- $AAOI at $12B

- $SIVE at $2B

- Foci at $2.8B

- Shunsin at $2B

Usually the best risk/reward to me currently. Lot of my answers before like $AXTI already 10x’d, so different lineup this time.

$AAOI due to absurd H1 2027 revenue projections from capacity ramp, doing everything from laser fab to assembly in America.

$471M/month… that’s in 2027, the TAM increases exponentially in 2028.

$SIVE is also ramping absurdly high, 77% revenue pipeline growth of the entire company’s history to ~$799M

Primarily from photonics… in a single quarter. And they’re projecting 60% gross margins off that.

Foci - $NVDA / $TSM primarily FAU supplier and bottleneck for COUPE. Genuinely not sure how this is $2.8B.

BOM share for their passive components + FAU are massive in 2028. Just a bit early H1 2026.

Shunsin - Legit you see Foxconn get CPO/photonics related orders over and over for $NVDA and others.

Just nobody knows the packaging/testing gets done by Shunsin.

A lot of contracts are also under Shunsin’s subsidiary too.. so markets/algorithms don’t know what’s coming imo.

Runner up is $XFAB, they’ll probably be central to EU CHIPS act 2 for silicon photonics at ~$1.5B MC.

And of course SiC/GaN foundries should go brr with 800vdc push by Nvidia.

Especially if they’re the only high volume one in United States per Dpt. Of Commerce.

And it’s such a low price/book ratio so you’re kinda getting the company upside for free, while US Gov/EU Gov subsidize their capex.

Holy crap, this is the most bullish thing I’ve heard from $SIVE so far.

From earnings transcripts:

“We do not look at competitors when demand far outstrips supply” (literally anything they make gets bought)

Along with: “We see 60% gross margins in the future” (incredibly high)

“We have two technologies that can feed into these three supercycles that are currently going on.” (Holy revenue opportunities)

My high conviction CPO/photonics long is $SIVE for a reason.

Just in case people are wondering about my track record with European equities:

$RPI: $280 -> $800 (agentic AI hardware demand thesis).

$LPK: ~$6, thesis at $13 -> $24.2 (glass cores substrates close monopoly)

$SOI: $44 -> $181 (silicon photonics, monopoly over substrates)

$SIVE: $4 -> $71 (CPO, critical chokepoints over lasers).

