$NVDA $MU $SNDK $LITE I have extensively shared the power and benefits of Autoresearch for agentic LLM processes. There is significant chatter now about Loops and Goals, which are the same/similar workflows. Whatever you want to call it, an agentic LLM process that iteratively improves its output will yield massively improved and more robust final answers than a one-shot response. All of this requires exponentially more GPU and CPU compute. It is almost infinitely unbounded.

@Sovanna_Sek Bonjour Sovanna,

Beaucoup de "high flyers" dans cette liste.

Je ne remets pas en cause la qualité des sociétés ainsi que leur potentiel mais seulement leur cherté.

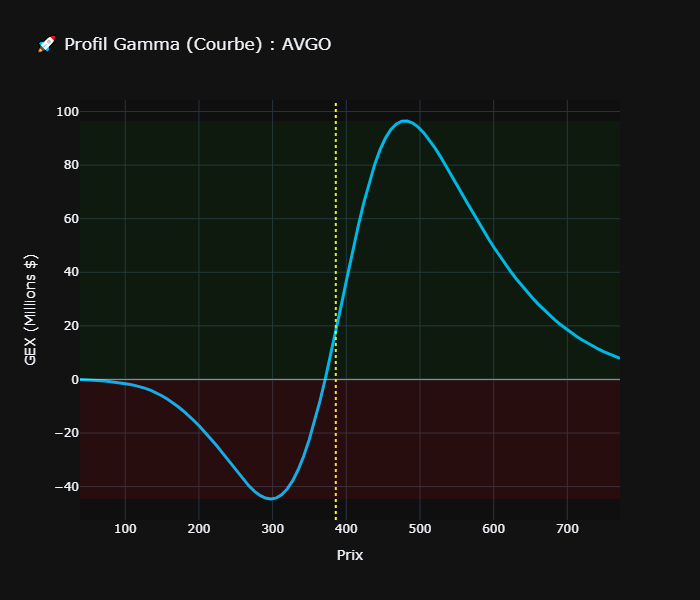

L'exposition gamma négative la plus importante est à 300 sur $AVGO :

Je partage avec vous un graphique que j'ai créé ainsi que la vue d'ensemble sur maturité de juin :

$META is considering charging up to $199.99/month for Hatch, its planned consumer AI agent, per The Information.

Hatch is described as a consumer version of OpenClaw that can create software tools and automate tasks through plain-language prompts, including scheduling events, sending emails, building simple apps, and creating travel itineraries.

A premium Hatch Plus tier would offer 5-10x more daily capacity than the free version.

During development, Hatch has used Anthropic’s Claude models, but at launch it is expected to run on Meta’s Muse Spark model.

Ceci étant dit, actuellement les investisseurs sur $AVGO paient le titre en valorisant une croissance hypothétique induite de la montée en puissance des puces IA.

Comme disait M. Graham, ils paient le prix mais en échange ils recoivent la valeur...

