Not raising money for @Delphi_Digital has been one of the best decisions we've made

Has allowed us complete freedom on how and why we build Delphi, and the company is entirely employee and founder owned

Introducing the Token Design Toolkit

A free tool from Delphi Consulting to model your token design before launch

Stress-test unlocks, liquidity, and demand, then simulate to compare designs

Get insight into your token economy here:

https://t.co/JsQwuB3dP1

The disinflation story is under pressure.

Our markets team has been flagging this for three months, and this week's CPI print is the confirmation. That's a meaningful shift from the pre-war outlook and removes one of the reasons 2026 looked more resilient than 2022.

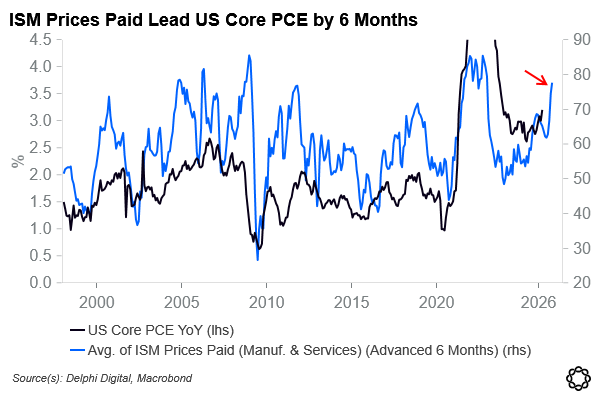

The oil shock from the Iran conflict is showing up in headline CPI. Core leading indicators are moving in the same direction. Prices paid remain elevated across manufacturing and services, and import prices ex-petroleum are picking up.

Wages are what's giving the Fed cover. Wages aren't yet accelerating enough to force the Fed's hand, but last Friday's reaction to a strong jobs print is a preview of how quickly that changes if labor data runs hot.

Against that backdrop, Warsh's first FOMC meeting lands next week. The market has a habit of testing incoming Fed Chairs (Greenspan in 1987, Bernanke in 2006). Consensus expects him to anchor on Dallas Fed Trimmed Mean PCE since it remains subdued.

But as a reminder, headline CPI leads it by six months.

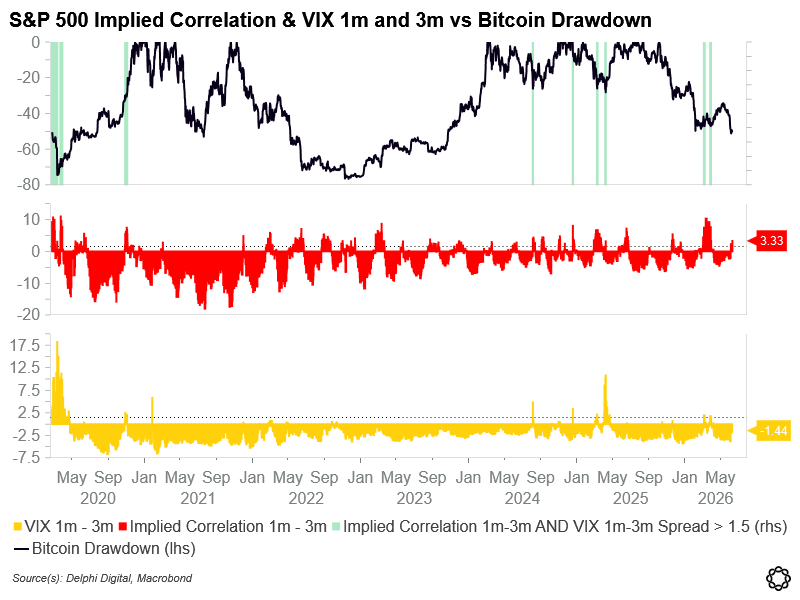

The S&P 500 $SPX Implied 1m-3m correlation spread is widening/+ve (so the market is expecting avg underlying stock correlations over next month will be higher than over next 3 months), but the VIX 1m-3m spread remains negative.

When both these spreads tick materially positive, it has been a historically good signal to bid risk - such as during the end of March sell-off. The same pattern happened then - implied correlation spreads went positive, followed by implied volatility (VIX) spreads.

A new episode of Market Matters is live.

