I valued SpaceX for its IPO a few weeks ago, with minimal information and a promise to revisit the valuation, when the prospectus was made public. The prospectus is public, the offering price has been set and my update is up and running. https://t.co/zRjpD1C0wv

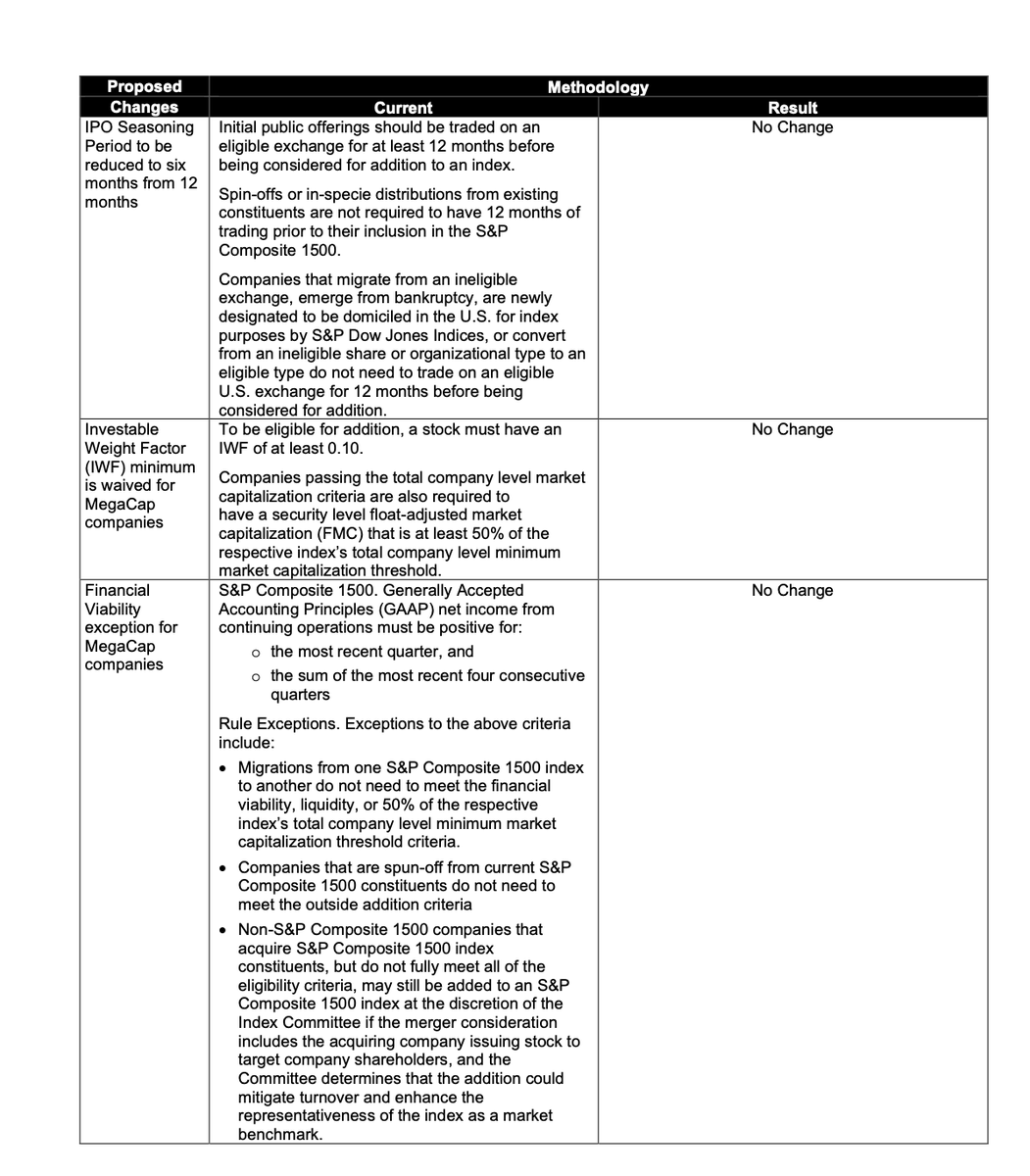

Wow, the S&P Dow Jones Indices has just officially announced that they will NOT be changing their inclusion rules to make it easier for “MegaCap” companies (such as @SpaceX) to be fast-tracked into the S&P 500.

