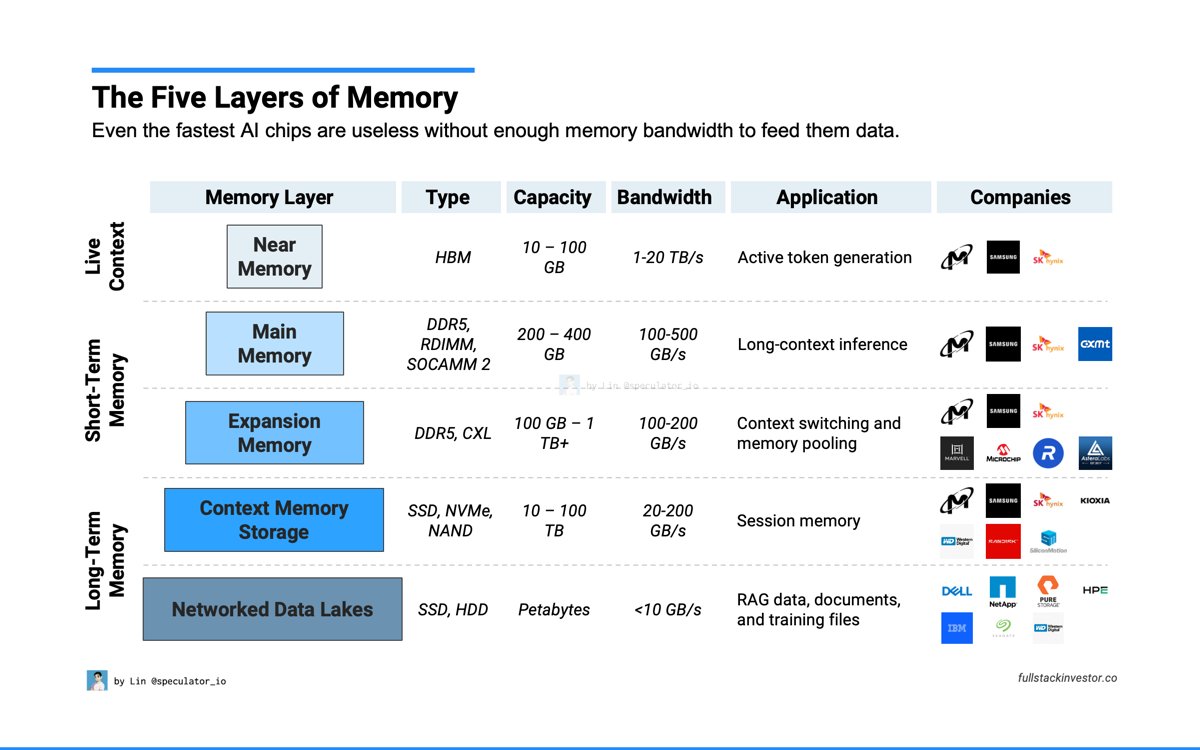

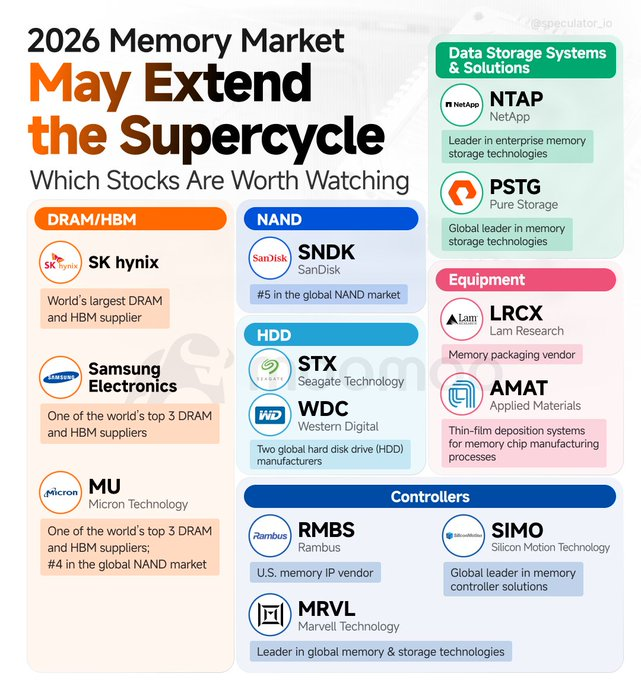

2026 WILL BE THE YEAR OF AI MEMORY

• $MU supplies the DRAM & HBM next to GPUs that let AI think longer & hold more context.

