@pete_rizzo_ i don't think CZ knows much about classical, nor quantum cryptography, so that's generic speculative chit-cat from a non-cryptographer. similar grounding to a guy on the street speculating about the future of faster than light travel.

THE BIGGEST BITCOIN TREASURY COMPANY ON EARTH MAY BE ENTERING ITS MOST DANGEROUS PHASE YET.

Strategy is now facing the exact pressure that could eventually force it to sell Bitcoin.

STRC crashed to $82.53 yesterday, down more than 17% from the $100 price it is designed to hold.

STRC is the financial product Michael Saylor created to raise cash and buy more Bitcoin.

Saylor has said he designed it using ChatGPT, and that the AI told him no one in the history of finance had ever built an instrument like it. It was legal, it was reasonable, and no one had ever had a reason to build it before.

For months it worked exactly as ChatGPT planned. It traded in a tight range near $100 and paid an 11.5% annual dividend. Then Bitcoin started falling.

Bitcoin is now near $62,000, down more than 5% this week. Strategy holds 846,842 Bitcoin, worth around $53 billion at current prices.

As Bitcoin falls, confidence in STRC falls with it, and the price has dropped far below the $100 it is supposed to hold.

Here is what that 11.5% dividend actually costs in real money:

1. Strategy has roughly 104.9 million STRC shares outstanding.

2. At $11.50 per share every year, that is about $1.21 billion a year they owe just to STRC holders.

3. That amount is paid out in cash every 15 days.

Strategy has paused its entire STRC fundraising program.

Here is why that decision costs them directly:

1. If they need to raise $500 million and STRC trades at its $100 par value, they have to issue 5 million new shares.

2. At the current price of $87, raising that same $500 million takes about 5.75 million shares instead.

3. That is 750,000 extra shares created for the exact same amount of cash, and every one of those shares still carries the full $11.50 dividend obligation forever.

Selling below par does not just raise less money, it permanently increases how much cash they owe every year for the same dollars raised. That is why the machine has been switched off completely.

There is already a warning sign of what comes next.

In late May, for the first time since 2022, Strategy sold a small amount of Bitcoin, 32 coins for $2.5 million, specifically to cover STRC dividend payments.

Here is what it would look like if that became the normal way to pay the dividend instead of a one time event:

1. The full annual STRC obligation is about $1.21 billion.

2. At Bitcoin's current price of $62,000, covering that entire amount through Bitcoin sales alone would require selling roughly 19,516 Bitcoin a year.

3. That is more than 600 times the 32 coins they sold in May.

4. It is still a small fraction of their 846,842 total holdings, but it is the difference between an isolated decision and a recurring habit.

It broke the single rule the entire company was built on. Strategy does not sell Bitcoin.

So is Strategy actually in trouble right now?

No.

STRC ranks below their debt, holders cannot force the company to pay, and the dividend can be reduced or skipped at any time. The balance sheet is not collapsing.

But the pressure point is clear.

The dividend rate has already been raised from 9% to 11.5%. Every 0.5% increase on 104.9 million shares adds about $52.45 million a year to what Strategy must pay out.

From here, Strategy has three options, and all three lead to the same place:

1. Raise the dividend rate again to defend the price. This directly increases the cash obligation.

2. Keep funding the dividend by selling Bitcoin. This breaks the one rule the entire company was built on.

3. Issue new STRC shares below $100 to raise cash. This locks in a permanently higher dividend bill for less money raised.

Every option leads back to the same requirement: Bitcoin has to go up.

Israel of 2026 is not the Israel of the Bible.

They’re not Gods chosen people.

Those people believe in Jesus.

Those Jews converted to Christianity.

Jews wrote the New Testament and they don’t believe their own people.

Grok: The **greenshoe option** (also called the over-allotment option) lets IPO underwriters sell up to 15% more shares than originally planned. It stabilizes the stock price if demand is strong by covering short positions without extra risk.

Named after the first company to use it: Green Shoe Manufacturing (now Stride Rite) in the 1960s.

The green shoes in the photo? Pure pun on the term.

THESE 3 WHALES JUST BOUGHT $100M OF ETH

3 whale addresses (2 of these being fresh addresses) just withdrew a total of $122.29M ETH from FalconX and Kraken.

The address that bought ETH previously, is currently down $9.1M on its past buy. Is this Tom Lee?

JUST IN: 🇺🇸 Former President Joe Biden's son, Hunter Biden, says "fiat is a sham, the banking class is corrupt."

"Decentralized digital currency and the blockchain are the inevitable future."

⚡️ UPDATE: CryptoQuant CEO Ki Young Ju says Bitcoin could be closer to $22,000 today if Michael Saylor and ETFs hadn’t absorbed the 1.24 million BTC sold by OG whales over the past two years.

