When we started the discount brokerage (flat fee per trade) model in India in 2010, we decided to charge the same fee regardless of trade size. The logic was simple: if the effort to execute a trade is the same, why should customers pay differently? We applied the same logic to mutual funds. We didn't launch MFs until we could sell exclusively direct plans.

You can't call yourself a discount or a low-cost broker if you charge a percentage fee on transactions, because there's no incremental effort in executing a larger order. This logic has informed all our product and pricing decisions from day one.

Anyway, @CoinByZerodha today is the largest direct mutual funds platform in India, with nearly ₹1.6 lakh crores in direct MF AUM, and all our customers have saved thousands of crores in commissions. Direct mutual funds are a no-brainer if you're a DIY investor.

It's interesting that most of the direct MF platforms that started when we launched Coin have either disappeared or pivoted to something else. The few remaining platforms are also rethinking their choice of offering direct plans. However, at Zerodha, we will continue to offer direct mutual funds for free.

A lot of investors still don't know the difference between direct and regular plans. If you are investing in mutual funds, it's worth checking if your investments are in regular or direct plans. If you are in regular plans and want to switch to direct, we can help.

Onboarding for NRIs has always been a pain. Right now, the FCNR deposit scheme is a total no-brainer: the RBI is bearing the currency hedging bill, allowing you to get local, FD-like rates while your money stays in dollars with zero rupee risk.

But despite how good the scheme is, it doesn't help if opening an account takes 60 days. By the time the paperwork clears, the window might have closed, or the NRI may have lost interest.

@rupeeflo, a @Rainmatterin-backed startup, is trying to solve this problem. They've partnered with leading banks to slash that 60-day onboarding down to just 24 hours, covering the bank account, trading account, demat, and the whole works.

It will be interesting to watch what happens to activation rates once friction is this low. Does removing the 60-day wait actually change NRI behavior, or does the inertia live somewhere else entirely?

Akshayakalpa has 13 years of data showing that simply introducing bee boxes increases the average coconut yield per farm by 20%. It’s such a massive win-win that they’ve now integrated 7,500 bee boxes across all their farms.

Shashi from @akshayakalpa recently brought over two bee boxes for my home to get us started with beekeeping. In this clip (full video in comments), he walks through how incredibly simple it is to set up a bee home, even in smaller or semi-urban spaces.

The bigger takeaway here is about how we view sustainability. We often look for grand, complex technological solutions to environmental issues. But the reality is that our survival is deeply tied to basic, interconnected ecosystems.

Without pollinators, our food systems collapse; roughly a third of what we eat depends entirely on them. Taking care of them isn't just a good deed; it's an absolute necessity for our own survival. And I think education is the key, which maybe the bee boxes in urban spaces can do.

Can’t be prouder of everything that the Akshayakalpa team is doing for improving the quality of life of farmers, their economics, their cows, and everything else.

NSE is a cash generation and distribution machine. In FY26 alone, NSE earned a profit of over ₹10,300 crore and paid out roughly ₹8,660 crore in dividends— a payout ratio of 84%. This will likely continue even after listing because NSE can't do much with the excess profits. SEBI doesn't allow exchanges to invest in other businesses, listed or private.

So why aren't there more businesses like this?

It comes down to a tax arbitrage. Assume a business earns ₹100. It pays ~25% corporate tax, leaving ₹75. If that ₹75 is distributed as dividends, the shareholder pays tax again at their marginal rate. Can be another ~36% for someone in the highest bracket. The investor ends up with ₹48 out of the original ₹100.

Now contrast that with a company that reinvests the entire ₹100 into growth. If that growth reflects in the stock price, the investor pays capital gains tax only when they sell and at a much lower rate of 14.5% (the highest rate). Adding to this, there is no tax on this ₹100 because nothing is booked as profit.

A differential of 14.5 % vs 51% creates a strong incentive for profitable companies to reinvest aggressively rather than distribute. Which is why you don't see many new-age businesses choosing to be profitable in the first place.

