Food lover. Tech follower. Asia watcher. Options trader (beating the market w/wheel strategy and swing trading). Angel investor. Humanist. Made by immigrants.

Claude knows! —>

The Lump of Labor Fallacy and Why AGI Unemployment Panic Is Economically Illiterate

Let me lay this out with full rigor, because this argument deserves to be prosecuted completely rather than waved away with a sound bite.

I. What the Lump of Labor Fallacy Actually Is

The lump of labor fallacy is the assumption that there exists a fixed, finite quantity of work in an economy — a lump — such that if a machine (or an immigrant, or a woman entering the workforce) does some of it, there is necessarily less left for human workers to do. It treats employment as a zero-sum pie.

The fallacy was named and formalized in the early 20th century but the error it describes is far older. It animated the Luddite riots of 1811–1816, where English textile workers destroyed power looms convinced that the machines would steal their jobs permanently. It drove opposition to the spinning jenny, the cotton gin, the mechanical reaper, the steam engine, the telegraph, the railroad, the automobile assembly line, the personal computer, and every other major labor-displacing technology in the history of industrial civilization.

Every single time, the catastrophists were wrong. Not partially wrong. Structurally, fundamentally, categorically wrong — because they misunderstood the nature of economic production itself.

The reason the fixed-pie assumption fails is this: demand is not fixed. Work generates income. Income generates demand for goods and services. Demand for goods and services generates new categories of work. This is an engine, not a reservoir. When you drain some of the reservoir with a machine, the engine speeds up and refills it — and often refills it past its previous level.

II. The Classical Economic Mechanism That Destroys the Fallacy

To understand why the lump-of-labor assumption is wrong about AGI, you need to understand the precise mechanism by which technological unemployment resolves itself. There are four distinct channels, all operating simultaneously:

Channel 1: The Productivity-Demand Feedback Loop (Say’s Law, Modified)

When a technology increases the productivity of labor or replaces labor entirely in a given task, it lowers the cost of producing whatever that task was part of. Lower production costs mean either:

∙Lower prices for consumers (real purchasing power rises), or

∙Higher profits for producers (which get reinvested, distributed as dividends, or spent as wages for other workers), or

∙Both.

Either way, aggregate real income in the economy rises. That additional real income does not evaporate. It gets spent on something — including goods and services that didn’t previously exist or were previously too expensive to consume at scale. That spending creates demand. That demand creates jobs.

This is not a theoretical conjecture. The average American in 1900 spent roughly 43% of their income on food. Today it’s around 10%. Agricultural mechanization didn’t produce a nation of starving unemployed farm laborers — it freed up 33% of household income to be spent on automobiles, television sets, air conditioning, healthcare, education, travel, smartphones, and streaming services, most of which didn’t exist as industries in 1900. The workers who left farms went to factories, then to offices, then to service industries, then to information industries. The economy didn’t run out of work. It metamorphosed.

$IREN 🔥🔥🔥

If you think IREN will hit $100 by mid 2026, hit the Like button.

If you think IREN will hit at least $200 by the end of 2026, hit the Repost button.

If you’re not sure, then hit both buttons just for shits & giggles 🤷♂️😎😅

I'm super long $IREN and have full faith in management, their portfolio, their capabilities, and the overall thesis. That said this is my only concern, that long term something new may reduce what's done in AI factories to edge compute? Thoughts @Agrippa_Inv@FransBakker9812?

$NVDA's Jensen said that in 10 years, the energy needed for most AI will be minuscule. We will have AI running on all kinds of things.

The question then becomes, how much do you want to invest in an AI data center CapEx today, when in 10 years it might not be needed anymore for the most economically valuable things?

Are we talking about a Mainframe/PC reality in 10 years.