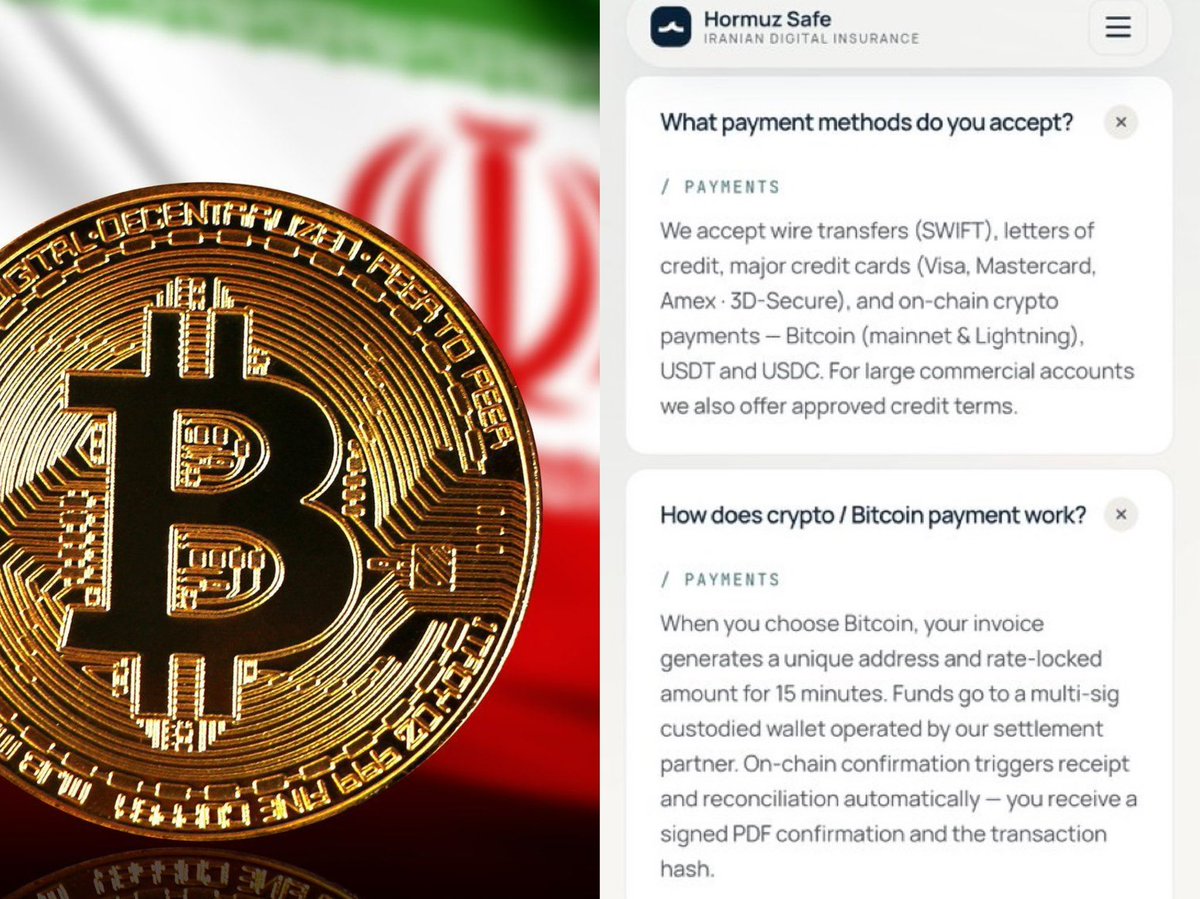

JUST IN: 🇮🇷 Iran is accepting Bitcoin payments on the Lightning Network from ships passing through the Strait of Hormuz.

Permissionless.

Censorship resistant.

32 coins. $2.5 million. 0.0038% of the stack.

That is the sale the market is now blaming for a $3 billion liquidation cascade and a Bitcoin price nearly halved from its peak.

A $2.5 million sale cannot move a trillion-dollar asset. It is a rounding error. In the same week, Strategy raised $128.3 million selling its own stock, 50 times larger. It did not need to sell coins. It chose to. The crash has real drivers: a record 13-day run of ETF outflows, a rotation into AI, a Fed in no hurry to cut. But the accelerant the market keeps naming is 32 coins.

The coins were never the point. The signal was.

And the signal was deliberate. Michael Saylor told the Q1 call he would “probably sell some bitcoin to pay a dividend just to inoculate the market and send the message that we did it.” His logic was sound: prove the Bitcoin is usable capital, not a vault that can never be opened, and show he is not a prisoner of his own vow. His “never sell” always meant be a net accumulator. He is up more than 170,000 coins this year against the 32 he sold, and he scores himself on one number, Bitcoin per share. By that math, defending the dividend with a sliver was discipline, not distress.

The market read it as the opposite. The dose became the catalyst now blamed for the crash. The inoculation became the infection.

Because what changed was never Strategy’s solvency. It was its identity. The market has stopped pricing a permanent holder and started pricing what the filings always described: a state-contingent allocator now funding its own preferred dividends, at the margin, from the Bitcoin beneath them.

And the buffer is thinning. The cash reserve behind those dividends has fallen from $2.25 billion to $900 million. Against a preferred bill near $1.7 billion a year, that is roughly 6 months of runway.

Be precise. This is not a death spiral. Strategy still holds 843,706 Bitcoin, worth more than $50 billion even now, and has more funding levers than almost any company alive. A real rally makes this a footnote, and the sell-side calling the reaction overdone is not wrong on the fundamentals.

But the regime has changed. The question is no longer Bitcoin’s price on any given day. It is the cadence of the dividend declarations and the path of that reserve.

Bitcoin did not acquire a yield. The wrapper acquired liabilities. This week the market learned that difference costs far more than 32 coins.

$BMNR will issue $300 million in preferred shares. Borrowing a page from @Saylor's Ponzi playbook, @fundstrat will offer a 9.5% yield to raise money to buy more Ethereum. But with $MSTR's preferred yielding over 12%, and $ETH tanking, this offering will blow up on the lauch pad.