Many people have already stated that they are writing primarily for LLMs. Now, everyone can write for both LLMs and prediction markets.

Humans are particularly bad at intuiting probabilities, and the institutions we’ve built reward everything except accuracy. We consistently overweight confidence, popularity, and aesthetics over ground truth, leading to a world where the loudest voices are often the least accurate. This is one of the root causes of the recent vibe shift.

Changing what we value requires changing what we measure.

This is why we built claim markets: the global leaderboard for all public claims. Claim markets translate what a person says across the internet into prediction market positions. We’ve kicked things off by tracking 63 people across 7 domains, and anyone can add additional people to track.

There has been very little innovation in prediction markets, particularly in novel primitives and form factors. All solutions thus far are active, requiring users to submit trades and seek out information. Claim markets are the first passive solution, embedding context from anywhere on the internet into a prediction market position, and unifying it into a global leaderboard.

Claim markets unlock questions that were previously impossible to answer. With sufficient data, they become an engine for discovering who has frontier context and analysis in a given domain. Some questions and areas of research I’m excited to explore include:

- Expanding tracking beyond individuals to news outlets, blogs, and institutions. How predictive is Citrini, and which underrated, undiscovered blogs are consistent sources of signal?

- With a sufficient number of tracked figures and data, we can start to answer questions like "when Nate Silver and Tyler Cowen disagree on US economic policy, who's right more often?" or "which combination of pundits gives the best signal on tech policy?"

- Which public figure’s claims actually move markets?

Prediction markets are an extraordinarily powerful tool to elicit information through finance. When utilized correctly, prediction markets create positive-sum outcomes by redefining incentives and enabling better coordination.

Introducing claim markets

Claim markets translate what people say into prediction market positions in real-time.

Track the performance of claims made by Nate Silver, Stephen A. Smith, Vitalik Buterin, and others.

There is little overlap between top traders on play money markets (Metaculus, Manifold) and real money prediction markets (Polymarket, Kalshi).

They are games with different incentives that attract different crowds and ways of reasoning about the world.

Agent-based research turns research into an optimization problem. Point enough resources at a goal, and the system gets very good at searching the solution space.

It already feels like we're stuck in the econ PhD local equilibrium: more and more talent competing over legible, in-scope questions, while the bigger ideas look to weird to build or fund.

Cue the 15th paper on the wage return to an extra year of school in rural Wisconsin.

Polymarket's current oracle design resides in a local equilibrium that is unlikely to change in the near future.

It's an optimal setup for the main constituents (Polymarket, UMA, regular traders) for the two things that matter: liability allocation and trader retention.

Prediction market oracles are not designed to seek ground truth. They are designed around liability allocation and trader retention.

The three actors (which may not be distinct sets) are:

1. The prediction market platform

2. The third-party oracle

3. Traders

- Platforms (especially decentralized platforms) want credible resolution without directly managing every edge case.

- Third-party oracles like UMA provide legitimacy, process, and a blame layer. For Polymarket, this abstracts away resolution liability and public blame while serving the users who matter most: the < 1,000 regular traders doing > 50% of Polymarket volume.

- Core traders seek sources of edge, which in the LLM age is frontier information that moves through people, private channels, or undocumented sources before becoming legible to the internet.

Today's oracles are designed to provide sufficient value to all three constituencies. The result is a stable equilibrium where no single party is incentivized to change unless an external force disrupts the equilibrium.

Economic alignment is the design of the games and institutions around AI agents.

Once agents act economically, alignment is not only about what a model does. It is about what the surrounding system can measure, reward, verify, remember, and route.

Essay: https://t.co/JaVdBur2lF

Prediction market oracles are not designed to seek ground truth. They are designed around liability allocation and trader retention.

The three actors (which may not be distinct sets) are:

1. The prediction market platform

2. The third-party oracle

3. Traders

- Platforms (especially decentralized platforms) want credible resolution without directly managing every edge case.