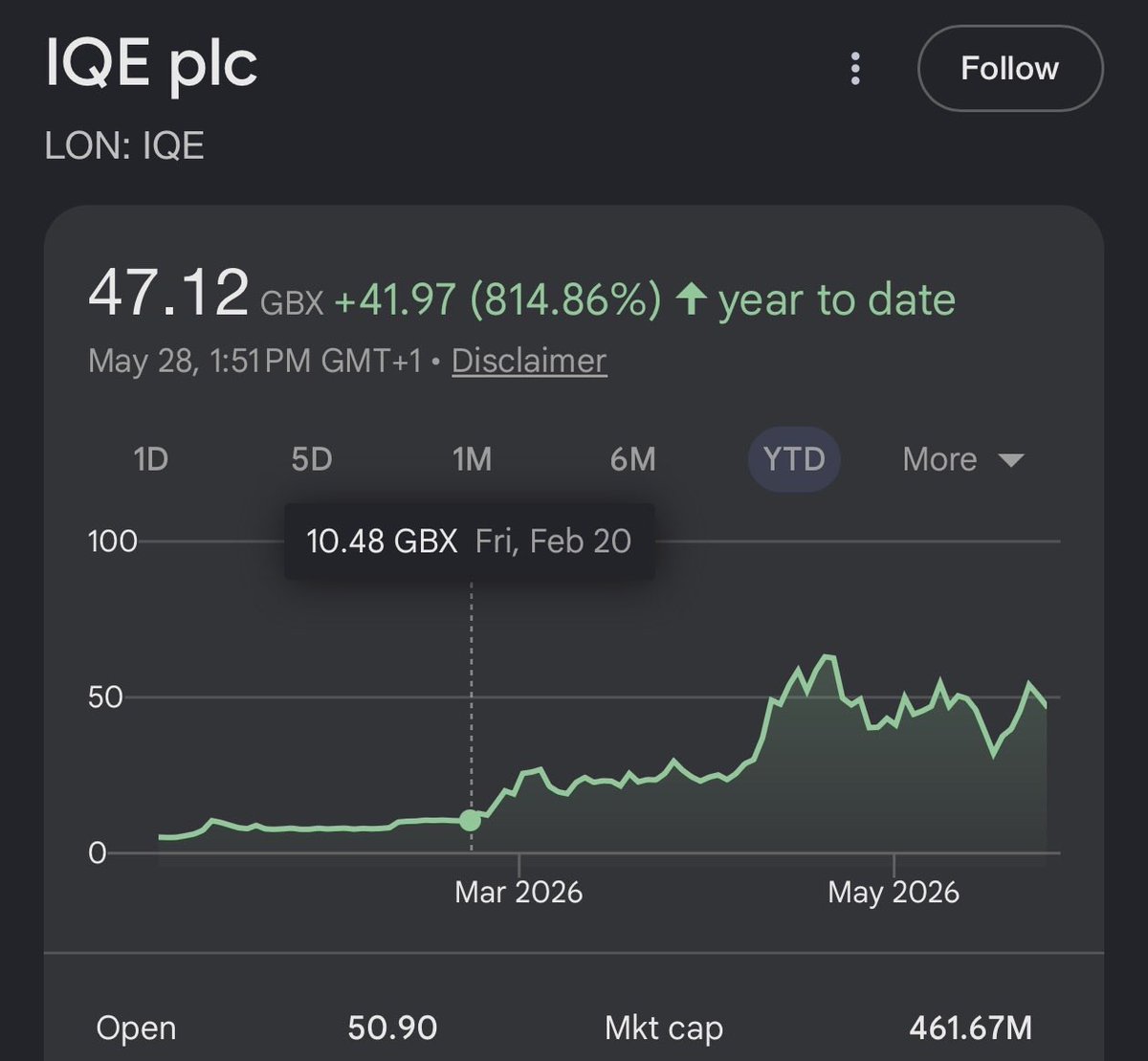

$IQE: $12 -> $47 (latent epiwafer capacity, information discovery around downstream photonics companies).

$ALRIB: $5 -> $15 (duopoly, synthesis around quantum buyers with photonics growth verticals).

And now $XFAB at $9.

I’m not always right.

But every single one of my European longs thesis have been validated so far by either earnings, investments (eg. $MTSI in IQE) or market returns.

$XFAB (photonics + power semis) is an interesting long idea at $1.28B MC, that I took positions in.

Given EU CHIPS act 2 is today as the catalyst for European photonics players.

> 800 VDC power semi exposure to $NVDA push through $NVTS + $POWI

> Silicon Photonics / CPO exposure with $NVDA as evaluation stage for high volume manufacturing (optical transceivers/switches)

> The only high-volume SiC foundry in the US.

> One of the critical MEMS foundries

> ~1.29 P/B, which was around what $SOI was sitting at when I went long. Depressed valuations due to legacy drag

> ~6.5-8.5 fwd p/e 2028 personal est.

> backstopped by Government:

- EU CHIPS act, $128M Euros

- US CHIPS act $50M PMT (department of commerce).

With likely more coming (just signals critical importance to Western supply chains).

So at a certain point with all the grants, they’re just getting the capex funded by the Governments.

EU CHIPS act 2 is coming out this week, and I’m gonna go ahead and guess $XFAB might get included given they were before, and this package is specifically targeting photonics.

~$1.3B MC seems compelling to me if it can pull a Soitec reversal (low p/b, very high growth segments, auto legacy drag).