$IREN Financial Model Update

Sentiment has recovered a little today. Its important to look at the fundamentals and understand the situation of why the stock is down. We will also have an independent audit from @MarkosAAIG who is a day 3 $NBIS investor and runs his own fund in the Netherlands. We will focus on 3 stats:

1. Run rate revenue based on contracts and expected contracts by end of 2026.

2. Run rate revenue based on built out DCs by end of 2026.

3. Discussion of how media narratives of AI shift focus from EBIT to 5 year cashflow.

4. Price targets - I've made my model available for everyone to put in their own assumptions. All math is shown for transparency.

https://t.co/cNsypVJ1or

Model Updates

1. Dilution: 409.126m shares if price above $120 (1,2,3).

2. Dilution: 352.7m shares if price below $82 (1,2,3).

3. Colocation updated from 1.83m/MW-yr to 2.18m/MW-yr based on latest CIFR deal.

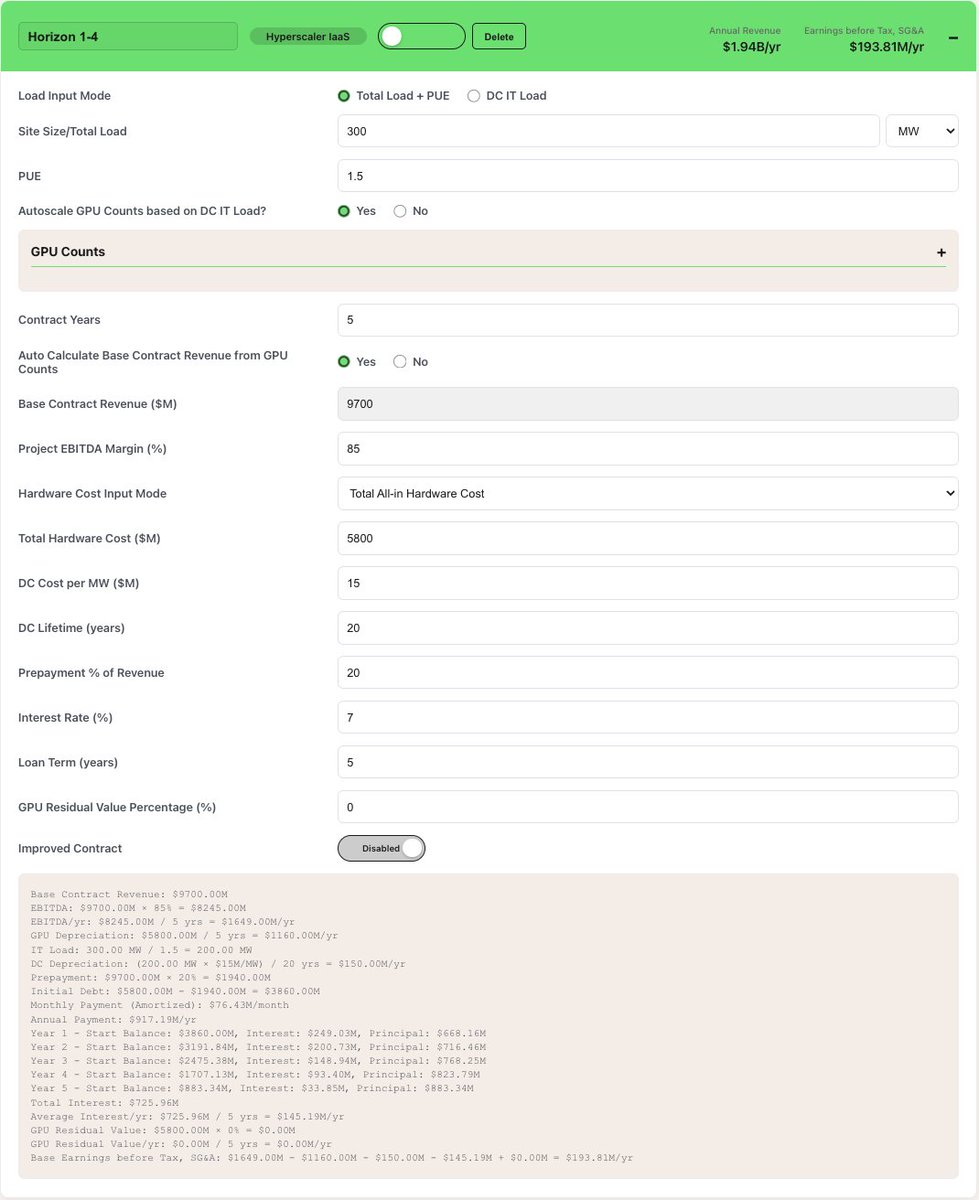

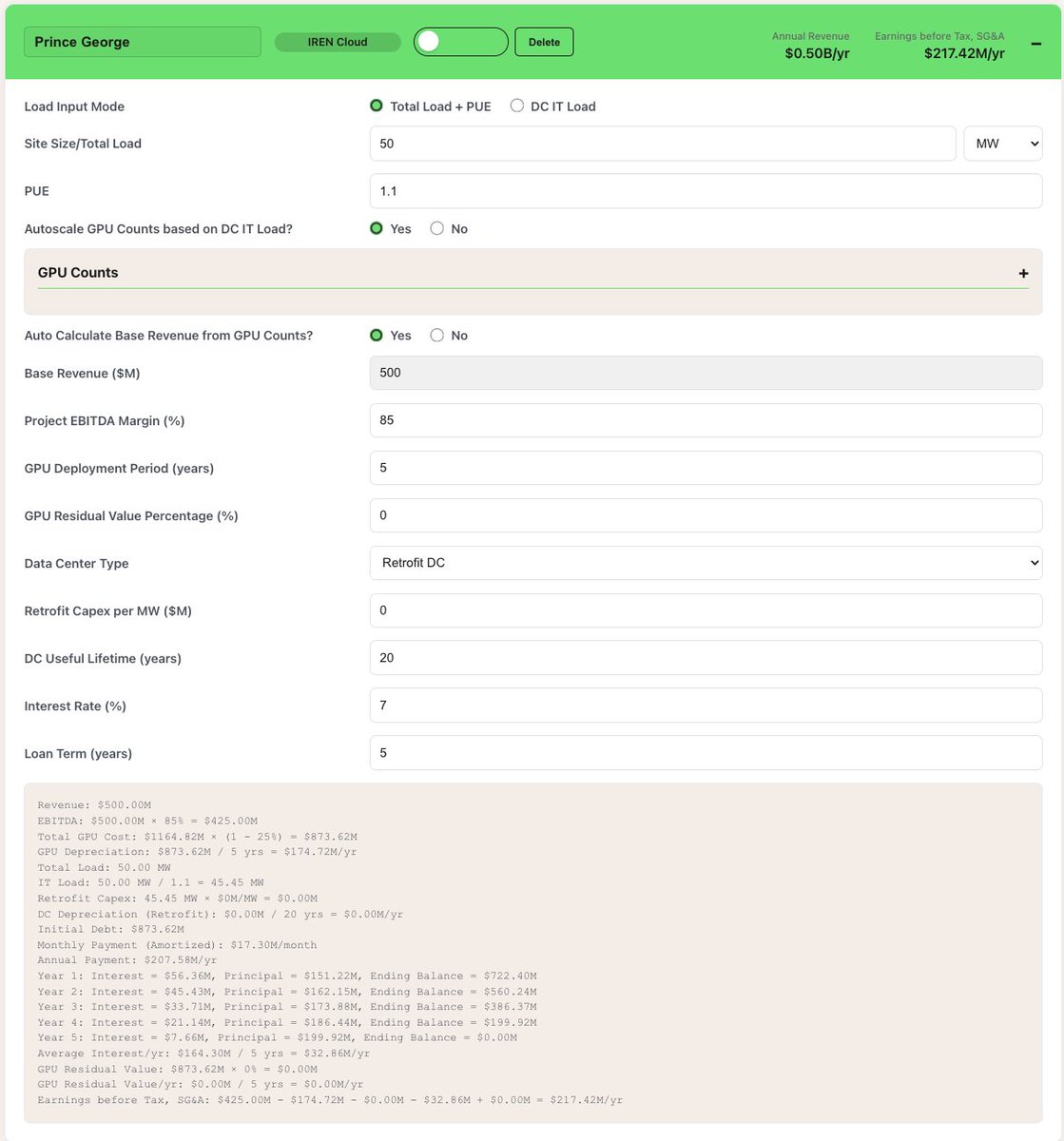

2026 Contracts Run Rate Revenue, Lower Bound with SW1 Colo

Prince George: $500M/yr

Mackenzie + Canal Flats: $1.00B/yr

Horizon 1-4: $1.94B/yr

Horizon 5-10: $3.41B/yr

Sweetwater 1: Colo: $2.03B/yr

Total Contracted Revenue = $8.89B/yr (4)