I hope something changes here. Reinvestment is good for the economy in the short run, but businesses that aren't profitable are also far more vulnerable. One bad cycle can kneecap them severely. In the long run, that isn't smart.

This is part of a much larger global debate: the double taxation of corporate profits. Many countries have tried to address it. The US taxes dividends from most listed companies at lower rates than regular income through "qualified dividends." Australia gives investors credit for tax already paid by the company on its profits.

I have a conflict of interest on this topic. At Zerodha, almost all the cash we generate is retained and reinvested in startups through @Rainmatterin, the social sector through our @RainmatterOrg, or listed companies/Gold/Bonds. Even otherwise, it doesn't make sense to pay another tax and take out dividends, one of the few negatives of not being listed.

I think there should not be such a big differential in taxes, on dividend income as compared to capital gain. 😀

This whole Gen Z categorisation feels very incomplete. When we were all younger in our generation, buying a house still felt like a distant dream. And it's not really changed massively. So what has changed?

Perhaps what's changed is glorification of experiences through social media. The yearning of validation. And yeah, it could be one of many reasons. But I don't think it's fair to say there is only one specific reason why people are spending more on experiences. Some of it is just natural as we get better choices and better products.

India has been consistently warming up. Decade after decade, temperatures have been rising, and this is a one-way journey unless humanity makes a dramatic course correction.

All the heatwave deaths that are in the news are the result of this relentless warming. You will see a lot of numbers floating around, especially the recent viral study that a single day of extreme heat causes roughly 3,400 excess deaths across India, and a five-day heatwave nearly 30,000. But the truth is, we still don’t have good statistics on how many Indians are losing their lives because of heatwaves.

What we do know is this: a vast majority of Indian employment is still informal. The number of people employed in agriculture, construction, gig work, and other outdoor work remains disproportionately high. We have come a long way, but this is still the reality for a very large number of Indians.

For many Indians, staying indoors when temperatures rise is simply not a luxury they can afford. There is also a deep inequality in access to cooling. Yes, the fact that almost all of India has been electrified is a genuine achievement. But access to air coolers, let alone air conditioners, is still low and mostly concentrated among people with higher incomes. Fans only do so much when the heat is this brutal.

This is the inequality of heat. People with good incomes can afford coolers and ACs. They can work from home and can avoid the worst hours of the day. But this is a small subset of India.

Remember, more than 40% of Indians are still employed in agriculture, even though agriculture’s share of India’s GDP has consistently declined. These are the real Indians who will be most affected by rising temperatures. Many of the regions most exposed to climatic shocks like El Niño and heatwaves are also among the poorer regions of northern India.

So the people who will be hit the hardest by rising temperatures are the poorest Indians, across regions that are yet to see real prosperity.

Sadly, this is a systemic crisis. Individual actions help, but they are not enough. We need collective action, not just at a country level, but at a global level. Climate change is not an Indian problem but a global problem.

That said, there are still some low-hanging fruits that can start making a difference.

There is a lot of debate and controversy over India’s forest cover and whether it has increased or decreased. But when it comes to cities, we can see the loss of green cover firsthand. Trees are cut to make way for roads, houses, flyovers, and buildings. Whatever few trees remain are often trapped under pavements and concrete. This weakens them. This is one reason why trees often fall even after moderate rains.

If you have space, you can plant native species like neem, moringa, jamun, amla, and curry leaves. These trees have deep roots and can survive better. People often avoid planting trees because they worry that the roots will damage the foundations of their homes. But in many cases, this fear is overstated.

These are small things which help.

But as depressing as it sounds, this problem ultimately needs systemic, collective action at a global level. And judging by the way the world is heading, it is very hard to have hope.

Rising temperatures are a serious challenge. They don’t have easy explanations, and they definitely don’t have easy solutions.

