Silicon Valley Bank unit economics clarify what happened.

And frame likely deposit recoveries.

Like & comment if you want the excel.

6 points:

*1) Basic bank math*

Banks take deposits and use them to make loans.

The delta between interest on loans and interest paid to depositors is the 'net interest margin' ("NIM") - the core metric of bank profitability.

And the delta between assets and liabilities is the bank's equity - the core metric of bank safety.

To generate positive NIM, banks make long-term loans at higher rates than they pay on deposits.

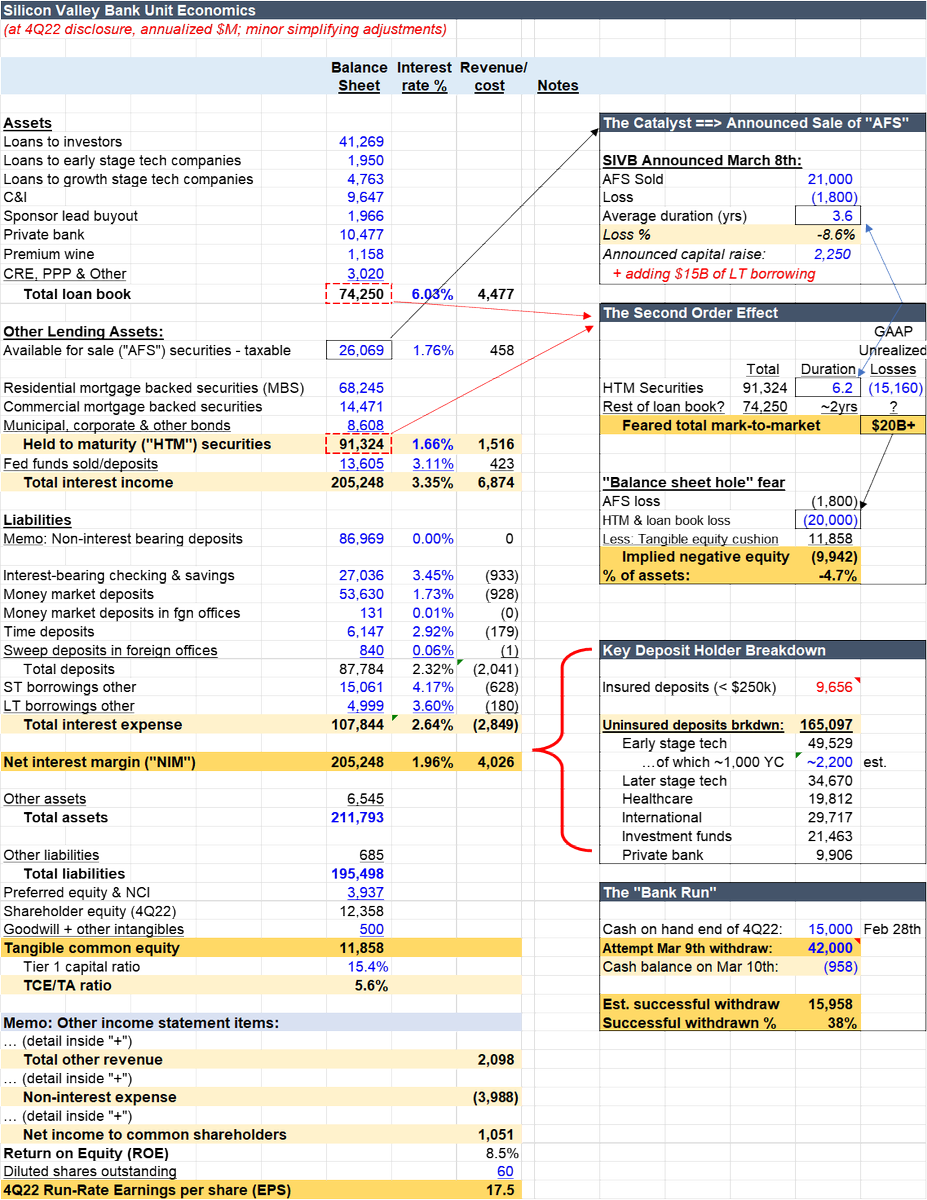

*2) Bank math at SVB*

Before the issues, SVB held $212B of assets against $200B of liabilities - a paper equity cushion of $12B (5.6% of assets).

