.@Robinhoodapp's launch is about more than another Earn product. It demonstrates how regulated financial institutions can build native stablecoin savings products without rebuilding every layer from scratch.

It also signals a broader market trend: institutions increasingly combine specialist infrastructure providers with allocation intelligence to power the next generation of stablecoin financial products.

We took a closer look at Spark's role in the USDG ecosystem, and why we think this launch marks an important step in the evolution of stablecoin-powered financial products.

Read more here: https://t.co/eM2Pv4f8FZ

I’m thrilled that Spark was selected as a Robinhood Chain Day 1 launch partner with Spark Savings USDG (spUSDG) to export the USDS savings rate to Robinhood’s 28 million users.

Spark Savings lets users deposit stablecoins and earn yield from Spark's liquidity deployments across DeFi, CeFi and TradFi, enabling fintechs to launch native stablecoin earn products without building liquidity infrastructure from scratch. We're already live with spUSDC, spUSDT, spPYUSD and spETH, with spUSDG representing the next step.

As mentioned in my post last week, we are moving to a world where exchanges, fintechs, and banks are converging on “Everything Apps”. The pattern is becoming clear with a centralized exchange component, a blockchain component, and a stablecoin.

As the primary liquidity tranche in the Robinhood Earn program, Spark will hold large amounts of USDG on its balance sheet. This otherwise idle USDG can be put to work inside the Stablecoin FX Layer on Uniswap to pair against USDS, which in turn provides deeper shared liquidity to USDC/USDT/PYUSD.

This launch is a significant event because it marks the first integration of a mid-cap stablecoin into a US fintech's earn program. This exposes the stablecoin to Robinhood’s sizable distribution, making USDG a serious contender in the stablecoin space.

As payments, savings and lending continue to move on-chain, swap volume between stablecoins is going to increase drastically, and the Stablecoin FX Layer is best suited to absorb this coming demand surge.

SparkLend is now the largest wstETH holder in the world!

SparkLend is the largest and most liquid venue for ETH looping, e-mode enabled for wstETH collateral exclusively.

See more here: https://t.co/2PuxgceeUu

SPK is now available on @Revolut across the EU, and UK.

This expands access to Spark through one of the largest consumer financial platforms in Europe.

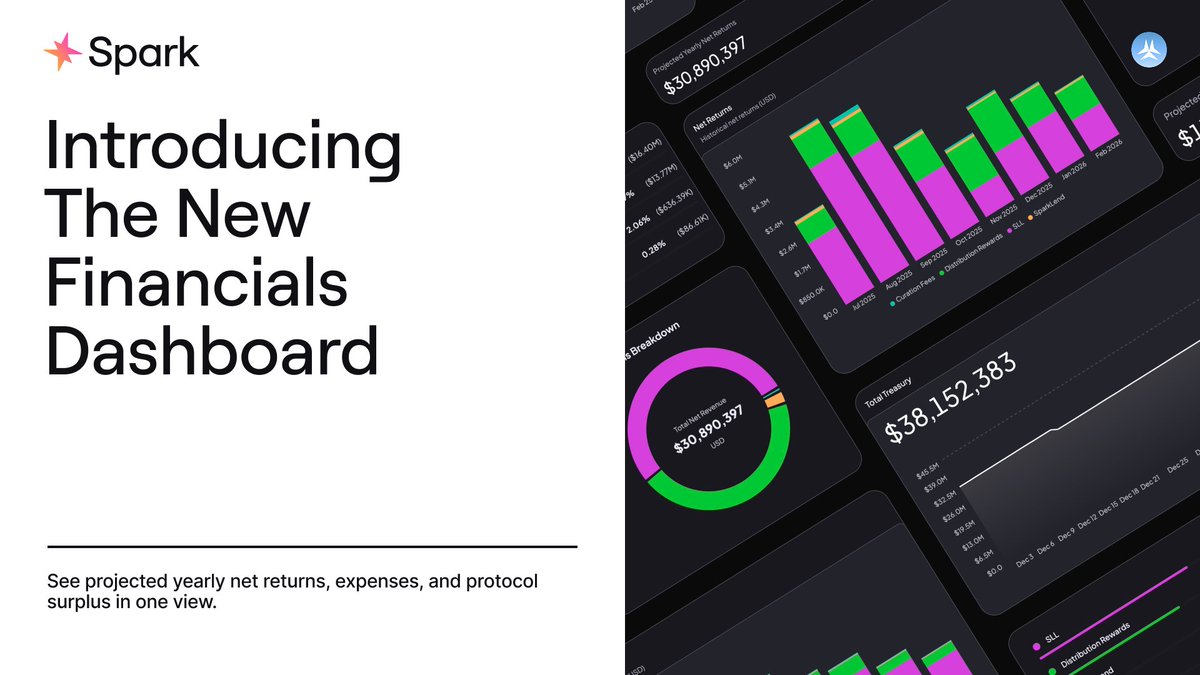

Spark is infrastructure for on-chain credit markets, allocating capital across lending markets and liquidity venues through a rules-based framework designed for predictable liquidity and transparent risk.

