This is true across the board… CAC does not scale linearly with customer value.

If your best customers are worth 15x more than your worst customers (often times even more) they may be only marginally more expensive to acquire.

"You're not winning a subscription box war with Butcher Box—they do $600M/yr."

So @chrisorzy did the opposite for ranchers:

Whole cow for $7,000.

Cold traffic on Facebook.

FREE freezer included.

"The CAC didn't scale with the cost of the product. I recognized this. No one else did."

@CJSlattery Every company lives/dies by CAC:LTV and then most of them completely ignore the LTV half of the equation. If CAC rises because CPMs rise, focus as much on improving LTV as reducing CAC.

LTV is also about who you acquire. People think about LTV terms of squeezing the most out of each customer (which is good and necessary), but not in terms of acquiring customers that arrive with hire potential retention/LTV.

That is to say, post click/post purchase efforts are critical for maximizing the captured LTV of any given customer. But the maximum capturable LTV of said customer is a byproduct of who they are, not what you do to them. We can't skip the upstream question of whether the customers walking in the door have high retention potential to begin with.

What Cody’s referring to here is an issue we found a few weeks ago:

Meta was no longer driving the type of revenue we wanted it to.

Our travel category growth had slowed, and we used Northbeam’s product analytics to identify that the type of revenue we were generating from our Travel Ads was fundamentally different year-over-year.

In 2025, 6% of Travel Ad-attributable revenue came from non-travel products. But for a short period of time, we were seeing over 40% of Travel Ad-attributable revenue come from non-travel products.

Because of recent changes we had made in creative, pixel, and ad account setup — and the fact that we were in a promo period — Meta’s best way to drive lowest cost conversions was serving to traffic converting on our most popular products.

Meta is extremely good at delivering the result you ask for (purchases, reach, etc), but this was more evidence that there are creative ways to better align a platform’s ad engine with your true business goals.

This goes back to one of my 2026 predictions: Signal engineering, the deliberate design of what signals are sent to an ad platform, will continue to grow in experimentation & importance.

@codyplof Have you experimented at all with https://t.co/dmEAlsshg6? Could be good for what you’re describing, their MCP makes it really easy to connect to Claude. I’ve used it a bit but haven’t had any real need, so it’s been mostly exploratory.

@DTCMidas Most small changes are great for squeezing a few more dollars out of the average customer, but once you start making meaningful jumps in the value of your average session/customer, you're basically just acquiring different customers with higher spend potential.

@PhilKiel if you're selling consumables (which I suppose peptides are not exactly but also are exactly) then I think the brands which optimize for retention will win.

"The obsession with short-term, bottom-funnel demand harvesting is causing us to shrink as ROAS slowly declines. How can this be? We’re spending more, reaching fewer people, hitting the same ones over and over. And ROAS is down?"

ROAS is not a 7 day measurement. Your best customers are worth 16x more over their lifetime than your worst. You can in fact push Meta to target those customers who will spend more and repeat purchase with you over and over.

CEO: Why the f*** aren’t we growing?

CMO: [Slacks screenshot of Meta ads account YOY]

CFO: WTF? That can’t be real.

CMO: I get we want “accountability” and “ROI,” but the obsession with short-term, bottom-funnel demand harvesting is causing us to shrink as ROAS slowly declines.

CEO: We need to increase the number of ads we launch.

CMO: We’ve already 10x’d the volume

CEO: Then we need more creative diversity.

CMO: We have. Our Meta rep says we’re crushing it.

CEO: We need a better offer

CMO: And take a bigger margin hit? Not wise.

CEO: How can this be? We’re spending more, reaching fewer people, hitting the same ones over and over. And ROAS is down?

CMO: Yup.

CEO: Just please don’t suggest broad reach brand building that has no measurable tie to revenue.

CMO: [sends screenshot of Huel case study]

CEO: What’s this?

CMO: Check this out. Sounds like they were seeing diminishing returns like us

CEO: So what did they do to fix it?

CMO: The exact thing you said we shouldn’t do: broad reach brand building.

CEO: Hmm - triggered rn

CMO: Why?

CEO: We can’t just convert our whole ad plan to ‘reach’. What if we’re just reaching randos who will never purchase?

