A New Era. A New Unit21 🚀

The math of risk and compliance is broken.

Transaction volumes have exploded. Alert queues are overwhelmed. And traditional systems mostly create noise. “More of the same” is no longer a strategy.

A new era of financial crime requires a new architecture to defend against it.

Today, we’re introducing a new Unit21: AI Risk Infrastructure

The Shift

Passive monitoring tools are no longer enough. Most systems simply record the work—they don’t actually execute investigations end to end. They don’t automatically tune your system for better fincrime detection. Until now.

The AI Evolution

AI isn’t just another feature. It’s a new operating model.

We’ve built AI Risk Infrastructure that acts as a force multiplier for financial crime teams.

AI Agents that:

𝗣𝗲𝗿𝗳𝗼𝗿𝗺 𝘁𝗵𝗲 𝘄𝗼𝗿𝗸 — eliminating manual data hunting

𝗦𝗵𝗼𝘄 𝘁𝗵𝗲 𝘄𝗼𝗿𝗸 — providing instant, transparent context

𝗘𝗺𝗽𝗼𝘄𝗲𝗿 𝘁𝗲𝗮𝗺𝘀 — delivering finished investigations, not just alerts

The future of fraud prevention and AML isn’t about how many alerts you generate. It’s about how much risk you resolve—with precision and automation.

A new era is here.

Read more from our COO, Tyler Allen: https://t.co/Wb6pNCpmeg

Transaction monitoring. Market abuse rules. STR filings. Regulator expectations that keep evolving.

MiCA authorized is not the same as MiCA ready.

On June 10, we're bringing together two practitioners who are living this right now for a candid panel discussion on what it actually takes to operationalize MiCA compliance at scale.

Joining the conversation:

↳ Eoin Kearns, Head of Compliance & AML, @moonpay — led MiCA compliance from inception, launched across the EEA, and has spent the last year working directly with the AFM to uphold their commitments

↳ Calley Jansen, Head of Financial Crime Intelligence, @BVNKFinance — on the operational front lines of MiCA: transaction monitoring, market abuse rules, alert efficacy, and governance

Moderated by Emily Garza, Chief Customer Officer, Unit21.

No legal explainers. Just practitioners who've built it, talking honestly about what works.

📅 June 10 | Register → https://t.co/cOKi0pO9eL

Unit21 quietly files roughly 5% of every SAR in America. Most banks have never heard of them.

Our cover story on @unit21inc

https://t.co/jUgGqprwC9 via Yespress

The hardest part about AI agents making payments is not the transaction itself. It’s proving intent, identity, and liability at the same time when there is no human directly pressing the button anymore.

What Tyler said during our conversation stuck with me because the industry is entering a world where fraud detection is no longer just about checking passwords, OTPs, or suspicious IP addresses. AI agents will operate from devices, behave like humans, and in many cases even imitate normal customer patterns better than fraudsters ever could.

That changes the entire risk model.

An AI agent making a payment for me might actually look legitimate because it knows my normal behavior, transaction sizes, merchants, and habits. So the decision engine starts relying less on one signal and more on layered intelligence across device behavior, transaction history, behavioral patterns, and agent detection.

The interesting part is that “this is an AI agent” does not automatically mean “this is fraud.”

It simply becomes another signal in the flow.

@unit21inc

Unit21 was just named a Category Leader by @ChartisRsch and ranked #1 in AI across 40+ fraud vendors.

We earned best-in-class scores in workflow, modeling, case management, and configurability.

If you're evaluating fraud platforms in 2026, this report is worth reading. It maps the market and explains what separates the leaders from the rest.

Download full report👇https://t.co/KfkB7pIYFx

Banks are still fighting AI fraud with yesterday's playbook.

Our CEO Tyler Allen sat down with @samboboev from Fintech Wrap Up Podcast to talk about why that's a problem - and what it actually takes to fix it.

In this podcast, he covers:

↳ Why rules-based systems and ML models aren't enough anymore

↳ How AI agents are changing fraud and AML operations

↳ The future of Know Your Agent and regulatory readiness

↳ Why compliance teams may go AI-native faster than expected

Worth a listen 🎧 → https://t.co/A7cMg9P7Uw

Fraud teams used to spend months building detection logic, tuning rules, and manually reviewing edge cases, but Tyler explained how fast that workflow is changing when AI can now generate and deploy fraud rules from a simple text prompt instead of requiring analysts to understand data models, SQL queries, or complex dashboards.