The assets fall into 3 buckets:

#1: Mortgage backed securities: $82B (83% residential)

#2: Direct loans: $74B (55% short term loans to VCs & PE)

#3: Liquid assets: $55B

The liabilities fall into 2 buckets:

#1: Deposits: $174B (~11% FDIC insured)

#2: Other debt & pref: $25B

*3) What happened?*

The Fed raised rates, making all long-term debt decline in value.

Including SVB's assets.

But accounting rules let SVB book mortgage securities as "held-to-maturity" (HTM), avoiding a hit to book equity.

In a December footnote, however, it disclosed the HTM book had $15B of "unrealized" (i.e. off-book) losses.

So even at that point, losses had wiped out the $12B equity cushion.

*4) What catalyzed the run?*

The wipeout of the bank's tangible equity cushion was concerning.

But the losses were visible to anyone watching SVB closely.

So what changed?

SVB announced Wednesday it had sold $21B of liquid assets (from bucket #3) at a 9% loss and would raise money to cover the loss.

That concerned investors a bit - greater losses than expected and a poor NIM outlook.

But, more significantly, it spooked depositors (and their VC investors).

*5) Bank run*

The next day (Thursday), depositors attempted to withdraw $42B from the bank, of which math implies ~$16B succeeded.

Leaving the bank with negative ~$1B of cash when the FDIC took over Friday.

*6) Simplistic recovery math*

The balance sheet is pretty clear now given how rapid the event was.

The starting point is ~$10B of paper equity ($12B minus the $2B recognized AFS loss).

The range of HTM & other book loss is $20-40B based on the unrealized loss at Dec, the loss on the sale of the AFS book, and market moves.

On net, that impairs assets by $10-30B against a deposit & debt base of ~$162B (deposits of $168B minus the $16B deposit outflow and ~$10B of FDIC insured deposits, plus ~$20B of other debt).

Add in liquidation cost and that implies in the 5-20% loss range on remaining deposits.

Investors will spend time putting a finer point on this.

As always though, the key is to watch headlines, but do math.

Without a solid grounding in the numbers, you're at the whim of someone else's narrative.

That's all for now.

Like & comment if you want the excel.

@timcheadle It’s easy, companies doing riffs can’t discriminate, that means age, sex and gender. Sooo let’s say they want to downsize by 10%, that means associates get swept up regardless of performance in order to prove a non-biased approach. The employee has right to view riff demographics

Just signed an LOI to purchase my 16-year-old a tiny eCommerce business on Microacquire.

This is going to be more educational than anything he will learn in school.