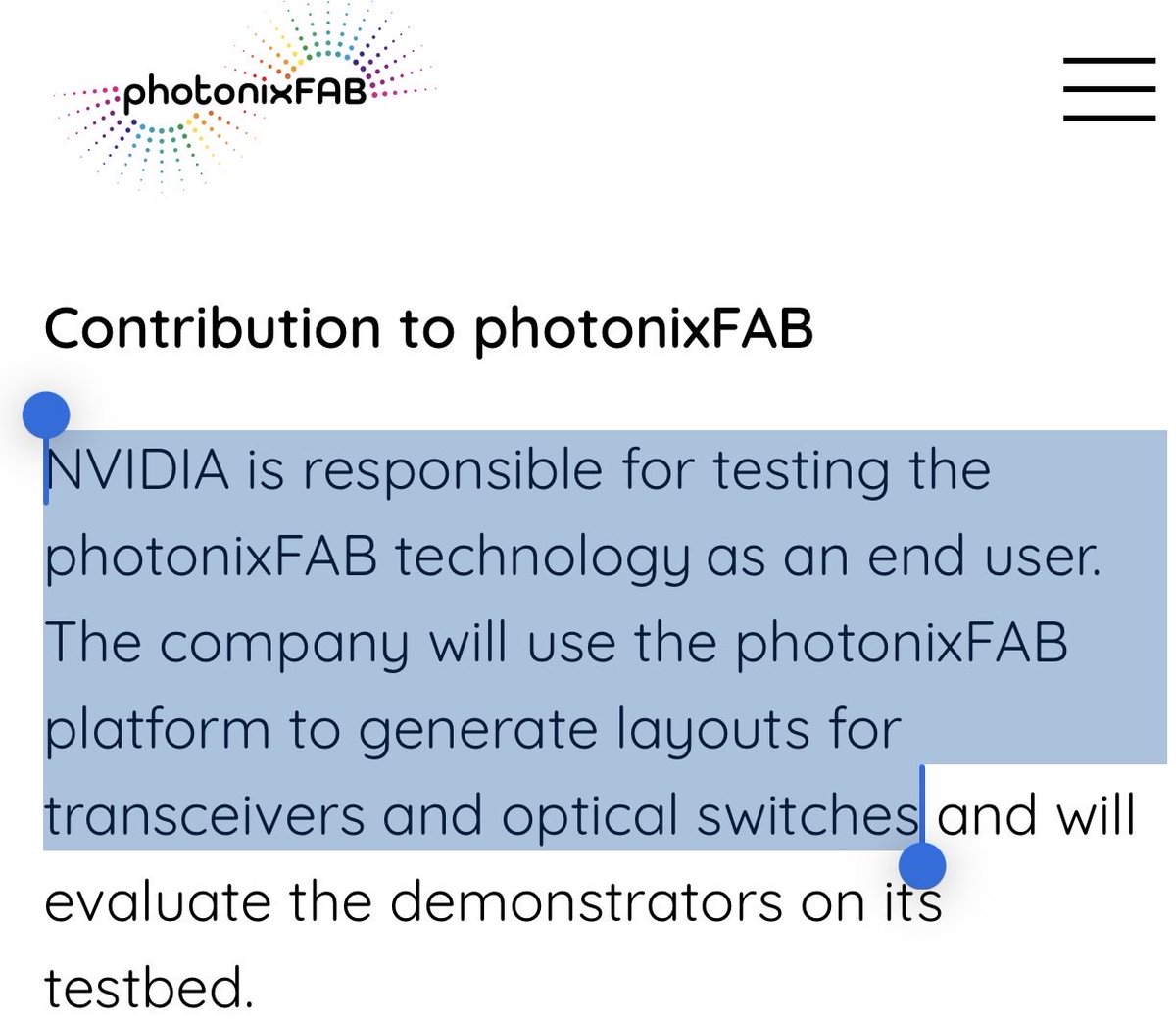

As for the $NVDA silicon photonics relationships it’s under “photonixFAB”.

Markets probably missed this silicon photonics relationship (like $TSEM when I went long) with Nvidia since XFab leads this… Just under a different name.

For power semis, XFAB is named for SiC + $NVTS. In PCN-22181, $POWI explicitly names XFAB as its foundry.

Given its exposure to power semis and photonics as growth, low P/B, gov backstop (of course dyor, just sharing my personal thoughts)

Thought it personally seemed compelling.