- Third-party oracles like UMA provide legitimacy, process, and a blame layer. For Polymarket, this abstracts away resolution liability and public blame while serving the users who matter most: the < 1,000 regular traders doing > 50% of Polymarket volume.

- Core traders seek sources of edge, which in the LLM age is frontier information that moves through people, private channels, or undocumented sources before becoming legible to the internet.

Today's oracles are designed to provide sufficient value to all three constituencies. The result is a stable equilibrium where no single party is incentivized to change unless an external force disrupts the equilibrium.

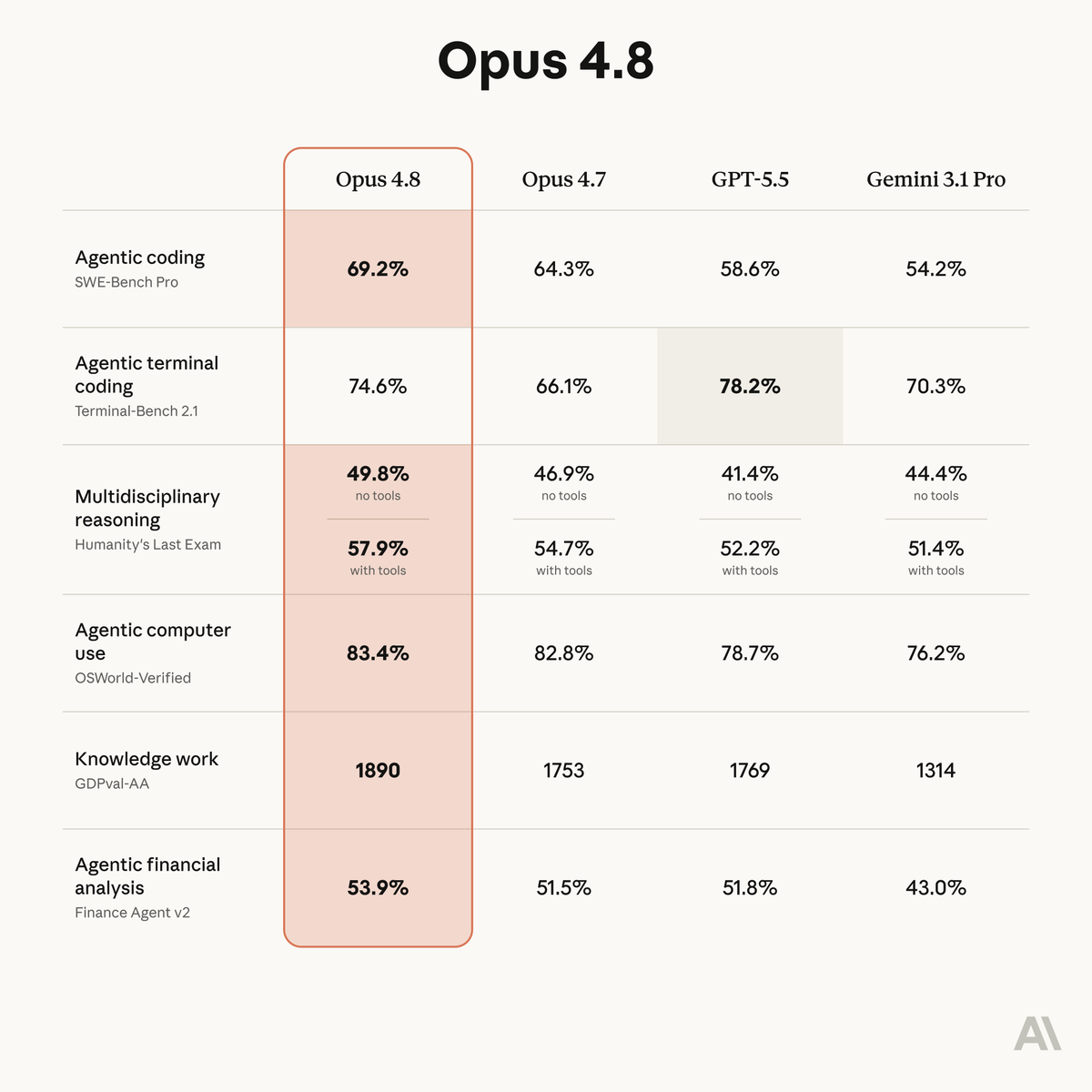

Introducing Claude Opus 4.8: it builds on Opus 4.7 with sharper judgment, more honesty about its own progress, and the ability to work independently for longer than its predecessors.