Today, Spark coordinates over $11B in capital powering lending and savings activity across DeFi.

More on Spark: https://t.co/KA7Y571BEU

rates on @aave have risen quite a bit in the past week, making LST loops unprofitable and stablecoin borrows significantly more costly

thankfully, the chads at @DeFiSaver have made migrating positions to alternative lending protocols like @sparkdotfi SparkLend easy

here's how->

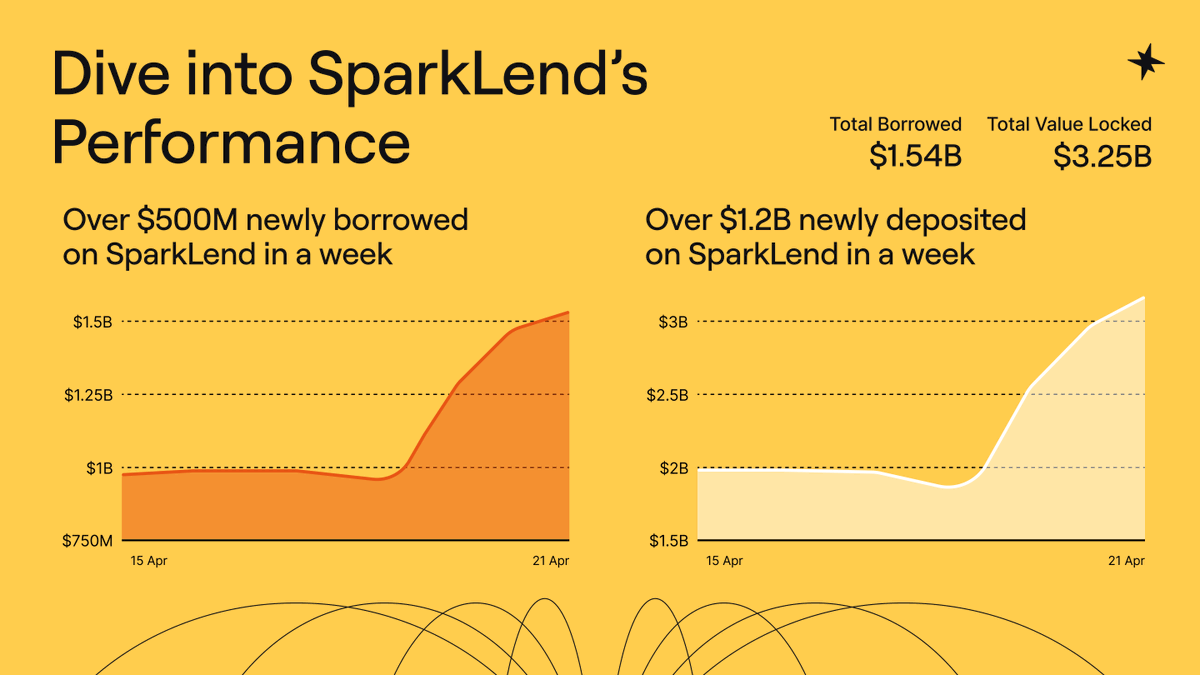

SparkLend recorded over $500M in new borrows and $1.2B in new deposits over the past week.

As volatility increased across lending markets, demand shifted towards reliable liquidity access and borrowing capacity.

SparkLend’s infrastructure and deep liquidity absorbed that demand without disruption.