CMO: That’s not what’s happening. We’re switching some of our existing spend, say 5% to start. The marginal return on that last 5% of spend is terrible, so it’s an easy transition.

CEO: Don’t understand. What do you mean by marginal return?

CMO: The marginal return on our ad dollars goes down for every additional dollar we spend. The first $100k acquires customers at, say, $25 CAC. The next $100k gets them at $50 CAC. The next $100k gets them at $75 CAC. If our profitability limit is $65 CAC, then every dollar in that last $100k tranche is actually unprofitable. We shouldn’t be spending those dollars on new acquisition.

CEO: Still don’t understand. Our customer acquisition cost IS $65.

CMO: That’s our blended CAC. It includes the customers we got for free and looks at total spend over total new customers as a single number. We need to understand the marginal return so we know when to pull back. By shifting some direct-response spend toward options that reach new people, we drive more incremental purchases and increase our marginal return.

CEO: Incremental, marginal—sounds like marketing fluff. Will we grow revenue and profit faster?

CMO: Thank you for calling my profession fluff. But yes, we’ll grow top and bottom line faster than not doing this.

CEO: Well butter my biscuits, let’s pop a wheelie and blow this popsicle stand!

CMO: Who are you?

Got to hang with some legends for day 1 of DTSki

Some things I learned:

LTV:CAC should be our number 1 metric. Ideally 3x

Leverage suppliers for innovation. Ask them for feedback and launch a product with them

Packaging is everything (duh)

Team is everything. Makes me want to move faster towards hiring.

Create spaces where you can learn from those that are 10 chapters ahead of you.

Day 2 about to kick off. Lets gooooo

Grüns wasn't acquired for $1.2b because Unilever can't create a greens gummy of their own.

They got acquired for over a billion dollars because they had a customer base worth acquiring.

They got off the ad->purchase->churn treadmill and prioritized LTV:CAC over everything.

"I run the business — and I would encourage everybody to run their business — at a minimum 3x LTV, fully burdened, delivered-to-the-door gross profit to CAC. That’s best in class."

“I grow as fast as the world lets me at that CAC ceiling. If there are 50k customers in a month I can go get at that efficiency, I’m going to go get them. If it’s 5k this month, I’ll go get 5k.

“The output of that discipline is our growth.”

Most marketers focus on driving that CAC down as low as possible to keep that ratio strong.

Then, if you're most companies, you focus on increasing LTV as if LTV is a psychology problem. That all you need to do is convince your customers to purchase more or purchase again, and that you can push your way to a better ratio.

You think that higher LTV is the byproduct of more emails, more discounts, more win-back flows.

But elite companies like Grüns understand that LTV is not an value extraction problem. It's a value acquisition problem.

Your customers arrive with their potential lifetime value largely set. The best lever isn't squeezing more out of the wrong people who arrive with low potential LTV, it's acquiring more of the right ones that are likely to spend.

Pushing them spend more is only affecting the last few percentage points of the LTV that plays out for them.

Almost every Ecom brand owner I know wants to make a BIG exit

Yet even the ones doing $100M/year with MRR can't exit for $100M

Meanwhile Grüns just exited for $1.2B

Huel just exited for $1.1B

Most of you build something that can't be sold

Here's what they did differently:

Your best customers don't become your best customers because you squeeze them harder.

They were your best customers the moment they converted.

They arrived with that potential lifetime value built in.

Retention marketing captures what's already there. It doesn't create it.

You can't turn a one-and-done deal seeker into a 4x repeat buyer with a win-back sequence.

You can't make whales out of guppies.

LTV is an acquisition problem, not an extraction problem.

Grüns understood that, and it's why Unilever wrote a $1.2B check.

Massive congrats to @chadjanis + the Grüns team on today’s acquisition 🐻

~$1.2B in under three years!

There’s a reason this was one of @9operators most popular episodes of last year.

In fact, at least three reasons …

1️⃣ LTV:CAC Discipline

“I run the business — and I would encourage everybody to run their business — at a minimum 3x LTV, fully burdened, delivered-to-the-door gross profit to CAC. That’s best in class.

“I grow as fast as the world lets me at that CAC ceiling. If there are 50k customers in a month I can go get at that efficiency, I’m going to go get them. If it’s 5k this month, I’ll go get 5k.

