@GreenhavenRoad Management need to provide more clarity over ST revenues, not to obfuscate reporting and change focus to licensing, or top line growth not credible. If u trust management comms on ST then high teen growth seems way understated even with macro and if you don’t, is it investable

@GreenhavenRoad Now in Q422 it’s grown 650% YoY, so let’s say $32.5m revs. That’s ~30% of On device media which only grew 22% YoY, or 18% of total revs growing at 650% but Rev only 19% YoY at total! While dynamic installs still 44% of ODM vs 50% fy21. It doesn’t add up

@GreenhavenRoad In Oct 21 saying scale to 150 advertisers or $1bn+ revs (ex licensing) in cpl of years, and hitting 50 advertisers in Q3, how’s that tracking? Now calling ST ‘enablement capability’ is disingenuous vs that context, and saying ‘not splitting it out’ - but they did with 650% YoY!

@FrankYanWang @GauchoRico@InvestiAnalyst Hi Frank, yeah I consolidated my PF and moved some of it into $apps during the drawn down. More and more interested in timing. I wait for mid 22 to move into Covid names if they continue to execute.

https://t.co/q3vZbBD2r2

@JibjoJames@FundasyInvestor Would caution tho that 1. ST testing historically slow and 2. mngt said publisher side would be ~10% of near term ST opp (~$150m annual runrate).

Interested to hear in Q3 cadence of testing & if any upside to this view.

Demonstrates the ST value proposition tho

@forced_long Recommend reading their presentation from May on the acqs & listen to 1 or 2 of their conferences for detail :)

Conferences:

https://t.co/os1iwMMzaa

Presentation:

https://t.co/z33im5GORM

@adventuresinfi @DanJoshuaRubin @StackInvesting@hhhypergrowth This is a key point, compare their sales efficiency - what does that say about their relative propositions (& future growth). U can buy growth at any price. Mkt price driving narrative here imo.

Will update table & inc. $S - won't be favourable for them.

https://t.co/ivlTpNAkaV

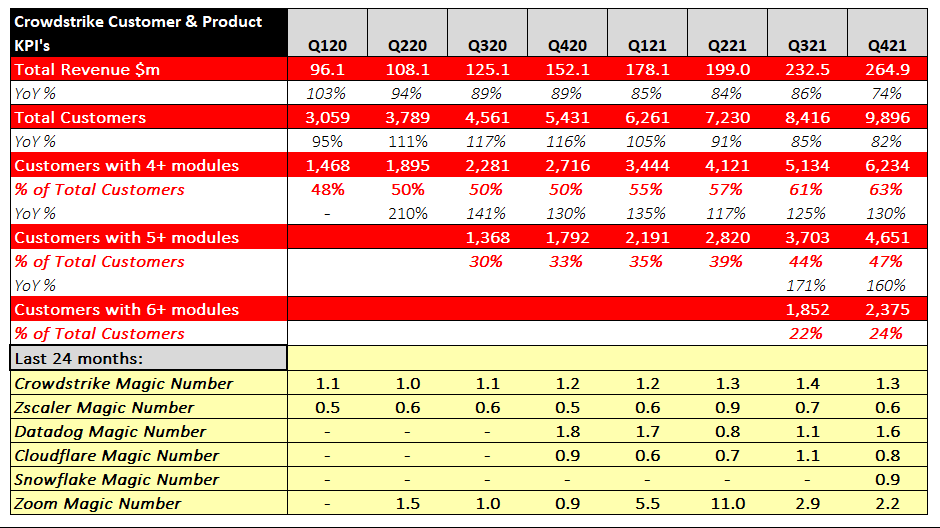

Crowdstrike is able to maintain its high growth rate in part by rapid module expansion and improving sales efficiency.

$CRWD now has 17 available modules with more to come this year.

Land & expand + 'Magic Number':

$CRWD $DDOG & $ZM

@srinath_kattula Hi Srinath, I don't disagree. Mgnt were emphatic multiple times that 150 advertisers would be quick and moderate. They have 750+ advertisers they are already partnered with. Their outlook is $750k avg spend p/m vs $500k atm. Will be interesting to track cadence in coming Q's

@9of9ine Acqn mix blip. With 130% EBITDA growth, 3 yr fwd Ebitda growth at 120% CAGR, margins will improve with op leverage, scale & synergies (broadly by owning full life cycle of device can cut out 3rd parties). So expect rapid margin improvement :)