He hecho la cuenta de la vieja cargando 26 kWh que da aproximadamente para 190 km.

Eléctrico:

Placas solares: 0€

Mercadona (0.25€/kWh): 6.50€

Gasolina (5.4l/100km):

Equivalente 10.26l en 190km

Total (1.50€/l): 15.39€

Aunque me toque ir a Mercadona una horita, compensa.

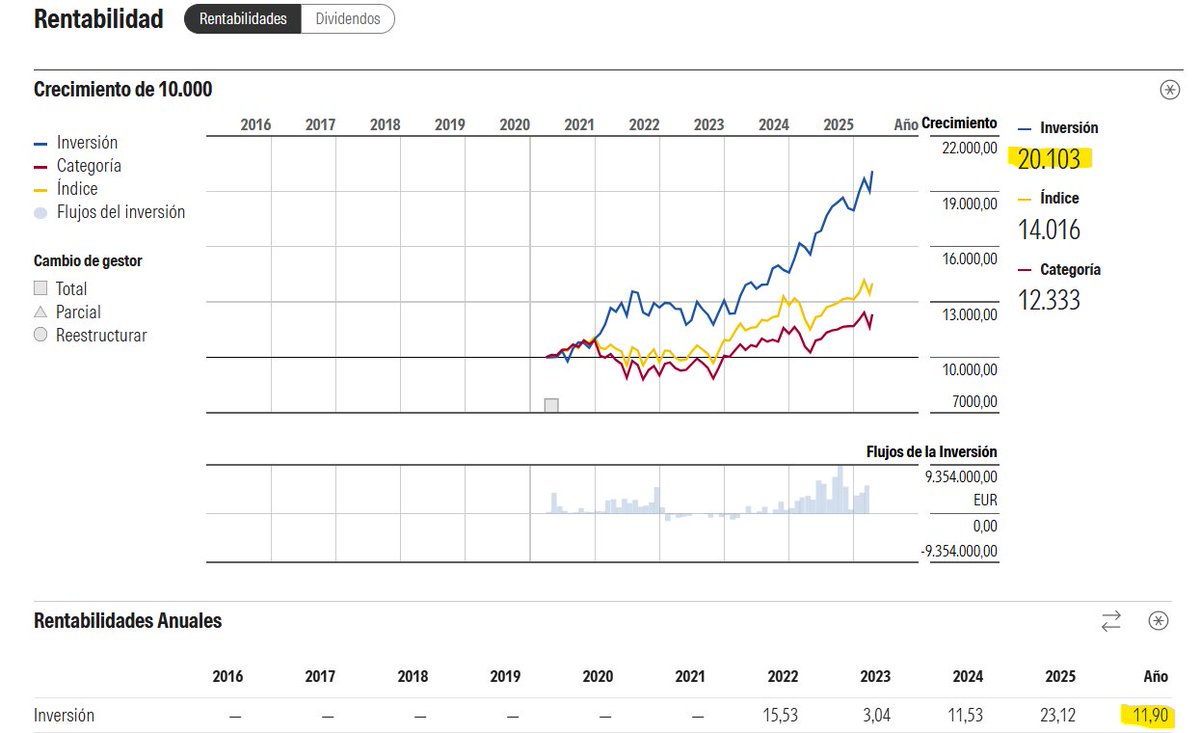

Estoy muy contento de anunciar que ayer alcanzamos un valor liquidativo de 20€ en Sigma Internacional, lo que significa que hemos doblado el capital en menos de 5 años, es decir, una rentabilidad anualizada después de comisiones superior al 15%.

El camino no ha sido recto, y seguramente habrá más curvas, pero puedo asegurar que seguimos tan comprometidos y exigentes como el primer día.

Gracias a los más de 4.000 coinversores por su confianza.

Fue un placer compartir esta charla con @pizarradeandres

Hablamos de una compañía que hemos estado comprando las últimas semanas. Espero que os guste!

https://t.co/LfoGGYkqBO

💥🎥Videotutorial para recuperar las RETENCIONES de los DIVIDENDOS de Francia y Alemania🎥💥

👉Explicación teórica

👉Tutorial punto por punto

Tiene que ser el post con más difusión de mi cuenta❗️

Quema el Like y Comparte ❤️🔁

https://t.co/fDQgzvfzrs

¡Buenos días! ☕️

Arrancamos el Lunes con el balance de PICKS 🆓 del 11-17 Agosto 🗓 a través de este; https://t.co/mBoAmsBR92 nuestro canal de Telegram 📲

VERDES: 44 ✅

SEMI/VERDES: 5 ✅🔵

NULOS: 7 🔵

ROJOS: 18 ❌

🏆📈 SEMANA RÉCORD EN TELEGRAM. La de mayor ganancia desde que iniciamos los balances semanales (16 enero 2023).

