I used to wave away quantum computing (QC) risks to Bitcoin as far-fetched. I don’t anymore.

The usual pushback goes like this: QC isn’t a threat for years, and if it is, then the whole financial system is in trouble anyway. That line of nihilistic thinking may be comforting to some, but it misses the point.

Big banks aren’t sitting idle. They’re already investing in quantum research, building internal teams, partnering with QC developers, and thinking about how to harden their systems over time. They’re not “quantum-safe” today — but they’re not starting from scratch either.

Bitcoin is different. It can upgrade, technically. But doing so requires slow, messy coordination across a decentralised network. There’s no risk committee, no mandate, no one who can just say “we’re switching now.”

So this isn’t about panic or pretending I know the precise timelines. Maybe QC is five years away. Maybe it’s fifteen. The problem is that quantum risk is low-probability but massive-impact — and those are exactly the risks decentralised systems struggle to deal with early.

Add AI into the mix, and it’s at least plausible that timelines compress rather than extend.

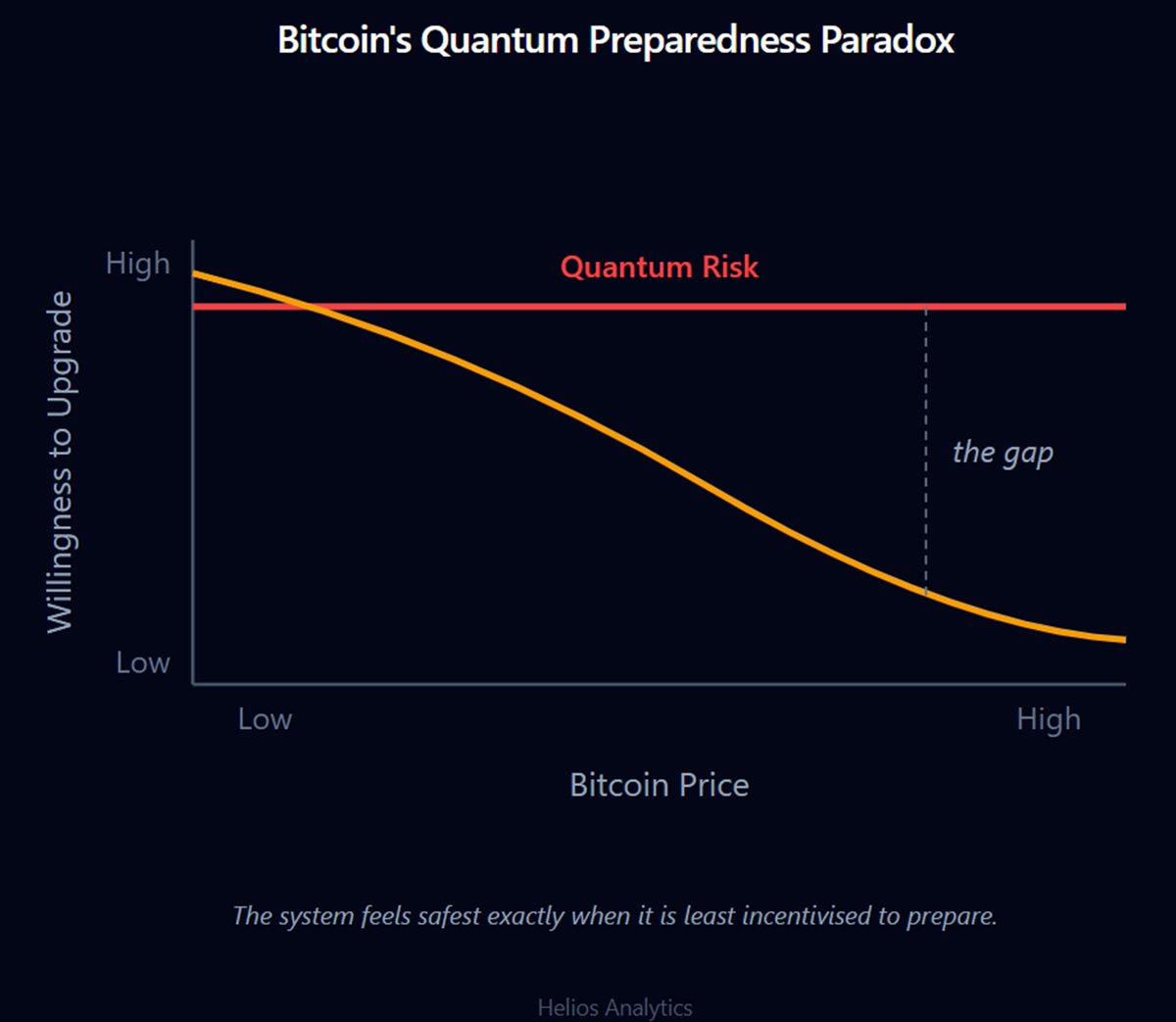

What’s interesting is the growing gap between developer confidence and institutional behaviour. Even if developers think there’s a zero percent chance of a quantum threat in the next five years, some institutions are clearly pricing it higher.