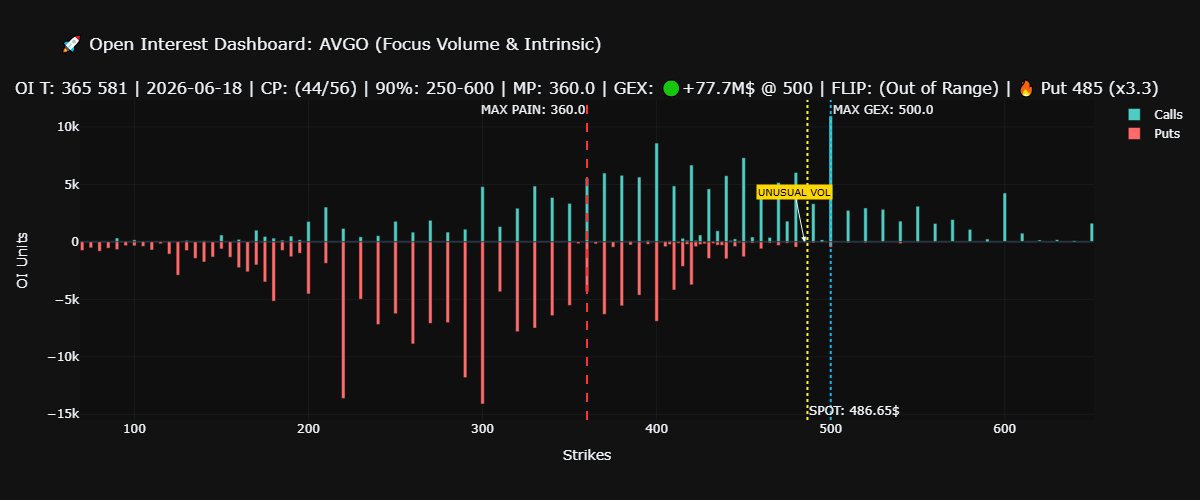

Je reviens sur $AVGO :

il y avait un bon gap entre MP et prix actuel.

Résultats exceptionnels mais pas paraboliques.

Ce à dire que les MM étaient en embuscade et chassent la moindre faiblesse. Je ne m'aventurerais pas dans ce raisonnement.

A vous de vous faire une idée...

🦔Broadcom beat revenue estimates ($22.19B vs $22.13B expected), beat earnings ($2.44 vs $2.39), and posted 143% AI chip revenue growth. The stock dropped 13% after hours anyway. AI chip sales guidance for next quarter came in at $16 billion, below the $17.2 billion Wall Street expected.

The stock had added $300 billion in valuation over the previous five sessions. But on the earnings call, Broadcom CEO Hock Tan was asked whether he sees productivity gains from AI agents. His answer was no.

My Take

Hock Tan sells the chips that power AI infrastructure and he just told an earnings call full of analysts that the productivity gains from AI agents haven't shown up. IBM's CEO said this week the revenue to justify $6 to $8 trillion in AI capex probably doesn't exist. Now Broadcom's CEO says the productivity those investments are supposed to unlock hasn't materialized either. Two shovel sellers in the same week, both profiting from the boom, neither able to defend the end product.

Broadcom gained $300 billion in five trading days and lost $63 billion in one evening on an earnings beat. Revenue up 48%, strong margins, solid free cash flow. But the AI chip guidance missed by $1.2 billion and Tan admitted the technology his chips power hasn't moved the needle on productivity. At some point the distance between what these companies are valued at and what AI is delivering in the real economy has to close. Either the productivity arrives or the valuations adjust. This week has offered a lot of evidence for one of those and very little for the other.

Hedgie🤗

Tbh $XFAB lowkey reminds me of early $TSEM.

Just sub <$2B MC.

You basically never find a company with $NVDA and $NOK actively validating your pre-commercial silicon photonics foundry… (photonixFAB)

While getting CHIPS act/Gov grants to subsidize capex.

While leading the Europe’s effort to build a photonics supply chain.

Feels like that alone would justify valuations… but you get the power semi SiC/GaN operations for free too and all its assets.

CHIPS act 2 is coming out tomorrow, and $XFAB is listed in the photonics blueprints.

Did I miss something?

Or did markets miss something?

Des arguments intéressants sur $XFAB !

Longtemps assimilé à un titre en corrélation étroite avec l'EV.

J'attends 2027 afin de voir si l'adoption de la photonique aura un impact sur le titre.

Est-ce $NVDA fera sortir le titre de l'ornière ?

$XFAB (photonics + power semis) is an interesting long at ~€1.5B market cap.

EU Chips Act 2.0 drops this week. Photonics is the centrepiece. $XFAB was on the steering committee that wrote the white paper demanding it.

Why this matters:

Mass-producing photonic components for Nvidia’s optical products under “photonixFAB”

800V DC power semi exposure through SiC partnerships

$128M euros from EU Chips Act 1. $50M from US Chips Act

~1.3x P/B — depressed by auto legacy drag, not business quality

Government is essentially funding their capex

Markets missed the Nvidia silicon photonics relationship because it operates under a different name.

Dans la même discipline avec un ratio plus soutenable que $MRVL on trouve $AVGO qui se négocie à un PE de 43.

Même thématique, exposition à l'IA similaire mais valorisation différente.

Avec un PE de 161 sur $MRVL, les investisseurs s'attendent à quoi au juste ?

Une croissance hors norme peut-être ?

Malheureusement on sait comment tout cela se finit tot ou tard ...