What stood out to me is that the future of fraud infrastructure may not even look like software people actively use every day. The system quietly runs in the background, monitors behavior, deploys detection logic, flags anomalies, learns from feedback, and only pulls humans in when something truly unusual happens.

That changes the role of fraud teams completely.

Instead of spending hours configuring systems, teams start focusing on oversight, exceptions, and strategy while AI handles repetitive operational work at scale. A company processing millions of transactions per day cannot realistically rely on manual reviews and static rules anymore when fraud patterns shift weekly and attackers already use AI themselves.

The interesting part is that fraud software is slowly becoming less of a dashboard and more of an invisible operating layer for compliance, risk, and decision-making.

@unit21inc

Tyler made an interesting point on the podcast when we discussed AI in fraud protection.

Last year, many financial institutions were still treating AI agents as experiments inside innovation labs. Now more than 50% of financial services companies are already deploying them or actively trying to move into production environments as quickly as possible.

What changed is simple. Fraudsters are already using AI at scale. They can launch thousands of synthetic identity attempts, phishing campaigns, or account takeover attacks in minutes, while traditional fraud teams still rely on workflows built for a slower internet.

The pressure is no longer about whether companies should adopt AI for fraud prevention. The pressure is whether they can adapt fast enough before attackers widen the gap even further.

What also stood out from Tyler’s point was how quickly the market sentiment changed in just 12 months. Moving from roughly 10–20% adoption to the majority of organizations exploring deployment shows how fast financial infrastructure decisions are now shifting once operational risk becomes impossible to ignore.

@unit21inc

𝗬𝗼𝘂𝗿 𝗰𝗼𝗺𝗽𝗹𝗶𝗮𝗻𝗰𝗲 𝗽𝗿𝗼𝗴𝗿𝗮𝗺 𝗯𝘂𝗶𝗹𝘁 𝗮 𝗖𝗥𝗥 𝗺𝗼𝗱𝗲𝗹.

Weighted attributes. Configured thresholds. A score for every customer. And when an investigator opens an alert, they see: High. 82/100. That's it.

They don't see that SAR_VOLUME is carrying 20% of the model weight and scored 100/100 because this customer filed two SARs in the last 12 months.

They don't see that AGE_OF_RECORD scored 0/100 because a 66-month-old account is considered low-risk by your model's configuration.

They see a number. They don't see the reasoning behind it.

So they can't document it. They can't challenge it. And when an examiner asks why a case was escalated, "the CRR was high" isn't a sufficient answer.

𝘛𝘩𝘪𝘴 𝘪𝘴 𝘵𝘩𝘦 𝘱𝘳𝘰𝘣𝘭𝘦𝘮 𝘰𝘶𝘳 𝘊𝘶𝘴𝘵𝘰𝘮𝘦𝘳 𝘙𝘪𝘴𝘬 𝘙𝘢𝘵𝘪𝘯𝘨 𝘈𝘯𝘢𝘭𝘺𝘴𝘪𝘴 𝘵𝘢𝘴𝘬 𝘴𝘰𝘭𝘷𝘦𝘴.

The moment an investigator opens a flagged alert or case, the task automatically surfaces the full attribute-level breakdown: each factor's weight in the model, its individual score, the underlying metric, the raw entity value, and the mapped score. The complete logic chain, already there, before the investigation begins.

𝗔 𝘀𝗰𝗼𝗿𝗲 𝘁𝗲𝗹𝗹𝘀 𝘆𝗼𝘂 𝘄𝗵𝗮𝘁. 𝗧𝗵𝗲 𝗯𝗿𝗲𝗮𝗸𝗱𝗼𝘄𝗻 𝘁𝗲𝗹𝗹𝘀 𝘆𝗼𝘂 𝘄𝗵𝘆.

Edition 03 of AI Task Spotlight is live. Read how it works: https://t.co/FmHz8LflHH

#AML #Compliance #CustomerRisk #TransactionMonitoring

New email. Same questions. Wait. Chase. Screenshot the thread. Upload it manually. Log it in a spreadsheet.

