Most NRIs investing in India ask "which fund should I buy?" before they've asked where they're tax resident. That sequencing error causes real, expensive tax problems.

We've looked at the major things NRIs and OCIs don't think about before investing in India: tax residency (and why your Indian passport has nothing to do with it), which investment instrument is most tax efficient as per your current tax-residency jurisdiction, and what getting that wrong actually costs in practice.

The structure around your Indian investment often matters more than the investment itself.

If you have Indian money to invest, or have Indian money already invested, this piece by @avijeet_sen worth a read.

https://t.co/57HJKBZpVg

I've got an agent in a loop optimizing a renderer with the goal to minimize frame times (and tests to measure). It got times down from 88ms to 2ms and allocations down from ~150K to 500. Sounds good, right? Wrong. This is exactly why agent psychosis is a big fucking problem.

As an experiment, I rewrote the Ghostty core render state in Go, with access to identically laid out data structures as Ghostty and the exact same validation tests. I made a purposely naive renderer (simple, correct, but slow). 88ms per frame with 150,000 allocations (horrendous, lol)!

I then kickstarted a Ralph loop to bring the frame times down. I told it it can't modify input data structures or the public API or tests (they're correct), but it can do anything else it wants. It got to work.

It has worked for about 4 hours. I've spent around $350 on this experiment so far. The results?

88ms => 1.5ms

150K allocs => ~500 allocs

Incredible right? Nope.

My hand-written renderer I ported has frame times (same benchmark) of ~20us (0.020ms) and 0 allocations in the update path.

This is the problem with psychosis and lacking systems understanding. If you don't understand the system, you're going to accept that this is an incredible result. If you understand the system, you'll see better solutions immediately and can do roughly 75x better on throughput.

The people who blindly trust agent output are in the former camp. They're sheeple, overdrinking from a fountain of mediocrity.

Standard disclaimer: I use AI all the time. I like AI. The point I'm making is to not blindly accept results. Think. Analyze. Learn.

Why you shouldn't write like AI

Because it's shit writing. Like absolutely bland. It's not this, it's that. Question mark? No, this is the answer. It's like eating, I don't know, sawdust. My apologies to sawdust.

It's late at night and essays that I'm reading have the exact same crappy footprint. I've learnt to live with the long hyphen. It's garish. It's out there telling you that hello, uncle, this is AI, but you know what, it might be interesting anyhow. And I've tried to give it a shot, but somewhere along the line it's like the whole paragraph has been attacked by Dementors and they took all the soul from the written words and it's left with these alphabets that juxtapose just enough to make grammatical sense.

Yes, your actual writing might be terrible. Or you don't have the patience to type endlessly into the ether, like I do, or like I love to do. I just love to write, so maybe I'm possessed with this demon that every piece of writing needs to have a soul. Maybe it's my unnecessary adulation, no, love, for prose. Too much prose, that too. Or to make that spelling mistak so you just know it's human. Hoo-man.

We are all government documents now. Devoid of colour, bereft of whatever bereft means to be bereft of. AI has perhaps made writing easier for a lot of people. And for technical stuff, it's all fine. You're expecting to be bored to the bottom of your stomach, so some outrageous terms, no matter how often they're used, ease the pain a little.

But that opinion piece which needs you to make the words be alive, it sucks when AI renders it into this communist level everyone-must-have-the-same-writing blandness. I don't think I want the extra long words - that is just showing off or winning at scrabble - but I do want a little punch in the sentence. The feeling that you said what you actually felt. The occasional slip, the authenticity. Maybe it's just me, but I don't care, this whole tweet is just me anyways.

Whatever it is, I swear, I will be nicer when it's got that hoo-man in it. Even to the nasty trolls, who I will mute with a smile because they wrote it themselves.

You have to give me one late night rant about nothing. I do spend most of the days telling governments and the RBI what to do, so I'll bloody well rant about what I want to read once in a while.