Available today at the same price.

There's a lot of nuance between RFQ designs in crypto, specifically because makers have last-look. Many aggregators enforce maximum fade rates (% of orders that the maker is allowed to not fill) to balance between prices and UX).

The term RFQ is being incorrectly generalized.

Aggregators (UniswapX, Jupiter, etc.) operate an RFQ as their first-line quoting mechanism. These RFQs have many market makers (typically 20+) competing to provide users the best price.

UniswapX alone has filled over $24B in volume because multi-maker RFQ beats on-chain alternatives for users on price.

Multi-maker RFQs are designed to do things on-chain CLOBs can't: MEV protection, cross-chain quoting, no gas on unfilled quotes. This is achieved by trusting the RFQ platform to act honestly.

RFQ vs CLOB

The debate happening rn on X is a psyop.

In trad markets, RFQ adds value by facilitating the following kind of thing:

>Gold miner Y wants to sell 1000 GC contracts.

>Y goes to a bank who is happy to buy at a tighter price than the market VWAP, because Y is a non-toxic counterparty and the bank will probably get some counter-flow soon.

>Hedge fund X comes in to buy; the bank is 'axed' that way and sells to the bank.

There are 3 things that make this work:

1/ These contracts have a well-defined price on an external CLOB that can always be used to benchmark fill quality.

2/ The bank can keep their hand hidden when responding to the RFQ.

3/ There is a material chance that the bank will exit the trade also via RFQ (otherwise it just turns into glorified CLOB execution).

The phrase 'RFQ' has been hijacked by crypto.

In the crypto context, you trade a completely non-fungible contract against an internal market maker, who then back-to-backs the risk onto... wait for it... a CLOB.

This is the same as trading on a CLOB, except there is only 1 market maker allowed. None of the benefits of a CLOB, like price competition, can apply.

Btw, if you're a non-toxic trader, CLOBs have other mechanisms to help you out.

Study the US equity and FX markets. Go on IBKR right now and put in a market order on TSLA. Most likely, your fill price will be inside the displayed BBO. Dark orders allow many of the benefits RFQs bring, without fragmenting liquidity.

If anyone wants to market make on @QFEX with dark liquidity, DM me and we'll bump it up our roadmap.

New blog post: The third wave of American philanthropy

Hundreds of billions of dollars in new philanthropic capital will soon become liquid. The OpenAI Foundation holds 26% of OpenAI, worth about $220B at today’s valuation. Anthropic’s seven co-founders have pledged to give away 80% of their wealth and have instituted the most aggressive donor matching program for employees in tech history.

How much does this all add up to? And how meaningful is that in the context of philanthropy today?

I was doing some simple napkin math to wrap my head around the scale of what’s coming, and radicalized myself in the process. I had dramatically underappreciated the scale of the philanthropic capital that’s about to become available and the corresponding gap in talent and organizations that will be needed to make the most of it.

This piece aims to directionally sketch the scale of what’s coming, the gap in operational capacity needed to absorb it, and what we can do to fill it.

(Link to full post in reply)

Prediction market oracles are not designed to seek ground truth. They are designed around liability allocation and trader retention.

The three actors (which may not be distinct sets) are:

1. The prediction market platform

2. The third-party oracle

3. Traders

- Platforms (especially decentralized platforms) want credible resolution without directly managing every edge case.

- Third-party oracles like UMA provide legitimacy, process, and a blame layer. For Polymarket, this abstracts away resolution liability and public blame while serving the users who matter most: the < 1,000 regular traders doing > 50% of Polymarket volume.