Every compliance analyst knows the drill.

That's not an audit trail. That's just hoping nothing goes wrong before the exam.

We built Request for Information (RFI) to fix it.

From any alert or case in Unit21, your team sends a secure, white-labeled form, sets a deadline, and receives everything back in the platform automatically. Full audit trail. No chasing. No manual uploads.

RFI is live. Read more: https://t.co/6mhWEnSpRz

Tyler made an important point during our conversation that fraud teams are now operating in a completely different environment because AI gives attackers an unfair advantage in scale, speed, and experimentation.

A fraudster only needs one successful hit out of 100 attempts to make money. A bank or fintech cannot afford that same error rate because one hallucinated decline can block a legitimate customer from accessing financial services, trigger compliance issues, or destroy trust instantly.

That is what makes this shift so difficult for financial institutions.

The same AI acceleration helping fraudsters is also giving risk and compliance teams entirely new capabilities. Real-time behavioral analysis, adaptive onboarding checks, AI-driven monitoring, and autonomous investigation systems are moving from experiments into production infrastructure much faster than most people realize.

The question is no longer whether AI can support fraud and compliance operations.

The real challenge is how quickly regulators and financial institutions become comfortable allowing AI systems to participate directly in critical risk decisions while still maintaining accountability, explainability, and accuracy at scale.

@unit21inc

⏰This Thursday, nearly 800 compliance leaders are tuning into this conversation…

FinCEN's NPRM is reshaping what AML program effectiveness actually means - and the comment period closes June 9.

Before it does, join us and American Banker for a live, unfiltered conversation on what compliance leaders need to know.

Joining the conversation:

↳ Sarah Beth Felix, Palmera Consulting - recovering auditor, founder, and AML consultant who's seen this from every angle

↳ Eric Ellis, @FifthThird Bank - former OCC BSA Policy Director who's sat on both sides of the exam table

Spots are still open.

📅 May 28 | 1:00 PM ET

Register → https://t.co/d5kTBjS8Gr

One thing that keeps coming back in conversations around AI agents and payments is that the industry is still thinking mostly about capability, while the harder problem is governance.

An AI agent being able to execute a payment is not the difficult part anymore. The infrastructure already exists. APIs exist. Stablecoins exist. Real-time payment rails exist.

The real challenge starts when an agent makes a mistake, exceeds permissions, gets compromised, or negotiates on behalf of a customer and moves money autonomously. At that point, the question becomes very simple: who is responsible for that action?

That is why Tyler’s point about an “AI agent registry” is so interesting.

Not because registries are exciting technology, but because financial systems have always depended on trusted identity and accountability layers sitting underneath transactions. Merchants have IDs. Banks have licenses. Payment providers have scheme memberships.

AI agents currently have almost none of that structure.

I would not be surprised if companies like Visa, Mastercard, or Stripe eventually become part of this layer because they already sit in the middle of trust, compliance, permissions, authentication, and dispute management across global commerce.

@unit21inc

"Unit21 gives us the flexibility and control to move fast. We can tailor rules, test safely, and scale compliance as quickly as Rippling grows."

Their old compliance stack wasn't built for scale but with Unit21, they got real-time transaction blocking before funds settle, dynamic customer risk scoring, and a single workflow from alert to SAR filing.

Read the full case study → https://t.co/ptYqT2AiAV

In this episode of the WRAP UP Podcast, I speak with Tyler Allen, CEO of @unit21inc, about why AI agents may become one of the most important tools in the fight against financial crime.

Tyler explains why traditional rules-based systems and machine learning models are no longer enough as fraud becomes faster, more automated, and more sophisticated. He also breaks down how AI agents can help compliance and fraud teams review alerts, investigate suspicious activity, reduce false positives, and respond to financial crime in real time.

The conversation also explores the future of “Know Your Agent,” AI-powered fraud decisioning, agent registries, regulatory readiness, and whether financial institutions are ready to trust AI with high-stakes compliance work.

In this episode, we discuss:

- Why financial crime is becoming harder to fight

- How AI is changing fraud and AML operations

- Why traditional machine learning is not enough

- The role of human-in-the-loop reviews

- How AI agents can reduce investigation time

- The future of Know Your Agent

- Whether regulators are ready for AI decision-making

- Why compliance teams may become AI-native faster than expected

Watch the full episode to understand how AI agents could reshape fraud prevention, AML, and financial crime compliance.