“The output of that discipline is our growth.”

2️⃣ Building Teams & Brand

“No good brand — no long-term, longstanding brand — is built off of five to ten people. Period. I was pitching back in February of 2024 that I could get this thing to $100 million in revenue with four employees.

“My chief of staff at the time, Katie Cirulli — she’s president of Grüns [now CEBO] — made a comment about a month into her role: ‘Hey, I think we need to hire people.’ She laid it out for me. I was like, ‘You’re right.’

“I needed someone to wake me up to that.”

3️⃣ On Pioneering Product

“Every gummy co-man I talked to said ‘that’s not going to work, it’s going to taste disgusting.’ I finally found one willing to give it a go — they also said there’s no way this is going to taste good. I said, ‘Just do it. Here’s the formulation. Let’s all taste it and then we’ll say whether it tastes bad or good.’

“For the first eight months of this business — this is going to sound crazy — our first co-man had 20 bodies with gloves standing around a table, taking eight gummies, sticking them in the sachets, and clamp sealing them. Super manual.

“That’s what you do when you pave the path for a new format to exist in the world.”

——

I’ve had the great pleasure of getting to collaborate with a few of @grunsdaily’s wonderful people:

- @DerekLauermann

- Katie Cirulli

- @connordault

Plus, @fulfilio’s @MattParkin20 was kind enough to foot the bill so we could run our first giveaway at Operators with Grüns!

Here’s to what you’ve built.

Not building it alone.

Everything that’s still to come!

Oh, and yes … on Monday, I swapped my next flavor for Grüns x @drinkolipop strawberry vanilla; mango is GOAT’d, so let’s see if it can come for the throne

🤓 Grüns Stan for life!

Last question: WHEN ARE YOU COMING ON AGAIN, CHAD?

This is exactly right. And what most brands miss is the input to this entire model: which customers are you actually acquiring?

Your customers exist on a potential LTV curve, and you can nudge them up a little bit with marketing after you've acquired them, but you're much better off simply acquiring better customers in the first place.

If Meta is filling your funnel with guppies instead of whales, your cohorts simply will never pay back the way they need to.

LTV:CAC is the ratio. But LTV is not a dynamic number you achieve after acquiring a customer, it comes predetermined (mostly) with every customer you acquire. Brands that scale like Grüns (which is basically nobody) aren't just disciplined about the ratio, by definition they're disciplined about who they're acquiring in the first place.

I wrote about why LTV is an acquisition problem, not an extraction problem - link in comments 👇

How did Gruns actually scale the way they did, financially speaking?

I dont have any inside info, but I can tell you how. Balancing inventory, CACs, opex, etc during hypergrowth is an extremely difficult task; however on a spreadsheet it can in fact all be reduced down to a very simple mathematical model that is highly dependent on two variables and one ratio:

Lifetime profit per customer divided by the cost to acquire said customer

or for the initiated; LTV:CAC

Put simply, there is approximately a zero percent chance that Gruns had an LTV:CAC less than 3.0x. Further, if they did manage to somehow scale without 3.0x, Unilever wouldn't have acquired them.

My best performing substack post ever (will link in the comments) is titled "Why 3.0 LTV:CAC"