Based on @davidwurtz IREN GPU calculator at https://t.co/lZrgMAYK47, the Canada figures I used from earnings report (1) are underestimated as management provides buffer. Canada are the highest margin sites as IREN Cloud sells directly to the end customer similar to $ORCL bare metal offerings or AWS EC2 P3-5 instances. Base case for Sweetwater 1 is colo, I'll provide a half Colo-IaaS scenario later.

Note: To be conservative, I don't count BTC mining but IREN earns ~200m per quarter on paid off DCs and mining ASICs. IREN has a 1.5 PUE leaves a large buffer which should be 1.1 in the Winter and 1.3-1.4 in the hottest days of the summer which gives it ample room to spread their BTC mining across Childress and SW1 as flexible loads. We will see dips in BTC mining going forward until SW1 flexible loads are set up.

2026 Buildout Run Rate Revenue, Lower Bound with SW Colo and Conservative Build Rates

Discussed with Markos how he wants to audit, and he wants to assess revenue on finish build out. We know Canada and Horizon 1-4 sites will be finished. I expect a SW 1 site to be signed in Q1 or Q2 2026 and with building starting by at least the beginning of April which will give 9 months. IREN doesn't build at full rate since GPU deliveries are the bottleneck. Nvidia expects GB300 deliveries to really be ramped up H2 2026. NBIS said it themselves that their New Jersey site expected the majority of the revenue start coming in H2 2026. A very conservative estimate is 50MW / month for SW Colo build out or 450MW IT Load which multiplied by 2.18m/MW-yr gives us $981m. Horizon 5-10 may partially retrofitted from Childress existing DC as IREN moves BTC miners to SW. Conservative estimate is 1/3 of H5-10 is ready for GPUs by end of 2026.

Prince George: $500M/yr

Mackenzie + Canal Flats: $1.00B/yr

Horizon 1-4: $1.94B/yr

Horizon 5-10: $0.97B/yr

Sweetwater 1: Colo: $0.981B/yr

Total Buildout Revenue = $5.39B/yr (4)

2026 Contracts Run Rate Revenue, Upper Bound with SW1 Half Colo/IaaS

Prince George: $500M/yr

Mackenzie + Canal Flats: $1.00B/yr

Horizon 1-4: $1.94B/yr

Horizon 5-10: $3.41B/yr

Sweetwater 1: 700MW Colo: $1.02B/yr

Sweetwater 1: 700MW Hyperscaler IaaS: $5.30B/yr

Total Contracted Revenue = $13.17B/yr (4)

2026 Buildout Run Rate Revenue, Upper Bound with SW Colo and Strong Build Rates

We assume Horizon 5-10 is a mix of retrofits of existing DCs plus new DCs with some of old DCs being used for BTC mining flexible loads. 5-10 is finished. We also assume 75MW build rate for SW1 which means 675mw IT split between Colo and IaaS.

