Fwiw spoke to someone the other day who pointed out software is typically internally coded for Chinese companies.

Really seemed inconceivable that enterprise will do their own thing before.

But sensing my own cfmation bias to price action for sure

Exponential tech improvements = most SaaS too hard.

Unclear on breadth and depth of impact

Unclear if valuations were just initially stretched

Unclear on HOW narrative will change if mkt is pricing in TV risk.

Probably works to be selective on valuation and AI integration

At Avenir, we’ve followed the emerging bear cases on SaaS closely.

This 46-page deck contains our reflections and research on the path ahead.

We see opportunity and risk as SaaS companies vie with AI natives to be "systems of context."

Link in replies, excited to discuss!

@CurryorNothing agreed that bloat was egregious - but thats changing rather quickly.

understand also that everyone hates management. But not sure why. Yes she seems a little Hollywood and unserious but (listened to her speak on Acquired iirc), but she has made big cuts when needed during covid

$EB is so cheap - negative EV business (due to WC). Business seems so intuitively simple and easy to run - niche platform + network effects etc. Underperformance is really just due to bloat. And it looks like that's changing?

What am I missing?

@CurryorNothing agreed re strategics. in your view what makes product design horrible?

never really used it for “discovery”, but back when i used it i just got a link in the gc.

tried discovery function w recent update and it seems intuitive.

@ClarkSquareCap Yea, but even if you remove US$ 322.8mm of AP, its still a ~170mm EV company on ~300mm on revenue (or 20mm of FY25E Adj. EBITDA, a Low base).

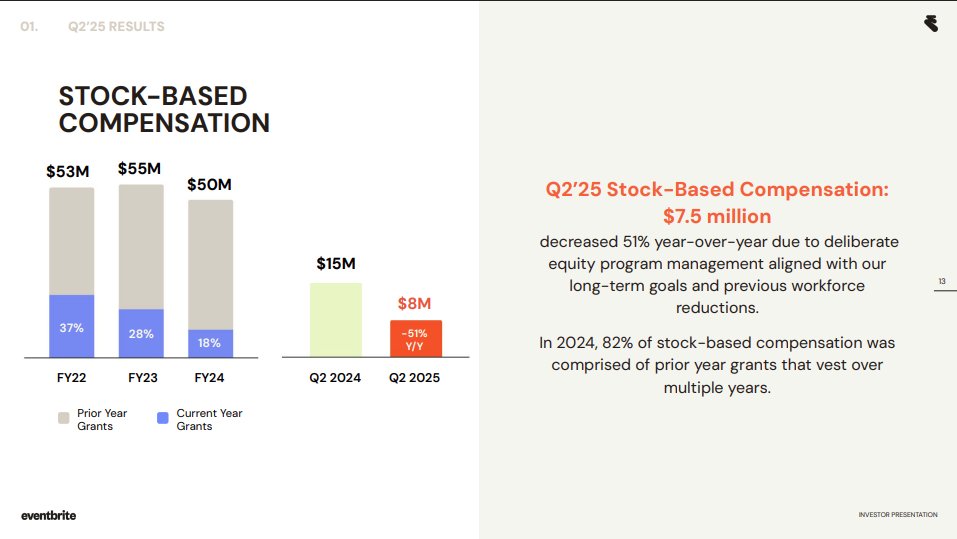

$EB paying down debt w cash flows, SBC is halved, Opex trending down.

Feels like a $GRPN (not the best example haha).

Cost-led inflection to GAAP profitability should move the stock. Yes, founder(s) decision making is a little questionable, but I do trust them to make hard decisions and re cost cuts (see 2020), there is good progress there

Seems like the team is just a lot more profit focused

Used $EB in Europe & Singapore maybe once a month for themed events. Seemed more interesting than just "hitting the club".

Stopped because I just drink a lot less now. Value proposition to both host and guest seems great.

Feel like $WOSG is going to have a negative news cycle for a bit. Getting Dejavu.

HK's Oriental Watch looks more exciting right now. ~40% of market cap is cash, 3x EBIT, 30% payout + large SBB in 2021. Capital return story + recovery call option.

$WOSG, 39% tariff probably won't stick. But this will certainly weigh on sentiment and obfuscate earnings potential further. Timeline pushed out.

At these prices, it's a steal, but I would wait for high-frequency data to improve, similar to 2024.

Still think $BFIT is interesting, but until IFRS profitability materialises even just a little bit, it's tough to have any sort of conviction.

We have been down this road too many times, but it is considerably cheaper now. Gonna wait and watch.

@jenslin_ Yeap, the company has defined it in their ARs. But expert calls quote much higher run rate numbers (closer to ~100K iirc). I think Andrew Walker threw this number out in his pod, referencing gym age

Regardless the name still is worth a look if u assume D&A = m. Capex, which I am

$BFIT is finally looking attractive. I understand it was a 2022 Fintwit / pod favourite, but the ROIC never actually translated to real results.

The "30%+ ROIC" was the regular adjusted BS that every box concept from F&B to Retailers claim to have.

There are great write ups / pods on business breakdowns / YAVB about how attractive the business model is.

Not going to rehash the original thesis that I believe still to be largely true.

P.S. Personally lived in Amsterdam for ~6 months for my semester abroad. My friends and I all made the switch from our bigger, better Uni gym with a sauna etc. to BFIT because we did not want to cycle that extra 5mins during the cold, rainy months.