I’m just going to leave this here with $AXTI.

100% of the comments were negative when I posted at ~$13.

And I got banned later after it went up 10 times.

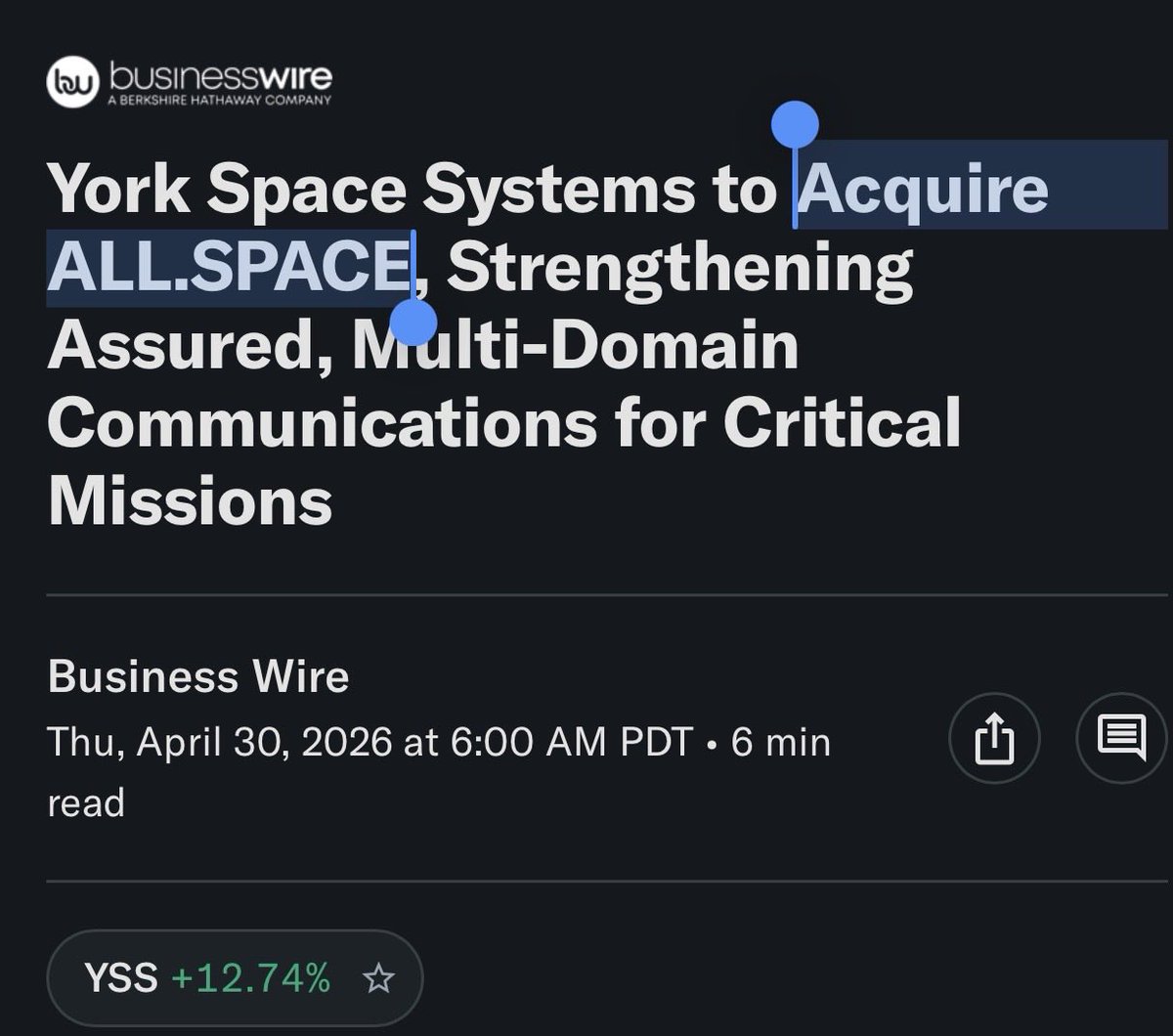

If you’re curious why $SIVEF is up even more today.

