Quant Ideas + Fundamental Research + Emotional Discipline + Consistent Effort = Alpha ; something like Walter Schloss, nothing like Bobby Axelrod. PSD Degree.

We will be getting similar reports on Chinese espionage across the west.

Canada, France, Spain, Germany, Australia.

Narrative warfare.

The CIA and NSA are about to go on a generational run

You forget about the infrastructure Kissinger & co built brick by cynical brick that underpins the peaceful life you now live.

Deeply flawed humans. But they were our pitballs. And they left a legacy.

Narrative warfare.

Hegemons dont just walk away and into the sweet summer night.

🫡

The Tariffs Were Struck Down But Yields Spiked. Why?

Today’s ruling by the U.S. Court of International Trade, which struck down the Trump administration’s tariff regime, triggered an immediate and seemingly paradoxical reaction in the bond market. Rather than declining on what should have been a deflationary catalyst removing trade barriers the 10-year Treasury yield surged past 4.50%. The 2-year jumped even more sharply, rising over 1% on the day. To many, this appeared to confirm the idea that tariffs, trade deals, and geopolitical posturing no longer move the needle. But that interpretation misreads the signal. The bond market is not expressing indifference it is issuing a warning.

The removal of tariffs was not seen as a stabilizing event. Instead, it underscored a deeper problem: a breakdown in coordinated economic governance. In principle, eliminating tariffs should reduce input costs, alleviate supply chain friction, and soften inflation expectations. In practice, it revealed that policy direction in Washington has fractured. The fact that a judicial body not Congress or the executive branch was responsible for this reversal only reinforced the sense that no one is driving the macroeconomic ship. Markets took one look and priced in disorder.

The sharp bear steepening of the yield curve reflects this institutional dissonance. The front end of the curve moved most aggressively, suggesting the market is pushing out expectations for rate cuts. That could indicate inflation fears, but given the context waning consumer demand, falling PPI, and deflationary pressures out of China it is far more likely to be a response to perceived fiscal instability. The long end also rose, but more modestly. This is not the curve of a healthy expansion. It’s the curve of a bond market beginning to question the solvency and credibility of its issuer.

What’s changed beneath the surface is the structural capacity to absorb U.S. debt. Net Treasury issuance remains near record highs, the Fed is no longer a buyer through QT, and foreign official institutions are in retreat. Recent auctions have already shown signs of strain soft bid-to-cover ratios, heavy dealer allocations, and waning indirect demand. Striking down tariffs doesn’t fix that it exacerbates it, by removing one of the few remaining artificial caps on goods inflation without providing any corresponding fiscal restraint or monetary accommodation.

Layered on top of this is a fragile financial plumbing system. Deeply negative SOFR swap spreads, elevated basis trades, and deteriorating liquidity conditions in UST futures all suggest that the market is approaching a breaking point. Convexity hedging and duration extensions by large institutional players can easily turn a 10–20 bps move into something reflexive and disorderly. That’s likely part of what we saw today: not just a repricing of policy risk, but the mechanical consequences of a bond market that is increasingly brittle.

There are historical echoes. In 1969, as the Nixon administration veered between protectionism and international coordination, yields surged in anticipation of what became the Nixon Shock. In 2013, Bernanke’s taper announcement rattled markets not because of the action itself, but because it revealed just how dependent the system had become on artificial support. More recently, the UK’s 2022 gilt crisis showed how even the perception of incoherent policy could spiral into a full-blown funding panic.

The U.S. may be entering a similar phase. The striking down of tariffs should have bought breathing room. Instead, it exposed the vacuum of leadership and the fragility of the broader macroeconomic regime. The market’s message is not that tariffs don’t matter it’s that, without a cohesive fiscal, monetary, and trade framework, no individual lever matters anymore. That is not a return to normal it is a systemic red flag.

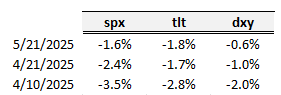

Here are days when the SPX and TLT are both down 1.5% or more on the same day and the dollar is down 50bps or more... (since 2010)

This is VERY much a 2025 risk dynamic. 2022 featured a number of stocks/bonds down...but that was amidst a Fed tightening cycle when the dollar was rising.

What just happened?

At 1:00 PM ET, the S&P 500 fell nearly -80 points in 30 minutes without any major "news."

What actually happened was a weak 20Y Bond Auction which sent US Treasury Yields soaring.

Investors MUST watch yields here. Let us explain.

(a thread)