Seeing is understanding.

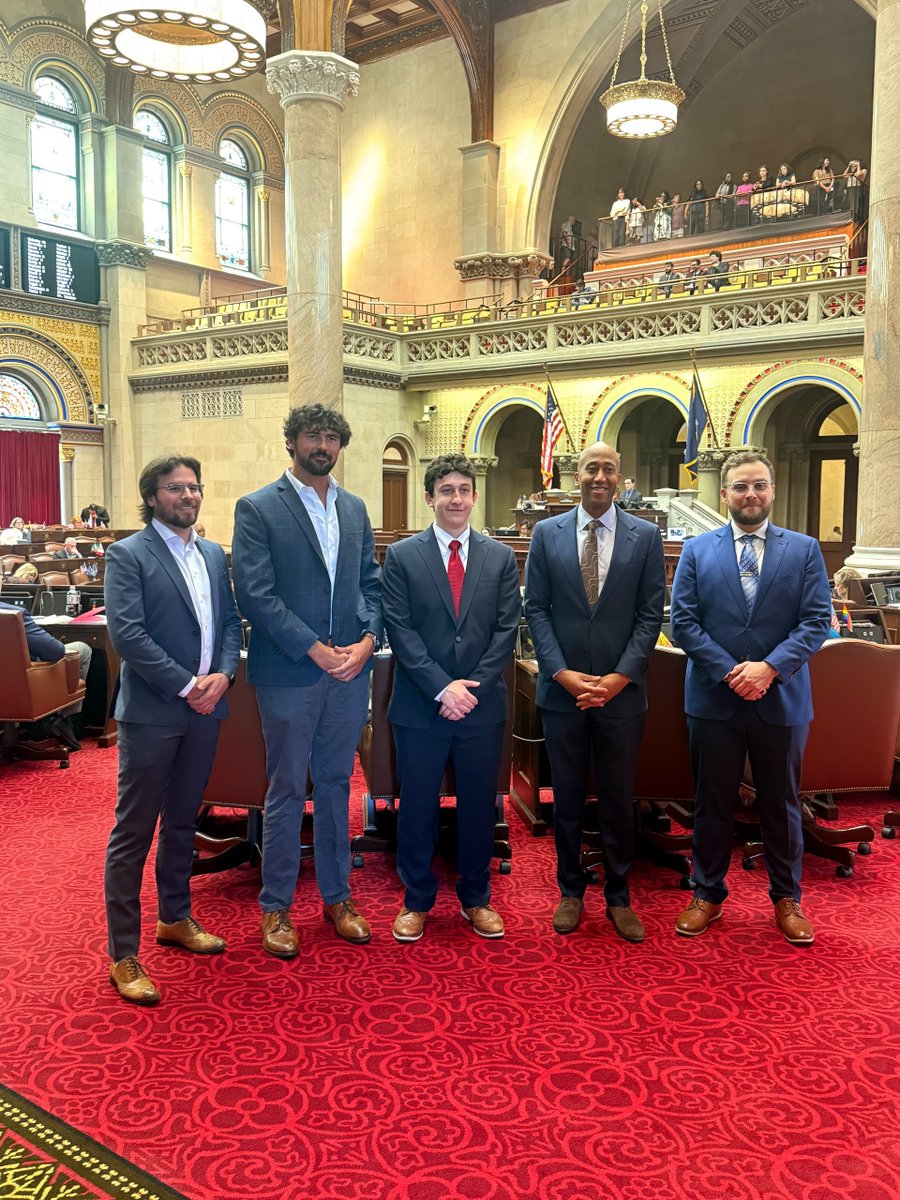

Last week with @DigitalChamber & @SpruceID, we demonstrated real-world blockchain & digital identity use cases for NY State Assembly Members & staff.

Practical applications, tangible outcomes & IRL conversations is how we push blockchain forward.

Because I didn't fork anything.

BTC changed the protocol. BSV restored and preserved the original rules.

Starting a new chain with a new genesis block would have created a different system, not Bitcoin.

The entire point was continuity of the existing ledger, existing transactions, existing ownership records, and the protocol as originally designed.

If you create a new genesis block, you are creating a new asset.

Bitcoin was already running. The objective was not to invent a replacement. It was to keep the original system operating under the original rules.

The real fork occurred when others changed the protocol. Preserving the protocol is not a fork. Changing it is.

There is a peculiar habit of mankind to imagine that prices are causes. They are not. Prices are symptoms. They are the fever, not the disease. A thermometer does not create an infection by reporting it, and a market does not create reality by pricing it.

So when BTC drifts downward over six long months toward forty thousand dollars, the interesting question is not what the number is. The interesting question is why the number remains there long enough for belief to become doubt and for doubt to become arithmetic.