• $SNDK, $STX, $WDC store massive AI datasets & model files so training and inference can scale.

• $PSTG, $NTAP turn raw memory & disks into reliable storage systems enterprises actually run AI on.

• $LRCX, $AMAT build the equipment that makes advanced memory like DRAM, HBM & NAND possible.

• $MRVL, $RMBS, $SIMO design the controllers that control how fast data moves between GPUs & memory.

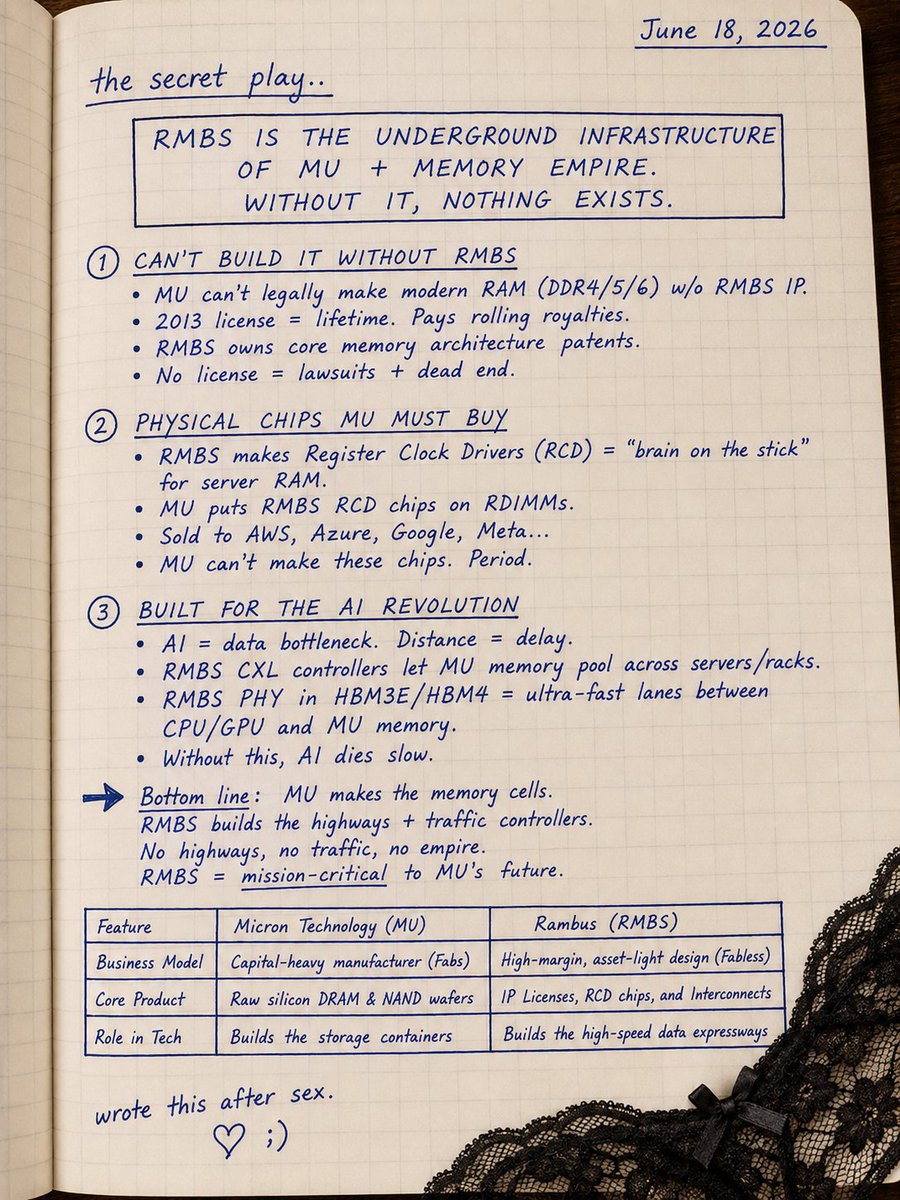

Why $RMBS Is Critical to $MU:

Think of it this way:

$MU builds the memory.

$RMBS owns many of the rules, designs, and traffic systems that make memory work at AI speeds.

Why it matters

• Patents & Licensing

Micron licenses Rambus IP to build modern DDR5, DDR6, and future memory products.

• Server Memory Chips

Rambus supplies critical RCD chips used on enterprise server DRAM modules sold into hyperscale AI data centers.

• AI Data Movement

Rambus develops the interconnect technology that helps move data efficiently between CPUs, GPUs, and memory.

• HBM & AI Infrastructure

As Micron scales HBM memory for AI, Rambus technology helps enable signal integrity at extreme speeds.

The AI Supply Chain Connection

NVDA → MU → RMBS

NVIDIA needs massive amounts of HBM memory.

Micron Technology supplies that memory.

Rambus provides critical IP, chips, and interconnect technology helping that memory function at AI scale.

One-Line Investment Thesis

If Micron is selling the AI memory, Rambus is helping build the roads that allow that memory to operate at full speed. Without advanced memory interfaces, controllers, and IP, AI servers become bottlenecked long before they reach their full performance potential.

$SIMO is an under-the-radar picks-and-shovels play on AI-driven NAND demand.

Everyone looks at the NAND suppliers first: $SNDK, Samsung, SK hynix, Kioxia, $MU. Makes sense.

But if AI workloads start using flash as a cheaper warm memory tier between HBM/DRAM and cold storage, then the SSD controller becomes a key piece of the stack.