Their reasoning:

"S&P DJI determined that exceptions to the financial viability, seasoning, and IWF requirements should not be granted solely based on market capitalization. The decision not to adopt the proposed exceptions preserves core index principles by maintaining consistent application of these key requirements. Although there may be trade-offs between strict adherence to these eligibility requirements and broad representativeness, the current methodology provides substantial market coverage and sector balance. As a result, the indices can continue to meet their stated objectives while preserving their role as representative and investable benchmarks for the U.S. equity market.

No changes will be made to the eligibility criteria including financial viability screens, seasoning period, or minimum IWF, for the S&P 500, S&P MidCap 400, or S&P SmallCap 600 as a result of the S&P Dow Jones Indices consultation on the treatment of MegaCap companies. Accordingly, there will be no changes to existing methodology for this index family."

This means that the earliest @SpaceX could be eligible to be added to the S&P 500 would now be June 2027.

The requirements that will now remain in place are:

• No changes to S&P 500 eligibility rules for mega-cap companies.

• Mega-cap companies will still need to wait 12 months after their IPO before being considered for S&P 500 inclusion.

• S&P will not waive profitability requirements for mega-cap companies. The company must have positive GAAP net income in the most recent quarter, and the sum of the most recent four consecutive quarters.

• S&P will not waive minimum public float requirements for mega-cap companies. At least 10% of a company's shares must be publicly tradable ("free float").

The S&P rejected proposals that would have:

• Reduced the IPO seasoning period from 12 months to 6 months

• Waived profitability requirements

• Waived minimum public float requirements

As with fat tails Llms are frequency machines that fail to extrapolate outside the sample set. What they know is the VISIBLE.

Almost as bad as economists, almost worse than psychologists.

Hoy presenta resultados $DOCU. Creo que puede ser una lotería, muy bien o muy mal. Tenía 1% de la cartera, con una ganancia de 20% en dólares. Vendí mi posición, ya que no tengo tanta convicción en el papel.

$DOCU Q1 2027 earnings: IAM Migration Drives Cash Generation While Top-Line Growth Remains Stable

Docusign delivered a disciplined Q1 FY27, beating expectations with 9% YoY revenue growth to $830.2 million. The core narrative is firmly centered on the Intelligent Agreement Management (IAM) platform, which now accounts for 12.6% of total ARR—an acceleration from 10.8% last quarter. More importantly, the company is successfully extracting cash from this transition. Free Cash Flow surged 27% YoY to $289.4 million, funding aggressive shareholder returns ($317.5 million in stock repurchases). However, top-line growth has plateaued in the high single digits, and gross margins showed a slight deceleration, signaling that Docusign is currently driving profitability through operational cost controls rather than explosive core product expansion.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐈𝐀𝐌 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐆𝐚𝐢𝐧𝐢𝐧𝐠 𝐌𝐞𝐚𝐧𝐢𝐧𝐠𝐟𝐮𝐥 𝐓𝐫𝐚𝐜𝐭𝐢𝐨𝐧 — IAM adoption is accelerating, representing 12.6% of total ARR (up from 10.8% sequentially), with 40,000 customers now on the platform. The upsell engine is working.

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 & 𝐂𝐚𝐬𝐡 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — Non-GAAP operating margin expanded 250 basis points YoY to 32.0%. Management effectively funneled this operational leverage into Free Cash Flow, which funded a record $317.5M in share buybacks.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐒𝐭𝐮𝐜𝐤 𝐢𝐧 𝐒𝐢𝐧𝐠𝐥𝐞 𝐃𝐢𝐠𝐢𝐭𝐬 — Despite the AI-powered IAM platform launch, total revenue growth remains stable at 9% YoY, and FY27 guidance implies this rate will not materially accelerate in the near term.