Explore SparkLend 👇

https://t.co/Utr5mW98Yo

Spark Savings spUSDT is the ONLY liquid defi deposit for USDT

Aave Core: illiquid for past 2 days (and potential bad debt for rsETH hack)

Morpho: currently all major vaults/markets are at 100% utilization

@sparkdotfi Savings: >$400 million in instantly available liquidity

Spark is focused on maximizing user safety across our product suite

this is why we deprecated rsETH (alongside other low-usage assets) in January, and continue to tighten the collateral and feature-set over time

it's also why we have continued to set a high max-rate on our SparkLend ETH market.

this was not very popular among eth-loopers, and likely lost us considerable business and revenue to aave markets over the past year as aave cut max borrow rates on ETH to 10% or less

but in the current situation, it is clear that our approach was the prudent choice, with SparkLend continuing to have ample liquidity for ETH withdrawals while Aave markets across Mainnet, Arbitrum, Plasma, Mantle, and Base are locked up

because ETH is a core collateral asset, illiquidity isnt just an inconvenience for depositors, it presents a critical safety risk where liquidations of ETH collateral cannot take place while markets are at 100% utilization. with current illiquidity conditions on Aave, a 15-20% ETHUSD price drop could cause significant bad debt accumulation (on top of any potential issues attributable to the direct rsETH exploit)

stay safe, use Spark

There are two apps I’m currently lending ETH for absurdly high rates, not suffering from any rsETH bad debt afaik but benefitting from the huge surge in ETH lending APYs.

@0xfluid@sparkdotfi Lend

Waiting for more information to come from Kelp and then more importantly from Aave. Aave will survive all this but it’s a big stress test for Umbrella (which can’t cover the total estimated bad debt).

There is nothing wrong with doing nothing here. Wait for more info.

it's really crazy that layerzero doesn't have some redundant sanity check and allows to bridge 116,500 rseth from a chain with a supply of 49

anyway here is my investigation https://t.co/4J0f7fscck

The India Early Bird voucher is now open for all residents of India 🇮🇳

✔️ Secure early access at $99 (lowest price for local attendees)

✔️ Limited vouchers available, until sold out!

How to secure your spot 👇

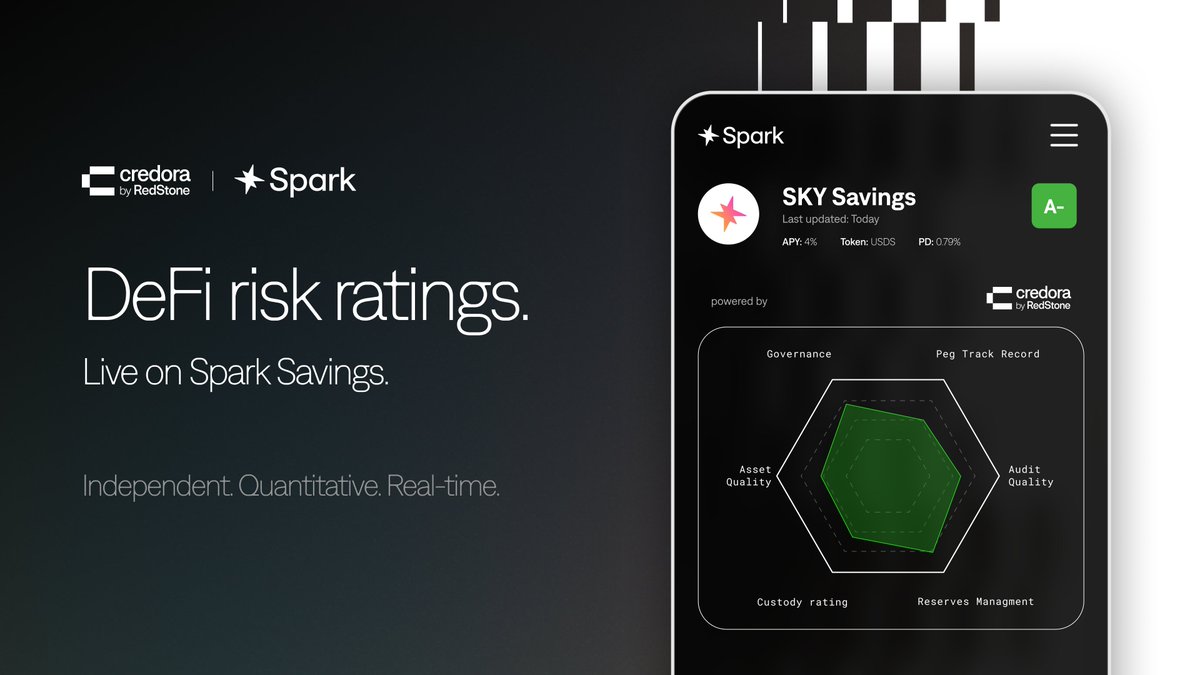

Credora ratings are now live on @sparkdotfi.

You’ve seen the grades: A-, A, B+. But what’s actually behind them, and how did we get there?

A full breakdown of the Spark Savings Risk Assessment 🧵