The recent decision by CLSA strategist Chris Wood to remove BTC from his widely followed portfolio due to QC risk may look like “paper hands,” but it matters. It signals that quantum risk is entering institutional risk frameworks — even if views differ widely.

And those views do differ. There’s plenty of counter-evidence. Harvard’s reported decision to increase its exposure by roughly 280% shows institutional support for Bitcoin isn’t disappearing. What’s changing isn’t demand, but dispersion — my guess is that institutional alignment on how to price tail risks diverges further as the QC threat rises.

It’s also plausible that Harvard’s decision had nothing to do with quantum risk at all. Falling volatility alone, consistent with their asset-allocation framework, would justify a higher weighting.

There’s nuance and a lot of in-depth technical understanding, which I’m still working through. But asking these questions is reasonable. @caprioleio has been pushing on this for a while, and he’s right to challenge the shrug-it-off attitude.

What is unreasonable is pretending that JPMorgan and Bitcoin face the same problem. One can prepare in advance and mandate change. The other has to convince everyone, in advance, that a future threat is worth acting on.

Which brings me to the incentive problem.

As Bitcoin’s price rises, confidence rises — and the willingness to push through disruptive, precautionary upgrades falls. The system feels safest exactly when it is least incentivised to prepare.

Quantum risk doesn’t move with price, but the gap does.

Concentrated liquidity coming to @THORChain is absolutely huge.

Liquidity inefficiency has been a big problem.

This will result in better quotes, and so more volume.