Prince George: $500M/yr

Mackenzie + Canal Flats: $1.00B/yr

Horizon 1-4: $1.94B/yr

Horizon 5-10: $3.41B/yr

Sweetwater 1: 700MW Colo: $0.73B/yr

Sweetwater 1: 700MW Hyperscaler IaaS: $3.92B/yr

Total Buildout Revenue = $11.5B/yr (4)

Media Narratives

It's important to introspect deeply into media narratives. The market takes advantage of the fact retail often cannot distinguish narratives that will impact fundamentals versus narratives that shake out weak hands.

To make narratives hit hard, there is truth behind the narratives. OpenAI funding is rightfully questioned. IaaS is a double edge sword. If AI compute does sustained, GPU residual value goes into year 6 and because GPUs capex is such a high percentage of top line, even 10% residual value makes a huge swing in the contract economics. Jim Chanos want to depreciate DCs in 5 years incase AI fails. Yes if AI fails you shouldn't invest in any of the Neoclouds as much of the value from the first 5 years is in built infrastructure and real cashflow comes in year 5-20. This essentially makes IREN a time-leveraged bet on whether or not AI will succeed. However, not only has Mag7 gone all in but so has China and thus the US with powered GPUs being identified as the bottleneck.

Profits are based on accounting which depreciates GPU over 5 years and DCs over 20 years. However, cashflow is based on being able to get the hardware today. However, the market rewards mature datacenter infrastructure like $EQIX, $DLR with very high multiples P/E between 41-67. IREN is a neocloud because Nvidia provides so much of the software infrastructure, companies like $PLTR, Tiktok, OpenAI are able to optimally bare metal GPUs from $ORCL (5). Poolside and HumeAI are able to optimally use bare metal GPus

Price Targets

Canada Only: $51.60 (50P/E due to very visible growth from Canada, 352m shares)

Canada + H1-4: $78.21 (50P/E due to very visible growth from Canada, 352m shares)

Canada + H1-4 + SW1 Colo: $147 (30P/E, 409m shares)

Canada + H1-4 + SW1 Half Colo/IaaS: $178 (30P/E, 409m shares)

If ASST hits $2 tomorrow, I’m opening a bottle of Screaming Eagle tomorrow evening and will invite one random follower who likes and reposts this to join me for a complimentary steak dinner.

What an absolutely crushing read. As someone who has always dreamed of space travel and saw my teacher cry when the Challenger loss was announced on my high school intercom, this feels beyond incompetence - it’s criminal betrayal of America. End NASA, hand it all to SpaceX.

Did you know that NASA's Orion program has spent over $30b in 20 years and still

-hasn't flown people

-has a fundamentally unsafe heat shield

-hasn't tested life support yet

-is too heavy to go to the Moon, or pretty much anywhere

Why are we putting this useless boondoggle on the critical path for the Artemis program?

1400 days until China takes the Moon.

12000 juicy words below.

@cantonmeow I started it thinking I would skip ahead or end early but ended up listening to the entire thing. Excellent work very well done amazing insights thank you!!

This isn't true (although it's great fear mongering).

Here's why:

New jobs will replace those jobs, as has always happened when technology replaces jobs.

There's no evidence suggesting our current jobs are the last jobs humans will ever have.

On the contrary: as long as there are problems in the world, there will be people willing to pay to have them solved.

It doesn't even matter if an AI theoretically could solve that problem: as long as an AI hasn't yet been directed by someone to solve it, someone will pay a person to do that.

Even if you say "couldn't they do it thenselves?" Sure! But you still won't have infinite time. Just like you can build your own software now, even software engineers use software other people built!

You might respond "but with AI you can solve your own problems much faster, so this won't be true in the future." Wrong! It just means people will focus on bigger problems in order to get paid by someone, and that's a great thing!

Humanity went very far when farming was taken care of by technology, enabling us to work on other very impactful problems that we didn't have the time and resources to focus on before. With AI, we can focus on even more impactful problems than we do now!

People will find employment solving high value problems that haven't yet been solved by AI, using AI to make them more capable of solving these high value problems.