That’s why $SIMO is interesting. They sell the controller brains that make NAND usable: speed, reliability, endurance, power efficiency, QoS, and enterprise-grade performance.

And there are signs they’re moving beyond phones/client SSDs.

Their MonTitan enterprise SSD controller platform is aimed at data-center and AI workloads, and they showed AI storage products at NVIDIA GTC around near-GPU storage, KV-cache extension, warm data storage, and AI server boot drives.

That maps directly to the idea that flash is becoming part of the AI memory hierarchy, not just cell phone/PC storage.

The catch: this is still early. $SIMO is not a pure data-center name yet. eMMC/UFS and client SSDs count for a large chunk of revenue, so the enterprise AI storage piece has to become big enough to move the model.

But if NAND becomes more important to AI infrastructure, $SIMO looks like one of the cleaner picks-and-shovels names hiding in plain sight.

Q1 2026 revenue was $342.1M, up 23% sequentially and 105% year over year, and the stock has clearly re-rated since. Not cheap anymore, but if AI-driven NAND demand keeps growing, this could still have room to run.

MARKET MECHANICS LESSON:

Why MRVL Crashed Into the Close

Yesterday MRVL ran from ~$305 to ~$329 by mid-afternoon. Then it fell $19 in 10 minutes and crossed at $310.58. No news. No earnings miss. No downgrade. Pure mechanics. Here's what happened and why it matters.

THE SETUP: INDEX INCLUSION ARBITRAGE

When a stock gets added to a major index, passive funds are required to buy it at the closing price on inclusion day. They have no choice. They must own it by the close. Everyone knows this in advance.

Arbitrage firms exploit this. In the days leading up to inclusion, they accumulate shares before the passive funds are forced to buy. Then they sell into the guaranteed demand at the close. The profit is the spread between their entry price and the closing cross.