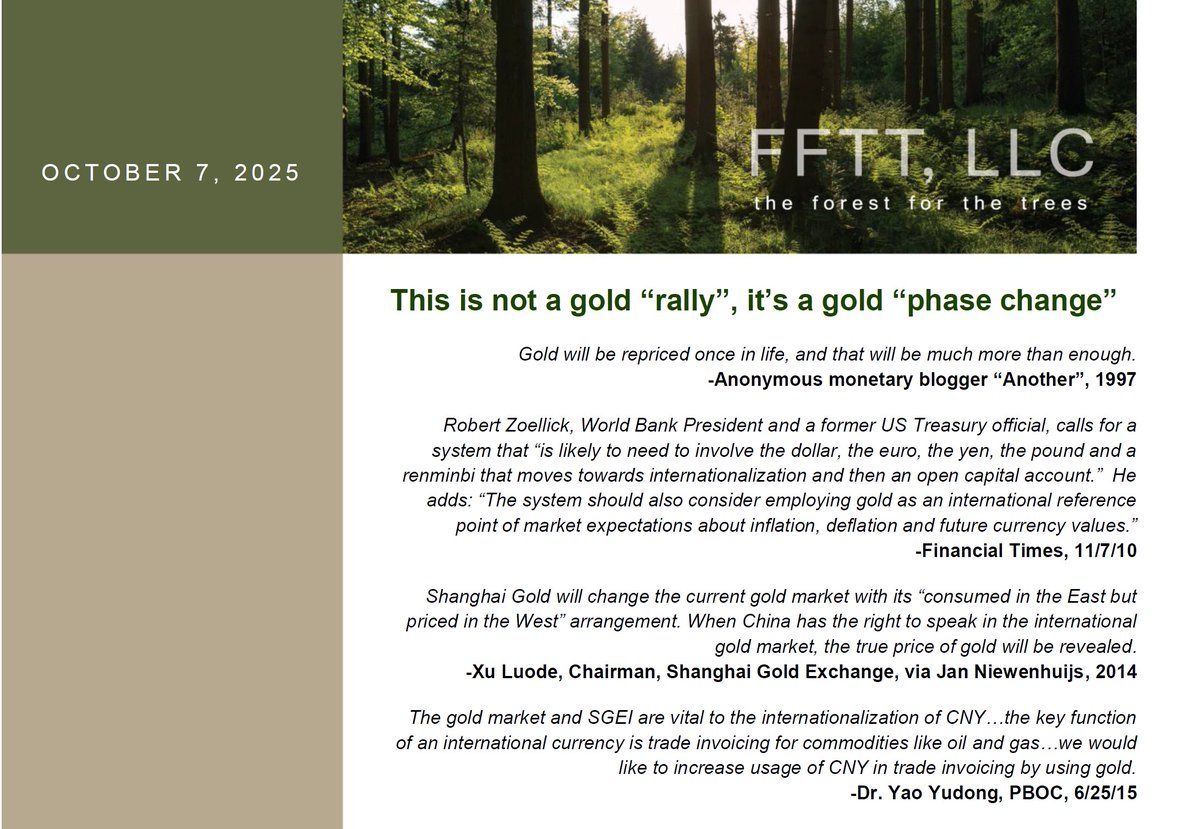

October 7, 2025 edition of FFTT full report: "This is not a gold 'rally', it's a gold 'phase change.'"

Gold price: $3,971.

"Gold will be repriced once in life, and that will be much more than enough." -ANOTHER, 1997

While the crypto bill might be delayed to keep working on it, I am very confident that a bill will get done soon. I have spoken to over 10 senators on both sides of the aisle in the past 24 hrs and I believe they all are working in good faith to get something done. Always gets tense at the end.

Thanks for the response! I disagree, so addressing each:

1. I don’t think there a mechanical reason to suggest that you are long and currency if you own an assets in it. The difference between local FX and foreign investing is a huge deal. When you buy a house in USD- you give up, you USD for the house. The house is denominated in the USD. If the dollar rises 50% against all currencies— it doesn’t have a direct pricing link to your house. You can make many macro cause-and-effect theses here ofc, but those are not at all direct pricing links. If you’re a local investor, you’re just not taking on FX risk.

2. What you’ve described is correct— but I think you missed that the cost of capital is the dominator for the present value of equities. What benefits cash/USD holder? Higher cash rates. But that *hurts* equities. This is why typically a falling dollar via easing vs RoW has come alongside strong equities. Does this always hold? No- but that’s the point, the macro links are time varying and inconsistent. But the thing we do know for sure— if USD cash rates are higher, equities are being discounted at a higher discount. The drivers operate in opposing directions. Are there arguments for the dollar and equities to be more correlated in today’s era? Yes for sure. But they are not from the cost of capital changes, because those are mechanically opposed to stock prices.

3. I think this visual is actually misleading, and dare I say, may even contain some fuckery. Not blaming you at all! but the original author may have take some liberties. They have compared a ratio of US to non-US stocks vs the real effective change rate of the dollar.

If we look at both items individually:

US vs non-US: this is denominated in USD, which is a big problem. What you have is:

(US Stocks, local FX - Foreign Stocks, local FX) + USDFX Rate

The us and foreign stock are actually *very* correlated over time. But the US has a stronger drift upwards. So, a lot of the upwards trajectory is just US stock outperformance. The remainder of the variance is just USD, which will dominate. So it’s literally the dollar

Real Dollar: you have a similar situation here. Nominal Exchange Rate + Inflation Differential. The inflation differentials play very little role in the variance over time. The primary driver is again, the nominal dollar

So what you’re really looking at is a comparison of the dollar, to the dollar. No wonder they correlate!

The Points module was one of the most requested features from Orderly One DEXs.

You asked for it so we built it.

A fully customizable points system, bespoke for your users.

In the latest issue of State of the Network, Tanay Ved observes from @CoinMetrics data that #crypto capital is concentrating in larger assets and liquidity pools as the investment universe expands, with #Bitcoin dominance rising and the #altcoin segment narrowing, highlighting structural shifts in market composition.

Key Takeaways:

🔹 As the crypto investment universe expands, capital is becoming more selective across a smaller set of assets: Bitcoin dominance is in a sustained uptrend, while growth in stablecoins and onchain derivatives compresses the space for the altcoin segment.

🔹 The altcoin segment is narrowing and becoming more top‑heavy, with the top 10 altcoins now representing about 82% of its value, up from roughly 70% over the prior five years.

🔹 Large caps have decisively outperformed mid and small caps since 2023, and post‑shock behavior has reinforced a preference for more liquid, established assets.

➡️ Read the full issue: https://t.co/2UbXRDlJqo