AI continues to lead equities higher while crypto struggles to find a bid.

Our Markets team discusses the AI rally, Bitcoin’s underperformance, the real-yield backdrop, and more.

The team went over the top on this one

Founders, builders, investors -- this is a must read with actionable takeaways for all the above

Bonus: tons of data + beautiful charts

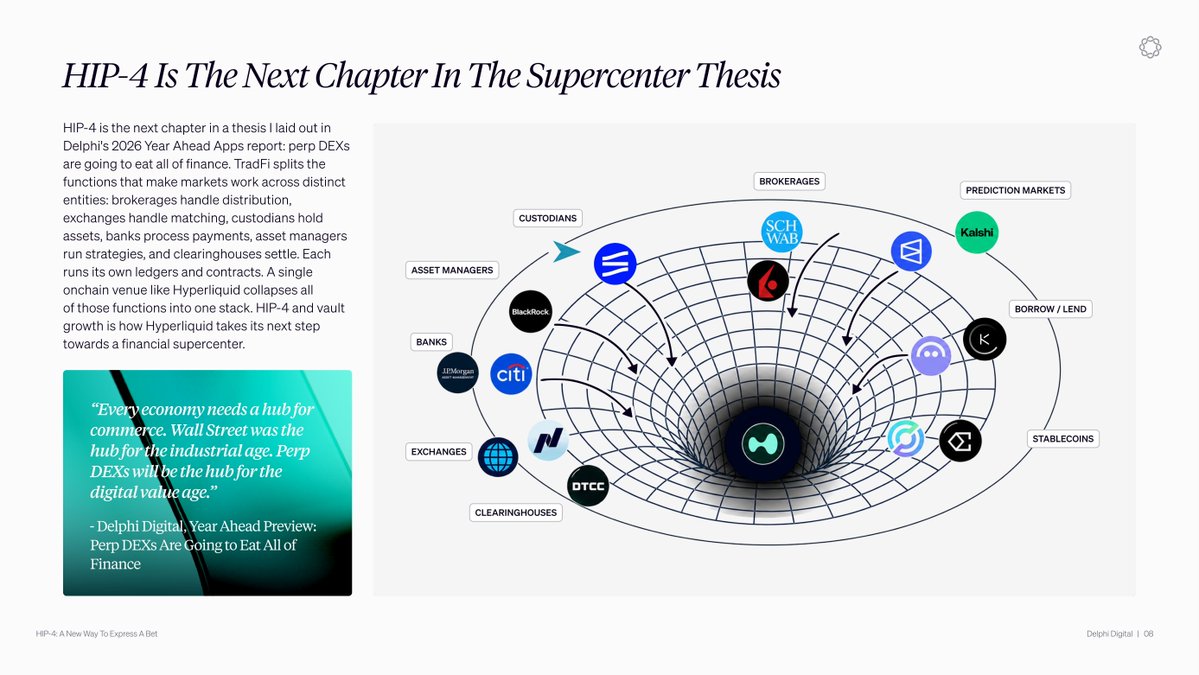

Hyperliquid hyperliquid:native reminds me a lot of MarketAxess $MKTX in 2017, when something like 80% of corporate bond volume was still traded over the phone.

Better tech = lower costs, better liquidity, and not to mention perp futures being possibly one of the most revolutionary innovations in financial markets in recent decades.

Hyperliquid is becoming the financial supercenter of crypto.

Tradfi splits brokerage, exchange, and custody across separate institutions. Hyperliquid is collapsing all of them into one venue with HIP-4 as its latest move.

HIP-4 lets traders express views perps cannot capture. A trader long BTC into the next CPI print can be right about the number and still lose on the price reaction. A binary pays on the outcome itself.

The direct fees HIP-4 generates are small relative to what the trade flow keeps inside Hyperliquid. At expected volumes HIP-4 contributes roughly $25M against Hyperliquid's $636M run rate.

Capital that used to rotate out for event views now stays on Hyperliquid. USDC sitting in the venue generates treasury yield with 90% of it recycled into HYPE buybacks.

HIP-4 also changes what vaults can run. Onchain vaults have been limited to what two linear instruments can express. Outcome contracts add a third instrument that pays on events and nets against the directional book. Curators finally have something new to build with.

