@HistoryInvestor is a dividend portfolio manager and author.

On the Paradigm Shock Podcast, he dropped a take that stopped me cold:

Capital gains are a forced reduction of ownership. Dividends aren’t.

It’s a powerful - and, for many uncomfortable - idea.

Let’s unpack it 🧵

@ramit @mike_kothakota Isn't lumping them all together unfair? There are major differences between credentialed fiduciaries and sales people. Yet both may charge AUM. Educated and credentialed advisors provide a valuable service to clients that goes far beyond just investments.

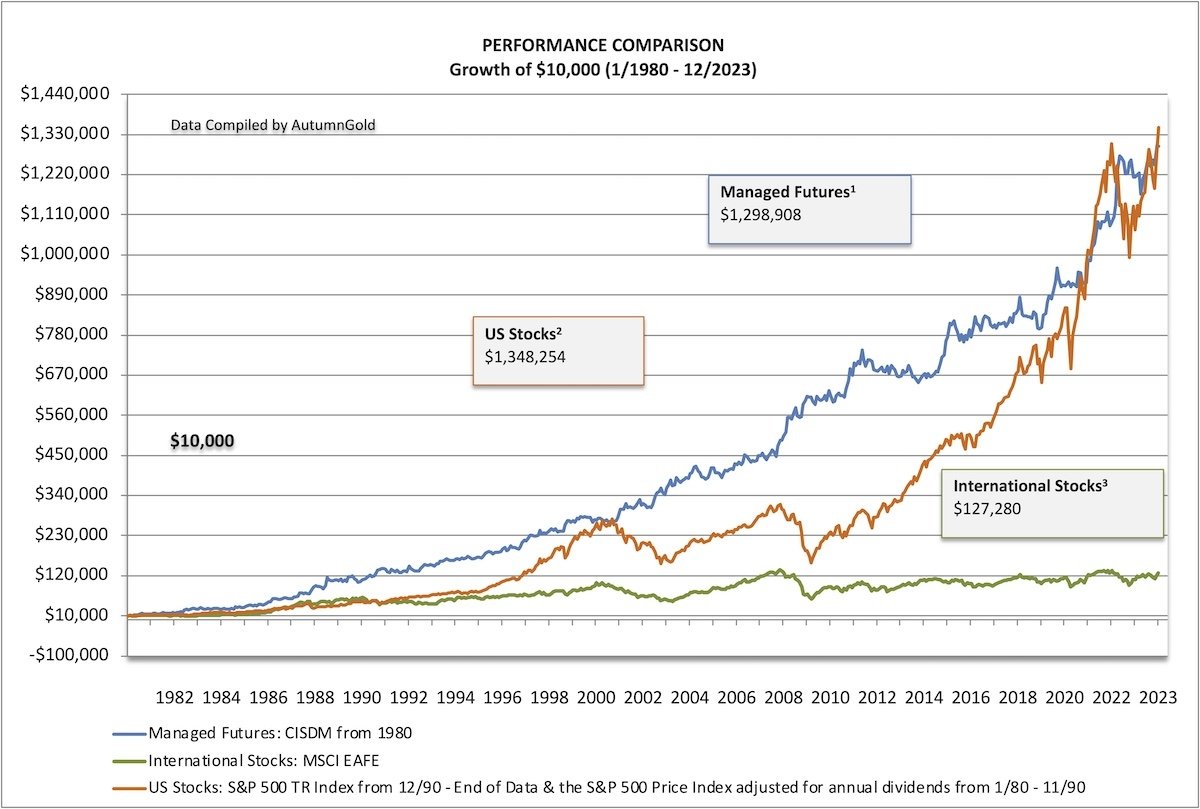

@HML_Compounder@MaciejWasek @IndexWealthy @andrewdbeer1 I think @IndexWealthy is also missing that you do not look at managed futures in isolation, but as part of a portfolio. The long term record is in favor of managed futures.

@TrendingValue How is he defining "recent" and "atrocious"? SCV returns for the last 5 years CAGR 14.56% narrowly trailing the S&P 500, 3 years 11.25% beating the S&P 500, YTD 18.96%. Hard to call this kind of performance "atrocious." @ErnRetireNow

@DominantPort@MarkMcGrathCFP@RationalRemind I get it. Not everyone is meant to hold a scientifically constructed, evidence based portfolio with high tracking error. My point is that owning broad indexes with 13K securities is speculating not investing.

@ramit People have been conditioned by the real estate lobby and simple inertia (thats what you do) that buying a house is the surest way to wealth. A look at the historical data will reveal that housing is a horrible investment in the aggregate. But you are right, few run the numbers.

@LoonieDoctor@MarkMcGrathCFP Happy to.

1: https://t.co/4LXq3ZM2Hz

2: https://t.co/XL67UsK0BK

There is a broad range of studies which support the conclusion that hyper-diversification, which we will define as diversification beyond 50-100 names in any one market, is counterproductive.

@LoonieDoctor@MarkMcGrathCFP Agree that you need more than 50 names total to have a diversified portfolio. But the idea that you need thousands has been disproven by the research. The relationship between concentration and excess returns is convex. You need maybe 150 names globally.

@MarkMcGrathCFP 2 things drive investment success: 1. Exposure to the factors 2. Ability to hold that exposure even when it gets difficult to do so. Research shows focused factor exposure leads to better outcomes. Read Quantitative Value.

@MarkMcGrathCFP Just saying it is an irrelevant data point. Research has proven investors can achieve sufficient diversification with 50 names. Owning 13,000 is unnecessary.