The first month is denial. It always is. Every great speculation begins with a story and ends with a spreadsheet. In the beginning, every decline is explained away as temporary. The true believer sees opportunity. The promoter sees a sale. The leveraged investor sees a buying chance. Everyone imagines that history has paused for them personally and that the market will soon resume its duty of making them rich.

But markets possess no such duty. Reality has a vulgar tendency to arrive uninvited.

The second month is where the first cracks appear. Not in price, but in narrative. The distinction is important. A falling price hurts. A failing narrative terrifies. Investors can tolerate losses more easily than uncertainty. Losses can be explained. Uncertainty threatens identity.

The holders who spent years proclaiming inevitability suddenly find themselves discussing timing. The men who spoke of destiny begin speaking of patience. The language changes because the facts have changed.

The market is beginning to ask a forbidden question.

What if the rise was not permanent?

By the third month the problem is no longer the retail participant. Retail participants are economically insignificant in systemic terms. They are passengers, not engines. The problem becomes institutions.

Institutions do not think in terms of conviction. They think in terms of mandates.

An individual may hold through a collapse out of stubbornness, hope, pride, or faith. A pension fund cannot. An ETF cannot. A treasury committee cannot. A lender cannot. They have rules, obligations, covenants, audits, and reporting requirements. They do not possess the luxury of ideology.

And so the market begins its transformation from a speculative system into a balance-sheet system.

This is the moment that matters.

A speculative market can survive almost any valuation. A balance-sheet market cannot survive arithmetic.

The arithmetic is brutal because it is indifferent.

A company holding BTC as a treasury asset can survive a temporary decline. It can even survive a severe decline. What it cannot survive indefinitely is the combination of declining asset values and fixed liabilities.

The liabilities never sleep.

Interest arrives on schedule.

Dividends arrive on schedule.

Payroll arrives on schedule.

Creditors arrive on schedule.

The market may forgive. A lender rarely does.

As the fourth month begins, the distinction between price and collateral starts to dominate events.

This is where most commentary fails.

People speak of value. Markets under stress speak of collateral.

An asset worth sixty thousand dollars yesterday and forty thousand dollars today has not merely lost value. It has lost borrowing power.

That loss spreads through the system.

Loans secured against it become riskier.

Haircuts increase.

Margin requirements rise.

Credit lines shrink.

The same quantity of collateral supports less leverage.

The same quantity of leverage therefore requires more collateral.

The process feeds upon itself.

A borrower who must sell does not sell because he dislikes the asset. He sells because mathematics has left him no alternative.

This distinction is everything.

Voluntary sellers seek profit.

Forced sellers seek survival.

The market can absorb the first. The second is dangerous.

By the fifth month the institutions begin to reveal themselves.

Stocks are dumping.

Gold is dumping.

Silver is dumping.

Crypto is dumping.

Bonds are dumping.

Even Oil is dumping.

If everything is dumping, where the hell is money going?

Updated rainbow chart, they forgot that rainbows terminate in the ground ($0), also they disappear when you get too close to them, and there’s no golden leprechaun.

Money has no loyalty.

It goes where it expects to be rewarded.

If BTC remains weak long enough, the institutional question becomes unavoidable:

Why hold this asset instead of something productive?

That is the question that drives redemptions.

And once redemptions become persistent, the ETF ceases to be a source of demand and becomes a source of supply.

That is the transition that matters.

Not the fall to $40,000.

The six months spent there.

"Election Fraud, Korean Style"

In Jamsil, Korea, only half of the ballots needed were sent to the local polling station. The locals rose up, and refused to release the cast ballots until everyone was given their chance to vote. (I spoke at the large rally/demostration/blockade held there last evening.)

This morning, the police arrived, penetrated the crowd, and retrieved the TWO ballot barrels. A short while later, FOUR ballot barrels were delivered to the central counting facility.

Nothing to see here, folks. Move along...

A 21yr old man was injured during the extraction, and is now in a coma.

BREAKING: Michael Saylor is down nearly $11 billion on Bitcoin, making him the largest loser in the entire market.

In 2000, Saylor lost -99% of his wealth after betting heavily on dot-com bubble stocks and was ranked the #1 biggest loser of the crash.

History is repeating itself. Exactly as I said it would years ago.

"There was a vulnerability in $ZEC that could be exploited for unlimited issuance since 2022.

If you knew about this vulnerability and used Opus 4.8 to exploit it, you could hack it and issue unlimited coins (of course, from the perspective of professional developers).

However, the problem is that we have no way of knowing whether anyone took advantage of this vulnerability from 2022 until it was fixed just two days ago.

Due to the nature of the privacy chain, we will never know for sure.

In other words, even if Lazarus hacked Zcash and cashed out a large amount of coins, we would never know about it."

It's likely game over for Zcash. See you at $30 like every cycle.