I’ve decided to make Oil 101 online second edition free.

Because clearly the world needs more experts before the next spike hits.

Grab it now while you still can and pretend like me that you saw it coming.

https://t.co/XDgbbMHc7W

The second edition of Oil 101 is now live and includes a full audiobook read by me.

There are four free chapters. Check it out at:

https://t.co/F1Dk8pwgQx

I am Nate Anderson, the founder of Hindenburg Research referenced repeatedly in this bizarre and fantastical interview. During my career, I helped expose numerous financial scams, including over a dozen Ponzi schemes and numerous instances of public companies lying to and stealing from investors: https://t.co/a40Lw3zTMp

I am immensely proud of that career including our work on Nikola Motors referenced in the interview.

Trevor Milton is a convicted fraudster held criminally responsible for the incineration of hundreds of millions of dollars in retail investors’ hard-earned money. As should be unsurprising, Milton in this interview seems to just fabricate key events and information out of thin air – unfortunately with zero critical questioning or pushback from Tucker.

For starters, contrary to Trevor Milton’s implications that his prosecution was some sort of Biden administration conspiracy, conveniently neither Milton nor Tucker share that the investigation into Milton was started and disclosed in September 2020 – under the first TRUMP administration and well before the 2020 election.

There were numerous inaccuracies throughout the interview. The claim that Hindenburg paid employees for inside information is patently absurd. The key whistleblower discussed in the interview was only briefly a contractor for Milton. He was so horrified by what he viewed as Milton’s repeated false claims that he did a tremendous amount of research on his own, unraveling numerous additional suspected lies that Milton peddled to the investing public.

Further, Hindenburg didn’t “coordinate” anything with media or the DoJ. Such entities ran their own investigations for their own purposes unconnected to us. There was ample evidence that Milton misstated numerous aspects of his business, as the company itself later acknowledged.

It would take hours to write about all the other absurdities, half-truths, innuendos and false statements in this interview but in the interest of correcting some of the record, here’s a handful:

- Milton waxes on about his pardon, but no one mentioned that Milton’s lawyer was Brad Bondi—the brother of AG Pam Bondi. Nor did anyone mention that Milton donated $900 thousand to Trump in October 2024, less than a month before the recent election—strategically timed well after his criminal conviction and immediately prior to the presidential election. Trump acknowledged he had never heard of Milton before being asked to pardon him but relied on others for the recommendation.

- Milton failed to mention that immediately prior to his resignation from his company, beyond the extensive allegations of fraud, he was also publicly accused of multiple instances of sexual assault, including by his own cousin, who went on-the-record with her allegations.

- I can only wonder what kind of investigation Tucker undertook of the fraud allegations against Milton before having him on. Milton literally video-taped a truck rolling down a hill implying that it was driving under its own power. He also went up on stage and said a truck that didn’t work “fully functions and works.”

- Waxing poetic about hydrogen in the interview echoes Nikola’s lies to retail investors that it successfully produced hydrogen at a cost ~81% lower than anyone on earth, a feat that would have upended the entire energy industry had it been remotely true. Nikola’s head of hydrogen production, presumably in charge of this world-changing scientific breakthrough, turned out to be Milton’s own brother, who had no scientific background and previously did odd construction jobs in Hawaii.

- These weren’t one-off misstatements—there were dozens of examples like these. As the DoJ said – and proved in court – Milton “made false claims regarding nearly all aspects of Nikola’s business.” The company itself admitted to many of these false statements, agreed to a $125 million fine, and won an arbitration against Milton holding him personally liable for his conduct.

- Milton claimed that Hindenburg made $30m-$100m on our Nikola investment—this isn’t even close (we made a fraction of that). Trevor seems to just be making these numbers up out of thin air.

Hilariously, Tucker opened by suggesting that short selling was illegal until 2007, a claim that is completely false. After confirming that he knows nothing about the subject, he went on to suggest that short selling should be criminalized outright.

Short selling has existed for hundreds of years, and for good reason. Short sellers play a critical role in the functioning of healthy markets, similar to the role of investigative journalists, (which I presume Tucker considers himself akin to).

Most companies are a force for good and economic growth. However, some companies lie and engage in fraud. Short sellers have exposed nearly every major corporate fraud in the past several decades because just as there is an economic incentive for identifying the good companies, there is also an economic model for identifying the scams. This is how free markets and free speech works—helping weed out the bad companies and those stealing from investors so good companies have more room to thrive.

Claiming to be a free speech advocate while casually advocating for the imprisonment of anyone who dares to speak critically about public companies is a contradiction of the highest order.

In short, Tucker, I highly suggest you actually vet the people you welcome onto your platform. If you find yourself staring, mouth agape at your interviewee, repeatedly saying “Wow! This is unbelievable!” it may in fact be because it’s unbelievable.

You reach a lot of people and this one was an avoidable miss. Good day.

Interesting setup over at $CVEO with a highly reputable activist involved.

