Worked for 29 Years at a Major Brokerage. Passion is selling Cash Secured Puts, Covered Calls and buying LEAPS. It's a journey that keeps getting better!

In case you’re keeping score America is the only country on earth…

With birthright Citizenship

no voter ID

And a MASSIVE social welfare system

Yeah I can’t imagine why we’re in so much trouble

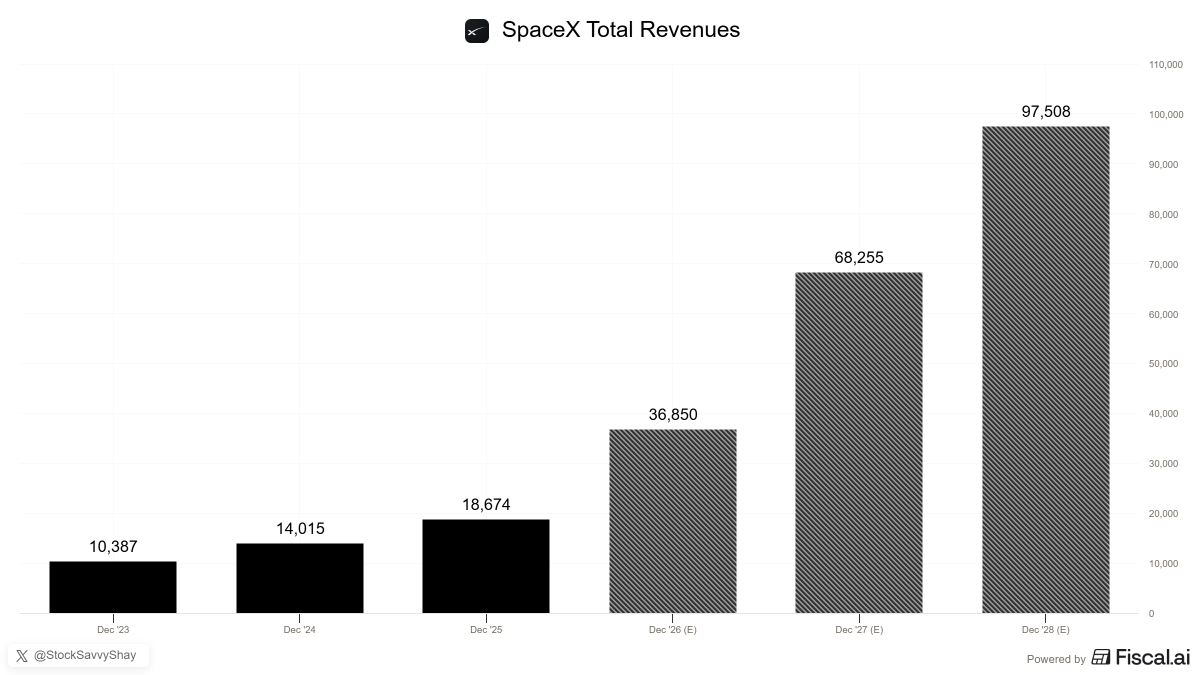

$SPCX is expected to approach ~$100B of revenue by 2028 which would make SpaceX one of the fastest-scaling businesses in the world at this size.

The reason that ramp is even possible is that SpaceX controls the launch layer, uses that launch capacity to scale Starlink, uses Starlink cash flow to fund Starship and is now adding direct-to-cell, V3 satellites, AI compute leasing and Grok/X distribution on top.

Starlink has scaled past 10M subscribers in under five years and is still early with next-gen V3 satellites carrying 10x the downlink capacity of V2 and direct-to-cell already reaching millions of devices across 30+ countries through partnerships with 30+ mobile carriers.

Starship is the piece that widens the lead further because at ~10x payload of Falcon 9 and built for full reusability where it can collapse the cost per kg to orbit and deploy V3 satellites at scale so every Starship improvement feeds directly back into cheaper launch and a denser Starlink network.

