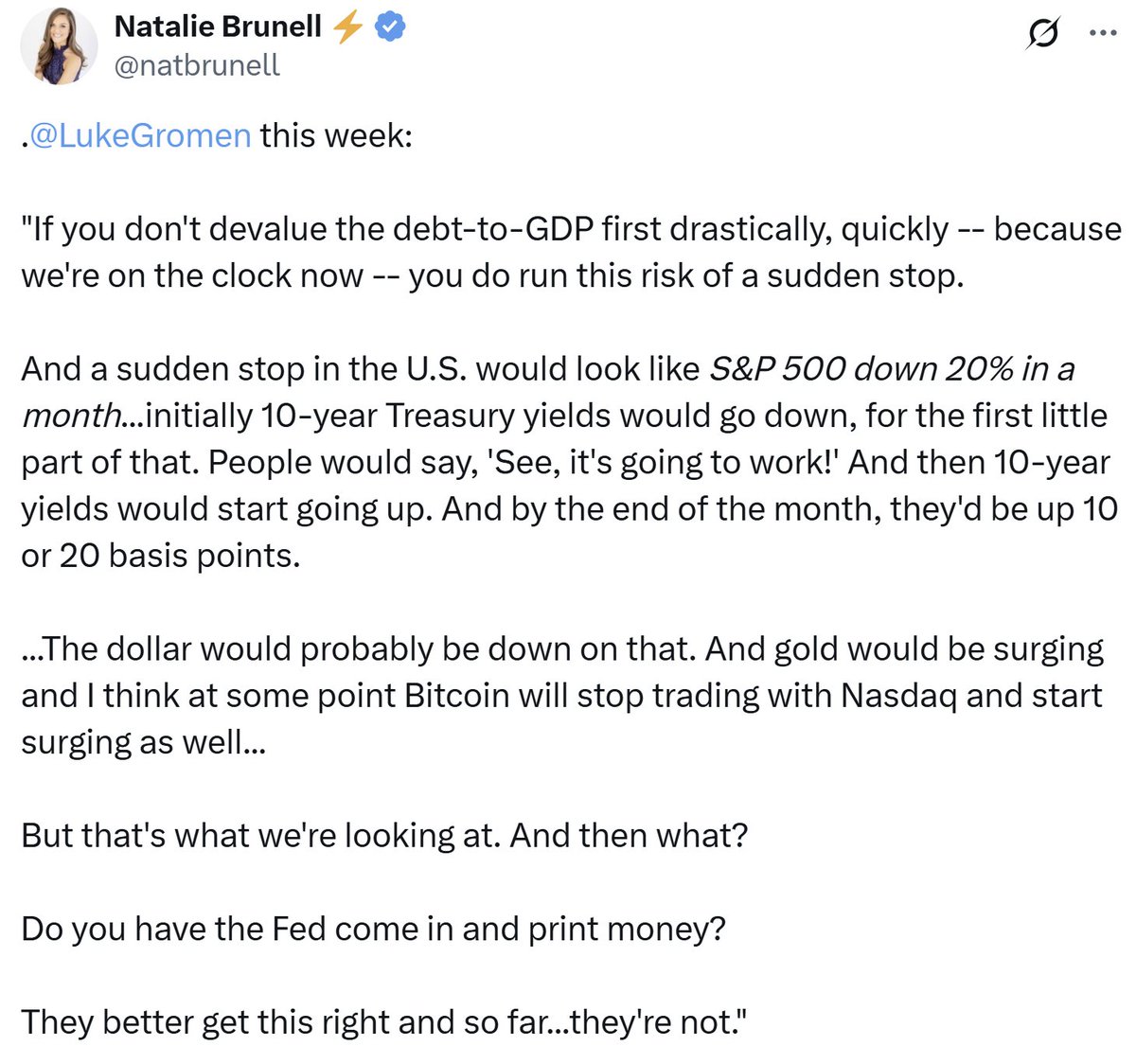

With DXY down, 10y UST yields up, stocks down, gold surging again, wanted to re-highlight this interview with @natbrunell from a week ago Monday (March 31, two days before Trump's tariff announcement), in which we said the following:

These sound like great businesses for long term owners focused on margin and sustainable growth. Feels like the ‘exitable’ part is the issue…but even that, historically, is attractive for an MBO market at the right price, or, maybe some mergers as you say. None of that is bad for the company unless their preference stack and board forces bad decisions. So I think the better question is what happens to the VCs that over invested at inflated valuations when the write downs inevitably occur? Prob a lot fewer funds in 10 years?

Over the course of my career, I've found when smart, sophisticated people say seemingly nonsensical things in their subject of expertise, it is often a signpost of cognitive dissonance between their hard-wired dogma/politics and a shifting reality they see but can't admit yet.

@gaborgurbacs@Jason Expenses meant to impact everyone evenly, revenue not so much (and if taxes covered expenses interest wouldn’t be a line item but different issue) so think it’s fair to say that - ~1tn of spend on anything is ~$3k per person not being spent on that person.