El balance se presenta así porque cada tipster usa un Stake distinto. Nuestra recomendación: apostar siempre lo mismo (2–5% del bank).

¿QUERÉIS MÁS PICKS? 👉💯

I gave the deal a second look, turns out it's better than I expected:

- The termination fee seems to be a way to ease the partners' liability recognition. According to the rules, the partner must take the lease under its balance sheet (20y contract), making the balance sheet weaker and concerning debt holders. Putting this provision in will reduce the liability, but it is extremely unlikely that SESA will replace the FLNGs. Be aware that YPF's subsequent phases have no relation to SESA! We need to model a 20-year contract, maybe even longer, as there will be enough gas by then.

-Variable fee. It's a massive win for Golar. For every USD 1/mmbtu gas price above USD 8/mmbtu, GLNG will gain approximately USD 100 million when both FLNGs are in operation, with no cap on the upside. We saw huge prices in 2022, and I'm sure we'll see abnormal prices going forward.

- Financing. The project is now set in stone. It is time to go to the bank, leverage the contracts, and create massive value in NPV terms. They can easily raise more than $3bn in debt.

- US CPI. Profits are linked to the US CPI, which means that EBITDA will grow in line with US inflation. I see 2% average inflation, which makes the FCF much higher, especially since the debt won't be inflation-adjusted. Fixed EBITDA will go up as time passes, different from the Gimi charter, where only expenses are inflation-protected.

- Backlog and EBITDA are understated. They don't include the CPI adjustment or the variable fee, and they especially don't consider potential production. Gimi's nameplate capacity is 2.7 mtpa, but it's only contracted by 2.4 mtpa. However, it was tested at about 3 mpta run rate and worked flawlessly. It is the same here, I'm unsure about Hilli, but I'm sure MK2 can do much more than 3.5 mtpa. It means that the total EBITDA could be 10% higher (>0.6 mtpa)!

- Golar owns 10% of SESA. They didn't disclose the capex they need to put in, but based on the rest of the shareholders' PR, I'd model $100m. This company must be worth multiple times this amount

Overall, $GLNG stock must trade higher as the current price doesn't reflect the already signed projects. Worth mentioning: I expect growth from here. There are many FPSOs in the market, and there is no reason not to have many FLNGs in the coming years.

@HolyFinance Como puede variar tanto el guidance (soliendo ser conservadores) a los datos esperados para dar este profit warning?? Tanto a cambiado el mercado en este corto tiempo?

$AAPL Cash Flow after 2Q

$102 B in FCF TTM (higher than FY23 even on lower revenue)

Apple is sitting out the AI arms ( $NVDA GPUs ) race

While the other Mag7 are ramping Capex, Apple has reduced spend (>$2 B lower in FY24 vs a year ago)

$ABBV debt maturities detail up to 2028

and the $4 B repaid in 2023

New debt to be issued (for acquisitions) will likely have maturities 2027+

Proposed acquisitions:

$10.1 ImmunoGen (closed 1Q)

$8.7 B Cerevel Therapeutics (expected H1)

$ABBV debt (10-Q published yesterday)

Net debt ~$56 B at the end of the quarter

Net debt increased ~$9B (ImmunoGen acquisition)

$15 B new debt issued (connected to ImmunoGen and proposed Cerevel acquisitions)

$9.2 billion acquisition cost of ImmunoGen, Feb12

[1/4]

HOW ENERGY TRADERS LEFT A COUNTRY IN THE COLD

Pakistan, one of the world’s poorest nations, thought it had secured natural gas to fuel its economy

Commodities firms had other ideas

Full story with @FaseehMangi 👇

https://t.co/NHVZMEy7WM

![DividendWave's tweet photo. $ABBV debt (10-Q published yesterday)

Net debt ~$56 B at the end of the quarter

Net debt increased ~$9B (ImmunoGen acquisition)

$15 B new debt issued (connected to ImmunoGen and proposed Cerevel acquisitions)

$9.2 billion acquisition cost of ImmunoGen, Feb12

[1/4] https://t.co/FJQvCJ90gW](https://pbs.twimg.com/media/GMu9XydXUAATe9o.png)