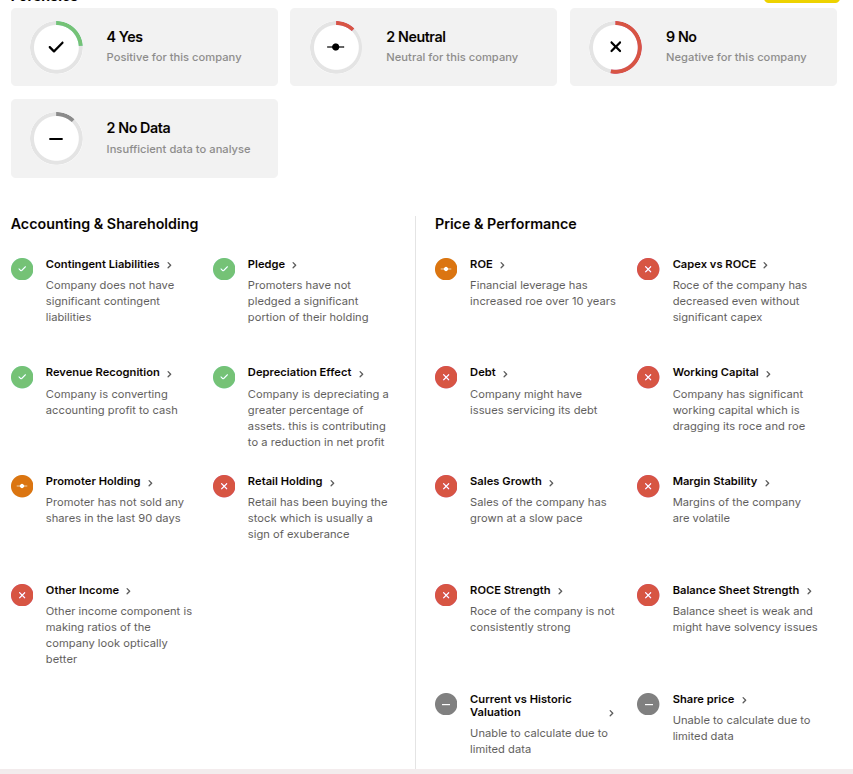

Indian investors keep getting regular reminders that ignoring corporate governance can come back to bite them in spectacular fashion. A bad stock pick and poor position sizing can wipe out a big chunk of your portfolio.

Avoiding the worst of the worst stocks is perhaps more important than choosing the best ones. @Tijori1 has two useful features that can help you screen out terrible stocks.

On Tijoristack, you can generate a Risk Probe Report that shows you all the risks, red flags, and vulnerabilities you should watch out for. This is a detailed report that analyzes all the company financials and disclosures.

The second is the forensics tab on their site that gives you a broad overview of things you should dig deeper into.