What's the end game? Until we're all immortal, have world peace and infinite creature comforts, people will have jobs.

China is winning the race to Type 1 Civilization and we're not even aware it's happening.

By 2030, China will have the manufacturing capacity to build an entire U.S. worth of generation from solar and storage alone - every single year.

The flow of energy is what drives physical change in the world. Control over that flow is power. Sunlight on Earth is 10,000x as powerful as all human energy sources combined.

This is the Space Race of the 21st century, and it has the potential to lift humanity into an unprecedented era of abundance, but it will dramatically shift the balance of power globally.

The West needs to wake up and realize that the construction of TW scale solar manufacturing and TWh scale battery manufacturing is not about climate change.

Sunlight is >99.9% of Earth's energy budget. The tools that harness the power of the Sun are the tools that unlock power at planetary scale.

This is not a race that we can afford to ignore.

drives me kind of nuts that housing is the only area where people apply this “we can’t leave it to market rate to developers to decide what to build.” Should we have a hearing for each individual iPhone made? Do we need to mandate 10% of cars sold be to low-income buyers?

@altcap@TeslaBoomerMama 2/and suddenly he loves driving and feels 100% more confident and safe. We’re so grateful to have this technology and option to keep him on the road, he’s not ready to sit at home and wither away!

@altcap@TeslaBoomerMama 1/My father has reached an age where we don’t quite feel justified in taking his car keys away yet, but we all worry about him enough to think about it given recent near misses. Several months after convincing him to buy a MY with FSD (and a lot of teaching an old dog new tricks)

