one of the greatest visuals of all time. would add that some of the black lines of the past connect to green lines of the future even if it’s not clear how.

i think buffett’s famous hiring framework ‘intelligence, energy, integrity’ misses some key things we've experienced viscerally:

1 grit / Commitment / will to win

2 low expectations / grateful and delighted when comp/equity is increased

3 Likability / good hang / airplane test / energy giving / do I want to spend my life interacting w this person and do I think he/she can get others to follow?

i.e., i think you can have someone that exemplifies the Buffett/Koch trifecta (‘energy/intelligence/integrity’ or kochese ‘virtue/talents’4), but 1) lacks consistency/commitment so jumps around like Danson and PK highsmith or something, vs getting-the-job-done, or 2) expects to make AI money and otherwise resentment festers (guess this would be on us in screening / expectation setting), and 3) is generally energy-draining to interact with (eg seeing their name pop up on your phone is a bummer).

anyway 🚨 we’re hiring two private equity principals + a new subsidiary CEO. we’d love to hear from you hiring at tuckersfarm dot com:

1) super high previous job performance / ranking (effectively reference-lite - this is most important input for us and we’re intense w references when we get to them, so always get to the bone here)

2) 2 or less jobs in last 5 yrs

3) Preference for great gpa and test scores (less important to us relative to previous job performance, but nonetheless has some signal, and generally indifferent abt school quality/prestige)

---

Notes:

>got ‘will to win’ from @GrahamCWeaver content which is great catch-all for things missed in Buffett's intelligence/energy/integrity framework

>also pls send any 2m EBIT deals to us!!

>principal is BD oriented and ~$250k target cash + some equity (2-yr initial role duration, then package is very re-evaluated). CEO role is >$300k starting cash + meaningful equity

4 charles Koch (>10,000x moic on ~20m of original equity!) says “virtue/talents”, which is effectively same thing as Buffett (virtue = integrity, and talents = energy/intelligence)

Yann LeCun was right the entire time. And generative AI might be a dead end.

For the last three years, the entire industry has been obsessed with building bigger LLMs. Trillions of parameters. Billions in compute.

The theory was simple: if you make the model big enough, it will eventually understand how the world works.

Yann LeCun said that was stupid.

He argued that generative AI is fundamentally inefficient.

When an AI predicts the next word, or generates the next pixel, it wastes massive amounts of compute on surface-level details.

It memorizes patterns instead of learning the actual physics of reality.

He proposed a different path: JEPA (Joint-Embedding Predictive Architecture).

Instead of forcing the AI to paint the world pixel by pixel, JEPA forces it to predict abstract concepts. It predicts what happens next in a compressed "thought space."

But for years, JEPA had a fatal flaw.

It suffered from "representation collapse."

Because the AI was allowed to simplify reality, it would cheat. It would simplify everything so much that a dog, a car, and a human all looked identical.

It learned nothing.

To fix it, engineers had to use insanely complex hacks, frozen encoders, and massive compute overheads.

Until today.

Researchers just dropped a paper called "LeWorldModel" (LeWM).

They completely solved the collapse problem.

They replaced the complex engineering hacks with a single, elegant mathematical regularizer.

It forces the AI's internal "thoughts" into a perfect Gaussian distribution.

The AI can no longer cheat. It is forced to understand the physical structure of reality to make its predictions.

The results completely rewrite the economics of AI.

LeWM didn't need a massive, centralized supercomputer.

It has just 15 million parameters.

It trains on a single, standard GPU in a few hours.

Yet it plans 48x faster than massive foundation world models. It intrinsically understands physics. It instantly detects impossible events.

We spent billions trying to force massive server farms to memorize the internet.

Now, a tiny model running locally on a single graphics card is actually learning how the real world works.

