And what percentage of that Bitcoin has been used to pay off dividends? Maybe 0.01% from the 32 Bitcoin he sold which massively tanked the market. If he funds 99.99% of obligations to existing investors by issuing new shares to sell to new investors, that’s ponzi-adjacent. How hard is that to understand?

When his dividend obligations have doubled YTD (to 1.7 billion a year or 7 million a trading day), cash reserve coverage has gone down 4x (to 6 months now), STRC is trading well under par, and the company had zero cash flow to begin with - you know that selling more bitcoin to cover obligations will start to become very necessary in the future.

The “hate” is due to the fact that he’s straight up building a ponzi on Bitcoin where he’s promising 11.5% returns, and paying off dividends by issuing new shares to sell to new investors. He’s scammed investors on 99% of their money before and it’s about to happen again with billions of dollars about to be lost.

• Cash reserves shrinking 4x, 2 years -> 6 months

• Dividend obligations growing 2x

• Bitcoin losses compounding (6 billion now)

• $STRC trading well under par for 2 weeks.

• Business has no cash flow

• Bitcoin being sold to pay out obligations.

Somehow the bulls are still claiming that Saylor’s decision to use the cash reserves and sell Bitcoin is still a “choice”.

So many people still blindly bullish. If Bitcoin drops this much on a tiny sell from MSTR, imagine what happens when they need to sell their entire stack. They owe $6.7 billion in debt and $1.7 billion (and quickly increasing) in annual dividend obligations. $STRC is well below par and cash reserves have dwindled from 2 years coverage to under 6 months. They are $6 billion underwater on their Bitcoin investment. It’s only a matter of time before they’re liquidated. Once that poison is gone, Bitcoin will be able to recover again.

Let’s play a game. Guess the company which is:

• Down $6 billion on its investments.

• Owes $6.7 billion in debt

• Owes an additional $1.7 billion to shareholders every year

• Cash has gone down from lasting 2 years to 6 months.

• Has zero cash flow and relies on issuing new shares to get cash.

• Led by a man who has already once crashed his company 99% and lost shareholders all their money.

Not only is he down 4 billion, he also owes 6.7 billion in debt, 1.7 billion (and growing) in annual dividend obligations, a cash reserve which dwindled from 2 years coverage to 6 months, and now starting to sell Bitcoin to pay off dividend obligations. All this while having zero cash flow whatsoever.

@MajorianBTC Things are going to get ugly. He has $1.7 Billion in annual dividend obligations, and that's doubled from 6 months ago. $128 million in dilution in a single week wasn't enough to cover the obligations last week, and it'll only get worse from here.

He’s just trying to prime the market to be ready for his bigger sells. His dividend obligations have doubled in the last 6 months and last week, even diluting the common by $128 million couldn't cover them - it will be necessary at some point to sell Bitcoin to pay off his ever-increasing obligations.

