Christian, Husband, Father. Love working with technology and helping teams accomplish more than they thought was possible. Browns / Cavs / Indians fan!

Jeff Bezos asked a room to imagine going back a hundred years.

When almost everyone was a farmer.

And telling those farmers that in 2018 there’d be a job called “massage therapist.”

Bezos: “They would not have believed you.”

Then a friend took it further.

Bezos: “Forget massage therapist, there are dog psychiatrists.”

He looked it up.

Bezos: “Sure enough, you can easily hire a psychiatrist for your dog.”

The room laughed.

The point under the laughter wasn’t funny at all.

Every time a major technology shift hits, we do the exact same thing.

We count the jobs it will destroy.

We never count the ones it will create.

Because we can’t.

They don’t have names yet.

The fear is always specific.

AI will replace accountants. AI will replace radiologists. AI will replace drivers.

The fear has job titles and timelines and projections.

The opportunity has none of those things.

Because you can’t name what doesn’t exist yet.

A farmer in 1920 could understand losing his job to a tractor.

He could not understand gaining a career as a social media strategist.

Not because he lacked intelligence.

Because the entire chain of inventions between his world and that job hadn’t been built yet.

Radio. Television. The internet. Smartphones. Social platforms. Creator economies.

Every single link in that chain had to exist before “social media strategist” could even be a sentence.

That’s where we are with AI right now.

Everyone is staring at the tractor.

Nobody can see the thing seven inventions away that doesn’t have a name yet.

The fear is loud because it fits inside language we already have.

The opportunity is silent because it doesn’t.

Every technological revolution in history created more jobs than it destroyed.

Every single one.

Not because anyone planned it.

Because human needs expand faster than machines can fill them.

We didn’t need massage therapists when we were breaking our backs on farms.

We needed them after machines freed our backs and stress replaced labor.

The demand didn’t disappear.

It migrated somewhere no one was looking.

That is exactly what’s happening right now.

The jobs AI creates won’t make sense to us yet.

They’ll sound as absurd as “dog psychiatrist” would’ve sounded to a farmer in 1920.

Until someone is running a $200 hourly practice with a six-month waitlist.

The entire conversation right now is about what we’re about to lose.

Nobody is talking about what we’re about to gain.

Because the gains don’t have vocabulary yet.

A hundred years from now, someone will stand on a stage and describe the jobs we couldn’t imagine today.

And the audience will laugh.

The same way we just did.

First Wave Fund (@JonahLupton) 13F shows they were extremely active in Q1. Big increases in $APP, $CRDO, $RDDT, $TMDX, $MELI, $HROW, $NU and $HIMS. Big trims of $ONON, $PRCT, $ONDS, $LITE, $CLPT, $CELH. New positions in $AAOI, $MU, $SOFI, $HOOD. Sold out of a large number of names completely (incl. $FOUR, $CIFR, $OSCR, $ZETA and a lot of others). Seems like they used Q1 to concentrate capital into high conviction names and position for the AI bottleneck trade.

Don't trust TurboTax. I passed the TurboTax Federal review with flying colors but before submitting I had Grok review the PDF and it found that TurboTax had incorrectly imported the data from my Brokerage firm. Grok was right. TurboTax was wrong. Grok saved me a lot of money. @elonmusk