• 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 — Non-GAAP gross margin compressed from 82.3% to 81.5% YoY. The impressive operating margin expansion is being achieved entirely through cuts in Sales & Marketing and R&D as a percentage of revenue, not gross profitability.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. While the 'double-digit growth' aspiration remains elusive, the company is executing perfectly on what it can control: aggressively upselling IAM to the installed base, ruthlessly managing operating expenses, and returning massive amounts of cash to shareholders.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐈𝐀𝐌 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐢𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

The migration of the legacy eSignature base to the higher-value Intelligent Agreement Management (IAM) platform is Docusign's primary growth driver. In Q1, IAM penetration reached 12.6% of total ARR (up from 10.8% in Q4 FY26), encompassing 40,000 customers. This demonstrates that the go-to-market overhaul executed last year is bearing fruit and successfully shifting the company from a point solution to an enterprise platform.

🟢 𝐄𝐜𝐨𝐬𝐲𝐬𝐭𝐞𝐦 𝐚𝐧𝐝 𝐅𝐫𝐨𝐧𝐭𝐢𝐞𝐫 𝐀𝐈 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 [NEW]

Management is embedding Docusign into the broader AI ecosystem rather than fighting it. The new 'Iris' AI engine and 'Docusign Agent Studio' allow teams to build custom workflows. Crucially, the introduction of the Model Context Protocol (MCP) server integrates Docusign directly with Anthropic Claude, Google Gemini, and OpenAI ChatGPT. This ensures Docusign remains the 'system of action' regardless of which LLM the enterprise adopts.

⚪ 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬 𝐃𝐫𝐢𝐯𝐞𝐧 𝐛𝐲 𝐂𝐚𝐬𝐡 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲

Free Cash Flow generation remains remarkably robust. Q1 FCF was $289.4M (a 35% margin). Management used this liquidity to execute $317.5M in stock repurchases—a massive acceleration from $183.4M in the prior year period. The share count is steadily shrinking, creating an underlying tailwind for EPS even if top-line growth remains moderate.

🔴 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐢𝐬 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

A concerning divergence appeared in the Q1 income statement: Non-GAAP gross margin fell to 81.5% from 82.3% YoY. The 250 bps expansion in operating margin was achieved entirely by reducing Sales & Marketing (31.8% to 29.8% of revenue) and R&D (13.1% to 12.2% of revenue). Shrinking R&D spend while attempting to win an AI arms race contradicts the narrative of aggressive platform innovation.

🔴 𝐒𝐭𝐨𝐜𝐤-𝐁𝐚𝐬𝐞𝐝 𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐚 𝐇𝐞𝐚𝐯𝐲 𝐀𝐧𝐜𝐡𝐨𝐫

While Non-GAAP metrics look stellar, Stock-Based Compensation (SBC) remains high at $141.3 million for the quarter. Although it decreased slightly from $145.5 million a year ago, it still consumes roughly 17% of total revenue. True GAAP operating margin, inclusive of these costs, is only 13.4%.

⚪ 𝐒𝐡𝐢𝐟𝐭 𝐭𝐨 𝐀𝐑𝐑 𝐌𝐞𝐭𝐫𝐢𝐜 𝐌𝐚𝐬𝐤𝐬 𝐒𝐡𝐨𝐫𝐭-𝐓𝐞𝐫𝐦 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲

As promised in late FY26, Docusign has officially eliminated the 'Billings' metric from its guidance, pivoting to Annual Recurring Revenue (ARR). While this smooths out the severe quarterly volatility caused by early renewals, it also removes a key leading indicator that investors previously used to gauge immediate short-term demand.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 32.0%

Accelerating. Up from 29.5% a year ago. Docusign continues to wring impressive operational efficiencies out of its business, significantly beating its prior full-year targets of ~30%. Management raised the FY27 guidance to 30.5%-31.0%, indicating confidence that these structural cost reductions are permanent.

