Bruh, when I first tried out ChatGPT around 2023, I thought it LLMs were garbage at coding.

3Y later, Mythos is considered a modern day “nuke” for cybersecurity.

People keep saying humanoids can’t do X or Y task today like plumbing or DC wiring. No sht, but it’s about where things are heading over the few years.

And it’s clear to me and VC apparently that we’ve just hit the inflection point where soon: majority of labor you think is human-only, can be replaced by robotics/humanoids.

You're already seeing this too with internal strategies: Remember $AMZN leaked strat planned to avoid hiring 600,000 workers by them with robots like $CCXI?

If you see past the "assistive robotics" public image framing to prevent protest, it's clear the goals is maximizing, opex efficiency.

The main areas I think are safe however are regulation bound (eg. Medicine), ultra specialized labor, or require human/emotional connections.

But I think you'll be blown away by the rate of change when frontier technologies become national security races between US and China... especially when China is currently in the lead.

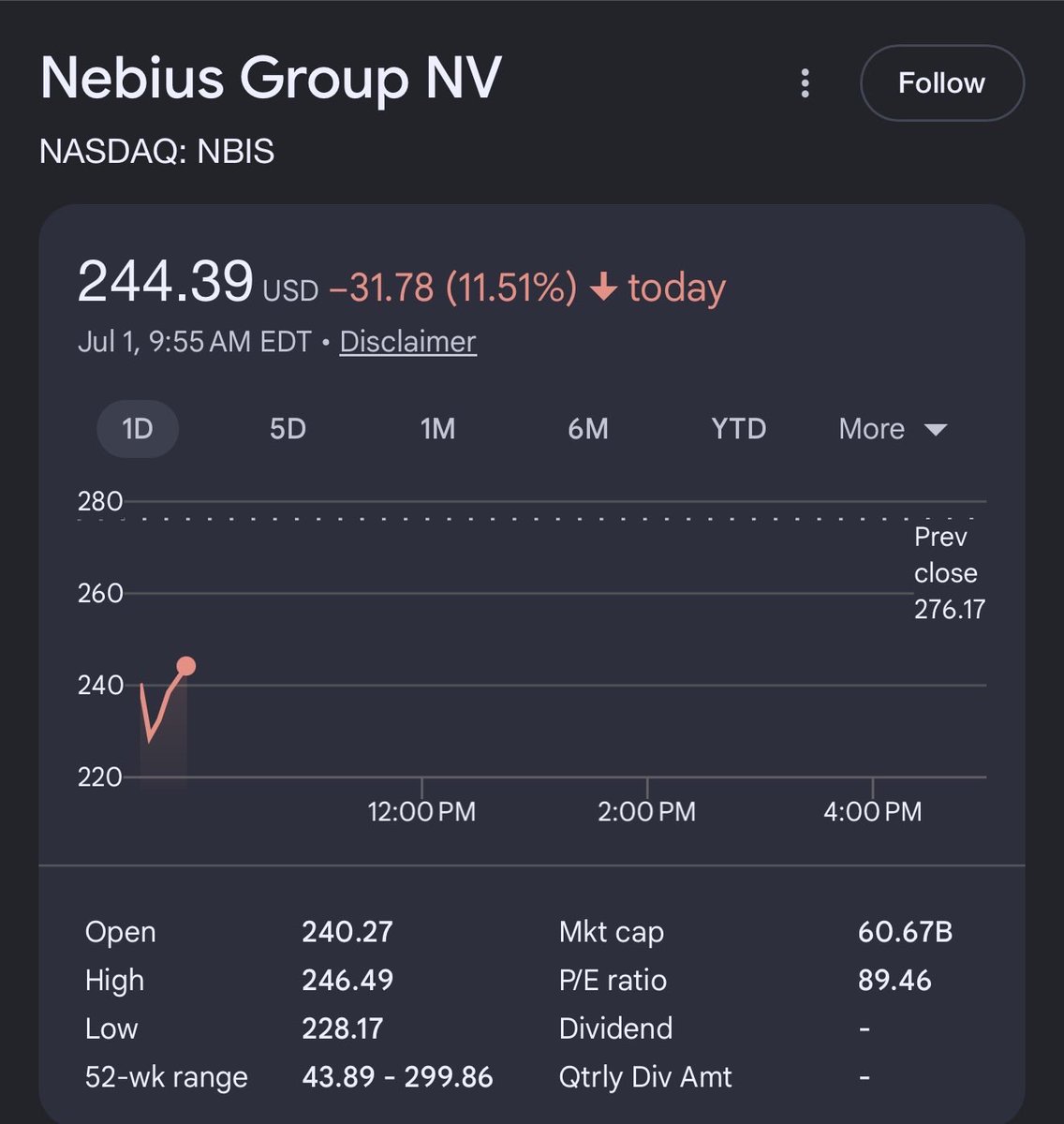

$NBIS dropped 15% today because its biggest customer MIGHT someday compete with it.

Meanwhile there are four or more customers fighting over every single GPU cluster $NBIS brings online.

That is not my take, that is management on the last earnings call. Total power sold out again. Four plus bidders per cluster. The CEO has said the constraint on this business has never been demand, it is how fast they can physically build.

So look at what actually happened today. Bloomberg reported Meta is building a cloud business to sell its excess compute, and the whole neocloud group got hit, $NBIS down 17%, $CRWV down 15%.

But $META is the same company that signed a five year deal with Nebius worth up to $27 billion in March, including $12 billion of dedicated next gen Vera Rubin capacity for 2027.

Why would you pay a supplier $27 billion for future compute if you are swimming in spare capacity. The plans are early, could still change, and Meta itself has not confirmed anything.

And the business underneath the headline is absurd. Revenue up 684% last quarter. AI revenue up 841%. NVIDIA put $2 billion directly into the company and gave them supply priority on next-gen GPUs. Microsoft signed for up to $19 billion.