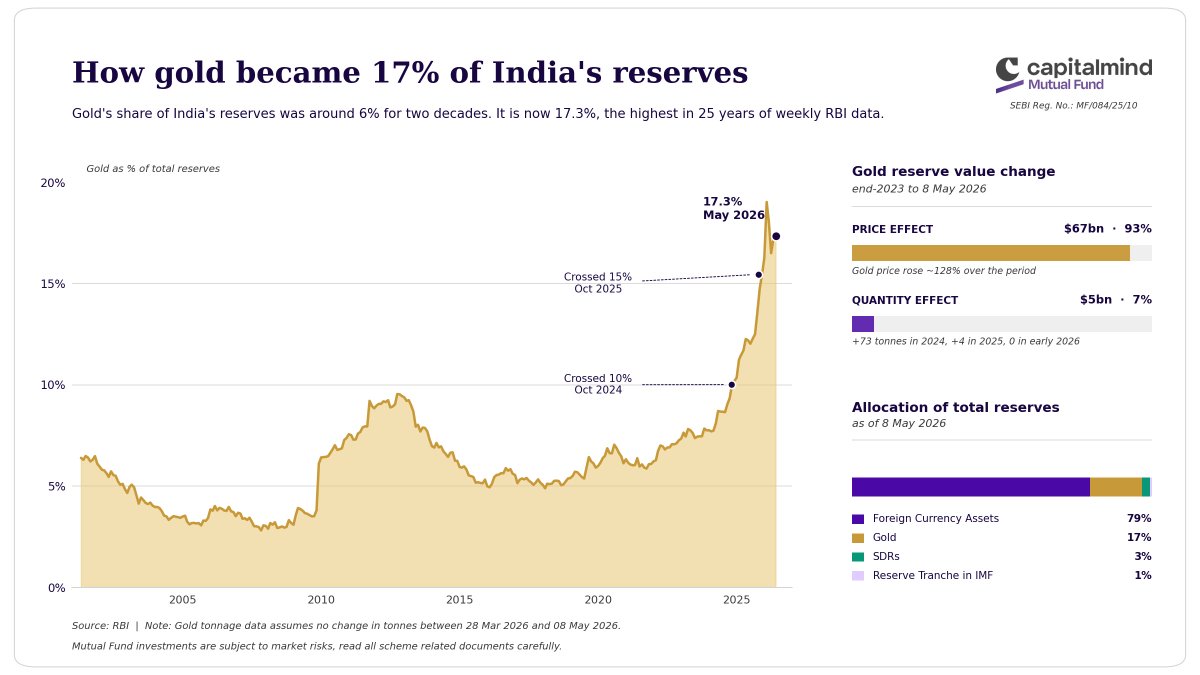

Has RBI been buying gold aggressively?

India's gold reserves just hit a 25-year high at 17.3% of total forex reserves.

Of the $72bn rise in gold's reserve value since end-2023, 93% came from price appreciation and only 7% from buying more gold.

RBI bought only 73 tones in 2024, 4 in 2025, and nothing in 2026.

Watch @CalmInvestor talk about:

- How to build winning portfolios

- The million-dollar question: where is the "value"?

On Air at @CNBCTV18Live

Watch: https://t.co/GsaW9VYY8O

Mutual Fund investments are subject to market risks, read all scheme related documents carefully.

Watch @CalmInvestor on @CNBCTV18News talk about the markets, our funds and more:

- Earnings of the large/mid/smallcaps

- Cynefin 4 situation framework

- How the @CapitamindMF Flexi Cap fund managed cash

- The Multi-asset fund that goes beyond Gold and Silver

- And more!

https://t.co/1S6EcYRh37

Mutual Funds are subject to market risks, read all scheme related documents carefully.

ESOPs are compensation. Hence, it will be taxed as income. That's not the problem. The timing i.e. tax liability arising upon exercise, creates a cashflow problem. A better way would be to shift that liability to the point of sale of the converted shares.

India taxes ESOPs twice...

I've observed this in 2 of my previous companies. Will be paying more tax when the listing happens and will sell it.

I'm all in for paying tax, but this arrogant tax policy should end.

Capitalmind Mutual Fund is now the first AMC to add "Portfolio Changes" summary in their factsheet.

Earlier, I used to manually compare two months portfolio & share the changes.

Now AMC itself is doing it. Great work @deepakshenoy@CalmInvestor@uptickr & team. 👏

More FMs should be doing this; the transparency and clarity regarding the Portfolio changes are a good addition, and more AMCs should follow

Kudos to the team! @deepakshenoy@CalmInvestor

Spotted in the NYC subway. “Zero screen time.” An iPod Shuffle ad in 2026.

When we built the iPod, the goal was the technology disappeared and you could have your music wherever you were. 1,000 songs in your pocket.

Now we’re living through a moment where people are actively looking for ways to disconnect from the infinite feed, algos, and constant notifications. That doesn’t mean technology is bad. It means the best technology understands when to step back.

Not every problem needs another screen, another menu, or another layer of complexity. Constraints create freedom (read: @DavidEpstein new book Inside the Box). And often removing features creates a better product than adding them.

The future of technology shouldn’t just be more engagement. It should help us be more human.

Learnt something last couple of days… appears vast majority of people think a PMS is only and only what you use to manage equity portfolios. World over one of the more prevalent use of PMS is to administer and execute advice for clients. A PMS which can allocate to direct plans of MFs and to REITs, InVITs, Bonds, Index Funds, ETFs et al can be a powerful structure for advisory practitioners. It can manage asset allocation and manager selection decisions with advice embedded in the PMS and a non clumsy formal mechanism of charging advisory fees. The fee might end up higher than direct plans of mutual funds but with advice embedded and it would be lower than regular plans of equity and hybrid funds on a full asset allocation basis.

While DIY investors debate PMS wrapper for MF, the PMSes everyday find more and more people struggling to manage their MF portfolios.