$SIVE, as a CHIPS act recipient:

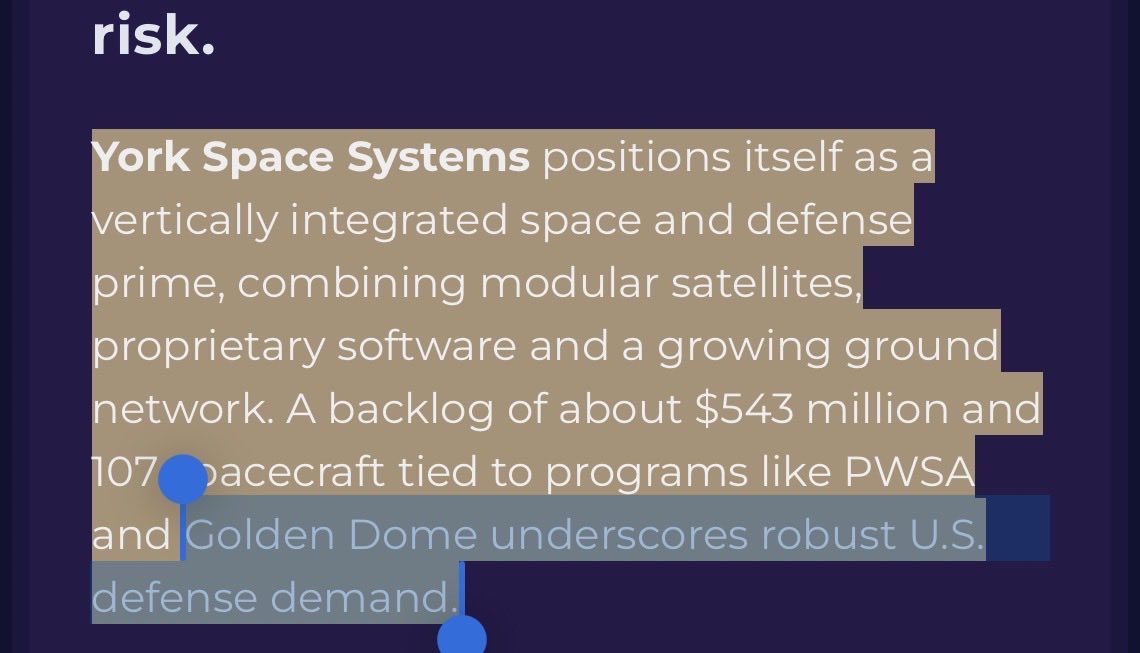

Now likely powers the Golden Dome.

As the upstream semi supplier since Sivers’ lead customer ALLSPACE got acquired by $YSS.

York happens to be a national defense prime contractor with links to the Space Force, Space Development Agency, DoD, and Golden Dome.

So Sivers, a mini Swedish company, basically got a backdoor to powering the US space buildout.

Just an FYI: I don't need to post something every day about the names I own.