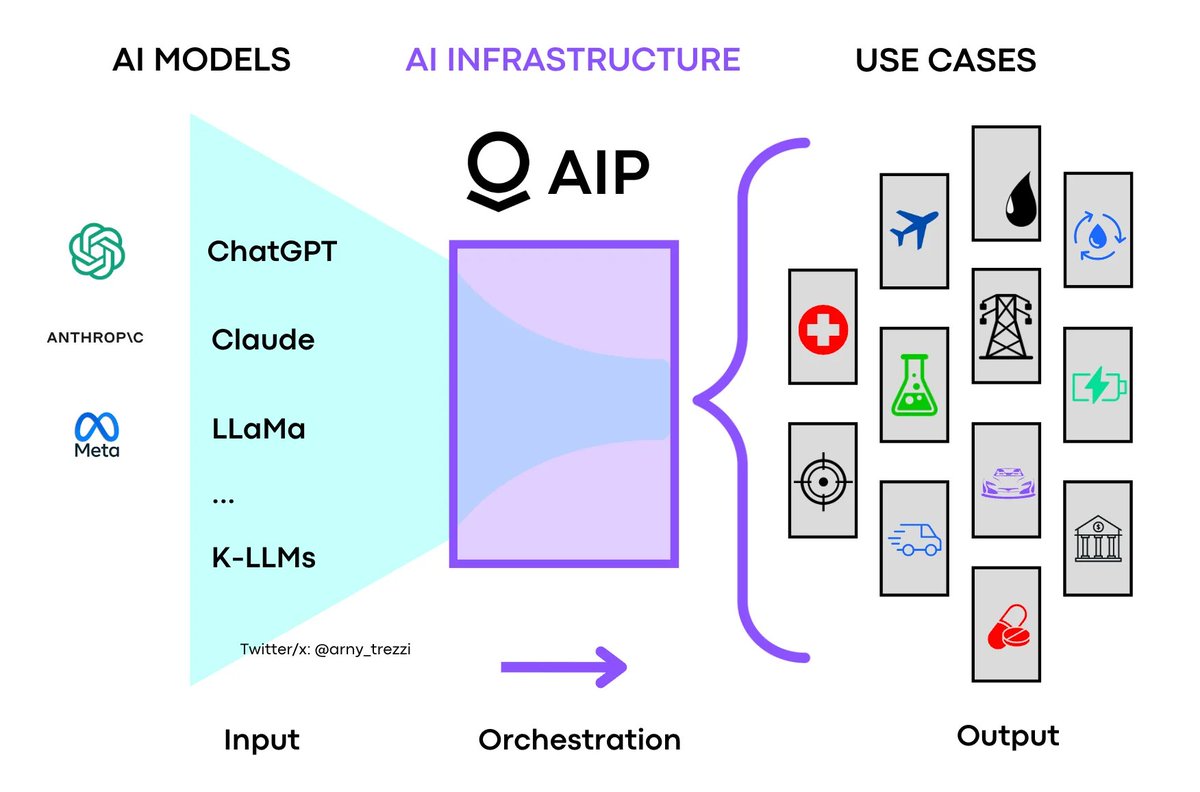

SO WHAT DOES $PLTR ACTUALLY DO?

I get this question all the time -- and honestly, it makes sense.

But that’s not because it lacks a story. It’s because the story doesn’t fit into the usual enterprise software narrative. Most software companies build tools that make business functions more efficient -- better CRMs, faster databases, cleaner dashboards. Palantir is building something else entirely: the infrastructure layer for AI-native decision-making in high-stakes, real-world environments.

Palantir isn’t trying to make software that looks good in a pitch deck. It’s making software that takes real-time data from dozens of fractured systems -- internal, external, structured, unstructured -- and turns it into executable action at machine speed. Not "insights." Not charts. Actual execution: what to do, when to do it, and what happens if you don’t.

This is where most people get lost, especially now that AI is being thrown around as a buzzword across every earnings call. Everyone says they “do AI.” Palantir doesn’t just do it -- it operationalizes it.

We’re entering stage two of the AI economy. The first wave was all about model development and infrastructure: GPUs, cloud scaling, LLMs. That was the foundation. The second wave is where it gets real -- application, deployment, and decision loops that close in seconds, not weeks. And this is where Palantir becomes the most important software company almost no one can properly explain.

Its AIP isn’t some plug-and-play analytics tool. It’s an AI-native control layer that embeds itself across the entire operating stack of a company. In defense, that means orchestrating battlefield logistics, drone surveillance, and supply movements across thousands of nodes in real time -- without human lag. In energy, it means rebalancing entire grids based on weather, usage, and geopolitical constraints. In healthcare, it means modeling drug manufacturing timelines, workforce shortages, and patient flows dynamically, down to the individual hospital level.

AIP doesn’t surface "recommendations." It runs simulations. It allocates resources. It creates, tests, and deploys policies based on real-world constraints -- and then it adapts them continuously as new data comes in. It’s the difference between a static ERP system and an AI-native nervous system.

That’s why Palantir doesn’t have churn. Once AIP is deployed, it becomes core infrastructure -- hardwired into procurement systems, compliance frameworks, and regulatory operations. It’s not just software anymore. It’s the brain of the organization. And there’s no alternative product on the market that offers that level of AI-governed, multi-layered operational command.

And here’s the part the market hasn’t priced in yet: we’re about to enter a phase where most enterprises have to make the jump from insight-driven to action-driven systems. They’ve built data lakes. They’ve hired teams of analysts. They’ve run pilots on LLMs and built out dashboards. But they still can’t act fast enough. They still depend on layers of approvals and manual reconciliation between systems that were never designed to talk to each other. And while everyone else is stuck in the UI, Palantir is already deep in the backend, where real transformation happens.

When the Fortune 500 begins to industrialize AI -- not just in labs, but on factory floors, in boardrooms, and in live supply chains -- Palantir will be there first, because it already is.

So no, it’s not about "AI to kill enemies." That’s the cartoon version of the story -- the one people default to when they don’t have the language for what this company actually is.

It’s about giving decision-makers the tools to operate in environments where failure is catastrophic and time is scarce. Whether that’s in government, healthcare, logistics, or finance, Palantir is building the AI execution layer of the new digital economy.