Cruising along lifelong learning about business & stocks. MBA MDI Gurgaon FRM. Energy Soldier.Designing Offshore Platforms. More you learn More you earn.

Serendipitous moment when Cobra Leader RS Shekhawat meets dad, grey shark & former CNS Adm VS Shekhawat, & VAdm IC Rao after a 70 yrs course GTG at the same airport where Ranvir started his flying career! ⚓️

A Dabolim R-V fm @IndiGo6E ❤️

All 3 growth levers i.e. revenue growth, margin expansions and valuation multiples are at play in #stallionindia ...turnaround in operating cash flow after WC change and a positive number of 29 cr is icing on the cake and is no more a concern.. on fire

https://t.co/Gp0ZirOgy8

#stallionindia 40% in a week and 100% in a month ...price action is indicating at the good time the business is about to enter...from blender to manufacturer ...journey from micro to small cap and then mid cap has just began...

https://t.co/1dIfADd8Lb

when mangement intention is to grow so fast that today's topline becomes a bottomline 5 years down the line...#multibagger in making #stallionindia management must do walk the talk

https://t.co/lfIKmPzZgH

when mangement intention is to grow so fast that today's topline becomes a bottomline 5 years down the line...#multibagger in making #stallionindia management must do walk the talk

https://t.co/lfIKmPzZgH

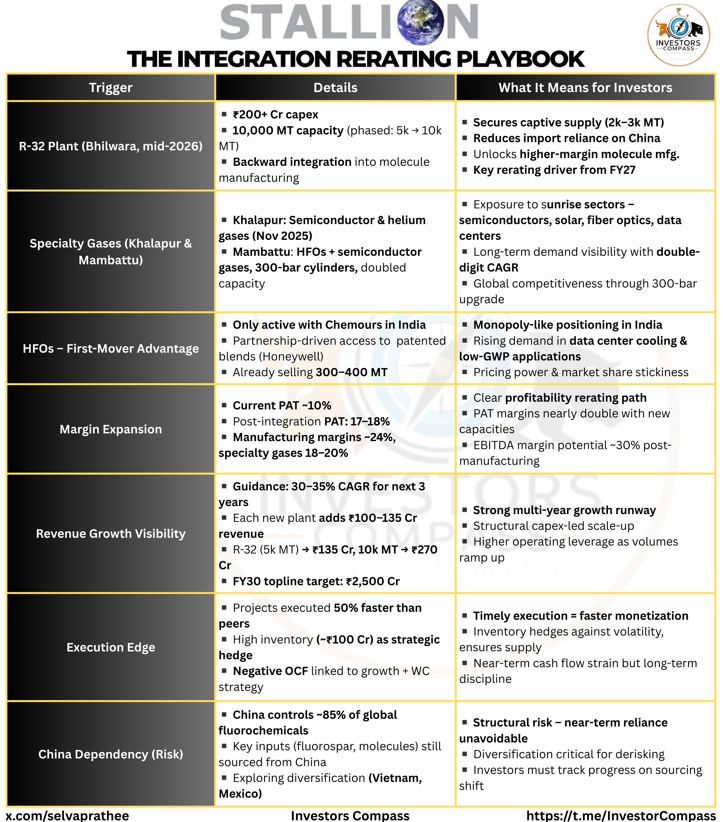

Stallion India Fluorochemicals – Entering its Decade of Rerating | Targets ₹2,500 Cr topline by FY30

- Stallion is not just a packager anymore.

- With integration, specialty gas expansion & faster execution, it’s positioning for a structural rerating.

- Here’s the breakdown

1️⃣ The Transformation

▪️Moving from blending → full molecule manufacturing (R-32 plant, mid-2026).

▪️Expanding into specialty gases – semiconductors, solar, fiber optics, data centers.

▪️Already a first-mover in HFOs (with Honeywell partnership).

2️⃣ Margin Expansion Story

▪️Current PAT margin ~10%.

▪️Post-integration: 17–18% PAT margin.

▪️Manufacturing margins ~24%.

▪️Specialty gases ~18–20%.

➡️ Clear rerating path as profitability almost doubles.

3️⃣ Multi-Year Growth Runway

▪️Guidance: 30-35% CAGR revenue for 3 yrs.

▪️Each new site adds ₹100-135 Cr revenue.

▪️R-32 plant: ₹135 Cr (5k MT) → ₹270 Cr (10k MT).

▪️Ambition: ₹2,500 Cr topline by FY30.

4️⃣ Execution Edge

▪️Projects delivered 50% faster than peers.

▪️₹100 Cr inventory kept as a hedge for supply & pricing cycles.

▪️Negative OCF driven by inventory build strategic, not structural, but cash flow discipline maintained.

5️⃣ Risks to Track

▪️China dependency (85% global fluorochemicals still controlled).

▪️Monsoon-induced delays in project rollout.

▪️Regulatory volatility in fluorochemicals.

6️⃣ Investor Compass View

Triggers

▪️R-32 plant commissioning (mid-2026).

▪️Specialty gases ramp-up (semiconductors, solar, data centers).

▪️PAT margin expansion from 10% → 18%.

Watchpoints

▪️Timely commissioning of Bhilwara, Khalapur, Mambattu.

▪️Speed of capacity ramp-up.

▪️Sustaining cash flow discipline.

➡️ Stallion is entering its decade of rerating, integration + specialty focus + execution edge could structurally reprice the business in FY26-FY30.

No Buy/Sell recommendation

#StocksInFocus #StocksToWatch #stallionsindia #Stallion #SEMICONDUCTOR

Stallion India Fluorochemicals Q1 FY26 Concall Decoded: “Cool Gases, Hot Ambitions” — 1. Opening Hook While the world was busy sweating over US tariffs and a border flare-up with Pakistan, Stallion calmly puffed out 50% YoY revenue growth. That’s… https://t.co/3a3nBqCOI9