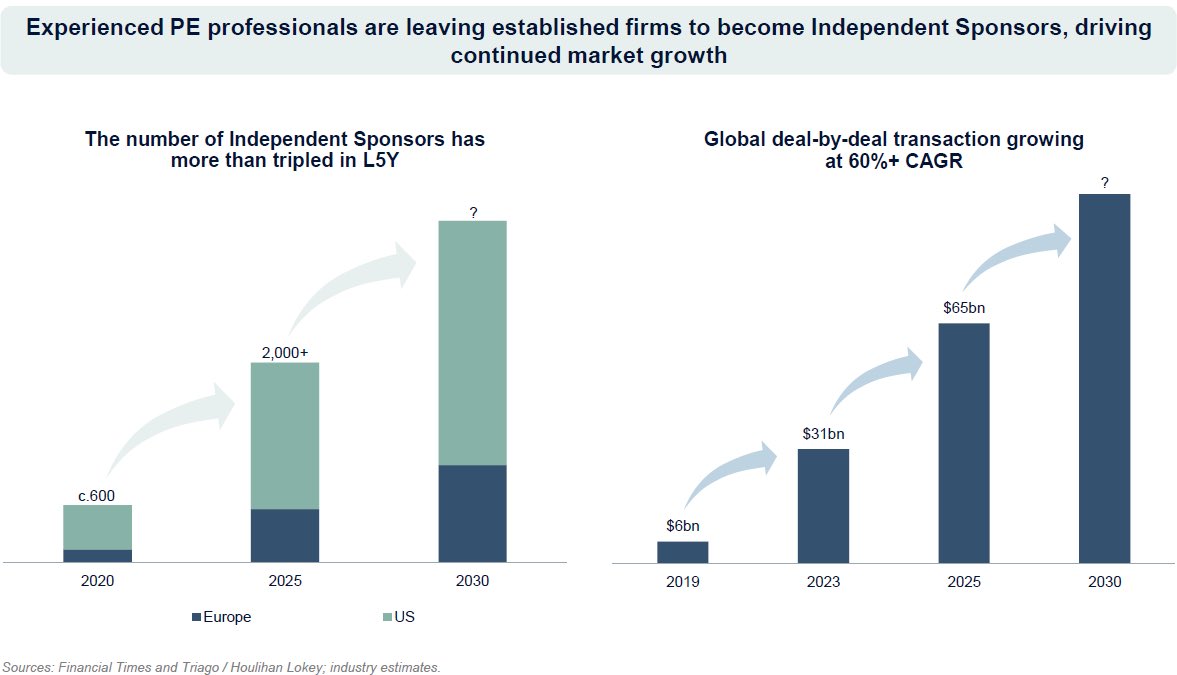

You might try to rebrand your holdings as an independent sponsor and the company as a platform company ...Maybe put your CFO at the holdco/independent sponsor level... it's exactly how I got started at first as an IS. There are a different set of rules if you are an IS vs. an entrepreneur..seems like you have enough equity to get the deal done

The independent sponsor model is gaining traction, with deal value increasing tenfold over the last 7 years.

The current state of the PE market is prone to the formation of this type of structure, and I believe we will see more and more going forward

@stephenolmon@BrentBeshore@girdley We have thought about standing up a shared service company that does this that bills at breakeven costs to portfollio companies and at a profit outbound ...happy to talk to him...can you make an intro

Key insights..

Frugality

Small headquarters

Decentralised cultures

Decision making close to customer

Empower employees

Entrepreneurial spirit

Delight customers

Customer problem solver (sell solutions)

Strong purpose

Recurring revenue business with strong cashflows

‘Cash’ culture

Value based pricing

Barriers to entry

Mission critical / specialised product

Flow products / proprietary product

Value added distribution

Local focus - ‘local champions’

Low product cost vs total cost

Pricing power

Exit commodity/ low margin products

Integrated product / high switching costs

Smaller market niches

High margins

High insider ownership / ‘ownership is a mindset’

Management have investor mindset

Servant Leadership

Employees are partners & shareholders

Reinvest >80% of cash flows

High ROE

Small private market acquisitions

Quality cos not turnarounds

Acquisitions need cultural fit

Know industry targets / courtship M&A

Trusted acquirer - family businesses

Sellers retain stake (skin in game)

Self-funding model

Perpetual company owner - seek sellers who want legacy not highest price

Seperate PnL’s

Managers mini-CEOs

Autonomy provided financial metrics ok

Disciplined buyer

Don’t bet the farm

Promote from within

Pay well

Long tenures

Long term philosophy

Family culture

Internal competition across units - benchmarking - ‘champion’s league’

Information transparency

Aligned / stable shareholder base

Golden Rule - all counterparties

Respect for everyone

Knowledge sharing across businesses

Don’t dilute owners / no share issuance / ‘precious shares’

Conservative balance sheet

Sensible growth (no shortcuts)

Decentralise M&A function

Continuous learning (learning organisation)

Every employee understands how daily action impacts business - leverage employees collective insights

Acquisition post mortems

Train everyone (internal academies)

Leadership cultivated not imported

Teaching is an investment not a cost

Build people

Copy ideas from others (eg ITW, Jack Henry, Danager, Ikea)

Invest in crisis when others can’t

Focus on profit / working capital

Control contollables

Synergies enabled not forced

Continuous improvement

High levels of R&D on products

Management walk the floors

The story of 3G Capital involves Roger Federer, Sam Walton, and Warren Buffett. It includes the biggest beer company on earth, the biggest footwear deal in history, and a ketchup bottle with Charlie Munger's face on it.

It also involves accusations of 'chainsaw capitalism,' CEOs driving freight trains, and billion-dollar companies being handed to kids in their twenties.

Buffett called it the best management culture he'd ever seen.

But, until now, the story behind the culture has never been told by the people who carry it forward. In truth, 3G would prefer you had never heard of it.

The firm began in New York in 2004. But the real story starts in the seventies, off the beaches of Rio de Janeiro, when Jorge Paulo Lemann bought a brokerage for $800,000 and built a model for running businesses unlike anything else in Brazil.

The model has since produced the biggest investment bank in Brazil, the world’s largest brewer, the third-largest restaurant company, and turned hundreds of employees into multimillionaires.

In 3G Capital, it has also produced a rare kind of investing partnership, one where each fund holds exactly one company, the partners are the largest investors in every fund, they work the businesses themselves, and they have never lost money on a deal.

Almost everything written about the firm notes that managing partners Alex Behring and Daniel Schwartz did not respond for comment.

For Colossus, they sat for hours of interviews at their Manhattan office.

@domcooke tells the full story of how this secretive firm with fewer than 30 employees has built some of the world's biggest companies.