Tijori website: https://t.co/JZVRNGyANK

Tijoristack: https://t.co/1bmRi2APD1

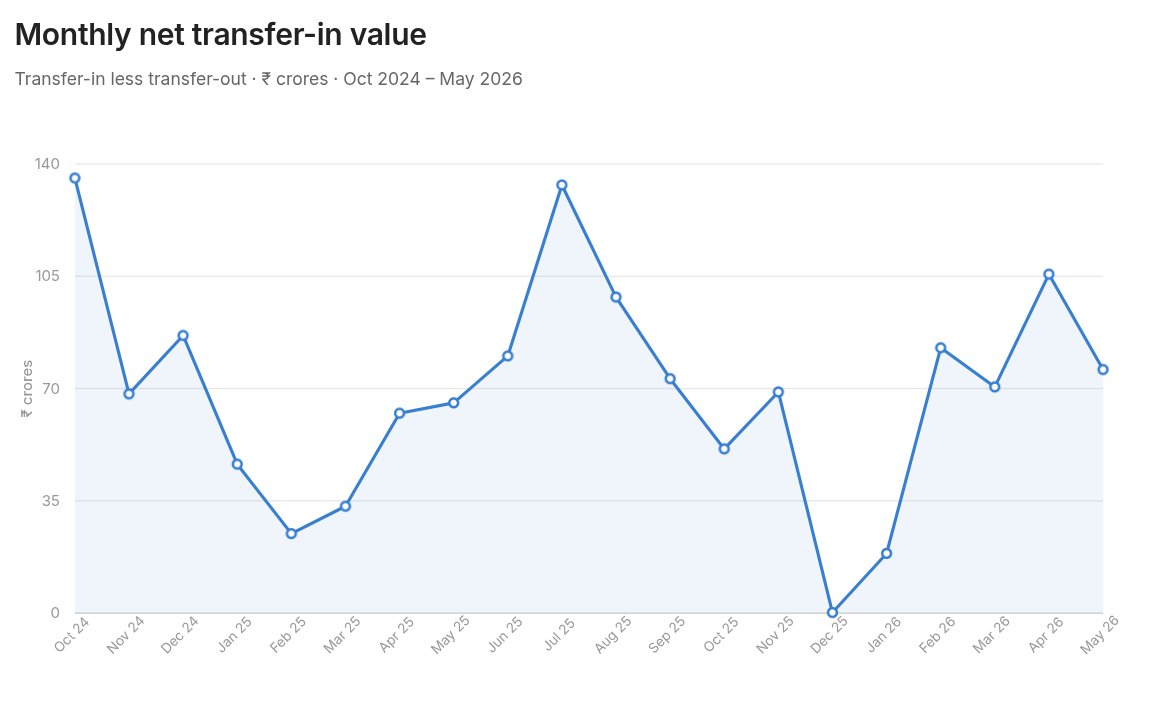

The average investor typically has 2-3 demat accounts with holdings spread across them. The problem with this is that it makes tracking one's investments and filing taxes a nightmare.

To make it easy for people to move their holdings to their @zerodha account, we'll now refund all depository charges (DP charges) that you incur to move your holdings to Zerodha. With this charge gone, pretty much everything at Zerodha is free, including investing in stocks, ETFs, direct mutual funds, and bonds.

Even the AMC is more or less free because of BSDA limits, and on top of that we're making the first-year AMC free. So you only pay if you do intraday or F&O trades.

For all transferred-in stock, we let you enter the acquisition price so that your P&L isn't messed up and you can track your portfolio properly. We also offer the option to open a secondary demat account if you want to segregate your holdings for whatever reason — short- and long-term investments, for example.

By the way, this is the monthly net delivery of stocks (transfer in − transfer out) at Zerodha. I'll share an updated chart in 6 months to see if us taking DP transfer charges on our head makes any difference😀

In the last year or so, we've continued to launch new features, both big and small to make life easier for traders and investors. The latest feature that went live on the Kite mobile app is position grouping.

If you actively trade and have multiple positions across different indices and expiries, tracking those positions can be messy. Odds are, you may end up making a mistake because of this. To make this easy, we've built position grouping on Kite. What you can now do is group your positions based on things like the underlying index of an F&O contract and expiry.

You can also use the feature to exit multiple groups of positions in one go.

Yesterday was all about the @GalaxEye team. And the way the country celebrated their success shows how far we've come.

But it is also a good time to remember there are so many other startups who are giving their best and trying to create impact in their own ways. And the margins are so fine in entrepreneurship that for every success we have tons of ventures who don't make it. But all entrepreneurs need to be celebrated. It's an ecosystem, that needs more and more support.

I wish for our Govt, our leaders to speak about one startup every month, and get them the attention they rightly deserve. Our Prime Minister has been championing it through @mannkibaat, but we need more and more leaders across party lines to try and help startups across the country. I hope through everyone who has a voice and has the reach, our startups can find more and more customers. So that they don't have to chase investors. :)

Since we published the 1st module on @ZerodhaVarsity (2014), there has been one constant request - to release the module in book format. I think many still prefer holding a book in hand, flipping through pages, highlighting, and taking notes. For all of them, here is the book 😊

This book is for those who want to get started with the stock markets, but dont know where and how to start.