The new wildcard is AI compute where SpaceX is leasing spare Colossus capacity to $GOOGL and Anthropic at a combined ~$26B annualized run rate. What makes that even more interesting is that the recent Cursor acquisition also gives SpaceX a direct play in the application layer meaning it can own the compute, own software that runs on it and use X as a distribution channel.

The path to ~$100B by 2028 comes from launch, Starlink, direct-to-cell, Starship, AI compute and software distribution all compounding inside the same platform in a theme that's just getting started.

@TJTheWheelDeal Not much today. Sold a CSP on $AAOI, 100 strike, Aug 21 expiration, 5 contracts at $10.40. Income $5,100+. It's a higher risk type of stock. .19 delta.

As for the AI trade, it was alive and well last week even though the broad indices mostly treaded water. Note below the S&P 500 ex-AI in green. The rally of the past 12-18 months has been mostly AI.

🧠 Gavin Baker on the staggering potential of AI:

"Imagine Albert Einstein had just thought about fundamental physics 24 hours a day. He doesn't have to eat, he doesn't have to sleep...

And never gets old. Never dies. Never has diminutive intelligence...

And he thought for one year. We might already have solved a lot of these intractable problems...

However bullish I was on compute before then, I'm just a lot more bullish."

— @GavinSBaker (Managing Partner & CIO, Atreides Management) on @BG2Pod with @altcap

The most overlooked part of the SpaceX IPO thesis is the model and most people are completely missing it (Save this)

Everyone has been focused on the Anthropic compute deal and the Colossus revenue because those are numbers you can put in a spreadsheet.

Six months ago, xAI was competing reasonably well on model performance but was not clearly on the frontier.

Then SpaceX exercised its option to acquire Cursor for $60 billion, the largest startup acquisition in history just days after completing the largest IPO in history at $75 billion.

Cursor is a team of 700 to 800 people, was on track to exit 2026 at up to $10 billion in revenue, had millions of professional developers using it daily, and had already built a team with the genuine potential to compete at the frontier, the one thing holding them back was compute.

SpaceX just gave them the largest GPU cluster in the world to work with.

Grok 4.3, a 1.5 trillion parameter model, is currently training with Cursor's proprietary coding data being injected directly into pre-training, not just fine tuning which is a fundamentally more powerful integration than anything the market is currently modeling.

The prior version, Grok 4, was already on the Pareto frontier as of 10 to 12 days ago, the most intelligent 500 billion parameter model in the world, sitting alongside Google Gemini, Anthropic, and OpenAI as one of only four systems at the true frontier.

Composer 2.5, the previous Cursor model was Pareto dominant in coding tasks just before the acquisition closed, meaning SpaceX inherited a model that was already best-in-class in the highest-value AI use case in the market.

The AWS parallel is the one everyone keeps missing.

Bezos built data center capacity for Black Friday, sat on idle infrastructure the rest of the year, and monetized it into what was at the time the most profitable technology business in history and investors hated it in 2009 and 2010 because he was burning free cash flow on capacity that had no obvious revenue yet.

SpaceX is in exactly that position, it built Colossus for xAI's own training needs, is monetizing excess capacity to Anthropic at $1.25 billion per month across 220,000 Nvidia GPUs, and has reportedly secured up to 20% of Nvidia's early Vera Rubin allocation, giving it the most powerful and scarcest GPU infrastructure in the world during the critical window when those chips are hardest to get.

The $60 billion Cursor acquisition closed at a moment when SpaceX had essentially unlimited compute, a team already at the frontier, and a product with deep enterprise distribution, three things no other model lab had simultaneously when it was at this stage.

The market is pricing the compute business conservatively and ignoring the model call option entirely, and coding is the fastest path to AGI, once you are on the Pareto frontier with that compute, revenue scales fast.

Anthropic went from negligible revenue to $30 billion annualized in under 18 months and that is the existence proof.

