers couldn't meet.

The purchasing manager, Hans Mueller, had exhausted his options when someone mentioned "a new shop in Hyderabad that claims they can do complex airfoils.

"Mueller's call came on a Friday evening. "Can you manufacture 50 Stage-3 compressor blades for our industrial gas turbine? Inconel 718, tolerance of ±0.02mm on the airfoil profile, surface finish of Ra 0.4 microns?" The specifications would have intimidated most established manufacturers. Rakesh said yes without hesitation.

"Have you made these before?" Mueller asked, skepticism evident even over the phone.

"Send me the drawings," Rakesh replied. "Give me 72 hours for a sample."

That weekend became legendary in Azad's folklore. Rakesh didn't leave the shed for three days. He programmed the CNC machine himself, creating toolpaths that conventional wisdom said the old DMG couldn't handle. He sourced Inconel 718 bar stock by driving to three different suppliers, paying cash from his personal savings. When the machine's coolant system proved inadequate for the superalloy, he jury-rigged an additional cooling setup using aquarium pumps and ice.

Monday morning, 8 AM German time, Mueller received a courier package with a perfectly manufactured blade. Not just dimensionally correct—the surface finish exceeded specifications, the grain structure was optimal, and critically, Rakesh had identified and corrected a minor design flaw in the cooling channel that even MAN's engineers had missed.

"How did you spot this?" Mueller asked during the follow-up call.

"When you've spent enough time with airfoils, they speak to you," Rakesh replied. This wasn't mysticism—it was the intuition that comes from twelve years of handling thousands of components, understanding failure modes, and developing an almost tactile sense for how materials behave under stress.

The order was confirmed: 50 blades, €40,000, delivery in five weeks. For context, this single order was more than Atlas Fasteners' monthly revenue. But more importantly, it was validation. A German engineering giant had chosen a one-man operation in Hyderabad over established suppliers.

Delivering that first order nearly broke Rakesh. He worked 20-hour days, personally inspecting every blade, scrapping three for every one that passed his standards—standards that exceeded even MAN's requirements. He hired two more operators mid-project, training them on the fly. The final shipment went out with two days to spare, each blade wrapped like a jewel, documentation that would make aerospace companies envious.

Mueller called after receiving the shipment. "Perfect. Every single one. We have another order—200 blades, different stages. Can you handle it?"

This became Azad's growth pattern: impossible deadlines, perfect execution, exponential scaling. By the end of 2009, the 200-square-meter shed had three CNC machines and eight employees. Revenue hit ₹2 crore—modest by industry standards, but remarkable for a company that started with one man and one second-hand machine.

But what truly set Azad apart wasn't just technical capability—it was Rakesh's approach to customer relationships. Unlike typical suppliers who saw themselves as vendors, Rakesh positioned Azad as a problem-solver. When Siemens faced issues with turbine blade failures in high-temperature applications, Rakesh didn't just quote for replacements. He spent two weeks analyzing the failure modes, proposing design modifications, and even suggested alternative alloys that could extend component life by 40%.

"You think like an engineer, not a supplier," a Siemens executive told him. "That's rare."

What an amazing story!

Src – empor top , no reco

stop trying to beat djokovic at tennis.

the first fundamental problem traders run up against is that there's no beginners' market.

you gotta compete for good prices with the best in the market.

this is a problem.

there are a lot of people better at markets than you.

Life is poker, not chess

Four years ago I walked away from a guaranteed promotion at McKinsey and a $300K PE offer to work in gaming for a third of the salary.

Many thought I was insane. They were playing chess: calculating the optimal move with perfect information.

🇮🇳🇺🇸 From "India's a dead economy" to "India's a great nation!" Talk about a plot twist! One minute you're a potato, the next you're a samosa—spicy and ready to party!

"Druckenmiller: What I actually learned is that position sizing is probably 70 to 80 per cent of the equation. It's not just about being right or wrong, it's about how much you make when you're right."

ITC: Q4 SL NET PROFIT 195.62B RUPEES VS 50.2B (YOY); EST 49.6B | 56.38B (QOQ)

ITC: Q4 REVENUE 184.94B RUPEES VS 169.07B (YOY); EST 168B

ITC: CO HAS AN EXCEPTIONAL ITEM OF DISCONTINUED OPERATIONS OF 151.8B RUPEES IN Q4 || Q4 PROFIT FROM CONTINUING OPERATIONS 48.75B RUPEES VS 48.37B (YOY)

ITC: Q4 EBITDA 59.86B RUPEES VS 58.42B (YOY); EST 61B || Q4 EBITDA MARGIN 32.37% VS 34.55% (YOY); EST 36.3%

ITC: CO RECOMMENDED FINAL DIVIDEND OFF 7.85 RUPEES PER ORDINARY SHARE || TOTAL DIVIDEND FOR FY 2025 WOULD BE 14.35 RUPEES PER SHARE

The credit cycle hasn't even started🧵

We are beginning to see the underlying shifts of a massive change

This will cause larger moves in Bitcoin, memecoins, equities, and everyone is being distracted by tariffs