JUST IN: Michael Saylor's 'Strategy' currently has a $14,000,000,000 unrealized loss on its Bitcoin investment.

Tom Lee's 'Bitmine' currently has a $10,500,000,000 unrealized loss on its $ETH investment.

One of China’s Best-Known Bitcoin Miners Sees BTC Bear-Market Bottom at $42,000-$44,000 in Late 2026

Jiang Zhuoer, one of China’s best-known Bitcoin miners, predicted that the current BTC bear market may bottom between October and December 2026, with a price range of about $42,000 to $44,000. He said Strategy’s mNAV has fallen to 0.72, close to the 0.7 low seen during the previous bull-to-bear transition in May 2022. Jiang argued that an mNAV bottom does not usually mean BTC bottoms at the same time, noting that BTC hit its final low about six months after MSTR’s mNAV bottom in the last cycle.

Feels like the only thing that hasn’t crashed…

Is memory like $MU, indexes, or large cap semis like Intel so far.

- Photonics from $AXTI to $SIVE down 40%.

- Space from $ASTS and $RKLB down 40% 1M.

- Popular AI names like $PLTR is down ~35% YTD.

- Software like $CRM down -40%.

- Bitcoin sub <60k, Ethereum sub <$16k.

Not a fun time with a hawkish fed narrative and potential rate hikes.

However this does sorta feel overshot due to margin liquidations on less liquid assets compared to mega caps.

But we’ll see what happens, usually fundamentals override liquidity shock in the longer run.

I’m still personally bullish on the AI buildout + upstream AI capex beneficiaries, but 1-2 potential rate hikes certainly don’t help.

Arthur Hayes: Bitcoin's Bottom Is Probably Around $40,000

On June 12, 2026, during an interview with @elliotrades, BitMEX co-founder Arthur Hayes @CryptoHayes shared his prediction for Bitcoin's bottom. When asked about the ultimate bottoming price and timeframe, Hayes admitted that he holds some put spreads, while his long-term positions remain massive and strictly long. He predicted that Bitcoin's bottom will probably be around $40,000 within the next six months.

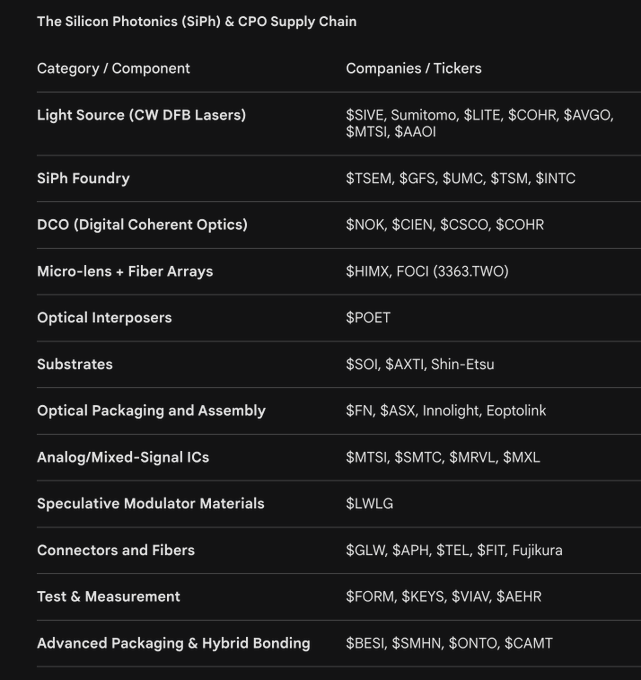

IMO photonics theme + CW laser chokepoint is goated.

It's legit like markets have short term memory loss and forgot how $LITE went from $3B -> $65B+ from 2024 to now.

Because $NVDA caused EML bottlenecks, and forced architectural changes.

We're literally seeing the same thing today with CW lasers + 1.6T/CPO shifts with Nvidia signing LTAs everywhere.

Now, $AMD + other CSPs are hunting for remaining scraps with large LTAs for CW lasers + optical components.

GS Research's ~9-10x $154B optical TAM in 2028 and near $0 -> $91B CPO TAM in just 2 1/2 years.

Don't just magically disappear from a month of trading volatility.

$AAOI sitting at ~$13B, $SIVE sitting at ~$3B, and other CW laser players look strategically very valuable.

And next year I think we'll look back and say "Why didn't I learn my lesson the first time with EML from Nvidia and pick up CW laser adjacent names!"

Then there's likely gonna be some new mini trend 1-2 years from now like microled or quantum dot and we're gonna see the same thing repeat.

Think Sumitomo's projections with CW laser share + silicon photonics being majority / dominant architecture should be correct.

I'm personally just focusing on that bottleneck as you've seen with $SOI, $TSEM, $SIVE, and others.

$LITE rode the first optical wave from $3B to $75B in 2 years time with EML and pluggables.

My thesis is $SIVE can do the same from $3B, with CPO/Pluggables and CW.