Bullish on SpaceXAI and @elonmusk

🚀 Brad Gerstner on how SpaceX's IPO story changed overnight:

"In literally 6 weeks, they went from not in the game to $27B of AI hyperscaler revenue with big deals from Anthropic and Google.

I think we can all agree @elonmusk and the team at @SpaceX are as capable as anybody on the planet. Jensen has said they’re #1 at standing up AI data centers... Jensen said they did in 100 days what it took others 2 to 3 years to do.

Going from $18 billion revenue last year to $160 billion, a huge portion of that is standing up AI data centers and leasing them right to the Anthropics of the world...I think they're going to run away and consolidate that business.

My estimate is in a few years they're going to be the largest AI hyperscaler in the United States."

— @altcap on @CNBC

If the 10-year does climb into the danger zone from here, say to 5%, that would equate to a 3 point P/E compression, taking us down towards the pink line below. Again, rising earnings provide the offset to falling valuations, with price as the residual.

🚨 BREAKING NEWS: Tens of thousands of Spencer Pratt voters are now receiving rejection letters from the county clerk saying that their ballots were not counted due to signature irregularities. Yet, Governor Gavin Newsom just passed legislation that would make it illegal for anyone conducting oversight, to contest signatures that they deemed fraudulent. Democrats allow ballots to be signed with an X, a -, or a 🙂 to pass and count, but all of a sudden, only Republican signatures are being flagged for irregularities, rejected, and not counted. 🤔 One of these California Republican voters said that his signature has been on file for over 20 years and there has never been an issue until he voted for Spencer Pratt. Nithya Ramen has beaten Spencer Pratt by less than 3000 votes. There are at least 18,000 Pratt voters who received this letter saying their votes were rejected.

The Equity Valuation and Fed Model chart below shows the distribution of the P/E ratio (top) and the Fed model signal (bottom). Fortunately, equity valuations are largely justified and the Fed model signal is near the middle. That suggests that the current left tail risk is only moderate for now (as compared to the extreme signals in 1987 and 1999).

Inflation is perking up again, with the PCE up 3.8% year-over-year and the core PCE up 3.3%. The latter is of little comfort to anyone who buys groceries or gas. The inflation rate has now been above the Fed’s 2% target every month for 5 years as shown in the Inflation Expectations chart with data sourced from FMRCo and Bloomberg below. 🧵(1/2)

A single gigawatt of orbital compute requires roughly 200 Starship launches and Elon Musk is not satisfied with gigawatts (Save this).

The target is 100 gigawatts of orbital compute per year which means SpaceX is staring down a launch requirement that no organization in human history has ever attempted at anything close to that scale.

He acknowledges that scaling to gigawatts per year in orbit is a very hard challenge, but then points to something most people have missed entirely, SpaceX has already demonstrated the foundational capability, because building and launching thousands of Starlink satellites per year is the same industrial problem applied to a different payload.

When you understand the orbital compute satellite as a larger version of Starlink V3 with an Nvidia GPU rack at the center instead of a communications payload, the manufacturing and launch scaling challenge stops looking like science fiction and starts looking like a production ramp.

The infrastructure to support that ramp is already being built.

SpaceX is currently capacitizing for thousands of launches per year, two launch towers and pads in South Texas are operational, the first pad at Cape Canaveral is nearly complete, a second is on the way at Launch Complex 37, and additional locations are already in discussion.

As the CFO says it "You need to have those cost curves as you ramp up in volume and time, your costs go down."

The vision he describes for what this eventually enables is striking in its specificity.

He imagines asking Grok a question on his phone, the inference running on an orbital compute satellite, and the answer coming back down through Starlink direct-to-cell, a complete AI query processed entirely in space, from prompt to response, without touching a single terrestrial data center.

That moment, he says, is closer than the industry thinks, with initial capability demonstrations possible as soon as next year.

The bottleneck that stands between now and that moment is not the satellite design, the cooling physics, or the silicon, all of which SpaceX has already worked through.