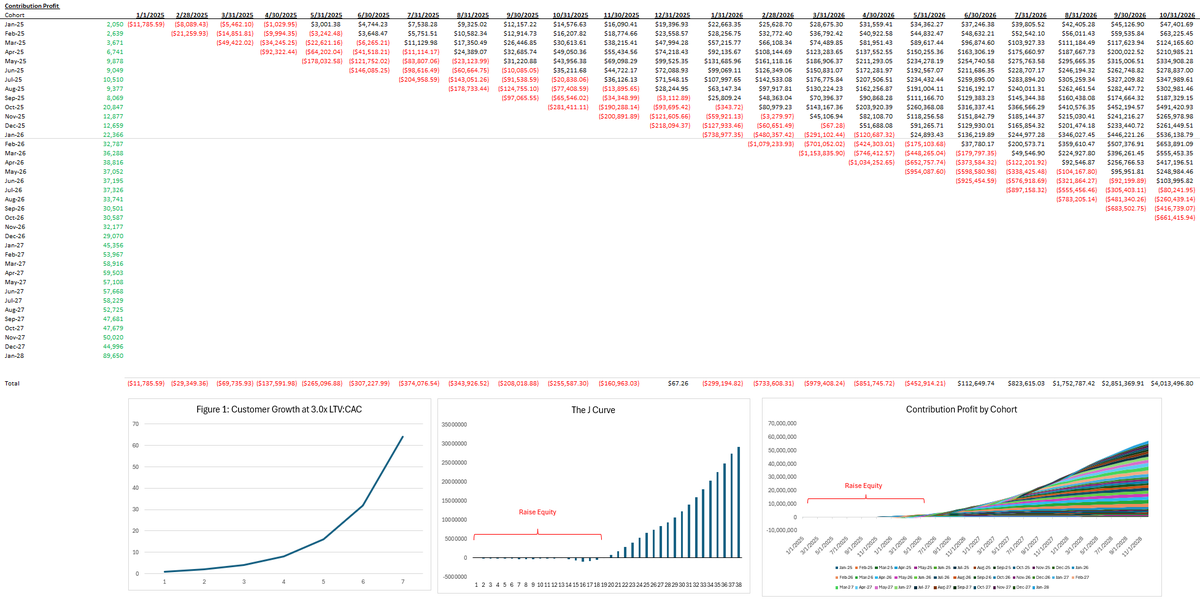

Summarized into a sentence; the answer is: because when 1 customer gives you enough profit to pay back the first customer and acquire 2 more customers, you can grow exponentially. 1 customer turns into 2, 2 customers turns into 4, 4 turns into 8 and voila - you have your hockey stick (figure 1).

Over time, the wide majority of revenue becomes repeat customers. Terminally, a healthy ratio for new:repeat is about 30% new to continue compounding at an exponential rate.

However, you are acquiring these customers at a loss on the first purchase. In the early days, this creates a cash burn. I theorize that this is why Gruns raised fairly significant capital early on, becuase they recognized the nature of the 'J-curve'

The J-curve is when you are burning cash on customer acquisition, and you don't yet have enough cohorts returning to actually cover the cost of the marketing investment you're deploying to acquire new customers. It creates a period of negative contribution prior to a period of compounded profits, in the shape of a J.

When you have the proper LTV:CAC, the business case for financing the negative portion of J curve with equity is very very strong, hence the early capital raising.

So the calculus is essentially:

establish unit economics -> raise capital ->scale

The most critical part of executing on this model is ensuring that as you scale customer acquisition, each cohort is CREATING enterprise value, not DESTROYING it. This is where 99% of founders fail.

EV is only created then those cohorts pay back and start generating profit. As you scale, often CAC goes up so much that cohorts never pay back, and you are actually losing money and destroying enterprise value, even if revenue is going up.

This is where the phrase 'not all growth is good growth' comes from.

And that ladies and gentleman, is your financial modeling primer. Someone told me not to put the term 'financial modeling' at the front of this post because they will fall asleep, but ha ha i've tricked you into learning it!

This is the kind of work we do every day with brands at iris. We deploy agents to clean your data & build your models. if that sounds like something you could benefit from, shoot me a DM

![PrestonRuther10's tweet photo. CEO: Why the f*** aren’t we growing?

CMO: [Slacks screenshot of Meta ads account YOY]

CFO: WTF? That can’t be real.

CMO: I get we want “accountability” and “ROI,” but the obsession with short-term, bottom-funnel demand harvesting is causing us to shrink as ROAS slowly declines.

CEO: We need to increase the number of ads we launch.

CMO: We’ve already 10x’d the volume

CEO: Then we need more creative diversity.

CMO: We have. Our Meta rep says we’re crushing it.

CEO: We need a better offer

CMO: And take a bigger margin hit? Not wise.

CEO: How can this be? We’re spending more, reaching fewer people, hitting the same ones over and over. And ROAS is down?

CMO: Yup.

CEO: Just please don’t suggest broad reach brand building that has no measurable tie to revenue.

CMO: [sends screenshot of Huel case study]

CEO: What’s this?