Every trade that stays in the venue powers the flywheel.

Our new report "How Far Can Saylor Stretch It" is now live!

STRC has become the center of Strategy’s BTC accumulation model.

The question now is whether each new raise can still add BTC per share after accounting for the common issuance needed to service the preferred stack.

Strategy’s earlier BTC purchases were powered by a wide equity premium. MSTR traded far above the value of its BTC holdings which made new share issuance accretive.

At ~1.24x EV-based mNAV, that math is weaker. Common issuance sits close to the breakeven line and no longer gives Strategy the same clean path to BTC/share growth.

Convertibles were useful because buyers accepted low coupons for MSTR volatility. They also left behind $8.2B of principal and a repayment schedule that starts to matter in September 2027.

STRC now carries more of the load. It gives Strategy access to yield buyers underwriting an 11.5% annual dividend paid monthly, rather than MSTR equity upside. The proceeds can keep flowing into BTC without adding another convert maturity.

The tradeoff is the recurring claim STRC creates. Each raise adds Bitcoin today and another dividend obligation tomorrow. If BTC rises and MSTR’s premium holds, the structure can absorb that cost. If BTC chops sideways, the obligation stack grows while common issuance becomes less efficient.

The stress case is whether STRC-funded BTC purchases can keep outrunning the common issuance needed to service the preferred stack. Strategy’s $2.25B dollar reserve can handle the ~$1B September 2027 put. This buys time but the larger 2028 wall still needs an answer.

The next boundary is the $28.3B STRC authorization cap. Before the cap, STRC can keep adding BTC and offsetting dividend-related dilution.

Without an extension to STRC issuance capacity, reaching the cap means the BTC-buying offset can slow or stop while the dividend obligation remains.

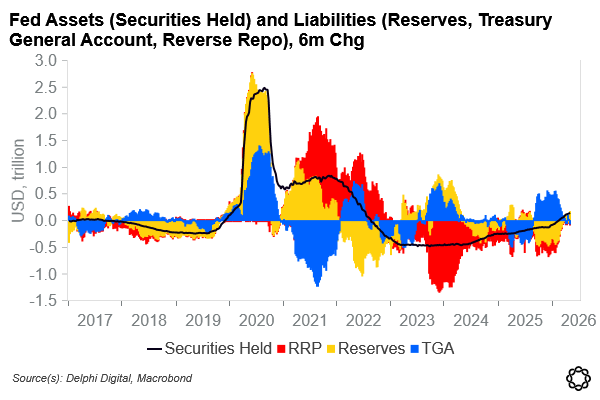

My colleague @that1618guy has done a great job analyzing the dynamics of the TGA, which have been a +ve rate of change impact on liquidity in markets YTD.

Changes in the TGA can be a form of stealth QE or QT that cause reserves to expand or contract; the key question is how the Fed chooses to act in response to changes in the TGA.

For example, in 2020, the TGA (blue bars) exploded higher but this did not result in implicit tightening of liquidity as the Fed massively expanded its asset purchases (black line), allowing reserves to surge higher (yellow bars).

YTD, securities held have risen as the TGA has drawdown, allowing reserves to increase (see second image for a zoomed in view).

While not at 2020 levels, this has been a +ve rate-of-change development for liquidity, and is likely one of the underlying drivers why the margin of safety offered by liquidity has ticked up (although still very negative overall).

We kinda nailed the $ZEC trade from $200, topped up on the dip to $300

1 month later ZEC already hit $550 and is in my initial target range from the lows

I do believe however that we have much higher to go

The newest episode of Market Matters is out now!

This week the team discusses equities at historic highs, rising oil and yields, mega IPOs, crypto market structure, and more.

A new episode of Hivemind is out now!

This week we discuss the market rebound, DeFi exploit fallout, Crypto AI resurgence, and more.

Timestamps:

0:00 Intro + market sentiment shift

08:55 The Aave/KelpDAO exploit explained

17:00 Why DeFi lending models may need to change

37:30 Where DeFi yield still makes sense

38:00 USDAI and real-world AI infrastructure yield

48:20 Venice, Bittensor, and AI token narratives

54:00 How AI agents are changing productivity

1:00:50 What the team is watching next