BREAKING: Charles Schwab's trading platforms are down with users unable to log in to their accounts.

Once again, Schwab's platforms have crashed during a period of high volume.

By this logic the relative value to other assets (like gold for example, or USTs, or broad $ money supply) isn’t relative to the price of BTC. Yes random walks exist, but to say no one is doing the *21mm math to sense check buy volume. One of the few assets for which an Enterprise Value isn’t obfuscated by a wonky capital structure.

W

"I will make certain declarations which I am satisfied are useful and are necessary to do justice between the parties. First, that Dr Wright is not the author of the Bitcoin White Paper. Second, Dr Wright is not the person who adopted or operated under the pseudonym Satoshi Nakamoto in the period 2008 to 2011. Third, Dr Wright is not the person who created the Bitcoin System. And, fourth, he is not the author of the initial versions of the Bitcoin software. Any further relief will be dealt with in my written judgment. I will extend time for filing any appellant's notice until 21 days after the form of order hearing, which will be appointed following the hand down of my written judgment and I ask the parties to seek to agree an order giving effect to what I have just stated."

Real estate is a massive component of the collateral that backs issuance of dollars - meaning it is divisible and billionaires do in fact use fractions of their buildings to buy coffee. I think he gets this but is trying to help bridge the (very counterintuitive) knowledge gap for people that have never lived in a world that didn’t separate wealth and money with middle men. Much easier to understand that property, when divisible, transferable, and verifiable, is money than the other way around.

What Constitutes Money Printing?

In 2020, the meme of money printer go brrr took hold of the investment world, spurred by huge amounts of Quantitative Easing occurring from the Fed, leading to M2 Money Supply going higher.

Many viewed this as direct money printing/creation and the memes exploded about how Jerome Powell was printing so much money that the devaluation of the dollar was going to be extreme.

However, the idea of money printing/creation is much more nuanced and complicated than that and some avenues that look like money printing may not actually be that.

With this in mind, let's break down the three avenues where money is most likely created and compare where they differ.

Commercial Banking Loan Growth

The concept of how commercial banks create money through the fractional reserve banking system is central to understanding the modern banking system and its impact on the economy. It is the most “traditional” form of money creation and the most agreed upon as true money creation.

This process is intricate and involves several key steps that allow banks to expand the money supply beyond the initial deposits they receive. Here's how:

First, let’s define this idea. Fractional reserve banking is a banking system in which only a fraction of bank deposits are backed by actual cash on hand and available for withdrawal. This fraction is known as the reserve ratio, and it is set by central banks. The remainder of the bank's deposits not being left as reserves are then used to make loans and create new money.

The process begins when a customer deposits money into a bank. The bank keeps a portion of this deposit in reserves, as required by the reserve ratio, and can use the rest to make loans. For example, if the reserve ratio is 10%, and a customer deposits $1,000, the bank must keep $100 in reserve but can lend out $900. When the bank lends out the $900, it does not physically move money from the depositor's account. Instead, it creates a loan account for the borrower, effectively creating new money. This $900 can then be deposited into another bank or the same bank, forming the basis for further loans. The process of lending, redepositing, and relending, with each step adhering to the reserve ratio, creates a multiplier effect on the money supply. This multiplier effect is represented as the following:

Money Multiplier = 1/ Reserve Ratio

Continuing with our example, with a reserve ratio of 10%, the money multiplier would be 10. This means that, theoretically, the initial $1,000 deposit could lead to up to $10,000 in new money created through the banking system (1,000 initial deposit + 9,000 in subsequent lending).

The amount of loan growth, and therefore money creation, that commercial banks partake in relates to a few factors:

Reserve Requirements: Central banks may adjust reserve requirements to control the money supply.

Capital Requirements: Banks must hold a certain level of capital aside from reserve requirements.

Excess Reserves: Banks may hold reserves above the required minimum to manage risk, especially in uncertain economic times.

Borrower Demand: There must be sufficient demand for loans at interest rates that banks are willing to offer.

Regulatory and Economic Conditions: Government regulations, economic conditions, and central bank policies can all affect banks' ability to create money.

Put simply, the economic conditions must be accommodative enough to both allow banks to be willing to take on loan risk and create these new loans, as well as there to be a strong enough economy that borrowers feel the willingness and ability to take on these new loans at the offered interest rates.

Comparing loan growth activity at commercial banks with NGDP, we see a strong correlation between loan growth and economic strength.

Quantitative Easing

As a refresher from a previous report, this is how QE works:

Since 2008 when interest rates hit zero, the Fed began to engage in Quantitative Easing, commonly referred to as QE.

The Federal Reserve initiates QE by purchasing a substantial amount of financial assets, typically treasury bonds or mortgage-backed securities, from the open market. The Federal Reserve transacts with a group of financial institutions known as primary dealers. These dealers are authorized to trade directly with the Fed in the open market and include major banks and securities firms. The primary dealers act as intermediaries between the Federal Reserve’s NY Trading Desk and the broader financial markets.