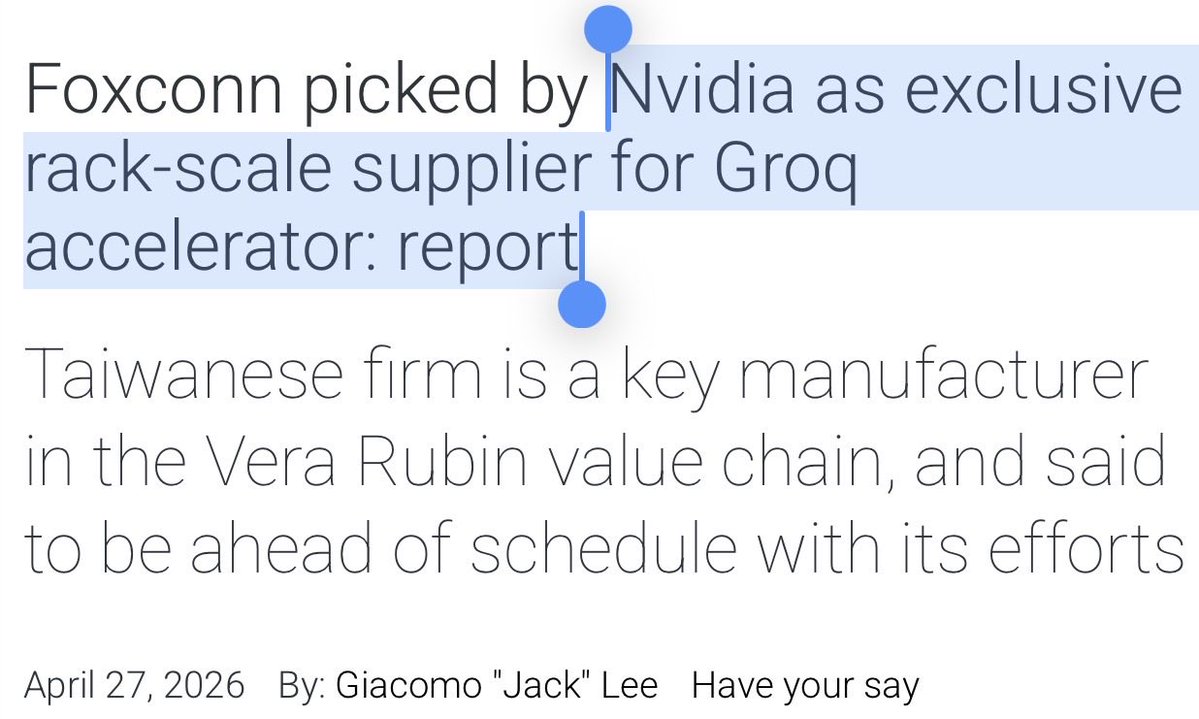

However, I did miss this with Shunsin (6451):

Foxconn picked by $NVDA as exclusive rack-scale supplier for Groq accelerator.

This is highly positive for Shunsin (Foxconn's optical packing arm).

So ShunSin's CPO and optical packaging basically backdoored Nvidia's next-gen supply chain with this news.

Markets just haven't realized this connection yet (and it's on disposition, so frozen for most).

The article explicitly notes that Foxconn is integrating these systems "including ... networking."

Bc Foxconn is the exclusive assembler, they'll vertically integrate and likely use ShunSin's optical packaging solutions into the design, bypassing ShunSin's need for networking contract directly from Nvidia.

This is what I meant by Shunsin is literally a free piggy back ride to $NVDA CPO ecosystem. Foxconn is massive.

And you're getting the leading player in Nvidia's optical supply chain for a lower valuation than $LWLG lol.

Bottom line: not a hype trade, but a high-quality compounder with a more reasonable valuation than before. For patient investors, $ADBE deserves attention.

Adobe $ADBE looks like a long-term buy to me. Revenue is still growing in the low double digits, margins remain elite, and free cash flow is strong. Valuation has cooled vs. its own history, so the risk/reward looks better than it has in a while.

@aleabitoreddit Just to let you know 210k people are here, are ready, loyal soldiers, many joined late, many still dream for a next level investment, you push the thesis & make the call, and we are your catalyst, new heights new possibilties for retail, 100k are in, in that second 🚀

@aleabitoreddit@Lee_Trades Are These all? Do you possibliyhave a list you can share for the new subscribers like me?

$LWLG

$SOI

$ALRIB

$RPI

$AXTI

$AEHR

$HPS.A

$IQE

$JBL

$MRVL

I’m learning that discipline matters more than being early.

Risk management matters more than hype.

And patience matters more than tweets.

That’s the real edge.

#NVDA#Stocks#Investing#MarketPsychology

With $NVDA, the question isn’t “Is AI real?”

It’s:

• Can growth stay exceptional?

• Are expectations already extreme?

• Am I sized correctly?

Great companies don’t protect you from volatility.

They invite it.

If u can’t sit through drawdowns,

u don’t own the stock, it owns u.