@J5jayfive Thoughts on other AI components manufacturers?

$ALAB, $LITE, $AAOI, $VRT?

Why exit from $EWY? They have a great exposure to memory companies.

Interview with a $GOOGL employee who thinks we still have at least five more years of strong capital deployment ahead in the AI buildout:

1. The expert sees the AI data center build cycle as roughly at the halfway point, with the buildout expected to continue through 2035 before the next architectural shift. The current phase is transitioning from training-heavy investment to inference, and the expert sees at least five more years of strong capital deployment ahead. On the shape of spending, the expert expects the composition to shift rather than the total to decline, with heavy hardware investment dominating through 2027 and 2028 before giving way to a larger proportion of software and operational spend as AI becomes more of a commodity.

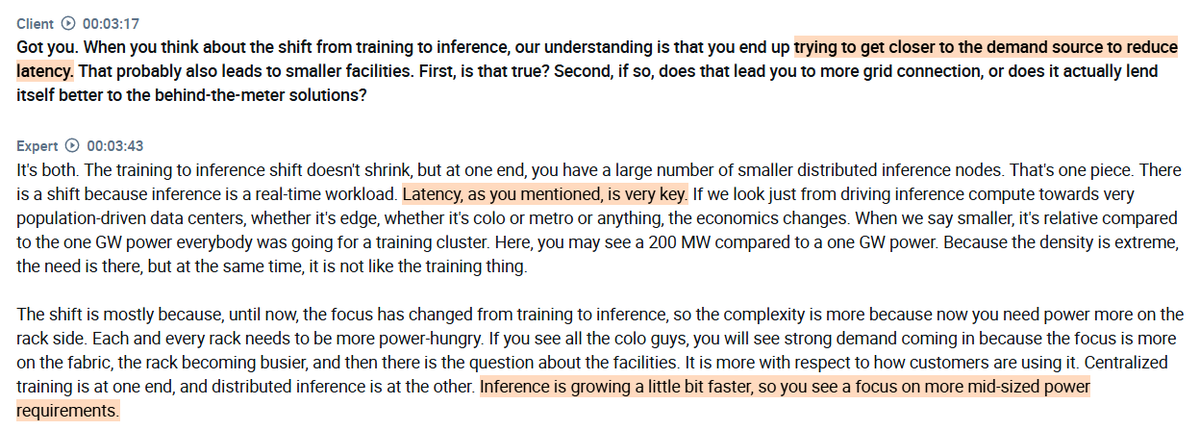

2. He emphasizes that the shift from training to inference pushes compute closer to population centers to reduce latency. Training clusters were chasing 1GW facilities, while inference deployments sit closer to 200MW, spread across colocation and metro sites rather than concentrated in one place.

3. The expert highlights a clear distinction between training and inference from a power design perspective. Training runs at flat, sustained load for weeks, making it predictable but requiring over-provisioned capacity, while inference is spiky and needs capacity available on demand even when mostly idle.

4. According to the expert, hyperscalers would willingly pay a 5-15% premium above the equivalent volume price to secure a shorter-duration PPA, with the logic being that retaining the option to extend, restructure, or walk away after 7 years is worth paying for compared to being locked into a 20-year commitment with no flexibility. The expert sees hyperscalers holding a stronger position in most markets, since power assets without a signed contract generate no revenue, giving hyperscalers leverage in all but the most supply-constrained regions.

5. The expert sees two forces driving the push for on-site power over waiting for grid connections. GPUs are expensive depreciating assets that generate no return when not running, and customer demand cannot wait, with any hyperscaler that fails to deploy quickly risking losing that customer to a faster competitor. In the near term, a small increase in power costs is not a deal breaker, but over a 5 to 10 year operating period that difference compounds, and the expert expects cost efficiency to become a much bigger priority by 2029.

found on @AlphaSenseInc

60% of US data centers slated for 2027 haven’t started building yet, choked by grid delays.

Hyperscalers can't wait 5 years for utilities.

They must build local microgrids. With the KORE acquisition, $TE sits exactly at the mouth of the AI bottleneck.

https://t.co/fWJ7pC5cFd

For years, SBC was a "non-cash" expense that inflated FCF. But with AI CapEx draining reserves, $GOOG $30B IRS bill on employee vesting requires cold cash.

The fix? Diluting shareholders for $85B.

The illusion is now a real cash drain.

OpenAI CFO Sarah Friar says its next major training run this fall will be on $NVDA Vera Rubin platform.

She also said compute remains sold out through much of 2027 with power, land, chips and talent all becoming bottlenecks

It is less about a flaw in global AI fundamentals and more about a textbook, mechanical leverage unwind in a major proxy market that forces global portfolio de-risking.

$TE: ☀️ Quick AI summary on TD ACP note and how BESS deal yesterday is bullish for T1 Energy

T1’s KORE/NRI acquisition looks strategically well-timed because the TD Cowen ACP note frames BESS as moving from a renewables add-on to a mission-critical part of the AI/data-center power stack. The key market need is no longer simply “more megawatts,” but faster, cleaner, more flexible, and more reliable power. BESS helps solve exactly that through PPA firming, peak shaving, backup power, power-quality stabilization, and gas-generation optimization. That gives T1 a path to expand beyond being viewed as a solar module manufacturer into a broader U.S. power-infrastructure platform serving hyperscalers, utilities, and industrial customers facing interconnection bottlenecks, grid constraints, transformer shortages, and speed-to-power challenges.

The most bullish angle is that NRI appears to bring systems-integration and software/control expertise, not just commodity battery exposure. TD’s note emphasizes that complex data-center BESS projects require integration across inverters, UPS systems, generators, medium-voltage equipment, grid interconnection, and real-time controls—areas where experienced integrators can earn higher-value work. If T1 can use KORE/NRI to credibly offer solar plus storage plus grid-interface solutions, the acquisition could both pull through solar demand and open a much larger BESS/data-center infrastructure TAM. The main diligence point is whether NRI has enough technical depth and customer credibility to compete with Fluence, Tesla, FlexGen, Prevalon and other storage integrators, but strategically the deal gives T1 a timely and differentiated entry into one of the most constrained parts of the AI power buildout.

Nebius choisit la France.

L’acteur du Cloud IA dévoile un projet de plus de 8 milliards d’euros d’investissement pour déployer des infrastructures et des services de cloud, avec une capacité cible de 240 MW, positionnant le site parmi les plus puissants du continent.

Bedankt!

Market valuations are detaching from historical reality.

Alphabet sits at a clean ~10x P/S, but look at the infrastructure layer: Micron is trading past 16x trailing sales, and pure-play AI clouds like Nebius ($NBIS) are pushing a staggering 60x+.