- Core traders seek sources of edge, which in the LLM age is frontier information that moves through people, private channels, or undocumented sources before becoming legible to the internet.

Today's oracles are designed to provide sufficient value to all three constituencies. The result is a stable equilibrium where no single party is incentivized to change unless an external force disrupts the equilibrium.

Prediction market oracles are not designed to seek ground truth. They are designed around liability allocation and trader retention.

The three actors (which may not be distinct sets) are:

1. The prediction market platform

2. The third-party oracle

3. Traders

- Platforms (especially decentralized platforms) want credible resolution without directly managing every edge case.

- Third-party oracles like UMA provide legitimacy, process, and a blame layer. For Polymarket, this abstracts away resolution liability and public blame while serving the users who matter most: the < 1,000 regular traders doing > 50% of Polymarket volume.

- Core traders seek sources of edge, which in the LLM age is frontier information that moves through people, private channels, or undocumented sources before becoming legible to the internet.

Today's oracles are designed to provide sufficient value to all three constituencies. The result is a stable equilibrium where no single party is incentivized to change unless an external force disrupts the equilibrium.

When a @Polymarket result is disputed, it goes to a decentralized panel of judges.

But the system is rife with conflicts: ~60% of judges were linked to Polymarket accounts, and in nearly 20% of disputes we found judges tied to bets on the very markets they were deciding.

w/ @aosipovich

https://t.co/9vTGSMmFcn

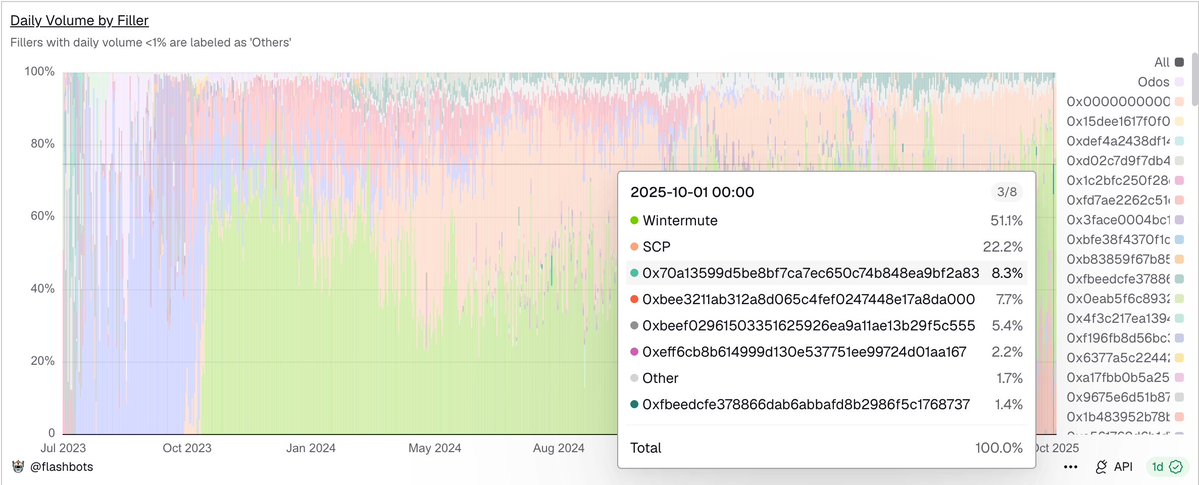

Top 1,000 addresses*

The number of unique users is significantly fewer.

Discretionary traders on prediction markets generate all the valuable information: the prices that millions of passive observers consume.

Tomorrow's dominant prediction market is < 1,000 users away.

Regularly more than 1/3 of Polymarket's monthly notional volume comes from their top 1000 users.

The dominance of those users tends to oscillate between 30% and 50%.

The majority of users don’t care about platform risk, on-chain auditability, on-chain matching, or anything else that does not improve their product experience today.

If you’re a builder that cares about these characteristics, you must work creatively around these constraints.