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: $289.4 million

Accelerating. Up 27% YoY from $227.8M in Q1 FY26. Free Cash Flow margin expanded to 35% of revenue. This exceptional cash conversion is the primary engine funding the company's multi-billion dollar buyback program.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐐𝟐 𝐅𝐘𝟐𝟕 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $865 to $869 million

Stable. The midpoint of $867 million implies an ~8% YoY growth rate. Adjusting for a projected 1.4% FX headwind, underlying constant currency growth remains pinned in the high single digits, failing to break out into the promised double-digit acceleration.

𝐅𝐘𝟐𝟕 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $3.490 to $3.502 billion

Stable. The midpoint ($3.496B) implies roughly 9% growth YoY. Docusign remains a steady compounder, but the numbers suggest the IAM transition is protecting and modestly expanding the base rather than serving as a massive new growth vector.

𝐅𝐘𝟐𝟕 𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 (𝐀𝐑𝐑) 𝐆𝐫𝐨𝐰𝐭𝐡: 8.25% to 8.75%

Stable. Reaffirming the target set at the end of FY26. This metric is now the official compass for Docusign's top-line health. Achieving the high end of this range depends entirely on migrating enterprise customers to the IAM platform.

𝐅𝐘𝟐𝟕 𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 30.5% to 31.0%

Accelerating. Raised from the initial FY27 forecast of 30.0% to 30.5% given in the Q4 call. Docusign is structurally more profitable today than it was 12 months ago.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐯𝐬 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧 𝐃𝐢𝐯𝐞𝐫𝐠𝐞𝐧𝐜𝐞

Non-GAAP gross margins compressed by 80 basis points YoY, yet operating margins hit 32%. Are we reaching the limits of S&M and R&D efficiency, and what is driving the core cost of revenue higher? Is it AI computing costs?

𝐏𝐚𝐜𝐞 𝐨𝐟 𝐭𝐡𝐞 𝐈𝐀𝐌 𝐑𝐨𝐥𝐥𝐨𝐮𝐭

IAM jumped from 10.8% to 12.6% of total ARR in one quarter. What proportion of this was driven by price uplift during renewals versus entirely net-new departmental use cases (like HR and Sales)?

𝐑&𝐃 𝐒𝐩𝐞𝐧𝐝 𝐢𝐧 𝐚𝐧 𝐀𝐈 𝐀𝐫𝐦𝐬 𝐑𝐚𝐜𝐞

Non-GAAP R&D fell to 12.2% of revenue from 13.1% YoY. How is Docusign funding the 'fastest pace of innovation in history' while simultaneously cutting R&D margins?

For Aristotle, the banausos is not just physically deformed by his profession, but politically and ethically stunted: specialization makes him less a complete man than a TOOL of his occupation.

Politics, book VII:

"And any occupation, art, or science, which makes the body or soul or mind of the freeman less fit for the practice or exercise of virtue, is vulgar; wherefore we call those arts vulgar which tend to DEFORM the body, and likewise all paid employments, for they absorb and degrade the mind."

Me cuesta entender a los que siguen pagando Marvell, $MRVL a estos precios. Es sorprendente además la influencia que tiene Huang, CEO de $NVDA, sobre las cotizaciones en este momento.

@DiegoLemansky Yo pienso lo mismo. Está quemando dinero tratando de hacer daño. Si realmente quisiera salir de la mejor forma posible, este es el peor camino.

Many obsessed only with the model. The models are the foundation, but real impact in business comes from deployment.

Deployment means knowing the technology ecosystem and maturing new solutions through real, iterative work. AI accelerates that loop — but the final understanding and adaptation to reality need human intervention. A person still provides the intention.

This is exactly what we have been seeing on the ground. Humans plus AI is the winning formula.

@Juancamolinari "Está bajando" asume cierto conocimiento del futuro. Es extrapolar el pasado. Lo que "está bajando" puede dejar de hacerlo, nadie sabe cuándo.