Sivers + GFS SiPH reference laser news, alongside the +54% increase today.

Is just one step of the way.

$SIVE is the most compelling CPO/photonics exposure to me.

Addressing the disinformation: I haven’t sold and don’t plan to sell a single share.

I do think this ends up the next $80B+ $LITE one day from ~$2.1B.

And I personally have plans to acquire more ownership + support their M&A prospects.

I believe earnings transcripts will be strongly positive.

As in the part few months we’ve discovered:

> AlChip/Amazon private placements, which is positive for Ayar -> $SIVE implying Trainium 4 design in

> Wiwynn + Ayar CPO scale up

> $JBL 1.6T optical transceiver ramp with Sivers incoming faster than markets expected (with relatively dramatic moat + demand as much as they can produce)

> O-Net scaling up ELS efforts with $SIVE

> $YSS acquisition of $SIVE allspace lead partner, designing Sivers into Space defense primes

> New CHIPS ACT funding for $SIVE

> $POET H2 volume ramp and their new $50m -> $500m order (with $SIVE as light source)

> information discovery around $AAPL using $SIVE lasers for next gen consumer devices

> information discovery around links to Lightelligence (went public $10B+ MC) + Lightmatter as likely customers.

> Celestial volume ramp with $MRVL indicators.

> new customers working on TFLN with $SIVE like Lightium

> $AMD going with $GFS for CPO, and GFS listing sivers as one of two laser suppliers

> Ayar removing $MTSI / $LITE from their website and signaling $SIVE as primary source/sole source

> Ayar raising $500m for volume ramp (intel, Mediatek, Nvidia, amd etc)

> pluggable TAM expansion signaled from 2025 annual report

> Nasdaq listing expected soon

> MSCI small cap index / Nasdaq omx inclusion, making Blackrock, Vanguard and others passive buyers

> M&A signaled from 2025 annual report + 2 new board members that have experience in that area

> $NOK as likely customer from 2025 annual report.

> $LITE getting cw bottlenecked from EML contracts, $SIVE signaling capacity agreements in place with Win, making the a likely bottleneck owner + chokepoint in CPO sector.

All of this market research was done before earnings.

Any results is just confirmation of supply chain mapping done.

I don’t think anyone cares about former quarter revenue since $SIVE is an exceptionally compelling 2027 long, especially H2 onward.

Only thing I’m looking at are:

> TAM expansion of the overall photonics supercycle (eg. optical engine, ELS, pluggables) either from M&A or developments

> volume ramp expectations from existing companies

> Nasdaq listing timelines for more liquidity to support their M&A efforts

> any new customers signaled for CPO/Pluggables

For $SIVE to become the next $80B+ $LITE.

Sivers is the current laser kingmaker of the optical transition to CPO and 1.6T.

They basically supply lasers to the leading players in the CPO space.

From likely $MRVL Celestial, Lightmatter, Lightelligence, $POET, and others for CPO. before they got big.

And now with large players like $JBL for 1.6T LRO + more test/qualifications underway for pluggables.

They've finally solved the Catch22 problem, and have the attention of the market to pull off foundational CPO related IP acquisitions downstream on NASDAQ listing (or now with equity).

And expand revenue as much as possible from the laser source into:

-> Optical Engine/ELS value.

-> Optical Transceiver IP

Just like $LITE did to drive their valuations from $2B -> $80B in 2 years.

But instead of EML + pluggables, Sivers is doing this for the CPO supercycle, the fastest TAM expansion in history for photonics.

I'm following the story for them to pull this off this David vs. Goliath shift catching up to $LITE.

More than I care about little MC % returns that's happening currently.

I don't post dollar amounts because they don't matter.

What matters is return %. Speaking of that...

YTD: 3840.39%.

I'm probably the only one in the world. Who called out multiple names that 10x'd in a short timeframe.

Do you remember these thesis anon?

1. $AXTI

2. $SIVE

3. $AAOI

4. $LITE

5. $IQE

6. $AEHR

7. $CRCL

8. $EWY

9. Unimicron

10. Nitto Boseki

11. $OSS

12. $GDRZF

13. $RPI

14. $SOI

15. $ALRIB

16. $SNDK

17. $SIMO

18. $VPG

19. $TSEM

20. $ARM

21. $MRVL

22. $INTC

23. $LPK

24. $NBIS

25. $MU

They're all up 100-1000%+, because...

1. I post a thesis.

2. People can see how the stock performs months later.

3. They turn out right (thesis validation) because they're up hundreds of percent + hold their returns.

I really dislike the traditional X influencer who shows large dollar amounts or fancy watches/cars/private jets.

Then use that to get more by selling expensive subscriptions rather than through market returns.

So trying to set a new trend off pure information discovery/synthesis from free thesis posts and the results that follow in terms of return percentages.

TLDR: Market returns in terms of percentages matter the most to validate a thesis.

Not the dollar amount made.