The comment period for FinCEN's NPRM closes June 9.

Before it does, we think compliance leaders should understand exactly what's changing, what's cosmetic, and what will actually move the needle in an exam room.

We're joining @AmerBanker for a live conversation on May 28 to break it all down.

Joining the conversation:

↳ Eric Ellis, @FifthThird Bank

↳ Sarah Beth Felix, Palmera Consulting

↳ Neda Shapourian, Unit21

On the agenda: what "effectiveness" actually means to an examiner, how AI earns regulatory credit vs. just providing cover, and how small teams can make defensible risk-based decisions.

Real talk only.

📅 May 28 | PM ET

Register → https://t.co/d5kTBjS8Gr

Most compliance teams think they have watchlist screening covered.

They have ongoing monitoring. Onboarding checks. Maybe a manual process for one-offs.

What they actually have is three vendors, three interfaces, and three audit trails, and when a regulator asks for a consolidated view, they're piecing it together by hand.

That's not a program. That's a patchwork.

A complete screening program covers five moments in the customer lifecycle: onboarding, ongoing monitoring, ad hoc checks, payment screening, and AI-powered investigation. All five. One platform. One audit trail.

We broke down exactly what that looks like, plus a full demo walkthrough so you can see it end-to-end.

📖 Read the blog → https://t.co/YYpBqQC4Nx

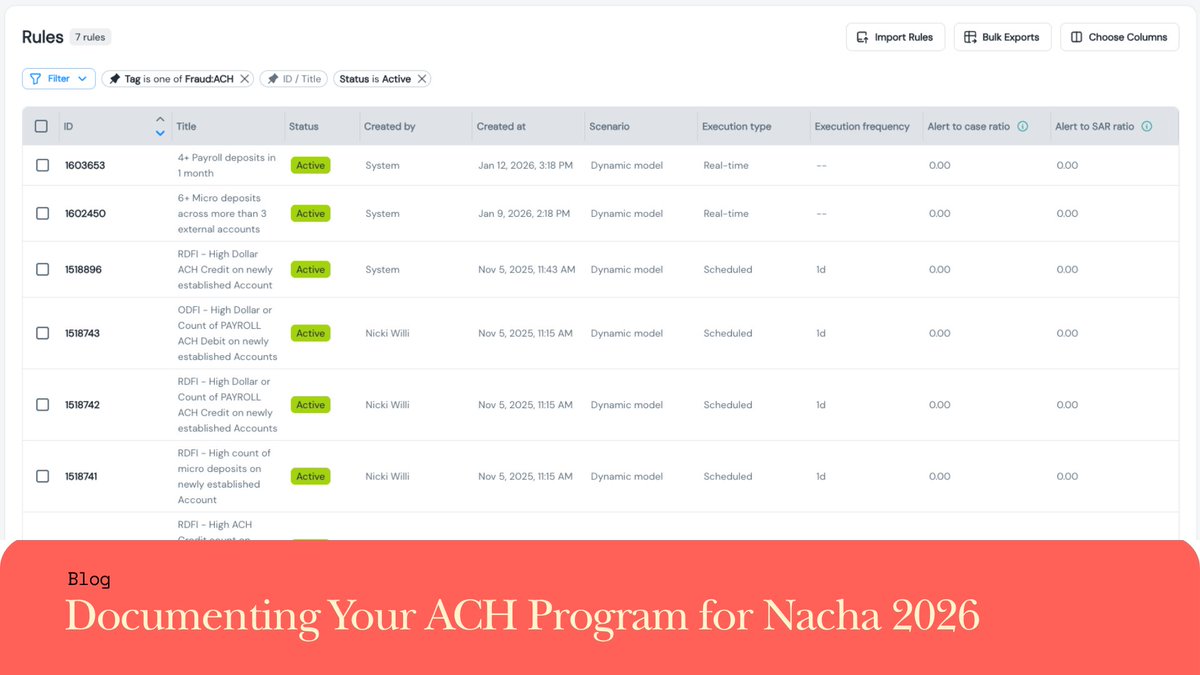

The Nacha 2026 rule changes aren’t just about detection; they’re also largely about documentation.

