Cursor ARR: $100M → $500M → $1B → $2B . In 13 months.

@SpaceX preempted the fundraise with a $60B acquisition right.

The exit might not be an IPO. It might be a bilateral private deal.

Investors without cap table access don't get a second shot. @cursor_ai

Q1 2026: $297B in global VC. +150% YoY.

OpenAI ($122B), Anthropic ($30B), xAI ($20B), Waymo ($16B) = 63% of all of it.

Seed deal count: -31%.

Capital concentration this extreme doesn't reduce opportunity. It concentrates it elsewhere.

Meta started paying creators in USDC this week.

Colombia, Philippines, Solana, Stripe. Libra tried building a new monetary system. USDC just attaches to the dollar.

Same week: @ycombinator seeds in USDC. @a16z backs a stablecoin clearinghouse. GENIUS Act moves. @Meta

Blackstone co-invested in a 2-year-old AI coding startup at Series C.

Factory: $150M at $1.5B. Droids handles the full software development life cycle autonomously. Customers: Nvidia, Adobe, EY.

They don't do this for developer productivity plays. They do it when AI starts replacing labor at portfolio scale.

David Silver just raised $1.1B at a $5.1B valuation.

No product. No revenue. No roadmap. Sequoia, Lightspeed, Nvidia, Google, UK Sovereign AI Fund.

Largest seed in European history.

This is venture capital as research grant.

$38B. Five months old. No product.

Project Prometheus raised $10B. JPMorgan and BlackRock on the cap table. 120 people from OpenAI, Meta, DeepMind.

Not priced on a roadmap. Priced on talent density.

That's where physical AI alpha sits.

Physical Intelligence: $600M at $5.6B. Now $1B at $11B. Four months.

It doesn't build robots. It builds the model that controls any robot.

π0 is the GPT-4 moment for physical AI. Infrastructure, not hardware.

@physical_int

Cerebras goes public at $22-25B (CBRS).

WSE-3: 57x larger than H100. 20x faster inference. $10B OpenAI deal anchors the IPO. AWS cloud next.

The private window on AI chip infrastructure is closing. @cerebras

$1B ARR → $30B ARR in 15 months.

Claude Code crossed $2.5B annualized by Feb. 1,000+ customers at $1M+ spend.

Model subscriptions don't explain 30x growth. Workflow embedding does.

The next company running that playbook is still private.

@AnthropicAI

70% of US startup funding in 2025 went to $100M+ rounds.

Seed bar in 2026: $300K-$500K ARR before anyone writes a check.

AI took 65% of VC deal value. Non-AI founders compete for the rest at the highest traction bar since 2018.

"Venture exposure" isn't one market anymore.

Gulf sovereign funds aren't passive LPs anymore.

MGX co-led Anthropic's $30B Series G at $380B. Saudi's PIF is building the world's largest data center ($2.7B, 480MW).

By the time a round prices, the sovereign allocation is already committed.

@mgx_ai

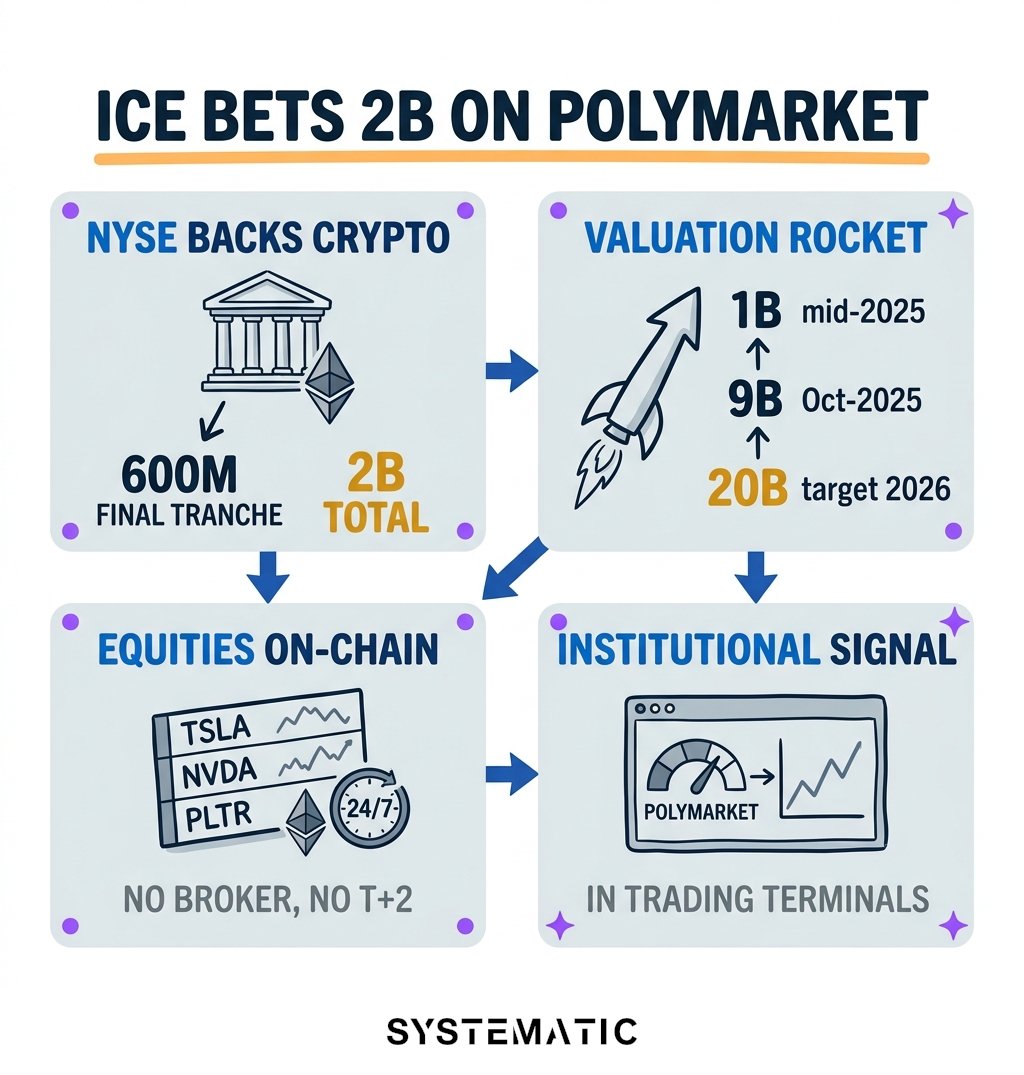

The NYSE's parent committed $2B to a prediction market on Ethereum.

$1B → $9B → targeting $20B. All private. Under 12 months.

That's not a crypto bet. It's an infrastructure call.

@Polymarket@NYSE@BitMNR

$BMNR $ETH

The NYSE's parent committed $2B to a prediction market on Ethereum.

$1B → $9B → targeting $20B. All private. Under 12 months.

That's not a crypto bet. It's an infrastructure call.

@Polymarket@NYSE@BitMNR

$BMNR $ETH

Databricks just closed $7B at $134B. $5.4B ARR. Growing 65%. FCF positive.

Still private.

Public markets set the multiple at IPO. The value creation happens before the ticker exists.

@databricks

$950M into industrial robotics in 48 hours. Largest single week on record.

@rhodaai : $450M, $1.7B. Mind Robotics: $500M, $2B.

Physical AI is at the LLM moment of 2020-21. Investors who can read hardware see the next one at $150M. Everyone else finds out at the IPO.