Yo no miro en términos de si están bajando o subiendo, sino en términos de si están subvaluados o no, y con qué margen de seguridad.

I have a great idea. I am going to spend a trillion dollars so I can make $10 billion a year in profit, if all goes well.

That’s a 1% annual return – IF it works out.

Who’s in?

Don’t worry about the risk that it might not work out!

![Finsee_main's tweet photo. $DOCU Q1 2027 earnings: IAM Migration Drives Cash Generation While Top-Line Growth Remains Stable

Docusign delivered a disciplined Q1 FY27, beating expectations with 9% YoY revenue growth to $830.2 million. The core narrative is firmly centered on the Intelligent Agreement Management (IAM) platform, which now accounts for 12.6% of total ARR—an acceleration from 10.8% last quarter. More importantly, the company is successfully extracting cash from this transition. Free Cash Flow surged 27% YoY to $289.4 million, funding aggressive shareholder returns ($317.5 million in stock repurchases). However, top-line growth has plateaued in the high single digits, and gross margins showed a slight deceleration, signaling that Docusign is currently driving profitability through operational cost controls rather than explosive core product expansion.

Full article with charts - link in bio

🐂 𝐁𝐮𝐥𝐥 𝐂𝐚𝐬𝐞

• 𝐈𝐀𝐌 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐆𝐚𝐢𝐧𝐢𝐧𝐠 𝐌𝐞𝐚𝐧𝐢𝐧𝐠𝐟𝐮𝐥 𝐓𝐫𝐚𝐜𝐭𝐢𝐨𝐧 — IAM adoption is accelerating, representing 12.6% of total ARR (up from 10.8% sequentially), with 40,000 customers now on the platform. The upsell engine is working.

• 𝐌𝐚𝐫𝐠𝐢𝐧 𝐄𝐱𝐩𝐚𝐧𝐬𝐢𝐨𝐧 & 𝐂𝐚𝐬𝐡 𝐆𝐞𝐧𝐞𝐫𝐚𝐭𝐢𝐨𝐧 — Non-GAAP operating margin expanded 250 basis points YoY to 32.0%. Management effectively funneled this operational leverage into Free Cash Flow, which funded a record $317.5M in share buybacks.

🐻 𝐁𝐞𝐚𝐫 𝐂𝐚𝐬𝐞

• 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 𝐆𝐫𝐨𝐰𝐭𝐡 𝐒𝐭𝐮𝐜𝐤 𝐢𝐧 𝐒𝐢𝐧𝐠𝐥𝐞 𝐃𝐢𝐠𝐢𝐭𝐬 — Despite the AI-powered IAM platform launch, total revenue growth remains stable at 9% YoY, and FY27 guidance implies this rate will not materially accelerate in the near term.

• 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐂𝐨𝐦𝐩𝐫𝐞𝐬𝐬𝐢𝐨𝐧 — Non-GAAP gross margin compressed from 82.3% to 81.5% YoY. The impressive operating margin expansion is being achieved entirely through cuts in Sales & Marketing and R&D as a percentage of revenue, not gross profitability.

⚖️ 𝐕𝐞𝐫𝐝𝐢𝐜𝐭: 🟢

Bullish. While the 'double-digit growth' aspiration remains elusive, the company is executing perfectly on what it can control: aggressively upselling IAM to the installed base, ruthlessly managing operating expenses, and returning massive amounts of cash to shareholders.

𝐊𝐞𝐲 𝐓𝐡𝐞𝐦𝐞𝐬

🟢 𝐈𝐀𝐌 𝐏𝐥𝐚𝐭𝐟𝐨𝐫𝐦 𝐀𝐝𝐨𝐩𝐭𝐢𝐨𝐧 𝐢𝐬 𝐀𝐜𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

The migration of the legacy eSignature base to the higher-value Intelligent Agreement Management (IAM) platform is Docusign's primary growth driver. In Q1, IAM penetration reached 12.6% of total ARR (up from 10.8% in Q4 FY26), encompassing 40,000 customers. This demonstrates that the go-to-market overhaul executed last year is bearing fruit and successfully shifting the company from a point solution to an enterprise platform.