Investigators can't audit what isn't logged. Examiners don't just look at whether your rules fired. They look at your rule inventory, modification history, performance data, and whether your program shows evidence of continuous improvement.

We just published Part 3 of our Nacha 2026 series breaking down exactly what explainable and auditable documentation looks like and how to build it.

If your team is preparing for the annual assessment, this one's worth a read.

🔗https://t.co/URj4i8dtRy

A lot of great conversations these past few weeks.

From @ABABankers Risk & Compliance in Charlotte, to @acams_aml Kansas City, to @qubevents Payments & Regtech in Barcelona, and Corelation Client Conference in San Diego, one thing kept coming up in every room: financial crime teams are being pushed to move faster without losing control.

AI, regulatory pressure, operational scale, cross-border complexity. The challenges may look different depending on the audience, but the direction is pretty consistent.

Thank you to those who spent time with us across sessions, booth meetings, and conversations over cocktails. Special shout out to our friends at @Equifax for co-hosting our mixer in Charlotte!

A few highlights from the 4 events spanning 7 days and over 6000 miles 📸

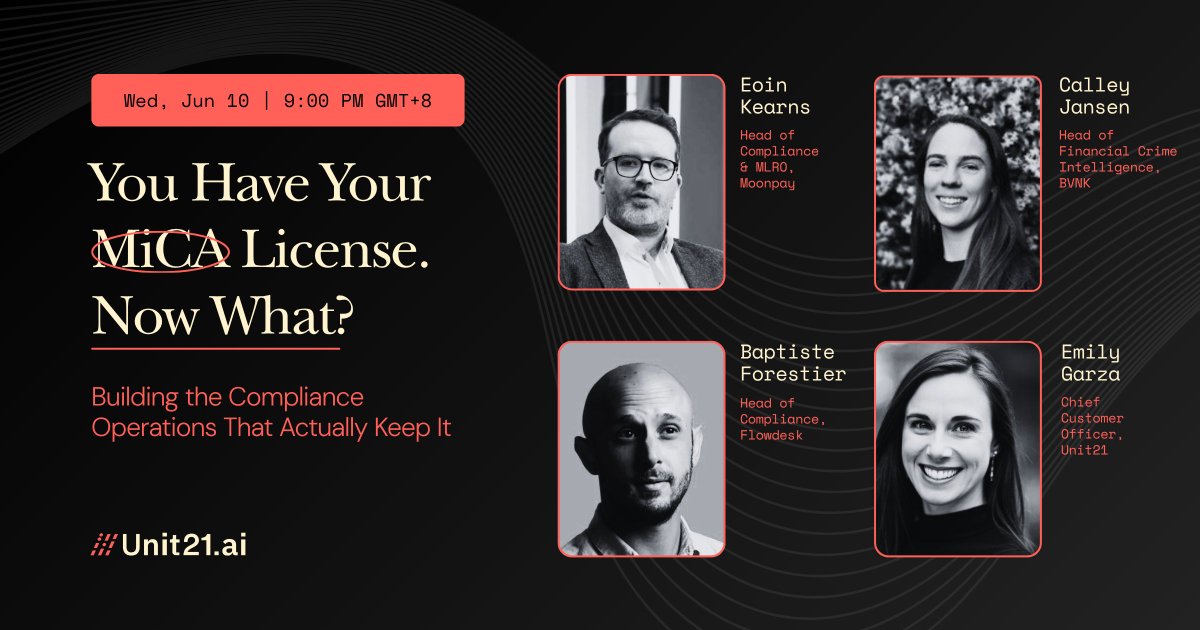

You got your MiCA license. Now the real work starts.

We've found that most MiCA conversations stop at licensing, so we’re bringing together operators from @moonpay, @BVNKFinance, and @flowdesk_co to talk about 𝘄𝗵𝗮𝘁 𝗵𝗮𝗽𝗽𝗲𝗻𝘀 𝗮𝗳𝘁𝗲𝗿 𝗮𝗽𝗽𝗿𝗼𝘃𝗮𝗹.

This will be a practical conversation about what teams are seeing on the ground, what’s changing under MiCA, and where companies are still getting stuck.

👉 Register here: https://t.co/vSAlCSRT7C