THE MRVL TRADE:

June 15-17: Arb desks accumulated roughly $20-30B of MRVL inventory through dark pools. Blended cost: approximately $290-300.

Yesterday morning: MRVL ran from $305 to $329. Momentum traders and short-covering piled in ahead of the inclusion print. The arbs sat on their inventory and watched the price rise. Every dollar higher was additional profit on their position.

3:50 PM: The MOC (Market on Close) imbalance feed published. This is the official number that tells the market how much net buying the passive funds need at the close. The imbalance indicated $5-8B of net buying needed.

THE PROBLEM: The arbs had $20-30B of inventory to sell. The passive funds only needed $5-8B. There were 3-4x more sellers than buyers.

3:50-4:00 PM: The arbs recognized the mismatch instantly. They started selling aggressively on the lit order book to clear inventory before the close. They couldn't wait for the 4:00 PM cross because there wasn't enough passive demand to absorb their full position. MRVL dropped from $327 to $310 in 10 minutes.

4:00 PM cross: $310.58. The passive funds got their full allocation at this price. The arbs unloaded the bulk of their inventory. Still profitable. They bought at $290-300 and sold at $310. But significantly less profitable than $327.

4:01-4:14 PM: The remaining $10B+ of residual inventory cleaned up through dark pool and swap structures at the official close mark.

THE OPTIONS TELL:

At 3:33 PM, with MRVL trading at $327.62, someone bought $310 puts expiring that same day for $0.24. Those puts were 5.4% out of the money with 27 minutes until expiration. On any normal day, that's a lottery ticket that expires worthless.

Those puts went deep in the money. MRVL crossed at $310.58. The $310 strike was at the money at the close. A $0.24 option became valuable in 27 minutes because the buyer understood the inclusion mechanics that were about to unfold.

THE LESSON:

This wasn't manipulation. It wasn't a crash. It was the predictable resolution of an arbitrage supply-demand imbalance.

The passive funds created guaranteed demand. The arbs front-ran that demand. The arbs accumulated more inventory than the demand could absorb. The MOC imbalance revealed the mismatch at 3:50 PM. The arbs sold into each other trying to exit first. The price fell to the level where supply met demand.

Every index inclusion event has this dynamic. The magnitude depends on the gap between arb inventory and passive fund demand. When the arbs overestimate the demand (or over-accumulate inventory), the closing cross is violent. When the sizes match, the cross is orderly.

The flow told the story before the price did. The dark pool accumulation over three days mapped the arb inventory. The MOC imbalance at 3:50 PM revealed the mismatch. The options market at 3:33 PM showed someone positioning for the exact outcome. The mechanics were visible to anyone watching the right data.

This is why we track flow, not headlines. The mechanic says: index arbs over-accumulated and the MOC imbalance was too small to absorb them. Same result. Different understanding. Different edge next time.

$MRVL $SMH $QQQ

William O’Neil (1933–2023) explains how the general market creates major tops long before most investors realize what’s happening.

In this classic lesson, O’Neil analyzes more than 10 leading stocks simultaneously, showing how market leaders often begin breaking down before the broader market peaks.

Featured names include:

$NASDAQ

$AAPL

$NFLX

$AMZN

Green Mountain Coffee

Cerner

VistaPrint

https://t.co/QTlCXZnv3l

$BIDU

Express Scripts

Synaptics ($SYNA)

One of the greatest investing lessons you’ll ever study:

Don’t just watch the indexes.

Watch the leaders.

When leading stocks start cracking, the market top may already be forming.

A timeless masterclass from the founder of CAN SLIM and one of the greatest growth investors of all time. 👇📈

$SPX Continues to follow the blueprint.

A near-term pause before challenging new highs would actually strengthen this potential bullish formation.

👉Higher lows just under key resistance are powerful.

One of the biggest downsides of chop not discussed enough is the after math opportunity cost missed.

You are sick of taking losses so you hesitate when you shouldn’t and then find yourself locked out wanting to FOMO bc you over traded the chop/basing.

The cycle repeats over and over.