They just joined the Nasdaq-100. Guidance points toward a $7 to $9 billion annualized run rate exiting the year, and they keep selling capacity before it is even built.

Still up around 150% this year even after today. The story did not change, the tape did.

Fear headline, sold out business, four buyers per cluster. I know which side of that I want to be on.

The market is overreacting to the Meta cloud news, and the irony makes it obvious.

Bloomberg reported $META might sell its excess AI compute, putting it in the same lane as neocloud names, and $NBIS dropped as much as 18% on the fear of a new competitor.

$META is already a $NBIS customer, with a capacity deal worth up to $27 billion. Meta is paying Nebius billions precisely because it cannot build compute fast enough on its own.

If Meta had endless spare capacity to sell, it would not be handing Nebius $27 billion to build more. The selloff is punishing Nebius over competition from the same company funding it.

This sector exists because demand for AI compute massively outstrips supply. Nebius grew revenue 684% last quarter and keeps selling capacity before it is even built.

They cannot build fast enough to meet the demand already signed, let alone worry about a competitor that has not launched anything.

This is a report of plans, not a product. Meta reselling leftover compute someday does not change the fact that the market is starved for compute right now.

100% what I thought.

The word "excess" triggered all algos and made the bears get excited.

We are insanely capacity constrained so this wording is ridiculous.

What it really means is that $META figured out their internal ROI on capacity is lower than the profit they make from selling it to other companies because DEMAND IS SO HIGH!

free -17% dip imho

The lawsuit against 3 memory makers is so dumb. It shouldn't effect the price unless you are a scared buyer.

1) Anyone can sue anyone. Means nothing unless you have the top hyperscaler suing. Of course hyperscaler won't sue because it wouldn't hold up in court, and they would pay in additional damages.

2) Multiple factories are coming up for MU and other makers next year.

3) This morning the korean memory maker announced 500b investment.