As these primary dealers bid to the Fed, it determines the purchase price based on the bids received. The goal is to inject a specific amount of money into the banking system and the accepted bids become the basis for the transaction prices, and the Federal Reserve credits the accounts of the selling institutions with the purchase amount. As the Federal Reserve acquires these assets, it credits the accounts of the selling institutions with newly created reserves, called Central Bank Reserves. This process effectively adds to the banking system's reserves, increasing the overall money supply.

Key to this discussion is understanding that at the foundational level, QE is a swap of assets, not a creation of a new pair of assets. As opposed to commercial bank loan growth where bank reserves are used as collateral to create new loans in a fractional manner, during QE, the Fed simply swaps Treasuries owned by primary dealers for central bank reserves.

What confuses many is that during QE, M2 Money Supply rises - leading to many to assume that QE is printing actual money.

The reason for this is quite simple: The Fed is absorbing assets that do not count in M2, Treasuries, and giving central bank reserves to primary dealers, which are counted within M2. Therefore, simply by changing the composition of primary dealer balance sheets to something that is counted within M2, we see what looks like an increase in actual money.

Moreover, during this swap of assets, the Fed is removing collateral which can be freely used within the entire financial system (Treasuries serve as the bedrock of collateral for the financial system, especially short end bills which are viewed as effectively cash by many), and replacing it with central bank reserves which can only ever be held on commercial bank balance sheets. The commercial banks could use those reserves as collateral to create new loans and therefore print money, but the economic calculus has to make sense. If it does not make sense, which it hasn’t for many periods of time within the last decade, the central bank reserves simply sit on the balance sheet doing nothing.

It is for this reason that many believe that the velocity of M2 has been decreasing so much in recent years:

The money is stuck! So what does QE actually do? In my opinion, a few things:

- It removes duration from markets, allowing for a wealth effect to occur as risk on/animal spirits take hold

- It suppresses yields on the long end of the curve, pushing lower term premia, allowing for private enterprises to fund themselves on cheaper long-end debt, boosting economic activity

- It floods the system with central bank reserves which can be used as collateral only within the core financial system, with the inability to really enter “main street”, allowing for increased financial prices without the secondary effect of higher inflation on “main street” prices. Some call this high street inflation.

What does QE not do? It does not CREATE new monetary assets. It swaps more broad-based collateral with collateral of lower duration and more restricted velocity, allowing for a wealth effect to occur that increases financial assets without pouring into the main street, which could be misconstrued as money printing.

Fiscal Expansion/Deficit Spending

For many years, the Fiscal side of the US monetary system has laid dormant in a form of soft-austerity, spurred by a congress in gridlock making it near impossible for any bill to be passed, paired with political movements such as the Tea Party that have platformed on a notion of fiscal restraint. In 2020, however, this soft-austerity was lifted when COVID struck and congress had to come together to pass major spending bills to bridge the economy through an all-out shutdown.

Ever since then, the political parties in power have been running significant deficits which need to be financed through increased debt/Treasury issuance. Because of both the absolute $ amount of debt being issued and the continuation of major deficits being run even during economic expansions to fund the self-fulfilling increase in interest payment obligations to Treasury holders, much more attention is being paid to the Fiscal side of the financial system. Many call this era we are in Fiscal Dominance.

Increased Treasury issuance and running deficits is argued by some to be indirect money printing. The key to the matter is how the debt issuances are being funded:

When the Federal Reserve is directly purchasing Treasuries from auctions in the primary market as opposed to the secondary market (which it almost never does, and would be considered debt monetization by the Fed), the TGA account at the Treasury would be credited with spendable cash that could be used in the economy. In this case, this would be full-on money printing.

When private domestic buyers such as individuals, hedge funds, pension funds, and commercial banks buy Treasuries, they are swapping domestic assets such as cash for Treasuries, in which case it is only a swap and not outright money printing. That said, the swap is giving the buyer a piece of collateral with a coupon, which could then be utilized in taking on new loans at the same time as getting the coupon payment from the Treasury. In this instance, the combination of the coupon payment + the marginal increase in collateralized loan creation that could occur would provide X amount of new money into the system.

Finally, when it is Foreign Buyers such as foreign governments purchasing US debt at auctions, this is new money entering the domestic system since it is foreign cash being swapped for US debt instruments. In this case, this is outright money creation from a domestic perspective, but not a global perspective.

Overall, when combining these three different types of buyers in aggregate, we see that an increase in deficits and therefore debt issuance leads to more money being created within the system. Following this logic, new fiscal spending being approved by congress leads to new money being created.

Summary

Through exploring these three avenues of money creation, we see that the answer to the question of what constitutes money printing is much more nuanced than what meets the eye. Commercial bank loan creation is the purest form of money printing, followed by Treasury issuance, with traditional QE where the Fed buys from the secondary market and not the primary market being more of a swap than an asset creation.