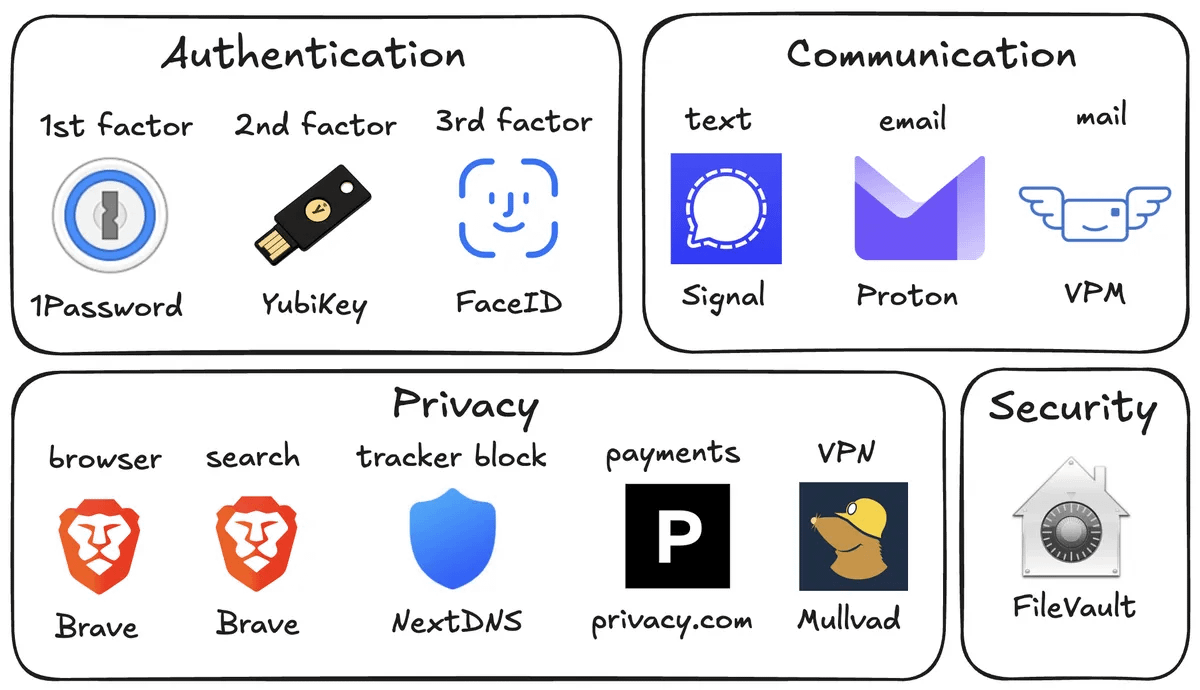

Claude Mythos is like Hiroshima for software.

everything you own online, your bank, your email, your photos, your identity, is now dangerously exposed in ways that didn't exist 48 hours ago

that's why Karpathy's digital hygiene guide is probably the most important thing you can read this week

here's every step to protect yourself in these uncharted times:

> use a password manager for every account

> set up physical security keys so attackers can't log in

> enable face id and fingerprint everywhere

> randomize your security question answers

> encrypt your hard drive

> get rid of unnecessary smart home devices

> switch to signal for private messaging

> use brave instead of chrome

> switch to brave search instead of google

> mint virtual credit cards for every purchase

> get a virtual mailing address

> never click links inside emails

> use a vpn on public wifi

> block ads and trackers at the dns level

> install a network monitor to see which apps are spying on you

full breakdown of each step below:

THE BUSINESS: TransMedics is more than a medical device company ; it's a platform. Their Organ Care System (OCS) keeps donor hearts, lungs, and livers warm and beating during transport, replacing decades-old cold storage that destroys marginal organs. As of 2025, OCS is the only system with regulatory clearance for all three major organs in the U.S., a position not matched by any competitor. But here's what makes TMDX truly untouchable: their National OCS Program integrates clinical services, logistics, and a dedicated aviation fleet — a turnkey, end-to-end organ procurement solution. Rivals like OrganOx and XVIVO are device-only, single-organ players. They don't have the logistics infrastructure and their organ care solution is clinically proven to not be as good at the TMDX solution.

FUNDAMENTALS ARE PRISTINE: TMDX delivered 2025 revenue of $605.5M, up 37% YoY, with net income of $190.3M and 60% gross margins. They've guided 2026 to $727–$757M in revenue, implying 20–25% growth. Every single quarter in 2025 saw guidance raised. Analysts have an average Buy rating with a 12-month price target of $154 — implying 65%+ upside from current levels. This is a company that went from $441M → $605M in one year while becoming solidly profitable.

EXECUTION HAS BEEN ELITE: As of late 2025, TMDX owned 22 aircraft; a proprietary flight network competitors literally cannot replicate overnight. They completed 3,715 U.S. OCS cases in 2024, a 58% increase vs. the prior year. Early 2026 transplant activity has analysts calling for upside to consensus. They even announced a strategic collaboration with Mercedes-Benz to deploy a dedicated organ transport vehicle fleet across Italy; international expansion is just getting started.