Here's the usual journey of a PMS investor for MF wrappers :

1. Start off like most of us did. Invests in MFs sold by bank RMs or family agents.

2. Someone who is DIY-ing questions regular vs direct.

3. Investor takes some initial help and sets up some investments in Direct MFs.

4. They try to educate themselves, make mistakes and build a portfolio of 20-25 MFs minimum across regular and direct MFs (I have seen 75-80 schemes in one client portfolio).

5. They miss the one-on-one relationship that came with bank RMs or agents. Specially in uncertain markets. In FOMO. In Fear.

6. They find educational material and courses online supporting both passive and active mutual funds.

7. As they learn more, they realise it only gets more nuanced. Not simple.

8. The overwhelm is real. So is self-doubt.

9. They buy, but they never sell.

10. They realise, just like a lot of other things we can do ourselves but we don't, they would rather have someone manage it for them end-to-end. But in direct funds.

11. They understand there are no free lunches and their problem is critical enough to justify a reasonable fee for solving it.

12. In PMS, they invest in Direct mutual funds baskets and everything is delegated - purchase, redemption, SIPs, allocation et al.

13. They gain an advisor relationship who also helps them build a small DIY portfolio on the side, if they prefer, so they can participate in the thrill without making costly mistakes.

14. And lo behold! Contrary to the general commentary, some PMS comes at a fixed fee of 0.5% p.a and no profit share.

Very quickly, here's how most UHNI decision making goes (the wealthy ones with double digit Cr portfolios) :

1. At some point in the past, already decided - I will pay for someone to handle everything that's not my primary business.

2. I want something that doesn't create frequent tax instances.

3. Take the fee and let me use the MF Basket.

4. I am paying for time and mind space. To me, this is building leverage for better use of my time on endeavours that can actually give me outsized returns.

It really is that simple. DIY is not for everyone. PMS is not for DIY investors. PMS is also not for everyone.

While DIY investors debate PMS wrapper for MF, the PMSes everyday find more and more people struggling to manage their MF portfolios.

Here's the usual journey of a PMS investor for MF wrappers :

1. Start off like most of us did. Invests in MFs sold by bank RMs or family agents.

2. Someone who is DIY-ing questions regular vs direct.

3. Investor takes some initial help and sets up some investments in Direct MFs.

4. They try to educate themselves, make mistakes and build a portfolio of 20-25 MFs minimum across regular and direct MFs (I have seen 75-80 schemes in one client portfolio).

5. They miss the one-on-one relationship that came with bank RMs or agents. Specially in uncertain markets. In FOMO. In Fear.

6. They find educational material and courses online supporting both passive and active mutual funds.

7. As they learn more, they realise it only gets more nuanced. Not simple.

8. The overwhelm is real. So is self-doubt.

9. They buy, but they never sell.

10. They realise, just like a lot of other things we can do ourselves but we don't, they would rather have someone manage it for them end-to-end. But in direct funds.

11. They understand there are no free lunches and their problem is critical enough to justify a reasonable fee for solving it.

12. In PMS, they invest in Direct mutual funds baskets and everything is delegated - purchase, redemption, SIPs, allocation et al.

13. They gain an advisor relationship who also helps them build a small DIY portfolio on the side, if they prefer, so they can participate in the thrill without making costly mistakes.

14. And lo behold! Contrary to the general commentary, some PMS comes at a fixed fee of 0.5% p.a and no profit share.

Very quickly, here's how most UHNI decision making goes (the wealthy ones with double digit Cr portfolios) :

1. At some point in the past, already decided - I will pay for someone to handle everything that's not my primary business.

2. I want something that doesn't create frequent tax instances.

3. Take the fee and let me use the MF Basket.

4. I am paying for time and mind space. To me, this is building leverage for better use of my time on endeavours that can actually give me outsized returns.

It really is that simple. DIY is not for everyone. PMS is not for DIY investors. PMS is also not for everyone.

Fair question. A lot of AMCs that also run PMS' do this. @capitalmind_in has one Investment Approach that's a feeder into our Flexi Cap fund - on which the PMS doesn't charge any management fees at all. It was offered because the erstwhile PMS fund manager moved to the AMC to run the Flexi Cap scheme.

Performance fees on top of a mutual fund portfolio - that too without a hurdle - is unusual, to say the least.

It's asking for a profit share for recognising someone else's skill. When the underlying isn't allowed to charge a performance fee, layers on top shouldn't be allowed either.

The pitch reads well. The math underneath does not.

The PMS fee sits on top of the mutual fund expense ratio, not in place of it. All-in: 1.1 to 2%. A direct MF portfolio does the same job at 0.5 to 1%.

Tax pass-through is a feature of mutual funds, not the PMS wrapper. The moment the PMS rebalances between schemes, the demat books a redemption and tax follows.

Profit sharing without a hurdle rate is not alignment. The manager keeps 20% of the upside and bears none of the downside. Investors pay carry for beating zero.

A HNI with 50 lakh can buy 4 to 6 direct funds, pay an RIA a flat fee, and keep most of what the wrapper would have taken. The structure pays the provider better. Not the investor.