🟢 𝐄𝐜𝐨𝐬𝐲𝐬𝐭𝐞𝐦 𝐚𝐧𝐝 𝐅𝐫𝐨𝐧𝐭𝐢𝐞𝐫 𝐀𝐈 𝐈𝐧𝐭𝐞𝐠𝐫𝐚𝐭𝐢𝐨𝐧 [NEW]

Management is embedding Docusign into the broader AI ecosystem rather than fighting it. The new 'Iris' AI engine and 'Docusign Agent Studio' allow teams to build custom workflows. Crucially, the introduction of the Model Context Protocol (MCP) server integrates Docusign directly with Anthropic Claude, Google Gemini, and OpenAI ChatGPT. This ensures Docusign remains the 'system of action' regardless of which LLM the enterprise adopts.

⚪ 𝐀𝐠𝐠𝐫𝐞𝐬𝐬𝐢𝐯𝐞 𝐂𝐚𝐩𝐢𝐭𝐚𝐥 𝐑𝐞𝐭𝐮𝐫𝐧𝐬 𝐃𝐫𝐢𝐯𝐞𝐧 𝐛𝐲 𝐂𝐚𝐬𝐡 𝐄𝐟𝐟𝐢𝐜𝐢𝐞𝐧𝐜𝐲

Free Cash Flow generation remains remarkably robust. Q1 FCF was $289.4M (a 35% margin). Management used this liquidity to execute $317.5M in stock repurchases—a massive acceleration from $183.4M in the prior year period. The share count is steadily shrinking, creating an underlying tailwind for EPS even if top-line growth remains moderate.

🔴 𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐢𝐬 𝐃𝐞𝐜𝐞𝐥𝐞𝐫𝐚𝐭𝐢𝐧𝐠 [NEW]

A concerning divergence appeared in the Q1 income statement: Non-GAAP gross margin fell to 81.5% from 82.3% YoY. The 250 bps expansion in operating margin was achieved entirely by reducing Sales & Marketing (31.8% to 29.8% of revenue) and R&D (13.1% to 12.2% of revenue). Shrinking R&D spend while attempting to win an AI arms race contradicts the narrative of aggressive platform innovation.

🔴 𝐒𝐭𝐨𝐜𝐤-𝐁𝐚𝐬𝐞𝐝 𝐂𝐨𝐦𝐩𝐞𝐧𝐬𝐚𝐭𝐢𝐨𝐧 𝐑𝐞𝐦𝐚𝐢𝐧𝐬 𝐚 𝐇𝐞𝐚𝐯𝐲 𝐀𝐧𝐜𝐡𝐨𝐫

While Non-GAAP metrics look stellar, Stock-Based Compensation (SBC) remains high at $141.3 million for the quarter. Although it decreased slightly from $145.5 million a year ago, it still consumes roughly 17% of total revenue. True GAAP operating margin, inclusive of these costs, is only 13.4%.

⚪ 𝐒𝐡𝐢𝐟𝐭 𝐭𝐨 𝐀𝐑𝐑 𝐌𝐞𝐭𝐫𝐢𝐜 𝐌𝐚𝐬𝐤𝐬 𝐒𝐡𝐨𝐫𝐭-𝐓𝐞𝐫𝐦 𝐕𝐨𝐥𝐚𝐭𝐢𝐥𝐢𝐭𝐲

As promised in late FY26, Docusign has officially eliminated the 'Billings' metric from its guidance, pivoting to Annual Recurring Revenue (ARR). While this smooths out the severe quarterly volatility caused by early renewals, it also removes a key leading indicator that investors previously used to gauge immediate short-term demand.