WHY THE DROP IS UNWARRANTED: The stock is currently near ~$100, vs. a 52-week high of $156. The recent weakness is macro-driven — broad market tariff fears and risk-off sentiment — NOT company-specific deterioration. TMDX's revenue is domestic, procedure-driven, and medically necessary. Wars and Tariffs don't stop heart transplants. The fundamentals have never been stronger, yet the stock trades at a P/E of ~20x on a business growing 25%+ with expanding margins.

TECHNICALS ARE HOLDING: The $124 zone was flagged as a key prior support level, and the stock has now consolidated further near the $100 level — which represents a critical long-term demand zone. Volume on down days is macro-fear selling, not institutional distribution. The setup here is a classic "fundamentals stay strong, price gets macro'd down".

BOTTOM LINE: $TMDX is the only vertically integrated organ transplant platform on earth. Growing 25%+ with 60% gross margins, profitable, raising guidance, expanding internationally, and trading at a near multi-year low on fears that have nothing to do with their business. Every 1% increase in U.S. organ utilization = $10M+ in incremental revenue. Global lung utilization sits at 20%, hearts at 30%, livers at 65% — the TAM expansion runway is enormous.

@JoshTradeOption I highly recommend Josh's service. I subscribed to Josh's X community 5 weeks ago and I've made $5,513 in profit so far and I have learned a ton.

NVIDIA CEO Jensen Huang just said the quiet part out loud about what the education system will never admit.

For a century, we built humans to think like calculators.

The algorithm made that skillset obsolete overnight.

Huang: “The definition of smart is somebody who’s intelligent, solve problems, technical. But I find that that’s a commodity. And we’re about to prove that artificial intelligence is able to handle that part easiest.”

Software engineering was supposed to be the safe play.

Superintelligence cleared it first.

The SAT was supposed to measure intelligence. It was measuring the ability to follow instructions. Raw technical processing isn’t a competitive edge anymore. It’s the floor the machine stepped over before you woke up.

The question isn’t what you can calculate.

It’s what you can see before the data shows up.

Huang: “People who are able to see around corners are truly, truly smart. And their value is incredible. To be able to preempt problems before they show up, just because you feel the vibe.”

That vibe isn’t magic.

It’s the collision of first principles, human empathy, and lived experience no model can fake.

Huang: “That vibe came from a combination of data, analysis, first principle, life experience, wisdom, sensing other people.”

The operators who see around corners will command the AI.

The ones waiting for dashboards to update will be replaced by it.

Huang: “I think long term the definition of smart is someone who sits at that intersection of being technically astute, but human empathy and having the ability to infer the unspoken, around the corners, the unknowables.”

The unspoken variables are the new leverage.

The human psychology inside a market. The invisible friction in a negotiation. The instinct to build something nobody asked for yet.

You can’t spreadsheet your way there. You can’t prompt your way to that perception. It comes from decades of watching what doesn’t show up in the metrics.

Huang: “And that person might actually score horribly on the SAT.”

The future doesn’t belong to people who memorized answers.

It belongs to people who sense the questions before anyone thinks to ask.

The old system tested your ability to follow orders. The new one tests your ability to move through the unknown. And the machine can’t help you with that part.

That part is entirely on you.

NVDA Apr 17 $165 Put: NVDA remains the highest-conviction AI/semiconductor leader with strong long-term demand tailwinds and elevated IV offering the best premium-to-risk ratio for wheel scaling.

RTX Apr 17 $200 Put: RTX is benefiting from immediate geopolitical defense spending momentum, providing stable premium and dividend support with lower assignment risk in a risk-off environment.

EQT Apr 17 $38 Put: EQT offers direct exposure to surging natural gas prices driven by AI data center power needs, with attractive undervaluation and dividend yield for diversified wheel income.

PLTR Mar 20 $140 Put: PLTR combines high AI/government contract growth with currently elevated IV, delivering strong premium in a shorter DTE for faster capital turnover.

AAPL Apr 17 $250 Put: AAPL provides blue-chip stability, consistent ecosystem growth, and reliable dividends, making it the safest wheel anchor with dependable (though lower) premium.

WMB Apr 17 $45 Put: WMB serves as a low-beta natural gas infrastructure hedge with high dividend yield and reasonable premium, adding essential diversification to your tech-heavy portfolio.