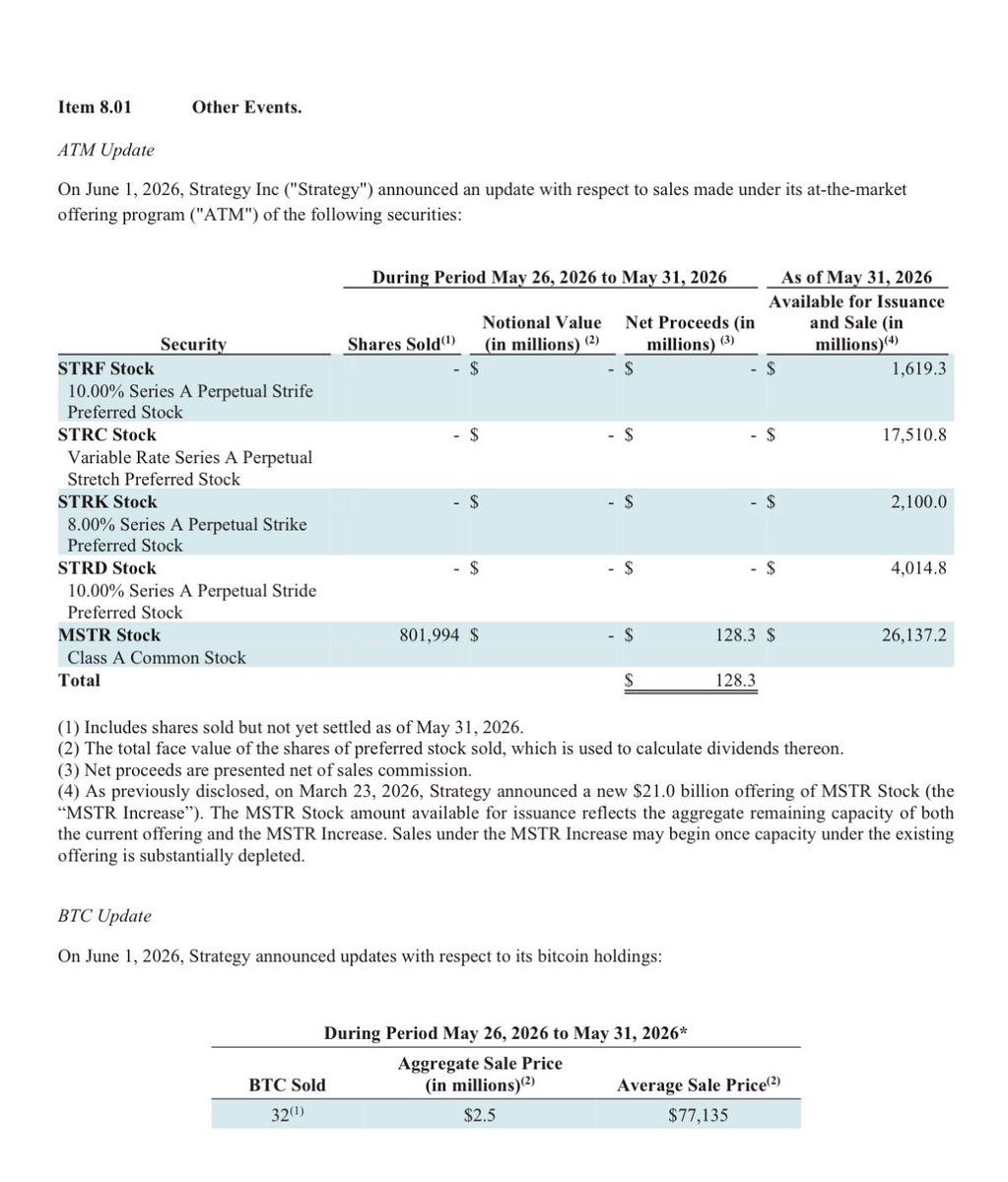

⚠️🚨 Mornin’, it’s that time again! and we got a very special 8K today!

In addition to selling 32 Million $BTC, Saylor diluted $MSTR common share holders another $128M to fund dividends on $STRC & the other Ponzi Preferreds.

Notably, he did not use his $900M cash reserve.

His “Strategy” is now to sell common & preferred shares to buy Bitcoin in order to sell the Bitcoin + more shares to fund the ever increasing dividend obligations on the preferreds…+ buy back debt, used to buy earlier Bitcoin. He claims this is the greatest credit invention of the 21st century.

Bitcoin would have been much better off without Saylor and his billions in buying pressure. It would not have shot up to 120k so quickly, but it also wouldn't have fallen to 70k right after. Nobody wants to be in an asset backed by a man owing Billions (and quickly increasing) in debt and dividend obligations with no way to pay it off besides issuing new shares to sell to new investors.

If by "comes with", you're using a newly sold share of $strc to pay for existing dividends, then yes, one new share can cover 9 years of dividends for an existing share.

$strc itself being sold doesn't "come with" any coverage, it just comes with a 11.5% interest tag indefinitely which Saylor has to pay.

MSTR's dividend obligations doubled in just the last 6 months, and he still couldn’t cover them after diluting the common stock by $128 million in a single week. The dividend obligations have only ever gone up and will only continue to do so. Saylor's just priming the market so that it's ready when he needs larger sells to cover his increasing dividend obligations.

MSTR's dividend obligations doubled in just the last 6 months, and he still couldn’t cover them after diluting the common stock by $128 million in a single week. The dividend obligations have only ever gone up and will only continue to do so. Saylor's just priming the market so that it's ready when he needs larger sells to cover his increasing dividend obligations.

@TheFlowHorse His dividend obligations have doubled in just the last 6 months. Soon, selling Bitcoin to cover the quickly increasing obligations will be necessary.

@3orovik Maybe it’s not the buying and selling, but rather the fact that a single entity with no cash flow holds 5% of the supply while simultaneously holding Billions (and growing) in debt and dividend obligations. And this fact is not good for Bitcoin.

@PiusSprenger His dividend obligations have doubled in the last 6 months. It will be necessary at some point to sell Bitcoin to pay off his ever-increasing obligations so he’s trying to prime the market to be ready for his bigger sells.