@realroseceline Hard to go out of business when you’re expecting to earn $12 billion profit this year. Should probably buy shares if you like the building as that’s the closest you’ll get to owning it $CRM

Historically, semis were priced as a cyclical industry. As margins peaked, P/S ratios would fall.

Over the past year, though, semi multiples have exploded as margins hit all-time highs.

Either the industry has become less cyclical OR it is a sign of exuberance.

Netflix $NFLX is down another 6% today and fast-approaching a 50% drawdown. Fresh multi-year lows, now back to late 2024 levels. Market cap is back down to $300 billion. Where to next?

13 of the 20 worst-performing stocks in the S&P 500 this year are software and related services companies.

The market is treating AI as an existential threat to large parts of the software industry.

Opportunity or value trap?

$ADBE Adobe’s PE is very cheap (below 10x) and the buyback authorization is more than 30% of its market cap, but the earnings report Thurs night fed right into the bear thesis on legacy software (which contends that companies will either cede market share to new AI competitors or be forced to sacrifice revenue in defense of their franchises – Adobe went with the latter option).

And we’re off and running with a $2.2T valuation for a perpetually cash burning company

I’m old enough to remember hucksters saying this market was nothing like 1999… after all, that was a market characterized by tons of money pouring into profitless IPOs, right?

This is the best analysis you’ll read on Twitter about $ADBE ⬇️

The long I initiated yesterday and doubled today - still a small position - is based on the premise that if the market has in fact become too pessimistic about $ADBE future by pricing it at 8x FY26 EPS, there is a lot of upside.

As @realroseceline writes there is a lot of uncertainty. He puts it in the “too hard” pile. There always is: “Predictions are hard - especially about the future.” I certainly don’t know how it will play out. But I’m more than happy to take a small position at this price because the risk/reward feels compelling to me.

We’ll see what happens….

Thoughts on $ADBE

$ADBE is one of the most fascinating stocks in the market today because it highlights one of the most important lessons in investing. It continues to execute at a high level. Revenue continues to grow, margins remain exceptional, free cash flow is enormous, and millions of customers still rely on $ADBE products every day. Yet despite all of that, the stock has struggled for years hitting all time lows.

This confuses many investors, especially newer investors. They look at the financial statements and see a business that appears healthy. Then they look at the stock price and assume the market must be making a mistake. After all, if the business is improving and the stock is falling, shouldn’t that create an even better opportunity?

Sometimes the answer is yes. Some of the greatest investments in history occurred because the market became too pessimistic about a business whose future remained bright. But it is important to remember that the market is not trying to value what a company earned previously or even currently. The market is trying to value what that company might earn in the future.

This is where the story becomes interesting. $ADBE looked cheaper at $500 than it did at $600. It looked cheaper at $400 than it did at $500. It looked cheaper at $300 than it did at $400. Many investors looked at the declining valuation and concluded that the opportunity was becoming more attractive. Yet the stock continued to fall because investors were not debating the current business. They were debating what the business might look like in the future.

For decades, $ADBE built one of the strongest moats in software. Photoshop, Illustrator, etc became the standard tools used by creative professionals around the world. Entire careers were built around learning Adobe’s products. Millions of designers, marketers, photographers, and video editors integrated $ADBE into their daily workflow, creating an ecosystem that appeared almost impossible to disrupt.

Then artificial intelligence arrived and changed the conversation. For the first time, images could be generated with a prompt. Videos could be created automatically. Design work that once required years of expertise could suddenly be performed by almost anyone. The question investors began asking was not whether $ADBE remained a great company today. The question was whether $ADBE moat would be as strong five or ten years from now as it was five or ten years ago.

That distinction is incredibly important because stocks are ultimately claims on future cash flows, not current cash flows. Imagine owning a toll bridge that earns $100 million per year. If someone announces that a second bridge will be built beside yours five years from now, the value of your bridge immediately changes even though today’s profits remain exactly the same. Nothing changed in the present, but something changed in the future.

This is why investing can be so difficult. The numbers investors see today often tell a very different story than the future investors are attempting to price. A business can appear healthy while its long term competitive position weakens. At the same time, a business can appear expensive while its future becomes far more valuable than most people realize (ie $PLTR). The market spends surprisingly little time pricing the present and an enormous amount of time attempting to price a future that has not yet happened.

This is also why one of the most dangerous phrases in investing is, “The stock is down but the fundamentals are improving.” Investors have said that about newspapers as the internet emerged, department stores as ecommerce gained share, and cable television as streaming began taking over. In many cases the current business remained healthy long after the future business had already started to deteriorate.

1/2 👇

Stellar quarter from $ADBE but the CFO is leaving so they’re selling it because they think he knows something.

You can now own it for 8x current year EPS guidance. Sold! I’ll be buying tomorrow morning.

If the AI is destroying legacy software narrative is wrong, these stocks can easily double in the next 2-3 years. They’re all screaming buys IMO $IGV

1st Los Altos Spiritual Books Meetup

The Death of Ivan Ilyich by Tolstoy

Sunday June 14 11am-1pm at The Los Altos Library, Orchid Room

@CarpeDiem4477

https://t.co/SO3n15rJoH

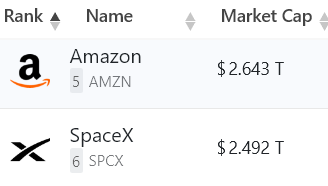

$SPCX Highlights of $1.75 trillion company:

-- 2025 sales $18.7 bn

-- 2025 operating loss $2.6 bn

-- 1Q26 sales $4.7 bn

-- 1Q26 operating loss $1.9 bn

You are cordially invited to take out 2nd mortgage and buy on margin at 93x 2025 sales.

S-1 filing: https://t.co/lczJvzf9oZ