At its core, the pitch rests on a combination of hidden assets, growing earning power, and the presence of a reputable activist, Engine Capital (which owns 10%), already driving significant changes in capital allocation. My conservative estimate of upside, excluding the value of underutilized assets, suggests a 40% gain over 2.5 years, compared to Engine Capital’s estimate of 100%+ over the same period.

A key aspect of the thesis is the ongoing capital return program. Engine Capital began its campaign in March 2025, pushing management to pivot away from dividends toward aggressive share repurchases. This led to a newly authorized plan to buy back up to 20% of outstanding shares. In the Q1 2025 call, management explicitly kept the door open for an expedited tender offer (as proposed by Engine), which could significantly accelerate value realization given the company’s thin float and tightly held shareholder base (with 40% owned by 3–4 large shareholders). Additionally, with 100% of free cash flow earmarked for buybacks, transitioning to 75% once the 20% repurchase target is reached, the capital return story is front-loaded here.

CVEO operates workforce lodges and mobile camps primarily in Canada and Australia, serving resource companies in remote areas. Its asset-heavy Canadian operations have underutilized capacity that could either be repurposed or sold, while its Australian, asset-light services segment is on a solid growth trajectory, backed by multi-year contracts.

The Canadian assets are currently at a cyclical low in utilization, but could be reactivated quickly if demand returns or sold otherwise. In late 2023, CVEO sold one of its Canadian lodges (McClelland Lake) for $33m. At their peak in 2022, underutilized assets were generating between $20–36m in EBITDA, compared to the expected 2025 EBITDA of $97m. Any new contracts for these idle assets would materially enhance the company’s earning power.

Valuation-wise, CVEO trades at just 5x forward EBITDA (including the recent acquisition), compared to peers trading at 5.5–7.5x. This is particularly attractive given the stability of its long-term contracts, the expansion potential in Australia, and the likelihood of further cost reductions in Canada (large overhead that could be eliminated). Using a conservative estimate of $102m in 2027 EBITDA—and assuming only the currently authorized 20% buyback—the base case implies ~40% upside. Engine Capital’s more aggressive buyback assumptions yield potential upside of over 100%.

Finally, CVEO is not overly exposed to commodity price swings with its current asset base. Its Canadian segment is anchored by long-life oil sands maintenance projects, while its Australian business benefits from tight labor markets and long-term contracts with metallurgical coal miners.

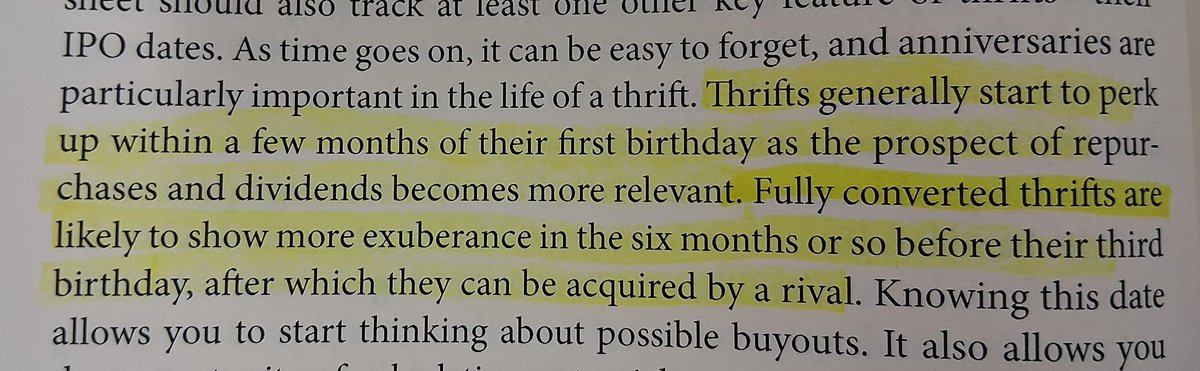

If you want to invest in Thrift Conversions or need to learn what a Thrift Conversion is, this book by @JimRoyalPhD is what you need to buy. Here are just a few of my notes

"set aside a situation room at your home or office, just as police and intelligence agencies do, with a whiteboard, wallboards on which to tack maps and photos, and a list of tasks to be done."

- The Sleuth Investor

@AvnerMandelman The Sleuth Investor takes Philip Fisher's scuttlebutt concept to the next level. The book is different from just about any investment book you will read. Here is a thread on a few of my notes.

"the concept of the “learning curve”. As a firm and its employees gain experience with a manufacturing or service process over time, the unit costs of whatever it is producing will usually fall as a result of the cumulative ongoing tweaking of the process."

- Value Drivers

I haven't heard many people talk about this book, but it's one of my favorites. Filled with so many key concepts and frameworks. Here's a thread on some of my favorite notes.

Below is my most recent update on $DG. The company continues to make strong progress on its issues and I expect further progress in the quarters and years ahead.

https://t.co/QKcFkWthmJ

Rough week for housing so far.

The main theme across our housing coverage lately (homebuilders & existing home market) is that the for-sale housing slowdown is spreading geographically. Showed up clearly in this month’s homebuilder and resale agent surveys, along with hard data.