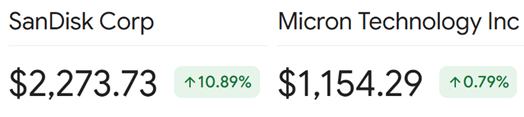

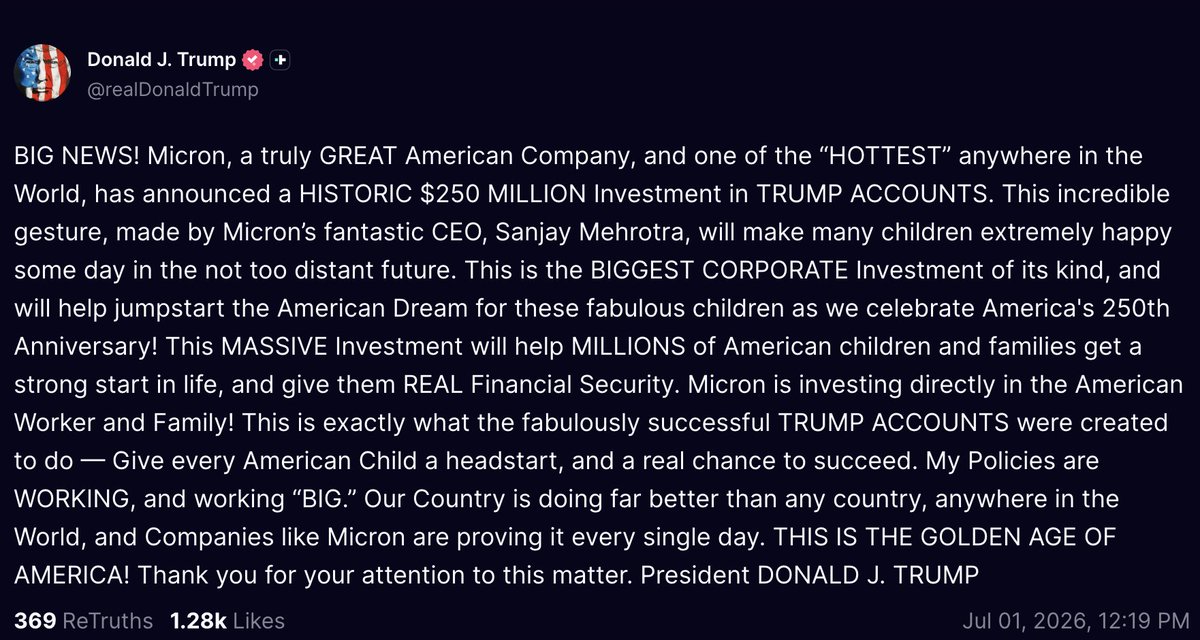

$MU

🇰🇷 SOUTH KOREA DECLARES AI AN "ALL-OUT WAR" WITH A $518B PROJECT

President Lee says the global AI race is now a battle between nations, warning that “speed is the only way to survive.”

Samsung and SK will each build two new chip fabs, part of a combined ₩800T, or $518B, AI push.

South Korea also plans to double DRAM capacity, build 18.4GW of AI data centers by 2035 and spend ₩30 trillion (19.4B) on next-gen memory.

The Kospi erased a 3.4% drop after the plans were unveiled.

$MU $DRAM $SNDK Five types of idiots showed up today on X.

Type 1: Thinks this memory rally is driven by $AAPL, consumers and iPhones. This rally has nothing to do with consumers. Nothing to do with iPhones. Zero. Nada. This is an AI data center infrastructure cycle.

Type 2: Still thinks DeepSeek kills memory demand. We settled this months ago. Move on.

Type 3: Thinks Trump will approve Chinese memory into the US supply chain. National security exists for a reason. Apple will never risk its ecosystem on Chinese silicon. It's a negotiation tactic. Not going to work on structural AI demand.

Type 4: Thinks 40% of DRAM demand comes from OpenAI alone. Wrong.

Type 5: Thinks TurboQuant reduces memory demand 6x. Where did that narrative go?

If $SNDK, $MU and SK hynix are down today because of the China FUD, then I don’t know what to say. It’s just stupid lol.

Long $SNDK, $MU and SK hynix as always.