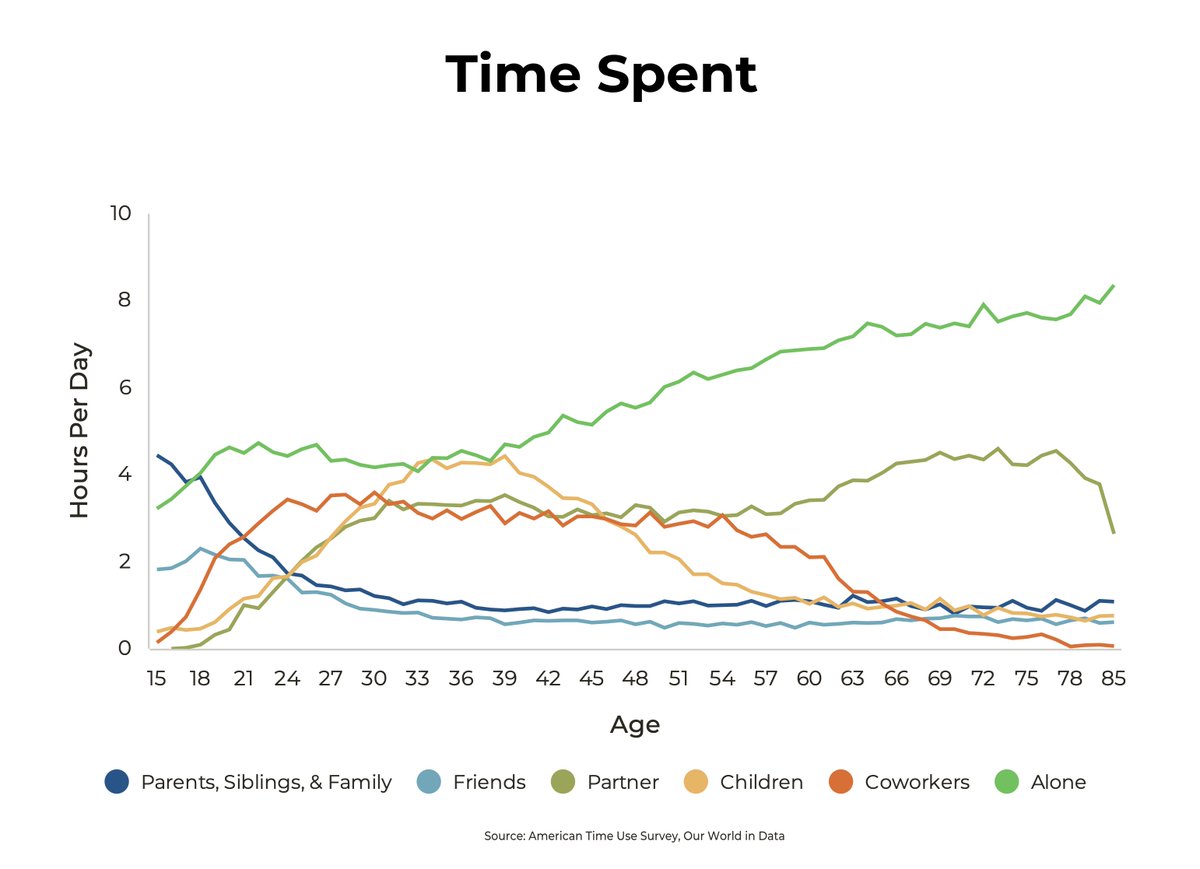

In summary:

(1) Family time is limited—cherish it.

(2) Friend time is limited—prioritize real ones.

(3) Partner time is significant—never settle.

(4) Children time is precious—be present.

(5) Coworker time is significant—find energy.

(6) Alone time is highest—love yourself.

Friends, I need some help

My husband Ryan was just diagnosed with one of the most aggressive types of cancer - a brain cancer called Glioblastoma

I'm looking for contacts at a hospital in japan or at drug maker @DaiichiSankyoUS

Read this and let me know if you can help 👇

So let me get this straight: liquid investment choices are either: (1) hold cash that is facing 10%+ inflation, (2) own stocks that go down 10% every day, (3) own tokens that go down 20%+ every day or (4) hold stablecoins that aren't stable and can be down 40% in a day

Check out this great interview between Kelly Lannan, Senior Vice President of Emerging Investors, and Rishi Vamdatt, Founder of Easy Peasy Finance, on how to get kids more engaged with finances early on. Can you believe Rishi is only 12 years old? https://t.co/GNTMNUYH1r

🎓 Are you a recent or soon-to-be college grad looking for a meaningful career?🚀 If so, launch your career with Fidelity this summer! Fidelity’s University Talent recruiting team will be hosting a career info session... #FidelityAssociate https://t.co/PZQpjz1cAl

Fidelity’s Impact Sustainability group is hosting events to highlight work being done to achieve positive environmental outcomes by our businesses and associates. This #EarthDay 2022, #WhatWillYouDo to #InvestInOurPlanet? #FidelityAssociate https://t.co/VLPbF3LFQZ

To support a diverse workforce, employers should offer inclusive benefits. Hear from Fidelity's Customer Inclusion Leader to learn more. #FidelityAssociate https://t.co/1pDtTdZcf6

Fidelity has entered the #metaverse! With a dance floor, rooftop garden, and interactive quests, the Fidelity experience is a great spot for exploring, lounging, and catching up on educational financial topics. Find us at coordinates... #FidelityAssociate

In one of our recent engagements with a customer, we were asked to audit some code which depended on BokkyPooBah's DateTime library. The contract calculates the day of the month from block.timestamp, and it does this to ensure an operation happens only up to once a month.