Thanks to Trisha Bora and @HarperCollinsIN for nudging me constantly to work on this book :)

It feels odd to say this - but the link to preorder the book is in the comments below 😬

Rainmatter started in 2016, with a few of us doubling up on our day jobs and trying to help startups that were trying to expand India’s capital markets ecosystem. Nine years later, it has grown into something far bigger than we ever imagined.

So far, we’ve invested over ₹1,500 crore across 160+ startups spanning fintech, climate, health, media, and deep tech. We’ve also earmarked 10% of everything Zerodha earns to invest in startups, and another 10% for the social sector through the @RainmatterOrg.

The thesis has evolved from just expanding the capital markets, but the thread running through it is simple. As a country, we need to own more of what we consume. Sovereignty, in the truest sense.

We’re not a typical VC. We don’t take board seats, and we’re not in this for quick exits. We’re not interested in forcing founders into short-term decisions just so we can make money in five or six years.

The simple reality is that building a good business is hard. Building one that is genuinely useful, scalable, and profitable is even harder when investors are pushing you to speedrun success and sustainability.

That kind of pressure usually leads to shortcuts. And shortcuts, more often than not, come at the consumer’s expense.

So our approach has been simple: be patient, back founders for the long term, and help them build the business the right way.

That, more than anything else, is the heart of @Rainmatterin.

The first step to fixing Indian sports is putting sportspeople in charge of sports federations. Out of 63 vice presidents across major sports federations only 6 have a sporting background. We allocated ~4480 crore annually to sports yet local stadiums remain dilapidated and athletes struggle financially. We’ve to replace self nomination and insider voting with athlete led elections. Olympians and athletes who've represented India should have the right to elect federation members and choose people who actually understand what it takes to compete at the highest level.

If we want better outcomes, we’ve to put decision making in the hands of people who’ve lived the sport. Else we’ll always keep debating medals instead of building a system that produces them.

Hyrox in India has grown from 1600 participants in the first edition to ~9000 in just the 4th edition. Each paying avg 9k for entry fee. Crazy growth in less than 12 months. Happy investor :)

This is a great and proactive move. The nuisance of unregistered advisory has only gotten worse.

Link to press release in comments.

Article in the @EconomicTimes.

Traders and investors have their own preferences on what they want on their screens. An intraday scalper will value speed and a quick order window above all else, while an options trader may always want the option chain open.

Kite's classic web UI was designed to work universally for everybody. More than a decade later, despite us adding a ton of features and capabilities, Kite is still extremely light and fast with a tiny bundle size.

While desktop trading platforms have historically had widgets, web technologies weren't suited for this for the longest time. We've prototyped this on and off over the years, and last year building a web-based trading terminal became doable with native web technologies.

Introducing Kite Terminal mode. We rebuilt Kite web completely and made every single feature it has into a widget. You can now drag, drop, and rearrange all the components inside Kite to design your own interface tailor-made for the way you trade and invest. We have put in a ton of work to make the interface snappy with smooth UX. Now you can build your own trading interface like assembling Lego blocks.

In addition to investment and trading widgets, we've also added a bunch of productivity and personalization ones like notes, clocks, calendars, wallpapers, my Twitter feed (follow me on Kite) 😛 and more.

I'm excited to see how people design their layouts. Share a screenshot of your workspace in the comments.

I don't use net banking apps on my phone because the mandatory permissions they ask for make no sense.

Why does a banking app need access to my SMS, phone, contacts, etc., in the name of security, when not seeking invasive device permissions is, in fact, the global benchmark for cybersecurity. This is called the Principle of Least Privilege (PoLP).

“Don't do unto others what you don't want done unto you” has been at the heart of the Zerodha philosophy.

This is exactly why we've built Zerodha the way we have. Kite asks for ZERO permissions on mobile, for instance, and this is one of the big reasons why millions of people trust us. What has enabled us is SEBI's mandatory strong two-factor authentication framework strike the right balance between security and privacy.

I think paying advance tax is the most underrated way to save up. Tomorrow is the last deadline for final advance tax instalment for FY 2025-26.

Miss it → pay 1% interest per month.

Note in the comments has steps to download your statements from @zerodha Console.