CMO: Check this out. Sounds like they were seeing diminishing returns like us

CEO: So what did they do to fix it?

CMO: The exact thing you said we shouldn’t do: broad reach brand building.

CEO: Hmm - triggered rn

CMO: Why?

CEO: We can’t just convert our whole ad plan to ‘reach’. What if we’re just reaching randos who will never purchase?

CMO: That’s not what’s happening. We’re switching some of our existing spend, say 5% to start. The marginal return on that last 5% of spend is terrible, so it’s an easy transition.

CEO: Don’t understand. What do you mean by marginal return?

CMO: The marginal return on our ad dollars goes down for every additional dollar we spend. The first $100k acquires customers at, say, $25 CAC. The next $100k gets them at $50 CAC. The next $100k gets them at $75 CAC. If our profitability limit is $65 CAC, then every dollar in that last $100k tranche is actually unprofitable. We shouldn’t be spending those dollars on new acquisition.

CEO: Still don’t understand. Our customer acquisition cost IS $65.

CMO: That’s our blended CAC. It includes the customers we got for free and looks at total spend over total new customers as a single number. We need to understand the marginal return so we know when to pull back. By shifting some direct-response spend toward options that reach new people, we drive more incremental purchases and increase our marginal return.

CEO: Incremental, marginal—sounds like marketing fluff. Will we grow revenue and profit faster?

CMO: Thank you for calling my profession fluff. But yes, we’ll grow top and bottom line faster than not doing this.

CEO: Well butter my biscuits, let’s pop a wheelie and blow this popsicle stand!

CMO: Who are you?](https://pbs.twimg.com/media/HFTYZC1acAAMn1f.jpg)

![PrestonRuther10's tweet photo. CEO: Why the f*** aren’t we growing?

CMO: [Slacks screenshot of Meta ads account YOY]

CFO: WTF? That can’t be real.

CMO: I get we want “accountability” and “ROI,” but the obsession with short-term, bottom-funnel demand harvesting is causing us to shrink as ROAS slowly declines.

CEO: We need to increase the number of ads we launch.

CMO: We’ve already 10x’d the volume

CEO: Then we need more creative diversity.

CMO: We have. Our Meta rep says we’re crushing it.

CEO: We need a better offer

CMO: And take a bigger margin hit? Not wise.

CEO: How can this be? We’re spending more, reaching fewer people, hitting the same ones over and over. And ROAS is down?

CMO: Yup.

CEO: Just please don’t suggest broad reach brand building that has no measurable tie to revenue.

CMO: [sends screenshot of Huel case study]

CEO: What’s this?

CMO: Check this out. Sounds like they were seeing diminishing returns like us

CEO: So what did they do to fix it?

CMO: The exact thing you said we shouldn’t do: broad reach brand building.

CEO: Hmm - triggered rn

CMO: Why?

CEO: We can’t just convert our whole ad plan to ‘reach’. What if we’re just reaching randos who will never purchase?

CMO: That’s not what’s happening. We’re switching some of our existing spend, say 5% to start. The marginal return on that last 5% of spend is terrible, so it’s an easy transition.

CEO: Don’t understand. What do you mean by marginal return?

CMO: The marginal return on our ad dollars goes down for every additional dollar we spend. The first $100k acquires customers at, say, $25 CAC. The next $100k gets them at $50 CAC. The next $100k gets them at $75 CAC. If our profitability limit is $65 CAC, then every dollar in that last $100k tranche is actually unprofitable. We shouldn’t be spending those dollars on new acquisition.

CEO: Still don’t understand. Our customer acquisition cost IS $65.

CMO: That’s our blended CAC. It includes the customers we got for free and looks at total spend over total new customers as a single number. We need to understand the marginal return so we know when to pull back. By shifting some direct-response spend toward options that reach new people, we drive more incremental purchases and increase our marginal return.

CEO: Incremental, marginal—sounds like marketing fluff. Will we grow revenue and profit faster?

CMO: Thank you for calling my profession fluff. But yes, we’ll grow top and bottom line faster than not doing this.

CEO: Well butter my biscuits, let’s pop a wheelie and blow this popsicle stand!

CMO: Who are you?](https://pbs.twimg.com/media/HFTYZC3akAA0khV.jpg)