𝐎𝐭𝐡𝐞𝐫 𝐊𝐏𝐈𝐬

𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 32.0%

Accelerating. Up from 29.5% a year ago. Docusign continues to wring impressive operational efficiencies out of its business, significantly beating its prior full-year targets of ~30%. Management raised the FY27 guidance to 30.5%-31.0%, indicating confidence that these structural cost reductions are permanent.

𝐅𝐫𝐞𝐞 𝐂𝐚𝐬𝐡 𝐅𝐥𝐨𝐰: $289.4 million

Accelerating. Up 27% YoY from $227.8M in Q1 FY26. Free Cash Flow margin expanded to 35% of revenue. This exceptional cash conversion is the primary engine funding the company's multi-billion dollar buyback program.

𝐆𝐮𝐢𝐝𝐚𝐧𝐜𝐞

𝐐𝟐 𝐅𝐘𝟐𝟕 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $865 to $869 million

Stable. The midpoint of $867 million implies an ~8% YoY growth rate. Adjusting for a projected 1.4% FX headwind, underlying constant currency growth remains pinned in the high single digits, failing to break out into the promised double-digit acceleration.

𝐅𝐘𝟐𝟕 𝐓𝐨𝐭𝐚𝐥 𝐑𝐞𝐯𝐞𝐧𝐮𝐞: $3.490 to $3.502 billion

Stable. The midpoint ($3.496B) implies roughly 9% growth YoY. Docusign remains a steady compounder, but the numbers suggest the IAM transition is protecting and modestly expanding the base rather than serving as a massive new growth vector.

𝐅𝐘𝟐𝟕 𝐀𝐧𝐧𝐮𝐚𝐥 𝐑𝐞𝐜𝐮𝐫𝐫𝐢𝐧𝐠 𝐑𝐞𝐯𝐞𝐧𝐮𝐞 (𝐀𝐑𝐑) 𝐆𝐫𝐨𝐰𝐭𝐡: 8.25% to 8.75%

Stable. Reaffirming the target set at the end of FY26. This metric is now the official compass for Docusign's top-line health. Achieving the high end of this range depends entirely on migrating enterprise customers to the IAM platform.

𝐅𝐘𝟐𝟕 𝐍𝐨𝐧-𝐆𝐀𝐀𝐏 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧: 30.5% to 31.0%

Accelerating. Raised from the initial FY27 forecast of 30.0% to 30.5% given in the Q4 call. Docusign is structurally more profitable today than it was 12 months ago.

𝐊𝐞𝐲 𝐐𝐮𝐞𝐬𝐭𝐢𝐨𝐧𝐬

𝐆𝐫𝐨𝐬𝐬 𝐌𝐚𝐫𝐠𝐢𝐧 𝐯𝐬 𝐎𝐩𝐞𝐫𝐚𝐭𝐢𝐧𝐠 𝐌𝐚𝐫𝐠𝐢𝐧 𝐃𝐢𝐯𝐞𝐫𝐠𝐞𝐧𝐜𝐞

Non-GAAP gross margins compressed by 80 basis points YoY, yet operating margins hit 32%. Are we reaching the limits of S&M and R&D efficiency, and what is driving the core cost of revenue higher? Is it AI computing costs?

𝐏𝐚𝐜𝐞 𝐨𝐟 𝐭𝐡𝐞 𝐈𝐀𝐌 𝐑𝐨𝐥𝐥𝐨𝐮𝐭

IAM jumped from 10.8% to 12.6% of total ARR in one quarter. What proportion of this was driven by price uplift during renewals versus entirely net-new departmental use cases (like HR and Sales)?

𝐑&𝐃 𝐒𝐩𝐞𝐧𝐝 𝐢𝐧 𝐚𝐧 𝐀𝐈 𝐀𝐫𝐦𝐬 𝐑𝐚𝐜𝐞

Non-GAAP R&D fell to 12.2% of revenue from 13.1% YoY. How is Docusign funding the 'fastest pace of innovation in history' while simultaneously cutting R&D margins?](https://pbs.twimg.com/media/HJ_uI6WWoAACr_b.png)